Three Charts I’m Thankful for This Week

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsI hope everyone reading this had a wonderful Thanksgiving full of family, love and laughter. Even if that wasn’t your experience, there’s still much to be grateful for. Below are three charts for which I happen to be most thankful this week.

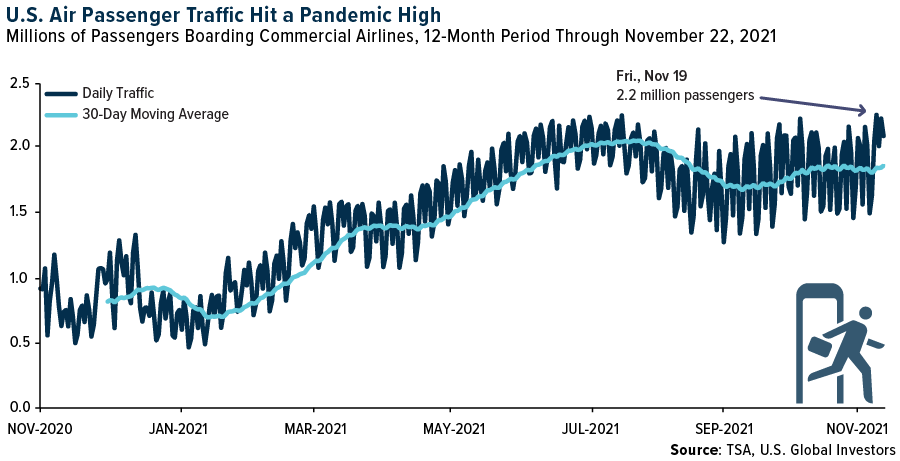

1. Americans appear to be flying again.

The U.S. hit a new pandemic high last week in terms of commercial air traffic. More than 2.2. million people boarded passenger jets last Friday, November 19, according to Transportation Security Administration (TSA) data. That’s the most in a single day since February of 2020, and it’s off by only 12% compared to the same day in 2019.

Anticipating strong holiday-related travel, U.S. carriers have been scrambling to staff up, offering premium pay and hefty signing bonuses to attract new talent. International travel from Europe has also been encouraging, despite a recent surge in Covid-19 cases.

Speaking to Barron’s, Cowen airlines analyst Helane Becker said she believes “summer 2022 will see a strong return on international travel, likely back to at least 2019 levels.” This forecast squares with that of Airlines for America (A4A), which expects U.S. airline revenues to return to pre-pandemic levels in the second half of next year.

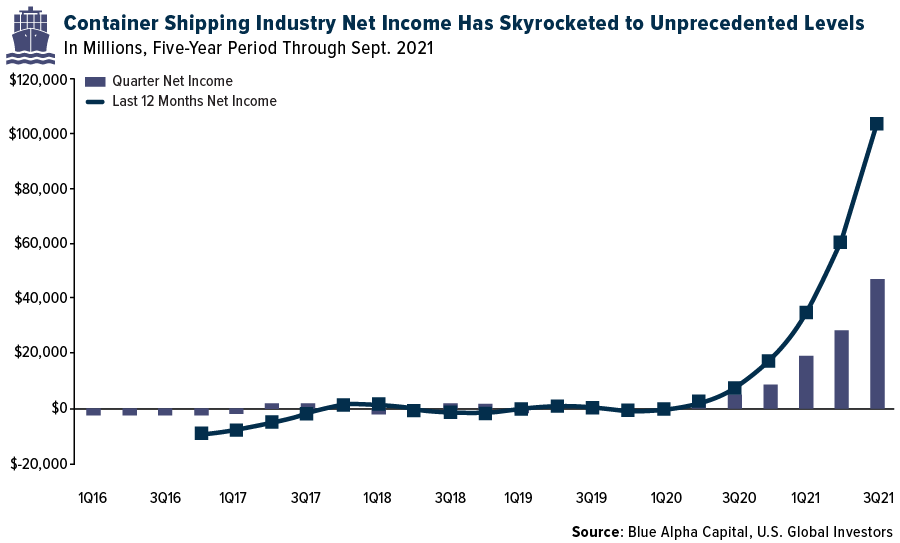

2. Container shipping companies are making insane amounts of money.

By now, everyone is aware of the shipping bottlenecks that have snarled the global supply chain. This has been a huge logistical headache for container shipping companies, but if I were them, I wouldn’t be complaining too much.

