Brace Yourself for Higher Prices this Thanksgiving

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOver the past year, inflation has turned up in everything from household items to used cars. Now it’s coming for your turkey and cranberry sauce.

Thanksgiving is next week for Americans, and as I’m sure you’ve noticed, prices are way up. The average cost of a typical holiday feast has increased 14% compared to Thanksgiving last year, according to the American Farm Bureau Federation’s (AFBF) annual survey. The price of the turkey alone is up 24%, which is nearly four times the official inflation rate as reported by the Bureau of Labor Statistics (BLS).

Higher fuel costs will certainly be felt during this year’s busy holiday travel season. As many as 53.4 million people are expected to hit the roads and take to the skies next week, according to the American Automobile Association (AAA). That’s within 5% of pre-pandemic 2019 levels.

Looking just at U.S. commercial air travel, some 4.2 million people are forecast to fly this Thanksgiving.

That would be close to double the traffic from last year and a decrease of around 9% from 2019. Indeed, air traffic numbers, although improving slightly, still lag 2019 levels as business travel has yet to fully recover compared to leisure.

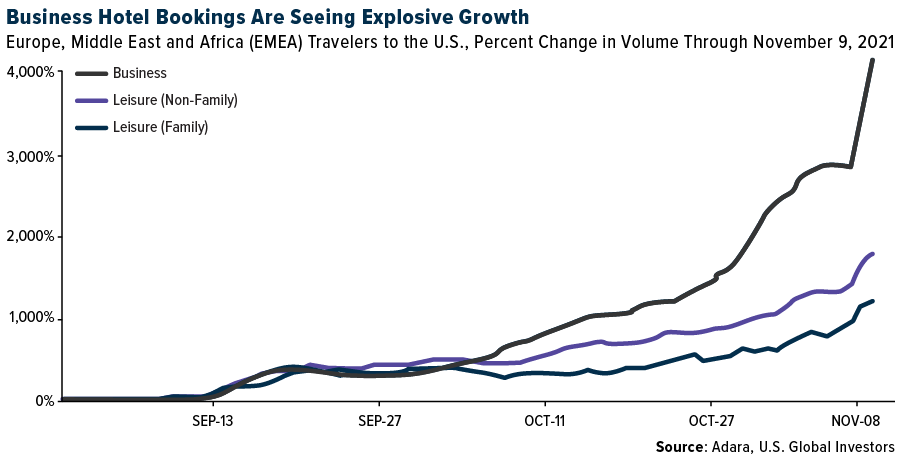

Business-Related Hotel Bookings Up More Than 4,000% Since September

However, the tide appears to be turning rapidly thanks to the decision to lift travel restrictions on vaccinated travelers entering the U.S. from Europe and elsewhere. According to data analytics firm Adara, hotel bookings in the U.S. for business purposes are skyrocketing among travelers from Europe, the Middle East and Africa (EMEA). Since September 1, such bookings are up more than 4,000%, well ahead of bookings for leisure purposes and visiting family in the U.S.

You can see how demand for business-related hotel stays exploded on November 8, the day when the U.S. officially lifted the travel ban that had been in place since the very beginning of the pandemic.

Sunny U.S. destinations appear to be highly favored by Europeans, according to Adara data. Hotel bookings in Miami are up 5% compared to 2019, while Phoenix is up a whopping 84%. On the leisure side of things, Honolulu is seeing an incredible 139% increase in hotel bookings versus 2019.

It may be obvious to point this out, but I’ll do it anyway: Adara’s data is highly positive not just for hotel chains but also commercial airliners. As I said earlier, air passenger volumes still trail 2019 levels, but I believe we’re finally starting to see significant growth momentum—perhaps the most significant since the start of the pandemic.

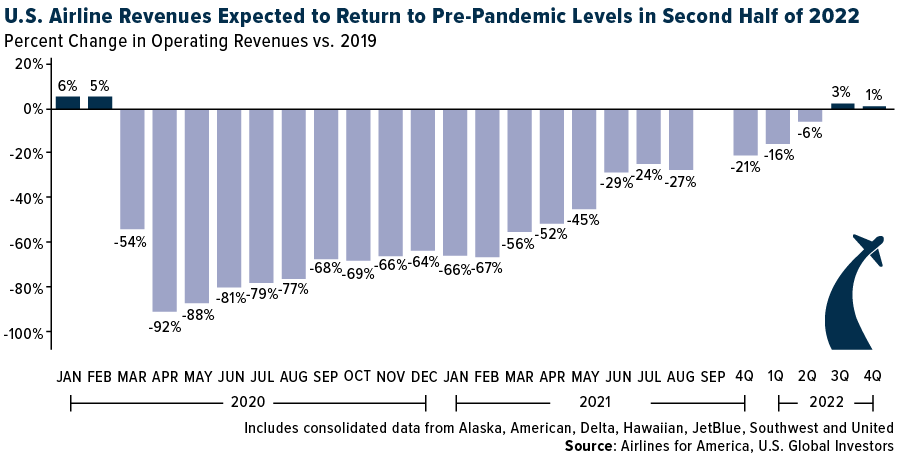

Airline Revenues to Recover by the Second Half of 2022?

