Reports Of Gold’s Death Are Greatly Exaggerated

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBack in December 1997, the Financial Times ran a now-infamous article titled “Death of Gold.”

In it, the author Kenneth Gooding claimed that as an investment, “gold is a goner.” The crises of the past 10 years—the 1987 stock market crash, the Gulf War, Asia’s financial meltdown—had not resulted in higher demand. Gold was now a “mere metal” and a “bad investment,” Gooding concluded.

But as it happened, reports of gold’s death were greatly exaggerated. The next decade saw the precious metal steadily rise in price, eventually hitting a then-record $1,921 an ounce in August 2011, for an increase of approximately 580% from when the Times published its obituary.

Fast forward to today, and the same gloomy prognoses are being made about the metal. And just as Gooding was proven wrong, today’s doomsayers will end up with egg on their face, I believe.

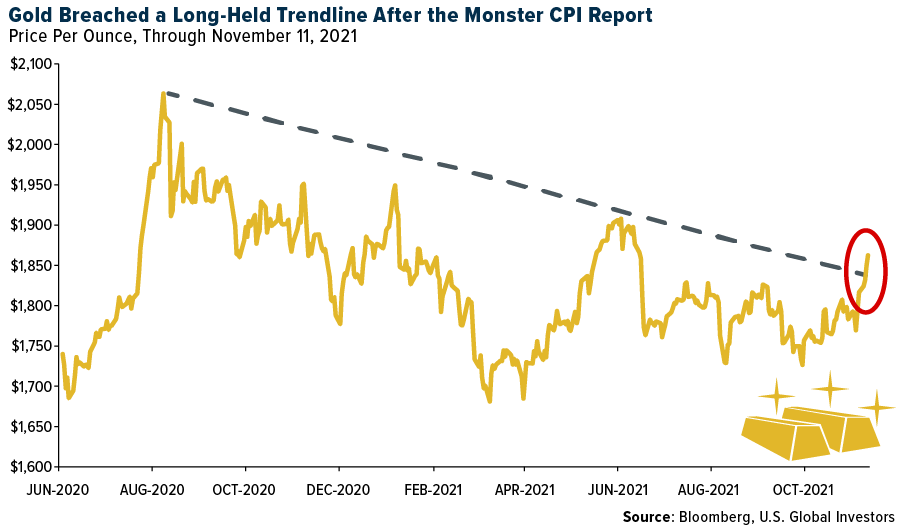

Gold performed as expected this week following a monster consumer price index (CPI) report that showed inflation skyrocketing 6.2% in October compared to last year. After advancing for a seventh straight trading day on Friday, its longest winning streak since May, the yellow metal broke out of its downward trend going back to August 2020, when it hit its all-time high of $2,073.

As I’ve said before, you shouldn’t expect to get rich investing in gold. It’s not Tesla stock or Bitcoin.

Instead, I believe it should be held as a hedge against poor monetary and fiscal policy. This is precisely why nearly every central bank on the planet has gold on its balance sheet.

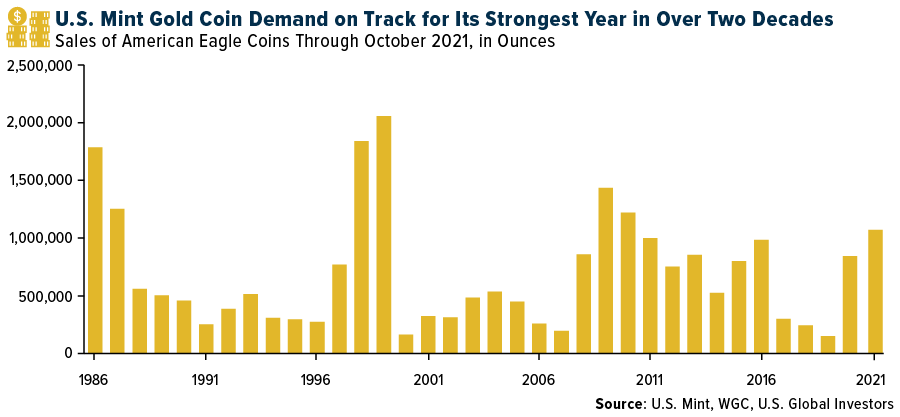

Gold Coin Sales at Highest Level Since 2010

Speaking of balance sheets, the Federal Reserve’s asset purchases continue to rise to unprecedented levels, despite Jerome Powell’s earlier announcement that the bank would begin tapering this month. According to Bloomberg’s Lisa Abramowicz, official holdings now stand at a record $8.58 trillion, or about a third of U.S. gross domestic product (GDP).

This, as well as blistering inflation, must be on the minds of consumers who are gobbling up American Eagle gold coins at a healthy clip this year. According to the World Gold Council (WGC), 2021 coin sales at the U.S. Mint have totaled more than 1 million ounces through the end of October, the greatest amount since 2010. Sales are on track to be the best in over two decades, the WGC says.