The reason I say that is because the global container shipping industry recorded a record net income of $48.1 billion in the third quarter of this year, according to a new report by Blue Alpha Capital’s John McCown. That represents the fourth straight quarter of record profits due to higher shipping rates.

Even more striking is that the $48.1 billion in profits were “almost 50% higher than total FANG profits,” says McCown, referring collectively to tech giants Facebook, Amazon, Netflix and Google. “Compared to earnings behemoths Apple and Microsoft combined, container shipping industry profits were still almost 15% higher with a profit margin that was almost 30% higher” during the third quarter.

That said, perhaps someone should make a cute FANG-like acronym for publicly traded shipping companies. I propose MECH, for Maersk, Evergreen Marine, COSCO and Hapag-Lloyd.

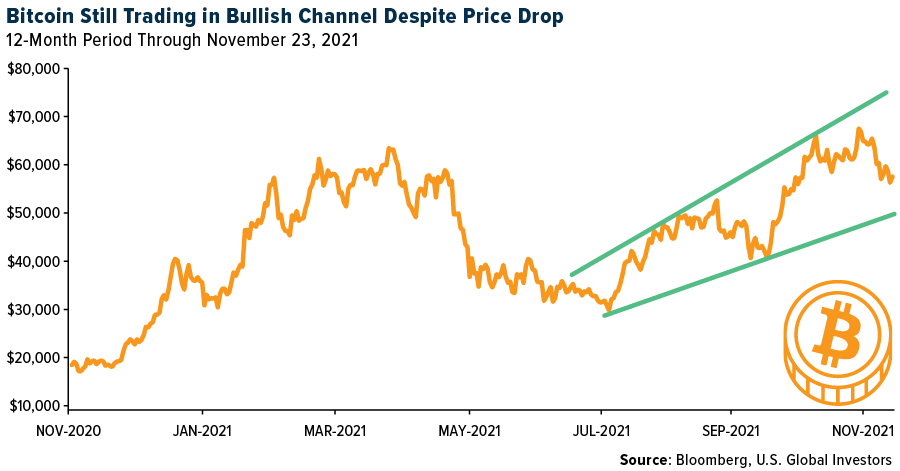

3. Bitcoin consolidates but is still flashing a bullish signal.

My third and final chart has to do with Bitcoin. The price of the world’s most popular cryptocurrency pulled back this week, touching $55,460 on Tuesday, its lowest level in over a month, on fears that interest rates may be hiked sooner and faster than expected.

Although Bitcoin fell through its support level of $57,653, one analyst points out that it’s still trading in a bullish channel. According to CoinDesk’s Omkar Godbole, the crypto’s outlook “remains constructive despite the recent pulldown,” hitting higher highs and lower lows since July.

Institutions and Bitcoin whales have largely been responsible for driving the recent price surge, and though activity has slowed somewhat, the pause appears only to be temporary.

For one, Citigroup is reportedly seeking to hire 100 people to bolster its digital assets business for institutional investors. And according to CoinTelegraph, the Commonwealth Bank of Australia (CommBank) will become the first of the “big four” Australian banks to offer crypto services. The decision comes after its CEO, Matt Comyn, determined that missing opportunities in cryptos posed a greater risk than participating in them.