I’ve had people ask me when we can expect airline revenues to return to pre-pandemic levels. As always, it’s difficult to make these sorts of predictions, but from what I’ve seen, the most plausible estimate comes from Airlines for America (A4A).

According to its most recent report, the U.S. trade group believes airline revenues could fully recover to 2019 levels by the second half of next year. This is based largely on monthly sales data from the seven largest U.S. carriers. By the September quarter of 2022, ticket sales could be 3% above pre-pandemic levels.

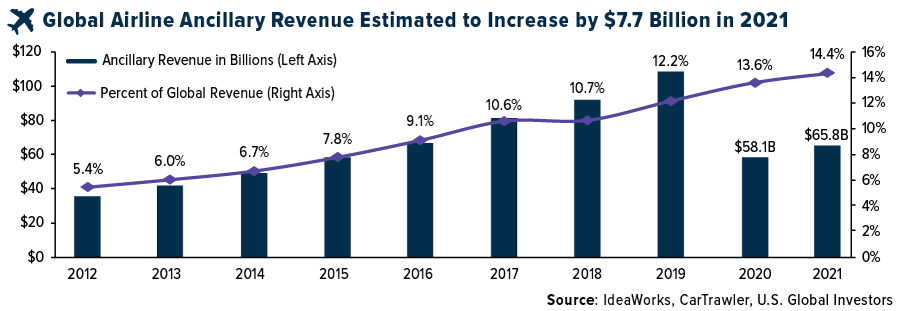

In the meantime, airlines continue to offset still-recovering ticket sales, not to mention higher fuel costs, with ancillary revenues. These include sales of services that go beyond simply transporting someone from A to B. Think frequent flyer programs, credit card applications, hotel bookings, extra legroom and the like.

(Speaking of which, United Airlines announced this week—just in time for some holiday cheer—that it would resume hard liquor sales on domestic flights for the first time in over a year, making American Airlines and Southwest Airlines the only major carriers with a blanket ban on alcohol in economy class.)

As you might expect, ancillary revenues dipped dramatically in 2020, but like the airlines industry as a whole, sales appear to be ticked up this year. According to IdeaWorks and CarTrawler, global ancillary fees increased to $65.8 billion in 2021, or $7.7 billion more than last year.

Although ancillary revenues are still below 2019 levels, they today represent a larger share of total airline revenues than they did two years ago. In 2021, these fees represent an estimated 14.4% of total revenues, compared to 12.2% in 2019. A decade ago, they represented only 5.4% of global sales, underscoring just how important this revenue stream has become and will continue to be.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 1.38%. The S&P 500 Stock Index rose 0.28%, while the Nasdaq Composite climbed 1.24%. The Russell 2000 small capitalization index lost 2.88% this week.

- The Hang Seng Composite lost 0.32% this week; while Taiwan was up 1.71% and the KOSPI rose 0.07%.

- The 10-year Treasury bond yield fell 2 basis points to 1.537%.

Airline Sector

Strengths

- The best performing airline stock for the week was Air Berlin, up 8%. Copa Airlines released third quarter better-than-expected results with operating income of $49 million, beating the consensus estimates of $12 million profit. Copa managed to beat their own revenue guidance ($445 million versus $415 million) and posted a lower CASM ex-fuel than expected (6.2 cents versus 6.6 cents).

- System net sales improved for the sixth straight week to down 37.9% versus 2019 levels for the week versus last week’s level of -40.9%. Domestic tickets booked through large corporate channels improved slightly this week to down 44.8% (versus -46.6% last week), while bookings through smaller agencies were flat sequentially at -18.7%. International tickets sold were down 32.3% this week but have improved from down 48.8% since the U.S. relaxed travel restrictions.

- U.S. airlines’ trailing seven-day website visits were up 20% for the week compared to 16% last week, with all airlines above 2019 levels. Every U.S. carrier remains above 2019 levels this week as website data continues to improve in recent weeks.

Weaknesses

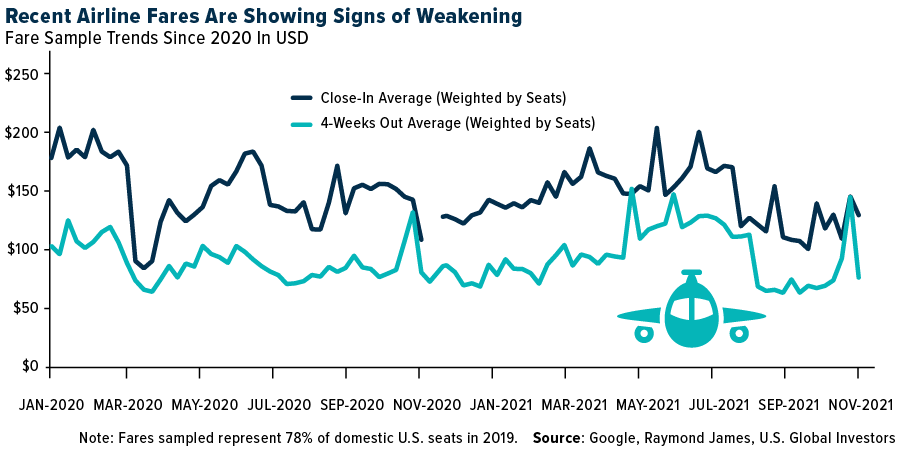

- The worst performing airline stock for the week was Jet2 PLC, down 14.5%. Overall fare trends surveyed this week were down as average close-in (one-week out) fares declined 11.1% this week, albeit against a tough comparison of 33.4% weekly gain in fares last week. The leisure (four-week out) fares dropped 47.5% this week, nearly giving away last week’s positive fare momentum of 56.8%, as four-week out fares are now lapping the Thanksgiving holiday weekend.