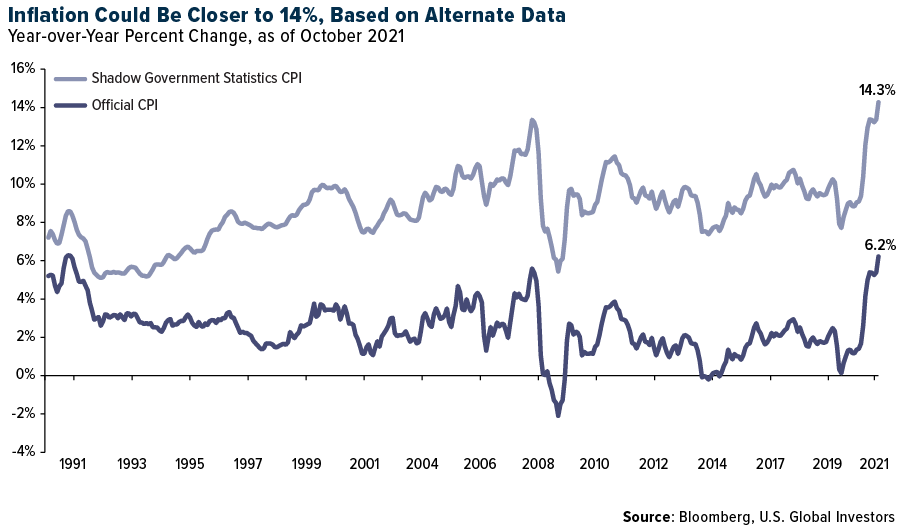

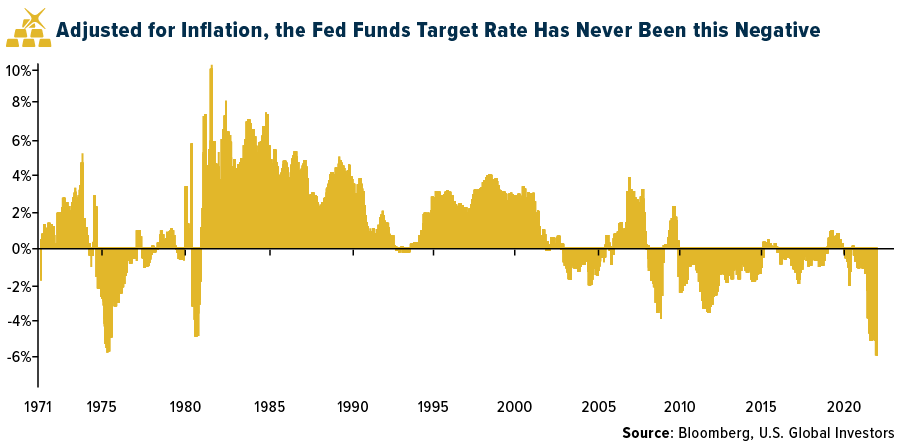

Inflation Likely Much Higher Than Official Reports

For over a year now, I’ve been raising questions about the accuracy of the CPI in measuring inflation. I believe that consumer prices are up much higher than is being reported by the Bureau of Labor Statistics (BLS). Watch my video on the CPI by clicking here, and be sure to share with friends and family.

Let’s consider used vehicle prices. After dipping slightly in July and August, prices increased a whopping 38% year-over-year in October, according to Manheim data. What’s more, this was the first October in Manheim’s data collection, which goes back to 1997, to see a non-seasonally adjusted price increase.

My favorite source of alternate inflation data is Shadow Government Statistics, which is maintained by economist John Williams. On his site, John compares the official CPI to inflation for today as if it were calculated using the methodology from 1980. As you can see, inflation is closer to 14% right now using that methodology, well above the 6.2% being reported.

With inflation at an approximately 30-year high, I believe it’s only rational and wise to have gold in your portfolio. As always, I recommend a 10% weighting, with 5% in bars, coin and 24-karat jewelry, and the other 5% in high-quality gold mining stocks and ETFs. Remember to rebalance once a year or even once a quarter.

Register Now for the HIVE Blockchain Earnings Webcast!

On a final note, HIVE Blockchain Technologies will be hosting a webcast on Tuesday, November 16, at 9:30 a.m. Eastern Time to discuss its financial results for the three and six months ended September 30, 2021.

As Executive Chairman, I’ll be presenting, as will Darcy Daubaras, Chief Financial Officer, and Aydin Kilic, Chief Operating Officer. Special updates will also be provided from Network Media Group and DeFi Technologies.

Index Summary

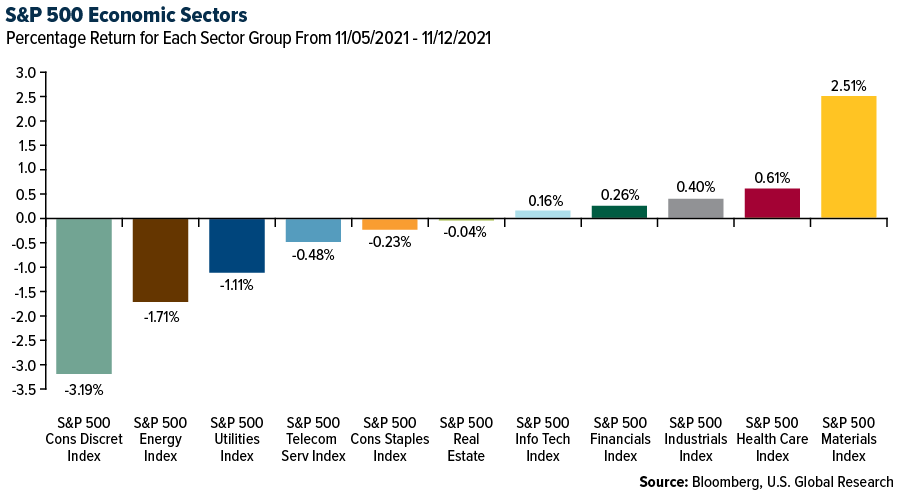

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.63%. The S&P 500 Stock Index fell 0.35%, while the Nasdaq Composite fell 0.69%. The Russell 2000 small capitalization index lost 1.06% this week.