Index Summary

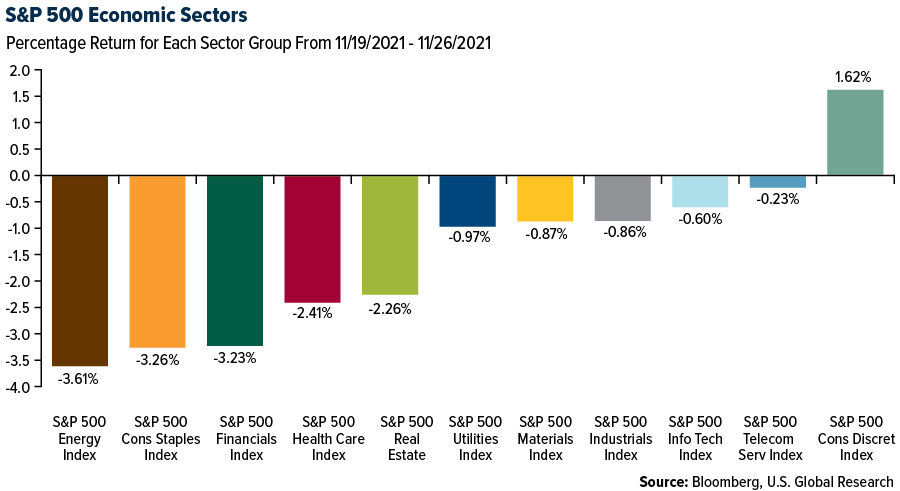

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.97%. The S&P 500 Stock Index fell 2.21%, while the Nasdaq Composite fell 3.52%. The Russell 2000 small capitalization index lost 4.23% this week.

- The Hang Seng Composite lost 3.27% this week; while Taiwan was down 2.52% and the KOSPI fell 1.16%.

- The 10-year Treasury bond yield fell 6 basis points to 1.488%.

Airline Sector

Strengths

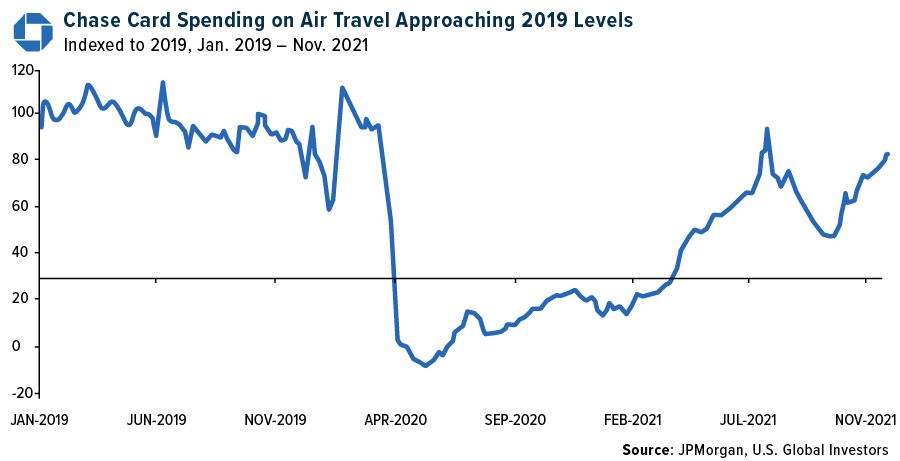

- The best performing airline stock for the week was Grupo Aeromexico, up 1.3%. Chase credit card spending on air travel continues to improve every day, and on an indexed basis, is approaching levels not witnessed since 2019. Similar positive momentum was seen with aggregated Bank of America debit and credit card data, with daily airline spending above 2019 levels for the first time this year.

- European airline bookings increased in the week, with robust growth in international net sales offsetting a decline in Intra-Europe. This is despite renewed concerns over rising COVID cases and the re-imposition of restrictions across Europe. Intra-Europe net sales were down by 2 points to -44% versus 2019 (versus -42% last week), and fell 3% week-on-week, after a large decline last week. International net sales increased by 6 points to -40% versus 2019 (versus -46% in the week prior) and grew by 8% this week to reach their highest post-pandemic level. This led to a 4-point increase in system-wide net sales for flights booked in Europe to -41% (versus -45% last week).

- System net sales improved for the seventh straight week to down 32.8% versus 2019, versus last week’s level of -37.9%. This week, both bookings and pricing improved, and we continue to expect strong holiday demand.

Weaknesses

- The worst performing airline stock for the week was Norwegian Air Shuttle, down 13.0%. According to Credit Suisse, following Jet2, Ryanair and Wizz Air’s updates on winter prospects, the bank cut its EasyJet fiscal year 2022 EBITDA by 13% from £802 million GBP to £694 million GBP, which drives negative free cash flow of £145 million GBP.

- For U.S. capacity, January saw a 2% reduction in planned capacity driven by United Airlines and JetBlue with ASMs for the month now 8% below 2019, while February was lowered by 1% with cuts across most of the airlines and ASMs for the month.

- S. airlines’ trailing seven-day website visits were 16% for the week compared to 20% last week, with all airlines above 2019 levels. Delta, with visitation at 6% (versus 2% last week), still trails behind American Airlines and United (both up approximately 20% versus 2019), but the rate of underperformance continues to narrow. Over the past month, the network carriers have gradually improved, while the low-cost carriers’ website visits have been choppy.