- European airline bookings declined in the week, with a sharp fall in the intra-Europe party offset by steady international net sales. Intra-Europe weekly booking trends have been quite volatile over the past month. This is due to the timing of school holidays as well as a continued short booking curve leading to softer bookings before the Christmas holiday. Intra-Europe net sales were down by 11 points to -42% versus 2019 levels (versus -31% in the prior week) and declined by 10% this week.

- Only 40% of Chinese respondents expect their travel to be significantly reduced relative to pre-COVID levels once things return to normal, which is one of the highest levels of disruption globally. China domestic travel is trending at pre-COVID levels when there are no travel restrictions but risks to the downside might be to international travel.

Opportunities

- Frontier Airlines announced a major fleet expansion with an order for 91 additional A321neo aircrafts from Airbus, which will triple the size of the airline by 2029. The new aircrafts are scheduled to be delivered between 2023 and 2029, and they are in addition to their existing order book of 143 aircrafts that are expected to be delivered between 2022 and 2028. Frontier’s total fleet size by the end of 2029 is expected to be 272 aircrafts, which is 143% larger than the carrier’s current fleet of 112 aircrafts.

- Wizz Air has ordered 102 A321s including 75 A321neos and 27 A321XLRs, with most to be delivered over 2025 and 2027. Wizz may acquire another 19 A321neos under certain circumstances, and it has taken 75 A321neo purchase rights for 2028-2029 deliveries, which can be converted into firm orders by the end of 2022. Wizz emphasized its plan for 500 aircrafts by 2030, to be determined by the second quarter of 2022.

- According to Bank of America, bookings across the U.S. and Europe are improving following the COVID-19 delta variant outbreak over the summer. 27% of global business travelers have already started to travel, and 46% now expect to be on the road in 2022 or beyond. U.S. business travelers appear eager to get back on the road, with 29% responding they expect to take their next trip in the fourth quarter of 2021 and another 23% in first half of 2022.

Threats

- According to Bank of America, in the 44th edition of the Aviation Nowcast, the data shows Chinese domestic traffic fell to 38% of 2019 levels in the first half of November, on par with the decline seen in the first half of August. Beijing saw the largest decline in domestic traffic, due to strict travel restrictions which hurt Air China and Beijing Capital Airport. Recent COVID cases in China and the daily number of flights have both improved.

- Schedules generally look locked in for November and December, with both months showing total flights/capacity 13% below 2019. Going into the new year, there is a 5% reduction in capacity for January through February and a smaller 1% cut in March with American Air being the main driver as it cut schedules by nearly 20% for January through February of 2022.

- With encouraging reopening trends in Brazil heading into the Southern Hemisphere summer, GOL Airlines expects revenue to improve from -48% versus 2019 in the third quarter to -30% in the fourth quarter. However, this is below prior forecasts, due to still depressed corporate demand in the Sao Paulo-Rio-Brasilia triangle where GOL has the greatest exposure.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 6.03%. The best performing country in Asia this week was Taiwan, gaining 1.85%.

- The Russian ruble was the best relative performing currency in emerging Europe this week, losing 0.93%. The Pakistani rupee was the best performing currency in Asia this week, gaining 0.31%.

- China reported stronger economic data this week. Retail sales rose 4.9% year-over-year versus 3.7% expected and 4.4% in September. Industrial production rose 3.5% year-over-year versus 3.0% expected and 3.1% in September

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 5.1%. The worst performing country in Asia this week was the Philippines, losing 2.75%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 11.23%. The Philippine peso was the worst performing currency in Asia this week, losing 1.35%.

- Europe is seeing a spike of COVID-19 cases. Many countries are imposing new restrictions to fight the recent surge in infections. Belgium, which has a 90% vaccination rate, has imposed a four-day work-from-home rule until December 12. The vaccination rate is much higher in Western Europe than Eastern Europe. A sharp spike in COVID-19 cases is being seen in Russia, Poland, the Czech Republic, Slovakia, and Ukraine.