- The Hang Seng Composite gained 2.50% this week, while Taiwan was up 1.28% and the KOSPI fell 0.02%.

- The 10-year Treasury bond yield rose 12 basis points to 1.58%.

Airline Sector

Strengths

- The best performing airline stock for the week was Air China, up 10.2%. System net sales improved for the fifth straight week to -40.9% versus 2019 for the week, versus last week’s level of -43.6%. During prior weeks, the improvement in net sales was driven primarily by better volumes, but this week, better pricing drove system net sales to its best level since the pandemic started (prior best was -41.2% in late June/early July). Domestic and international ticket pricing stepped up to -22.4% versus 2019 (and versus -26.8% last week) and -21.4% versus 2019 (versus -29.3% last week).

- European airline bookings showed a strong improvement in the week, reversing last week’s big decline. The recent volatility in bookings likely reflects the later timing of October school holidays and a departure from seasonal trends. Intra-Europe net sales were up by 11 points to -31% (versus -42% in the prior week) and grew by 12% week-on-week. International net sales increased by 9 points to -45% versus 2019 (and versus -54% in the prior week), up 16%. This led to a 9-point increase in system-wide net sales for flights booked in Europe to -41% (versus -51% in the prior week). Total European bookings are now at their highest level since the beginning of the pandemic, with intra-Europe pricing at 5% above 2019 levels.

- According to Morgan Stanley’s MS FLITE Index, a recovery to near pre-COVID levels in the first quarter of 2022 is possible. The latest forecast of the Forward Leading Indicator Traffic Estimate (FLITE) Index, the group’s proprietary short-term leading indicator of U.S. domestic air travel, predicts a traffic recovery at around 5% below the first quarter of 2019.

Weaknesses

- The worst performing airline stock for the week was Air France, down 9.4%. IAG’s EUR (485) million third quarter 2021 EBIT lagged its European network peers, Air France, and Lufthansa, that reported positive results (in large part reflecting the benefit of dedicated cargo operations). While lifting of restrictions in its network since late summer is likely to result in greater momentum at IAG (than at its peers) heading into 2022, the implied EUR (335) million fourth quarter 2021 EBIT guide was below the prior EUR (255) million estimate on similar capacity.

- According to Credit Suisse, Wizz Air is guiding to a EUR 200 million operating loss for the third quarter 2022, but the group now forecasts a net loss of EUR 440 million for its fiscal year 2022 estimate. Credit Suisse also reduced its fiscal year 2023 estimated net profit by 13% to EUR 461 million, as fuel price pressure and slower vaccination rates reduce optimism.

- GOL Linhas Aereas reported softer-than-expected third quarter results, still deeply impacted by COVID-19. Net revenues were down 50% versus the third quarter of 2019, to 1.9 billion real (ahead the 1.8 billion real consensus), while EBIT came in at a negative 753 million real. The miss was mainly driven by higher personnel costs and maintenance.

Opportunities

- U.S. airlines’ trailing seven-day website visits were up 16% for the week compared to up 10% last week, with all airlines at or above 2019 levels. Delta Air Lines has remained below 2019 levels since mid-June, but this week, its website traffic improved to flat versus 2019 (and versus -2% last week). Spirit Airlines website traffic also finally improved to above 2019 levels (up 4%) after remaining below 2019 levels since its operational issues in early August.

- According to Seaport Partners, the data this week doesn’t cause them to conclude the fourth quarter revenue story has changed materially, but it does begin to strengthen the case for revenue upside, aided by the delta variant subsiding in headline news and business demand snapping back domestically more quickly than they would have anticipated. And it’s a similar story to Europe where demand also has strengthened sharply over the last two weeks following the relaxation of pandemic travel restrictions.

- Last week, Congress passed a $1.25 trillion Bipartisan Infrastructure Deal (Infrastructure Investment and Jobs Act) after months of negotiations. As part of this new infrastructure deal, $25 billion will be invested in airports to address repair and maintenance backlogs, reduce congestion and emissions near ports and airports, and drive electrification and other low-carbon technologies. This investment will help upgrade the nation’s airports and improve U.S. competitiveness. According to some rankings, there are no U.S. airports that rank in the top 25 airports worldwide.

Threats

- According to Credit Suisse, the main threats to Wizz Airlines’ investment case over the next 12 months are likely to include: 1) fuel price exposure given its policy of not hedging fuel, and 2) 50% growth in fiscal year 2023’s fleet versus fiscal year 2020.

- Travel budgets may rebound in 2022 but expectations could fall versus prior surveys. Travel budgets are expected to be down at 50% of 2019 levels in 2021, rising to 78% in 2022. The average fall in budgets expected versus 2019 has increased incrementally from -15.5% in March to -17.5% in July and finally the latest value of -22.0%. The expectation is for an average 29% shift of 2022 travel volumes to virtual, up slightly from July estimates. Virus concerns were the primary reason cited for using virtual meetings. However, cost reduction, use of employee time, and environmental concerns may continue to keep virtual meetings competitive.