Opportunities

- American Airlines Chairman and CEO Doug Parker, remains confident that business travel will return to 2019 levels at some point. Last week, Parker stated he remains bullish on business travel and believes video communication platforms, like Zoom, will co-exist with corporate travel rather than compete with it. The company’s CEO also stated that (for now) smaller companies who had to curb business travel have been bouncing back better compared to larger companies. This may be considered a leading indicator for business travel volumes to return at larger corporations as many small to medium-sized businesses have returned to the office earlier than larger corporations.

- Domestic leisure (bookings through online channels) was flat this week at 2.3% versus 2019, while corporate (bookings through large corporate channels) improved to down 41.8% (versus -44.8% last week). Bookings flattening out is likely driven by consumers having already booked holiday travel and, historically, after mid-November, ticket sales decelerate serially every week into year-end.

- Weekly fare trends surveyed for the scheduled domestic U.S. air travel showed an overall improvement as average close-in (one-week out) fares gained 7.5% this week, ahead of the peak Thanksgiving travel period. The leisure (four-week out) fares were slightly up 1.4% this week (albeit ~15% higher versus the mid-August to mid-October average fares) with the upcoming Christmas to New Year holiday travel season as the expected next catalyst.

Threats

- Airlines prepare for a busy week ahead as air travel is expected to surge for the Thanksgiving holiday. Last week, the Transportation Security Administration (TSA) released a press release stating that it expects to screen 20 million passengers during the Thanksgiving holiday, nearly the same number as in 2019. According to CNBC, both Delta Air Lines and United Airlines said that the Sunday after Thanksgiving could be their busiest day since before the pandemic.

- The most concerning trend is a fourth wave of COVID-19 sweeping across Europe with some countries reinstating full and partial lockdowns, curfews, or other travel restrictions. After the Netherlands instituted a partial lockdown last weekend, this past week: 1) Austria outlined plans for a full lockdown; 2) Germany put in place stiffer restrictions on unvaccinated people; 3) Norway reinstated stricter entry requirements; and 4) Spain reimposed some curbs on large gatherings. While international tickets sold were down 29.7%, its best level since the pandemic, the situation unfolding in European continues to show the recovery in travel will not be linear.

- United’s CEO, Scott Kirby, noted a pilot shortage is manifesting at regional airlines due to accelerated retirements during the pandemic and resumption of growth at mainline carriers, which echoes comments by American Airlines and Alaska Air during third-quarter earnings calls. Mr. Kirby indicated markets that rely on 50-seat RJs are most likely to lose service. Schedules already indicate small-market cuts as the DOT’s service order requirements associated with the CARES Act expire.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 2.3%. The best performing country in Asia this week was the Philippines, gaining 0.1%.

- The Romanian leu was the best performing currency in emerging Europe this week, gaining 0.14%. The Philippine peso was the best performing currency in Asia this week, gaining 0.04%.

- Despite a spike of COVID-19 cases in Europe, the Eurozone reported stronger-than-expected preliminary PMI numbers. Manufacturing PMI was released at 58.6 versus 57.4 expected. Service PMI jumped to 56.6 versus 53.5 expected, bringing Composite PMI to 55.8 versus 53.0 expected, and above October’s 54.2.

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 4.9%. The worst performing country in Asia this week was India, losing 5.3%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 8.8%. The Thailand baht was the worst performing currency in Asia this week, losing 2.7%.

- The Turkish lira continues to depreciate against the U.S. dollar as the President of Turkey continues to call for lower rates despite inflation at 19%. The lira has lost 40% of its value since the beginning of the year and is the world’s worst performing currency right now.

Opportunities

- China will continue to support its economy and the heavily indebted real estate developers. Chinese banks have been told by financial regulators to issue more loans to property firms for project development in an effort to ease liquidity strains. In addition, China State Council has signaled more policy support for small businesses, increasing funding support, further tax and fee reductions, and permission for manufacturing small medium enterprise (SMEs) to defer fourth-quarter tax payments.