Opportunities

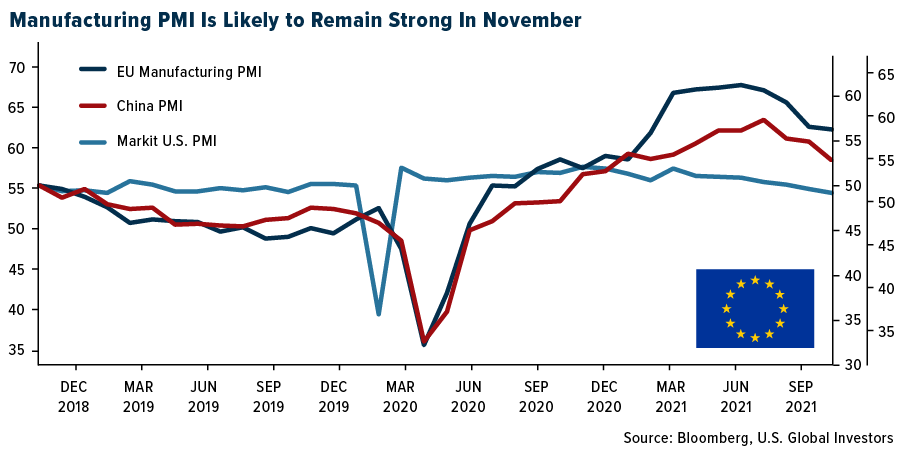

- In October, as the chart below illustrates, Europe reported higher manufacturing activity than the United States and China. The Eurozone will report November’s preliminary PMI data next week and we expect the index to have a strong reading, pointing to robust economic activity despite the recent spike in COVID-19 infections throughout Europe. In addition, the Eurozone service PMI should remain well above the 50 level.

- This week Bloomberg reported that panic is fading in junk bonds in China and signs of stability are emerging in China’s junk bonds. The notes dropped to 20%, down from a high of almost 25%. The sentiment improved after Chinese state media said authorities were likely to loosen curbs for developers to sell yuan bonds. On Monday, the central bank rolled over a record 1 trillion yuan ($157 billion) in maturing loans. No developers have defaulted on dollar bonds since October 26.

- China, which has a zero-tolerance policy for COVID-19 infections, may be ready to reopen the border with Hong Kong in December. Travelers will be able to enter mainland China quarantine free. However, the reopening will likely be gradual, with number of people allowed to pass restricted to just a few hundred per day, increasing steadily to a few thousand in the following months.

Threats

- Despite China reporting stronger economic data this week, Brown Brothers Harriman research team believes that the Asian nation’s economy is still in a medium-term slowing trend as policymakers continue their efforts to restructure and reform. The reforms could slow down the country’s growth.

- Geopolitical tensions remain high in Europe because of the Belarus border crisis. The EU approved new sanctions that allow it to target those involved in encouraging the flow of migrants through Belarus to its border with Poland. President Lukashenko has guided thousands of migrants from Iraq, Syria, Afghanistan, and other countries in what the EU has called a “hybrid attack.” Lukashenko has already threatened to block the flow of natural gas supplies from Russia to the EU. Poland has accused Russian President Putin of being behind the border crisis, but he has denied any involvement.

- The Turkish lira reached another record low this week, deprecating 34% year-to-date. It is the world’s worst performing currency year-to-date. On Thursday, the Turkish central bank cut its main rate by 100 basis points despite the country’s inflation remaining around 19%. Further rate cuts cannot not be rolled out.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was spot coal, as measured by the Bloomberg Powder River Basin Coal Index, which jumped 113.19%. U.S. coal prices surged to the highest in more than 12 years, threatening to bloat America’s already soaring electricity bills and signaling that the dirty fuel isn’t getting phased out anytime soon. Prices for coal from Central Appalachia climbed more than $10 last week to $89.75 a ton on the spot market, according to figures released Monday from S&P Global Market Intelligence. That’s the highest since 2009, when a spike in exports boosted domestic prices for the power-plant fuel.

- Ivanhoe Mines raised its annual production guidance for the Kamoa-Kakula copper mine to 92,500-100,000 metric tons after the Phase 1 concentrator ramp-up. The first full quarter of commercial production was 41,545 tons, handing Ivanhoe its first operating profit, the Vancouver-based company said in a statement. Kamoa-Kakula’s cash costs of $1.37 a pound is expected to trend lower as the Phase 2 plant is commissioned. Phase 2 is more than 60% complete and ahead of schedule, with a startup scheduled for the second quarter of 2022 combined, the two phases are forecast to produce about 400,000 tons a year.

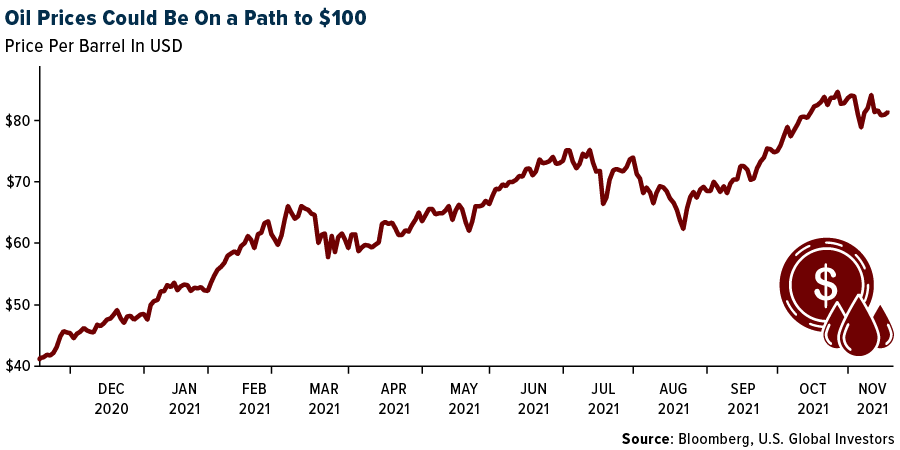

- The oil market is “very, very tight” and $100 a barrel is probably in the cards for the longer term, according to Jeremy Weir, CEO and chairman of energy trading giant Trafigura Group. “There are no freely available barrels,” he said at The Financial Times’ Commodities Asia Summit on Tuesday. Additional supply is needed but it’s uncertain if it will arrive, Weir said. China is releasing some oil from its strategic reserves days after the U.S. invited it to participate in a joint sale, suggesting the world’s two biggest oil consumers are willing to work together to keep a lid on energy costs.