- Raymond James held a meeting highlighting some risks at Southwest Airlines. Operational risks at Southwest are likely to remain elevated until the second quarter of 2022, which is when staffing levels are expected to be meaningfully improved while the pilot supply pipeline is building back up. Also, Southwest believes scheduling practices and technology shortcomings have led to a 15% decline in pilot productivity. In addition to reducing pilots’ take-home pay and recruiting competitiveness, Southwest believes this inefficiency is exacerbating operational issues related to building back the network.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 3.5%. The best performing country in Asia this week was Hong Kong, gaining 2.4%.

- The Czech koruna was the best performing currency in emerging Europe this week, gaining 1%. The Thailand baht was the best performing currency in Asia this week, gaining 1.5%.

- Eurozone expectation of economic growth spiked to 25.9 in November from 21.0 in October. The ZEW Germany Expectation of Economic Growth survey increased to 31.7 in November from 22.3 in October, above an expected reading of 20.0, in Europe’s richest nation. The current situation weakened to 12.5 from 21.6 with Europe once again being called the epicenter of Covid-19, but optimism around future growth remains strong.

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 5.1%. The worst performing country in Asia this week was Malaysia, losing 0.3%.

- The Hungarian forint was the worst performing currency in emerging Europe this week, losing 3.2%. The Pakistani rupee was the worst performing currency in Asia this week, losing 3.0%.

- The Chinese Producer Price Index (PPI) hit a record high of 13.5% in October versus the consensus for 12.3%. The prices of oil, coal and steel rebar surged amid a power crunch. Inflation picked up to 1.5% versus the consensus of 1.4%, and 0.7% in September. Core inflation edged higher to 1.3% from 1.2%.

Opportunities

- The press indicated U.S. President Biden and Chinese President Xi are scheduled to hold a virtual summit next week. There is no guidance on what will be on the agenda. However, recent attention was on the reopening of the U.S. consulate in Chengdu and the reopening of the Chinese consulate in Houston. Experts believe the two sides may work toward an agreement to relax restrictions on visas for each other’s journalists.

- This week, China’s heavily indebted property company, Evergrande, made its coupon payments on U.S. dollar bonds, avoiding default again. Beijing may be relaxing restrictions on how developers raise funds. The central bank is considering easing rules to help developers sell assets to avoid future defaults. Also, the rules for developers to issue domestic bonds may be loosened.

- China concluded its largest sales day called Single’s Day this week and companies reported strong revenue. Chinese shoppers spent $139.1 billion this year, breaking last year’s record. Alibaba tallied 540.3 billion yuan ($84.5 billion USD) in spending over the festival that spanned November 1-11, and JD.com reported 349.1 billion yuan ($54.6 billion USD) in transactions this year, from October 31 to November 11. People in China are still not able to travel internationally, however, and domestic travel is restricted in some places due to Covid-19 outbreaks – pushing Chinese citizens to focus on domestic consumption.

Threats

- The border crisis between Poland and Belarus is escalating. Poland estimates that thousands of migrants are gathered near the border trying to enter the EU territory. Poland declared a state of emergency a few weeks ago sending military personnel to the northeast border and, this week, Lithuania declared a state of emergency due to an inflow of illegal travelers. More confrontations may follow as the number of people attempting to escape west from Belarus is increasing and living conditions are harsh with temperatures dropping near freezing in the night.

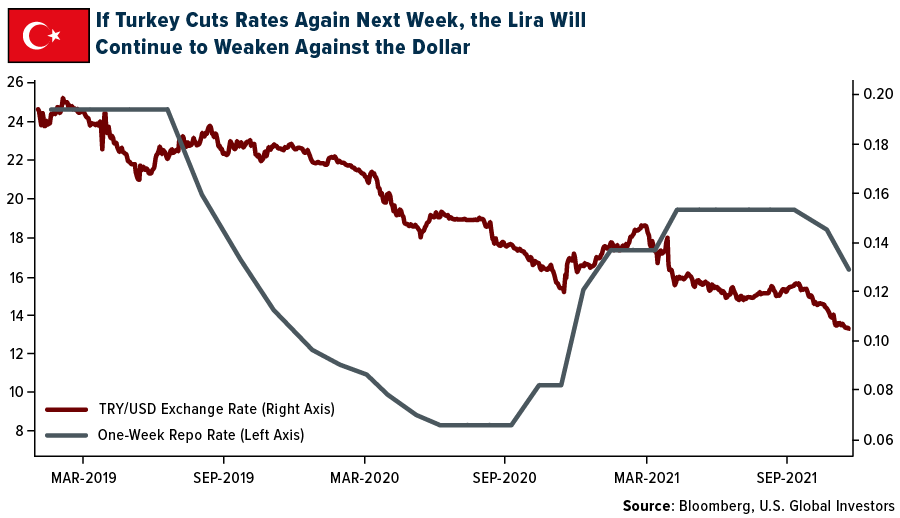

- Next week, the central bank in Turkey will most likely cut its one-week repo rate once again. A lower rate will put more pressure on the currency, depreciating it further against the U.S. dollar. Inflation in Turkey is at 20% and, with high inflation and the depreciating lira, President Erdogan’s popularity is rapidly declining. On a positive note, the weaker lira is pushing exports higher. A decision to decrease or increase rates will be made on November 18.