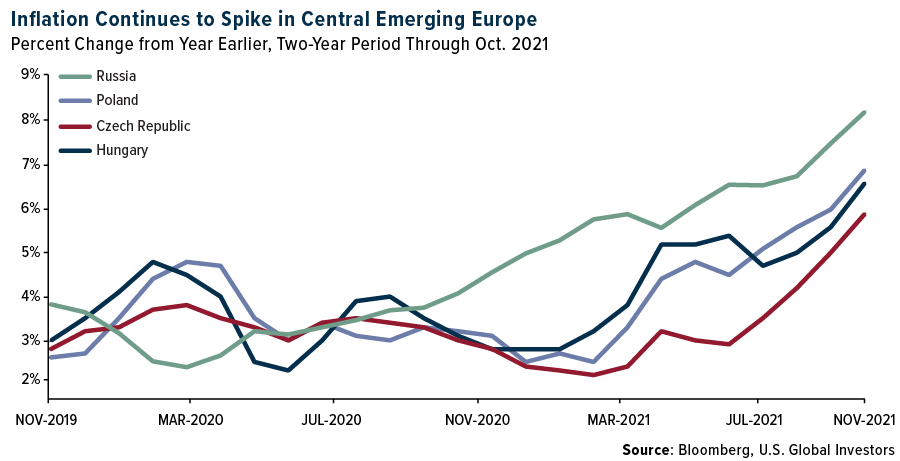

- Poland will release inflation data next week and Bloomberg economists predict inflation to move higher. Inflation in Poland is at 6.8% on a year-over-year basis. Central emerging Europe was first to start raising rates. Additional rate hikes out of Poland, Russia, Hungary, and the Czech Republic may follow.

- According to Bloomberg’s data released on Friday, money supply in Europe increased 7.7% in October, above the expected 7.4%. While the United States started to withdraw some stimulus from the market, the Eurozone will keep the liquidity taps open despite raising prices.

Threats

- Russia could remain at the center of geopolitical focus, building some negative attention. This week Intel shared its findings, with Europe showing a buildup of Russian troops and artillery along the border with Ukraine. Reports say that Russia is preparing to push more inward into Ukraine passing the disputed Donbass area. Others say that Russia is preparing to attack Ukraine in case the country tries to re-capture the disputed Eastern territory of Ukraine, the Donbass region. Russian equities and the Russian ruble declined this week on threats of increased geopolitical tensions and potential sanctions. Also, weaker oil prices put some pressure on the Moscow Stock Exchange.

- Euro-area consumer confidence contracted more than expected in October, to -6.8 versus the expected -5.5. The number suggests greater concerns by the region’s consumers due to a worsening COVID outlook and higher inflation. Next month’s consumer confidence will likely worsen due to stricter lockdown measures and social unrests across many European countries.

- Bloomberg economists expect China’s Manufacturing PMI to increase to 49.6 in November from 49.2 in October but will likely remain below the 50 level that separates growth from contraction. Service PMI is expected to decline to 51.3 in November from 52.4 in October due to COVID-19 restrictions. Composite PMI should remain above the 50 level, mostly supported by non-manufacturing PMI.

Energy & Natural Resources

Strengths

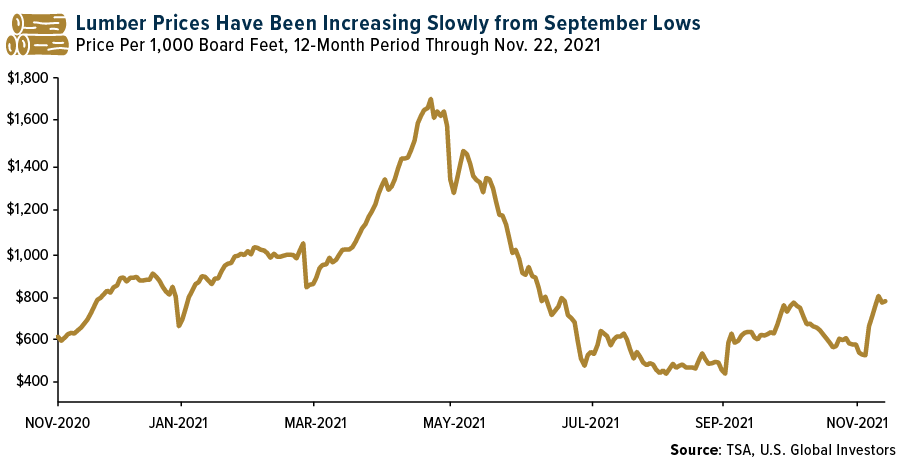

- The best performing commodity for the week was uranium, up 26.69%, with the bulk of the move coming on Friday with little specific news. Western lumber trading momentum significantly improved this week as heavy rains and flooding in British Columbia added to a list of issues (duties, log costs and harvest cutbacks) for the Western Canadian industry. Lumber ended the week up 12% at $620, up 18% relative to the third quarter, up 4% year-to-year, and up 58% year-to-date.