Weaknesses

- The worst performing commodity was lead, down 7.51% for the week on no specific news other than fears of another economic lockdown. Alto Maipo Spa, a subsidiary of AES Corp., filed for bankruptcy in Delaware this week after the hydroelectric plant it constructed high in the Andes Mountains to take advantage of the melting of the annual snowfall, had to cease operations due to a lack of snowfall. In recent years, snowfall in the Andes has become increasingly scarce as global warming has altered historically observed weather patterns.

- Ethane prices struggle to detach from natural gas while awaiting new ethylene cracker demand. With natural gas prices falling 16%, Mt. Belvieu ethane prices declined 8% to $0.396 per gallon, their lowest level since September after peaking in the mid-$0.40 per gallon range in recent weeks. Propane prices have weakened somewhat despite export strength and the approaching winter season. Mt. Belvieu propane prices have hovered around the $1.35 per gallon level, pulling back from recent peaks of $1.50 per gallon.

- Russia’s controversial Nord Stream 2 pipeline faces another delay after Germany suspended a key step in the approval process, sending European gas prices surging as much as 12%. The German energy regulator halted the certification process necessary before the new link from Russia can start, it said in a statement. The suspension will allow time for Nord Stream 2 AG, the operator of the pipeline owned by Gazprom PJSC, to set up a German subsidiary in a bid to meet European Union rules requiring gas producers to be legally separate from entities transporting the fuel.

Opportunities

- According to Morgan Stanley, investors continue to favor fertilizers (and nitrogen, in particular) over seeds and crop chemistry given the velocity of fertilizer prices and the resulting substantial free cash flow generation. Cost curve shifts in nitrogen have attracted the most attention given durability here could transcend the inevitable mean reversion in corn and soybean prices.

- S. natural gas production increased 2.1 billion cubic feet per day (Bcf/day) thus far in November, led by growth in the Haynesville and Permian. According to S&P Global Platts, November domestic production has averaged 93.8 Bcf/day month-to-date (MTD), up from the October average of 91.6 Bcf/day. Production peaked this month at 94.4 Bcf/day, the highest level since January 2020 but 2 Bcf below the record high of 96.4 Bcf/day. The Haynesville (13.9 Bcf/day in November MTD, up from 13.4 Bcf/day in October) and Permian (13.9 Bcf/day in November MTD, up from 13.4 Bcf/day in October) comprise approximately half of this growth, with the Marcellus/Utica another quarter.

- According to Goldman, copper stocks declined another 8% globally, the 20th weekly decline in a row. Cumulative declines of visible copper stocks now total just over 300,000 tons year-to-date, though this masks a steeper 470,000 ton draw from the middle of the year. In turn, this strongly implies that a substantially higher copper price is required to generate a more sustainable fundamental equilibrium.

Threats

- China’s production of crude steel declined by more than 20% from a year earlier, according to data released by the country’s National Bureau of Statistics (NBS). Total crude steel production over the first 10 months of the year was also marginally lower than over the same period in 2020, with a 0.7% drop, the data shows.

- Copper, which spiked to a record high in May, will face another volatile year as a global supply squeeze eases and China’s slowing property market weighs on demand, said BOCI Global Commodities U.K. The copper market is settling down a month after an unprecedented supply squeeze roiled trading. But global inventories are stuck at their lowest level since the financial crisis in 2008, which, together with a worldwide energy shortage, will support copper prices at elevated levels, said Fu Xiao, head of commodities strategy at the unit of the top Chinese bank.

- Saudi Arabia, Russia and the United Arab Emirates signaled that OPEC+ will continue raising oil output cautiously and won’t bow to U.S. pressure to pump faster. U.S. President Joe Biden, concerned that gasoline prices are at a seven-year high, are stoking inflation in America, has called on the 23-nation alliance to turn on the taps and bring down crude prices. OPEC+, led by Saudi Arabia and Russia, is currently increasing daily output by 400,000 barrels a month.

Domestic Economy & Equities

Strengths

- Continuing claims fell 129,000 week-over-week to 2,080,000, beating estimates for 2,130,000, and below the prior revision up from 2,160,00 to 2,209,000. Continuing claims are now back toward the post-pandemic low set-in late October.

- October retail sales increased 1.7% month-over-month versus consensus for a 1.1% rise and September’s upwardly revised 0.8%. This was the third straight monthly increase and the strongest report since March. Year-over-year sales increased 16.3% versus September’s 13.9%.