- Next week, China will likely release weaker sales data and industrial production due to a recent spike in Covid-19 cases and China’s subsequent zero tolerance COVID policy. Bloomberg economists predict retail sales will expend by 3.8% year-over-year in October versus 4.4% in September. The industrial production will possibly be reported at 10.8% in October on year-over-year basis versus 11.8% in the prior month.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was coffee, up 7.53%, on supply woes driving prices higher. Poor weather, shipping delays and soaring fertilizer costs are all acting in tandem to limit current deliveries and future production will be more costly. Fertilizer prices are increasing globally. Russia announced nitrogen export quotas and suppliers appear comfortable holding back and waiting for higher prices. Russia also announced plans to set an export quota on phosphate products. This follows the news of the Chinese shutting off its international export of fertilizer products.

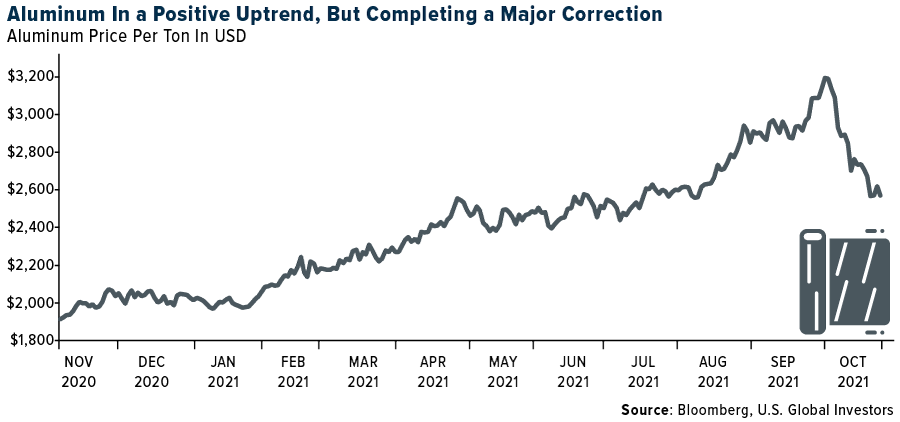

- Aluminum rose in London as Goldman Sachs said the metal was oversold and heading for a deeper global shortfall next year. China’s measures to control energy use and prevent pollution are setting up a tighter market, the bank’s analysts including metals strategist Nicholas Snowdon remarked in an emailed note. Demand will exceed production by 1.5 million tons in 2022, above Goldman’s previous estimate of 959,000 tons, and higher than the 1.4-million-ton deficit expected this year.

- Spare capacity in the oil market will shrink significantly next year as travel rebounds due to a lack of investment among producers, according to Saudi Aramco. Surplus capacity is the equivalent of 3 million to 4 million barrels a day and will drop as demand for jet fuel increases, Chief Executive Officer Amin Nasser stated.

Weaknesses

- The worst performing commodity was natural gas, down 13.14% on it biggest weekly slump since February on higher production and milder weather. Iron ore is having another bad week as the commodity’s poorer fundamentals force a sustained and dramatic repricing. Recent days have brought further signs demand is weakening just as supplies pour out from top producers. Among them: Port Hedland – Australia’s main gateway for iron ore cargoes – reported record loadings for the month of October; ArcelorMittal warned Chinese steel demand will contract this year due to property sector woes; and figures from Friday showed another big rise in stockpiles at major Chinese ports. China’s industrial production data due Monday will likely show another fall in steel output. A drop to the $70/ton range expected in Singapore.

- The price segment for U.S. consumer inflation for electricity in October increased 6.5% from the period a year ago and the biggest jump in a decade. Consumers are seeing higher energy prices across the board as consumers paid 28% more for natural gas from utilities, fuel oil rose 59%, and costs for propane, kerosine and firewood jumped by about 35% as reported by Bloomberg.

- Trafigura Group, the world’s largest copper trader and one of the most vocal bulls, expects Chinese copper demand to be weaker for the next few months – potentially providing relief for the market after available exchange stocks fell to the lowest in decades. Trafigura’s chief economist, Saad Rahim, made the comments on a call with investment bank Jefferies, according to an analyst note.

Opportunities

- Secretary of Commerce, Raimondo, will visit Tokyo on November 15 for the first time. Catherine Dai (Dai Qi), representative of the Office of the United States Trade Representative (USTR), will also visit Japan on the same day. The two sides are expected to discuss issues such as the additional tariffs imposed by the United States on steel and aluminum imported from Japan. Raimondo will visit Singapore on November 16 and 17 and Malaysia on November 18. She said: “Rebuilding the alliance is indispensable for strengthening the international competitiveness of the United States and cooperation will make [the] U.S. economy securer.”

- E&Ps posted a strong finish to earnings season last week: free cash flow set a new shale-era record, topping the already strong levels seen in the second quarter, as capital budgets were largely unchanged despite a sharp rise in commodity prices; many management teams pledged low or no growth in 2022. Importantly, much of the free cash flow is being directed back to shareholders.