- Permian Basin crude oil production is projected to hit a record high of 4.95 MMBPD in December, according to the EIA. If reached, production in the basin would surpass the previous high-water mark set in March 2020, with Permian production exceeding that of each OPEC member outside of Saudi Arabia. Recovery in the basin has benefited from low break-even costs and rationalized capital spending from domestic public producers that have prioritized the Permian over other plays.

- Total natural gas consumption in the U.S. climbed 3.0% in the week ended November 17, as colder temperatures boosted gas use in the residential and commercial sector, according to the U.S. EIA’s “Natural Gas Weekly Update.” Gas consumption in the country rose to 79.0 Bcf/d from last week’s 76.7 Bcf/d. Residential and commercial demand increased to 27.7 Bcf/d from 24.7 Bcf/d a week earlier, while industrial demand inched up to 23.4 Bcf/d from the week-prior’s 23.2 Bcf/d.

Weaknesses

- The worst performing commodity was crude oil, down 9.19% for the week with news of the emerging new coronavirus strain. The world’s biggest solar market will need a year-end installation rush to meet growth targets as cost inflation slows development. China added about 29.3 gigawatts of solar in the first 10 months of the year, the National Energy Administration said last week. That’s well short of the annual forecast of 55 to 65 gigawatts set by the China Photovoltaic Industry Association earlier in 2021. The slower-than-expected growth comes after cost inflation hit the solar supply chain, with the price of solar panels rising for the first time in eight years.

- OPEC+ officials warned they’re likely to respond to plans by the world’s largest oil consumers to release oil from their strategic stockpiles, setting up a fight for control of the global energy market. OPEC+ delegates said the release of millions of barrels from the inventories of their biggest customers is unjustified by current market conditions and the group may have to reconsider plans to add more oil production when they meet next week.

- World steel output fell 3% month-to-month (-11% year-to-year) due to lower Chinese output (-6% month-to-month, -23% year-to-year). Lower Chinese production was evident in the CISA data, driven by government restrictions to reduce CO2 emissions and reduce electricity usage. European Union prices fell 6-7% this month and U.S. prices fell 5% this month (-8% from the peak) due to automotive weakness and rising import pressure with U.S. import prices 23% below domestic prices. Chinese prices fell 10-12% this month due to ongoing weak demand.

Opportunities

- BP PLC has kicked off a hiring campaign to fill jobs in its fledgling hydrogen business. The U.K. oil and gas major is initially looking to fill some 100 hydrogen jobs to work on projects from Spain to Australia. It’s among a raft of global energy companies stepping up investment in the clean-burning gas on a bet that the market will boom as industries and consumers switch to lower-carbon fuels.

- While the top consuming nations are preparing to release oil from their national reserves to rein in rising prices, crude oil is actually cheap relative to other financial assets, according to JPMorgan. Among global stocks, bonds and commodities, oil is in the 19th percentile over the last 20 years, and to rise to the 50th percentile relative to historical levels, it would need to be at $115 per barrel.

- Long natural gas and short coal as a $12 billion Liquified Natural Gas (LNG) investment gains approval to develop the Scarborough field led by Woodside Petroleum. The project will supply up to 8 million tons annually for at least 20 years and is key in displacing coal in the future energy mix. In the U.S., Chenier Energy is a major North American player in the global LNG market.

Threats

- China’s steel industry may face another challenging year in 2022, with production and demand declining by 6.1% and 5.1% year-to-year, respectively. U.S. steel prices will likely come under pressure, although infrastructure stimulus should be supportive. China’s iron ore demand is set to be weaker, while the large miners will likely ship more tons, a combination that should push the raw material into surplus and keep prices at marginal costs; that said, a post-Olympics rebound is possible. Coal prices will likely come under pressure, partially because supply is set to normalize.