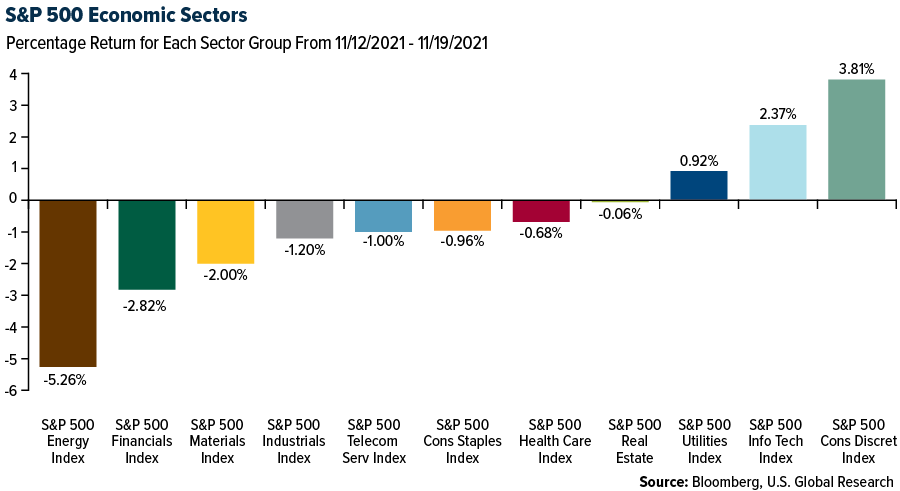

- Dollar Tree, a popular discount store, was the best performing S&P 500 stock for the week, increasing 19.46%. Shares gained 14.3% on Monday on a report that activist investor firm Mantle Ridge built up a $1.8 billion stake in the company. In addition, several brokers upgraded the target price for Dollar Tree this week.

Weaknesses

- Initial jobless claims increased by 1,000 week-over-week to 268,000, missing estimates for 260,000 (prior 267,000). The slight increase broke the six-straight weekly decline in claims, though it still remains near last week’s post-pandemic low.

- Inflation continues to move higher. The import price index increased 1.2% month-over-month in October, above the expected 1.0%. On a year-over-year basis, the import price index increased 10.7%, above the expected 10.3%.

- Apa Corporation, an oil and gas company, was the worst performing S&P 500 stock for the week, losing 12.09%. Shares declined with the price of oil. Brent crude oil declined almost 5%, and prices crossed below the 50-day moving average, closing below $80 per barrel.

Opportunities

- S. President Joe Biden signed his hard-fought $1 trillion infrastructure deal into law on Monday. The bill includes about $550 billion in new spending over 10 years since some of the expenditures in the package were already planned. Next, the government will work on its $1.85 trillion social spending package.

- This week the Philadelphia Fed Index was reported higher in November by 15.2 points moth-over-month, increasing to 39.0 and well ahead of estimates for 24.0. This makes November’s reading the highest point since April’s reading of 50.2, which was a 48-year high. The index measures changes in business growth covering the Pennsylvania, New Jersey, and Delaware regions. When the index is above zero, this indicates factory-sector growth, and when below zero, it indicates contraction.

- Bloomberg economists predict Manufacturing purchasing managers’ index (PMI) data to increase to 59 in the preliminary November reading, from 58.4 a month ago, pointing to strong economic activity. Service PMI is expected to jump higher as well.

Threats

- As per the November Federal Reserve meeting, tapering begins this week. The New York Fed last week released an updated purchase schedule that will result in total purchases worth $105 billion, which is $15 billion less than peak quantitative buying. The Fed plans to reduce its purchases every month by the same amount until June, when QE will have ended.

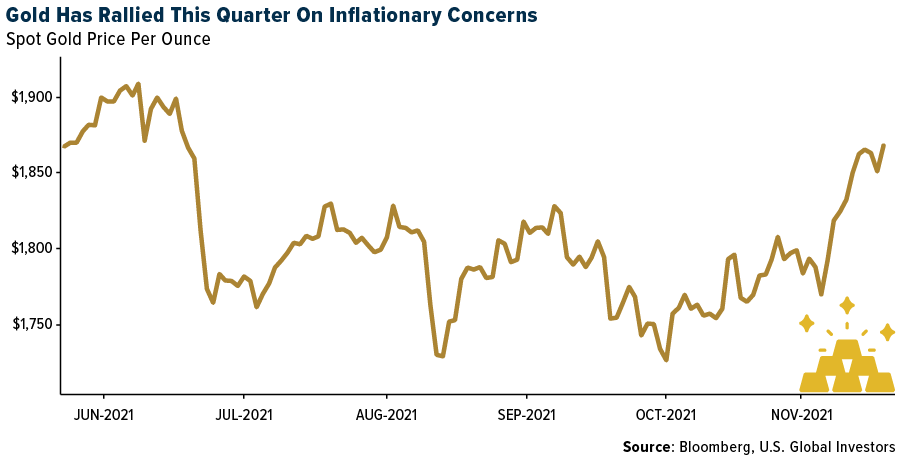

- S. equites keep moving higher, but the focus remains around growing inflation and what this may bring in the future. The price of gold spiked above $1,850 per troy ounce, the highest level in five months as U.S. consumer prices are rising at the fastest rate in three decades.

- The debt ceiling is back in the headlines again. Treasury Secretary Janet Yellen told congressional leaders on Tuesday that the federal government could run out of cash and be forced to default if lawmakers fail to raise the debt ceiling by December 15, reports Reuters.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was GenshinShibInu (GSHIB), rising 79,307.70%.