- Investor concerns about potential fertilizer demand destruction in 2022 from high prices could be overlooking the potential impact on crop yields from reduced applications and a shift toward less fertilizer-intensive crops. Global fertilizer inventory levels are not just tight, but for many countries are simply unavailable and/or too expensive for small traders. This is set to intensify because of shuttered nitrogen production in E.U. from high gas costs, along with the export bans imposed by China and Russia. While key agricultural countries like Brazil and the U.S. will be able to source near-term fertilizer requirements, many developing countries will be cut short, which could lead to lower crop yields or cause cultivation decreases from grain crops to oilseeds.

Threats

- The largest methane cloud detected in Australia in more than a year was documented last month by satellite imagery over the Bowen Basin in the country’s top producing coal region. With methane being one of the most noxious greenhouse gases and a focus of the recent COP26 climate conference, these methane plumes will attract more attention as they are easily detectable through satellite surveillance. It was estimated the emission rate observed was 76 metric tons of methane per hour. Perhaps regulations would require carbon credits to be purchased to offset this pollution by the coal miners responsible? Australia’s Department of Industry, Science, Energy and Resources (DISER) noted intermittent methane releases are a part of normal operations, but the department is now in the process of implementing a methane accounting system to help track emissions.

- According to Numera Analytics, Brent spot prices are trading above $80/barrel, their highest level since briefly breaking past $85/barrel in late 2018. In Numera’s Global Commodity Outlook, much of the oil ‘bull’ run over the past year reflects a combination of tight supply and improving demand conditions. Since August, however, oil prices have started to detach from market fundamentals, fueled by bullish trader sentiment (as evidenced by a very low put-call ratio on WTI options contracts). Their modeling work reveals that speculative trades explain virtually all increases in prices since August, more than compensating for a stronger U.S. dollar and weakening commodities demand.

- Australia’s liquefied natural gas exporters are unable to keep up with appeals for more supply ahead of winter. Australian LNG exports are already hovering near a record high, according to ship-tracking data compiled by Bloomberg. Australia isn’t alone in being tapped for more supply, as LNG importers seek to stock up on the heating fuel ahead of a potentially frigid winter. Qatar, the world’s top LNG exporter, has also been busy filling extra order requests from buyers including Pakistan and Japan.

Domestic Economy & Equities

Strengths

- Initial jobless claims declined by 4,000 month-over-month to 267,000, and just above the 265,000 estimated. Jobless claims hit a new pandemic low this week. However, continuing claims went up by 59,000 to 2,160,000, and above the 2,051,000 estimated.

- September job openings (JOLTS) were reported at 10,440,000, beating estimates for 10,300,000. The prior month’s JOLTS were revised up to 10,630,000.

- Seagate Technology Holdings, maker of computer hardware, was the best performing S&P 500 stock for the week, increasing 11.7%. Strong demand for personal computers and announced technological advances pushed the stock price to a new a record high.

Weaknesses

- The University of Michigan Consumer Sentiment Index fell to 66.8 from 71.7, below the consensus of 72.5. Both the current conditions and expectations indices fell, dragging the headline index to a 10-year low.

- As expected, inflation increased. October headline CPI was reported at 0.9%, above consensus estimates for 0.5%, and up from September’s 0.4%. Annualized CPI rose 6.2%, above consensus of 5.8%, and the highest since 1990. Core CPI was released at 0.6%, above consensus of 0.4%.

- Tesla, an electric car maker, was the worst performing S&P 500 stock for the week, losing 15.43%. Share price declined on news that the owner of the company, Elon Musk, has been selling shares. Additionally, Tesla’s competitor, Rivian Automotive had an IPO this week. Rivian’s shares surged 66% in the past three days, making it the fifth-largest automaker by market capitalization.

Opportunities

- Press sources indicated U.S. President Biden and Chinese President Xi are scheduled to hold a virtual summit next week. There was no guidance on what will be on the agenda. Recent attention was on a reopening of the U.S. consulate in Chengdu and the Chinese consulate in Houston. Experts believe the two sides may work toward an agreement to relax curbs on visas for each other’s journalists. This meeting may also create opportunity to talk about the U.S.’s large trade deficit with China.

- Bloomberg economists predict that retail sales, due to be released next week, will improve, supported by an improving job market and continued fiscal and monetary support. Retail sales are an important economic indicator because consumer spending drives much of the economy.

- Initial jobless claims will most likely continue to fall next week. Bloomberg estimates that claims will fall to 260,000 from 267,000 this week.

Threats

- The U.S. CPI number jumped 6.2% in October from a year ago. It was the sharpest annual rise for 30 years and way above the U.S. Federal Reserve’s target. Some businesses are warning that supply chain issues and inflation are here to stay for longer than previously expected.

- Bloomberg reported that hospitals in some parts of the U.S. are already starting to see the impact of an autumn wave of COVID-19 infections. Intensive-care unit beds occupied by patients are climbing in 12 states from two weeks earlier. Europe is the epicenter of COVID infections now, but the winter wave may arrive next in the United States.

- U.S. Treasury yields, that are most sensitive to Fed policy changes, have surged this week with 20 basis point jumps in the 5-year Treasury. The week’s big swings have also been exacerbated by a lack of liquidity, which may be at the worst levels since peak pandemic fears in March of 2020, FactSet reported.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Realio Network (RIO), rising a whopping 1,302,638,898%.