- JPMorgan Chase and Tiger Global announced investments in blockchain-infrastructure company Blockdaemon Inc., reports Bloomberg, as traditional financial institutions seek a foothold in the burgeoning area of decentralized finance. Blockdaemon already counts Softbank Group and Goldman Sachs Group among existing backers and in September had a value of $1.25 billion, the article continues.

- Almost one-third of North American-based investment offices for ultra-wealthy families are invested in cryptocurrencies. This number compares with 28% of family offices in Europe and 19% in the Asia-Pacific region, according to research published from Campden Wealth and reported by Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Elonomics (ELONOM), down 99.28%.

- In an interview hedge fund manager Kyle Bass, he stated that “from here on out, it’s going to be very difficult to make money on Bitcoin due to intense regulation.” Bass sees tighter rules coming in 2022 from the U.S government, following China’s crackdowns this year.

- According to Mike McGlone, a Bloomberg Intelligence analyst, “Some cleansing of meme coins might pressure the stalwarts as a necessary part of the evolving ecosystem. The sooner the better for the speculation machine coins to experience some purging, so as to move on with the adoption process of crypto assets in investment portfolios.”

Opportunities

- A third Bitcoin futures ETF in the U.S. has just entered the market, reports Bloomberg. VanEck announced that its bitcoin-linked ETF (ticker XBTF) went live on Tuesday, roughly one month after the ProShares Bitcoin Strategy Fund. This comes as the SEC rejected its “physically” backed offering last week, writes Bitcoin Magazine.

- According to a report from CNBC TV India, the nation’s government plans to reclassify cryptocurrency exchanges as “e-commerce” platforms, which will reduce the Goods and Services Taxes users pay per transaction from 18% to 1%, writes CoinTelegraph.

- Cathie Wood of Ark Invest says institutional buys make the bull case for Bitcoin reaching $500,000 by 2026, writes Bloomberg. During an interview with Barron’s Ark stated that if “institutional investors move into Bitcoin and allocate 5% of their portfolios, the value of Bitcoin would rise to around $560,000 by 2026.”

Threats

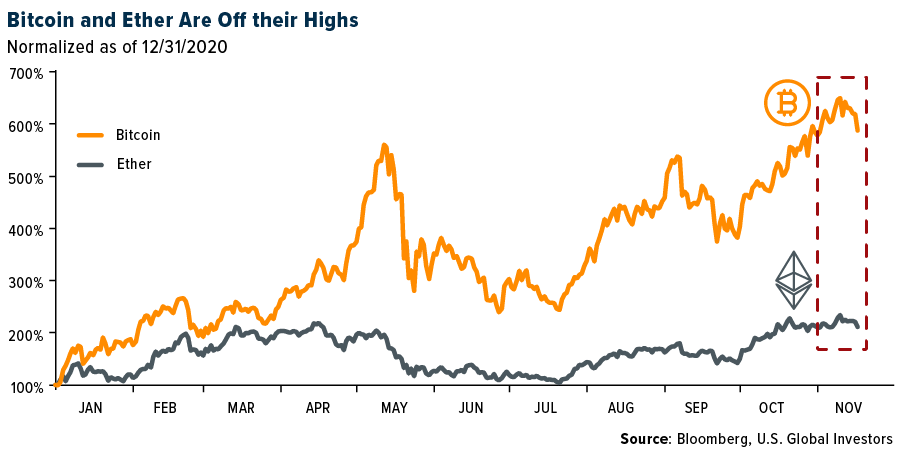

- Cryptocurrencies fell on Tuesday, with Bitcoin briefly dipping below $60,000 and Ethereum touching its lowest level this month. The largest digital token dipped as much as 8.2% to $58,661, the biggest intraday drop since September 24. Second-ranked Ether tumbled more than 10%, writes Bloomberg.

- A bipartisan team of U.S. senators is introducing a bill to narrow some cryptocurrency tax reporting rules. The legislation would address a new tax-reporting requirement for digital currencies included in the infrastructure bill. The law will force cryptocurrency companies to provide information on their users-as- some other financial firms are required to do (in an effort to enforce tax compliance), writes Bloomberg.

- The IRS seized $3.5 billion worth of cryptocurrencies during fiscal year 2021, which is 93% of the assets seized by tax enforcement during the year. Congress recently granted the IRS more ability to survey cryptocurrency transactions in the infrastructure package President Joe Biden signed into law on Monday.

Gold Market

This week spot gold closed the week at $1,845.73, down $19.17 per ounce, or 1.03%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.63%. The S&P/TSX Venture Index came in off 2.72%. The U.S. Trade-Weighted Dollar rose 0.99%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-14 | China Retail Sales YoY | 3.7% | 4.9% | 4.4% |

| Nov-17 | Eurozone CPI Core YoY | 2.1% | 2.0% | 2.10% |

| Nov-17 | Housing Starts | 1,79k | 1,520k | 1,530k |

| Nov-18 | Initial Jobless Claims | 260k | 268k | 269k |

| Nov-24 | Initial Jobless Claims | 261k | — | 268k |

| Nov-24 | GDP Annualized QoQ | 2.2% | — | 2.0% |

| Nov-24 | Durable Goods Orders | 0.2% | — | -0.3% |

| Nov-24 | New Homes Sales | 798k | — | 800k |

| Nov-25 | Hong Kong Exports YoY | — | — | 16.5% |

Strengths

- The best performing precious metal for the week was spot gold, but still down 1.03%. Gold climbed to the highest since June as the dollar weakened ahead of a slate of speeches by Federal Reserve officials and economic data. Bullion is up more than 4% this month, set for its best since May, having broken through key technical barriers after U.S. consumer prices rose the fastest since 1990. The data has sparked growing pressure on the Fed to speed up the pace of monetary tightening amid fears it could lose control of inflation.