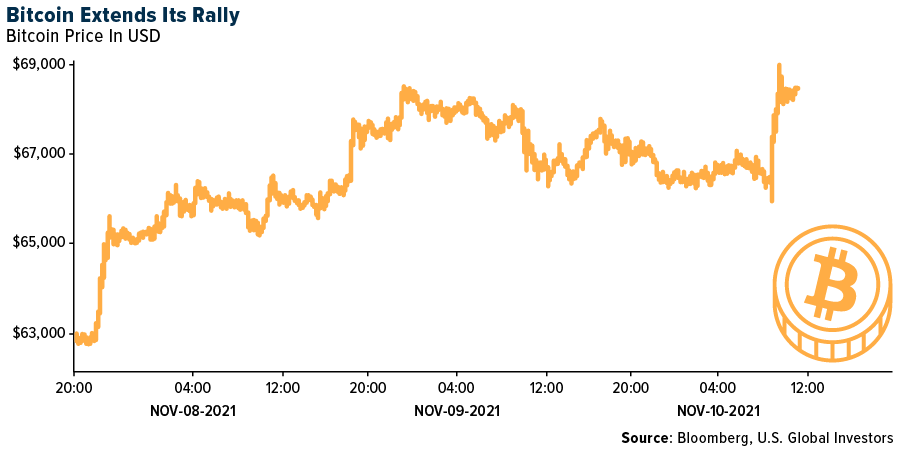

- Bitcoin and Ethereum hit record prices this week amid a broad rally in cryptocurrencies, writes Bloomberg. Some analysts attribute the price surge to investors searching for a hedge against inflation. Bitcoin reached $68,513 while Ether reached $4,840. The total value of digital tokens tracked by CoinGecko reached $3.1 trillion.

- The total value of all cryptocurrency assets has just exceeded $3 trillion, according to Bloomberg. This is a massive number when compared to Apple and Microsoft which each have a market cap of $2.5 trillion. The entire crypto sector is around 20% more valuable than the equity of the two biggest technology companies.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was LevelUp (LVLUP), down 100%.

- Apple CEO Tim Cook has no immediate plans to accept cryptocurrency on Apple Pay, reports Bloomberg, or as a means of tender for its products.

- Coinbase Global Inc. fell as much as 10% on Wednesday, its biggest drop since May, after the firm reported worse-than-expected third-quarter revenue figures, writes Bloomberg. The drop stripped about $2.7 billion in value from the largest U.S cryptocurrency exchange.

Opportunities

- Argo Blockchain filed for a $57.5 million offering of secured notes to fund a Texas mining facility. In an article published by CoinTelegraph, the company explains its intent to use the proceeds for construction costs and rigs at its Texas crypto mining facility. The site would give Argo access to up to 800 MW of electrical power.

- Bitcoin hit another record high this week and is flirting with $69,000 for the first time. The climb comes after inflation data bolstered the argument that the cryptocurrency is a hedge against inflation.

- La Haus, a Latin American property technology startup backed by Bezon Expeditions, said it will accept Bitcoin for real estate transactions. The move adds to the region’s growing adoption of the cryptocurrency as a means of payment, reports Bloomberg.

Threats

- Bitwise is the latest investment firm to tap the brakes on a futures-backed Bitcoin exchange-traded fund (ETF) as expensive roll costs loom large. CEO Matt Hougan tweeted the announcement on Wednesday. This follows a similar move by Invesco, that announced it would not pursue its futures-based ETF, mere hours before the first one launched last month.

- Blackrock’s global head of iShares and index investments said the firm has no current plans to launch cryptocurrency ETFs, reports CoinDesk. The asset manager also said the firm is holding back on launching such products due to the “opaque” regulatory framework and liquidity concerns.

- Regulators have started to question areas like cryptocurrency lending amid concerns about risks for participants and possible spillovers into mainstream finance. Defi’s overall market value was more than $170 billion on Friday, according to tracker CoinGecko, compared with some $22 billion at the start of 2021, writes Bloomberg.

Gold Market

This week spot gold closed the week at $1,864.90, up $46.54 per ounce, or 2.56%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.40%. The S&P/TSX Venture Index came in up 3.91%. The U.S. Trade-Weighted Dollar rose 0.86%.

| Nov-9 | Germany ZEW Survey Expectations | 20.0 | 31.7 | 22.3 |

| Nov-9 | Germany ZEW Survey Current Situation | 18.0 | 12.5 | 21.6 |

| Nov-9 | PPI Final Demand YoY | 8.6% | 8.6% | 8.6% |

| Nov-10 | Germany CPI YoY | 4.5% | 4.5% | 4.5% |

| Nov-10 | Initial Jobless Claims | 260k | 267k | 271k |

| Nov-10 | CPI YoY | 5.9% | 6.2% | 5.4% |

| Nov-14 | China Retail Sales YoY | 3.7% | — | 4.4% |

| Nov-17 | Eurozone CPI Core YoY | 2.1% | — | 2.1% |

| Nov-17 | Housing Starts | 1580k | — | 1555k |

| Nov-18 | Initial Jobless Claims | 260k | — | 267k |

Strengths

- The best performing precious metal for the week was silver, up 4.79% on a broad-based rally across the precious metals space. The latest U.S. producer and consumer price data this week will offer fresh insight on the likely course of Federal Reserve policy. Fed Chair Jerome Powell last week stressed that the start of monetary tapering didn’t mean rate hikes were coming any time soon. “The Fed is behind the curve on inflation as far as the markets are concerned,” refiner Heraeus Metals Germany GmbH & Co. KG. wrote in a note. “Should inflationary pressures remain high, gold could return to favor but, as stock markets keep hitting record highs, it is stuck in its trading range.”

- Newcrest Mining agreed to buy Pretium Resources in a cash and shares deal valuing the Canadian gold producer at about $2.8 billion, adding to a wave of consolidation in the sector. Melbourne-based Newcrest will offer Pretium holders C$18.50 ($14.87) a share, a 23% premium to the target’s closing price Monday in Toronto.

- Shares in Chalice Mining soared 44% this week on the initial release of its maiden resource statement for its nickel, copper, cobalt and platinum deposit at its Gonneville discovery. The resources were found undercover just 70 kilometers from Perth, so there is excellent access to infrastructure. This discovery represents the largest find of nickel sulfide in 21-years according to the Australian Financial Review.

Weaknesses

- The worst performing precious metal for the week was gold, up 2.56%. Jaguar Mining operating production costs of $19.4 million in the third quarter as compared to $14.1 million last year. The increase in operating cost is primarily due to local inflationary pressure on wages, mining materials and plant consumables, higher tons processed and higher secondary development. Cash operating costs increased 36% to $833 per ounce of gold sold as a result of reduced ounces sold and increased production costs.

- The last 12 months have seen a steady rise in inflation, yet gold has largely traded sideways as stock markets make new highs. The precious metal has long been regarded, correctly, as a hedge against inflation and monetary debasement but have only recently responded to the higher-than-expected inflation numbers. However, the gold miners have been in the company worst-performing sectors in the S&P 500.

- Pan American 2021 gold and silver production guidance was reduced by 9% and 8%, respectively, with silver cash cost guidance 14% higher and gold costs unchanged. The revised outlook implies a strong 4Q production rebound (+10% during the quarter).

Opportunities

- Nano One Materials share price sold off 26% this week on news that Johnson Matthey was abandoning its push into battery metals and announced a new chief executive officer. Only back in June Nano One and Johnson Matthey announced a development agreement to help bring down their costs at Johnson Matthey and the share price really didn’t acknowledge much for the deal. For Johnson Matthey to exit battery materials doesn’t really affect Nano One and it is a good entry point to add the stock on the overreaction. The other news was that Nano One was pulling back joint development of a LFP (Lithium Iron Phosphorus) with Pulead in China to bring that technology to a North American production line that is free from China and lowers the carbon footprint. Tesla’s is also focusing on LFP batteries as they are cheaper and safer, but don’t have the acceleration of a lithium-nickel-cobalt battery, likely to still have a roll where that kind of power output is needed.

- The developer of the world’s first standard diamond-investment product is launching a $50 million investment trust to make trading the precious stones more accessible to professional investors, the company said. Diamond Standard Co., a startup working to enable investors to hold diamonds in their portfolios, plans to create the Diamond Standard Trust in January.

- With global inflation pressures rising, the short-term “transitory” outlook for rising cost pressures is giving way to a longer-term, structural increase. As expected, investors are therefore once again looking for ways to diversify their investments and find a hedge against inflation, with gold the traditional beneficiary. Gold prices have started to respond, with the price of the precious metal up 5% since over the past month, and equity valuations outpacing gold’s performance, rising generally 15-20% over the same period.

Threats

- Exchange-traded funds continued to sell, bringing this year’s net sales to 9.11 million ounces, according to data compiled by Bloomberg. Total gold held by ETFs fell 8.5 percent this year to 98 million ounces, the lowest level since May 13, 2020.

- Greenland’s parliament has passed legislation that will ban uranium mining and cease development of the Kuannersuit mine, one of the biggest rare earth deposits in the world. Kuannersuit, owned by Australian mining firm Greenland Minerals and located near the southern town of Narsaq, contains a large deposit of rare earth metals, used to make consumer electronics and weapons, but also radioactive uranium. The law, passed by parliament late on Tuesday, was put forward by the Inuit Ataqatigiit party that came to power in April after campaigning to ban uranium mining and halt the Kuannersuit project, also known as Kvanefjeld..

- Impala Platinum Holdings’s decade-long quest to buy a smaller rival that owns assets key to prolonging the life of its own mines in South Africa came to a shuddering halt on Tuesday. Chief Executive Officer Nico Muller thought he finally had a deal to acquire 100% of Royal Bafokeng Platinum, after gaining the backing of the company’s management and board. Implats, as the miner is known, was preparing to make an offer this week after announcing it was in talks on Oct. 27, according to people familiar with the matter. The company’s fears were realized on Tuesday morning, when Northam Platinum Holdings said it was buying a 32.8% stake in RBPlat, potentially blocking Implats’ at least sixth attempt to acquire the company. RBPlat’s biggest shareholder Royal Bafokeng Holdings — the investment arm of the Bafokeng nation that’s led by King Kgosi Leruo Molotlegi and his advisers — switched sides at the last minute to back a bid for its stake from Northam.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All