- K92 Mining reported third quarter earnings, with cash costs ($596/ounce) significantly below consensus. Although K92 revised 2021 production guidance (production 96-102 thousand ounces) to account for Covid-19 challenges that predominantly impacted the first half of the year, consensus already accounted for such disruptions and is therefore, in line with expectations.

- Regression analysis, using 10-year U.S. real rates, the Bloomberg Dollar Spot index and ETF holdings going back to 2005, has an enviable record in tracing gold prices. Measured monthly over the past decade, the predicted and actual prices have a correlation of 0.7. On Tuesday, gold was $25 below where this model said it should be. In fact, since the U.S. inflation reading on Aug. 11, the metal has outperformed its derived fair value by $148. This suggests sentiment has turned for gold.

Weaknesses

- The worst performing precious metal for the week was platinum, down 4.76%, despite hedge funds staking the largest net-long position in 6-months. Spot gold has climbed since late September, while holdings in bullion-backed exchange-traded funds fell 1.8%. That’s unusual, as flows in this sector are among the biggest drivers of prices. Since the invention of gold ETFs in 2003, holdings have moved in the same direction as price in every year, bar one. This year, they’re close to notching a second divergence. Spot gold has trimmed the year’s losses that at one point tallied more than 10% to just under 2%. Meanwhile ETF holdings plunged 283 tons, or 8.5%.

- Pure Gold reported third quarter sales and earnings with diluted EPS lower than consensus (actual -$0.04 versus consensus -$0.02) largely due to lower revenues generated on the back of lower gold ounces sold versus produced. There were 10% lower gold ounces sold (8.4 thousand ounces) than gold produced (9.2 thousand ounces) while operating costs remained largely in line with consensus.

- Americas Gold & Silver reported earnings per share (EPS) of $(0.13), missing consensus of $(0.09) due to higher construction and maintenance (C&M) and operating costs (primarily at Relief Canyon prior to suspension of operations) as well as higher deprecation.

Opportunities

- On the back of the financing, Arizona Metals has approximately C$56MM in cash ready to allocate to the drill bit. Drilling thus far in 2021 has been threefold: i) increased confidence in the historic 5.8-million-ton Exxon resource, ii) discovering a Zn-Au zone directly adjacent to the historic Exxon resource, and iii) added tonnage at depth. With the new funds, AMC has a fourth rig on order, and is ultimately looking to scale drilling up to six rigs to increase cadence.

- Wheaton Precious Metals will purchase 50% of silver production from Blackwater until 18 million ounces have been delivered, after which the stream will reduce to 33% of silver production over the life of mine. The stream includes a partial buyback option whereby Artemis may purchase up to 33% of the stream by January 1, 2025, or the achievement of commercial production at Blackwater. There is a cash consideration of $141 million payable to Artemis in tranches during the initial construction phase of the project. Wheaton will make payments equivalent to 18% of the spot silver price until their investment has been recovered after which the Wheaton would pay 22% of the spot silver price over the life of mine. Artemis intends to use proceeds from the silver stream to fund construction and development of the Blackwater project.

- Mineros S.A. listed it common shares on the Toronto Stock Exchange in a small $20 million raise. Up till now, their shares were only listed for trading in Colombia where no other mining companies have listed shares, hence it came to the market at a significant valuation discount relative to its peers. For a quarter-million-ounce gold producer that had a strong history of dividends, currently yielding 6.80% and has double-digit returns on invested capital should spark some interest now that it’s a more liquid opportunity.

Threats

- With third quarter earnings now complete for gold producers, a common theme in the results was a discussion on cost inflation. Fuel continues to be the area most cited along with rising pressures on consumables/reagents, with FX headwinds particularly for those with Canadian operations. As well, supply chain logistics continue to be a challenge particularly in Latin America and Africa, where shortages in container shipping capacity and port congestion have impacted sales volumes and procurement. Lastly, larger producers have noted the potential to partly mitigate rising cost impacts via global purchasing strategies and leveraging order consolidation in negotiating/renewing supplier contracts.

- Barclays Plc, Société Générale SA, Scotiabank, and London Gold Market Fixing Ltd. will pay a combined $50 million to end antitrust litigation over an alleged scheme to rig the gold “fix,” a key pricing benchmark, according to a federal court filing in Manhattan. The traders leading the lawsuit sought preliminary approval for the agreement from Judge Valerie E. Caproni, who’s overseeing the multidistrict case. She has tentatively signed off on a $62 million settlement with Deutsche Bank AG and a $42 million deal with HSBC Holdings Plc.

- Gold closed the week on negative note with Fed Vice Chairman Richard Clarida along with Fed Governor Christopher Waller both echoing comments that the Fed needs to look closely at the date leading up to the December’s policy meeting. There is a push to quicken the pace of reducing asset purchases and raise interest rates to quell inflation.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All