- The U.S. will release 50 million barrels of crude from its strategic reserves in concert with China, Japan, India and South Korea and the U.K — an unprecedented, coordinated attempt by the world’s largest oil consumers to tame oil prices that could prompt a backlash by OPEC+. Of that amount, 32 million will be released from the U.S. Strategic Petroleum Reserve as an exchange over the next several months, while 18 million will be as an accelerated release from previously authorized sale, the White House said in a statement Tuesday.

- World markets were rolled on Friday as reports of a new COVID-19 variant emerged out of South Africa. The suspension of flights and travel by a number of countries around the world has the market worried that we will have to go back into physical lockdowns around the world – just when we thought we were done. Energy prices took the brunt of the hit, but metal markets also sold off.

Domestic Economy & Equities

Strengths

- Initial jobless claims fell by 71,000 to 199,000, beating estimates for 265,000. This is the lowest reading since 1969. Continuing claims declined from 2,080,000 to 2,049,000, above the expected 2,032,000.

- Preliminary November Markit Manufacturing PMI was released at 59.1 as expected, while the Service PMI declined to 57.00 from the expected reading of 59.0. Composite PMI declined to 56.5 from 57.6 from the prior month but remains well above the 50 level that separates growth from contraction, pointing to robust economic activity in the United States.

- Moderna, a pharmaceutical company, was the best performing S&P 500 stock for the week, increasing 24.96%. Shares gained on Friday following news of a new COVID-19 variant found in South Africa.

Weaknesses

- New home sales declined from 800,000 to 745,000 in October. Bloomberg economists were excepting the new sales to hold at the same level of 800,000.

- Third-quarter gross domestic product (GDP) was revised up to an annualized 2.1% from 2%, and below the 2.2% estimate.

- Popular clothing store GAP was the worst performing S&P 500 stock for the week, losing 28.0%. Shares declined 24% on Wednesday after the company announced weaker sales. For the fiscal third quarter, the company’s earnings of 27 cents per share missed the Zacks’ consensus estimate of 49 cents.

Opportunities

- S. President Joe Biden announced on Monday that he is re-nominating Jerome Powell for a second term as Federal Reserve Chairman and will put forth Fed Governor Lael Brainard as Vice Chairman. In making the decision, Biden praised Powell’s Fed for its “decisive” action in the early days of the pandemic. The nominations will head to the Senate next for confirmation.

- The White House announced that the U.S. would release 50 million barrels of oil in a coordinated effort with China, India, Japan, Korea, and the United Kingdom. The announcement said that 50 million barrels would be made available, including 32 million barrels over the next several months, while 18 million will be an acceleration into the next several months (of oil that Congress have previously authorized for sale), FactSet reports. Biden also said he will take additional action if needed to maintain adequate supply.

- The U.S. economy continues to expand. Consumer spending jumped 1.3% in October, beating expectations. Spending is likely to support growth during the busy shopping months. Black Friday could see record strong sales.

Threats

- November FOMC minutes leaned hawkish, FactSet reports. Some participants favored a more aggressive taper in an effort to put the Federal Reserve in a stronger position to raise rates.

- On Friday, one day after Thanksgiving, U.S. indices sold off sharply. A new COVID strain was discovered in South Africa. Reports note that the B.1.1.529 variant features a high number of mutations, though it is unclear the degree to which the variant is more transmissible or deadly. In addition, Goldman Sachs predicts that the Fed could double its taper pace at the December meeting.

- Bloomberg economists expect the ISM Services Index, the amount of activity related to the services sector, to fall to 65.0 in November from 66.7 in October. Data will be released December 3.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Solar Energy, rising 5,751.35%.

- An American multinational investment bank, Citi Group, has been on a hiring spree over the past week as the bank continues to build its digital asset department. Citi has hired over 100 crypto professionals for its digital asset department headed by Puneet Singhvi, who was previously the head of blockchain and digital assets in Citi’s trading business.

- In new filings with the SEC, banking giant Morgan Stanley has revealed some of its funds added Bitcoin exposure in the third quarter, writes Bitcoin Magazine. For the period ending September 30, Morgan Stanley’s Growth Portfolio Fund added 1.5 million shares of the Grayscale Bitcoin Trust Fund.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Fast Swap, down 99.25%.

- Elon Musk had some choice words for cryptocurrency exchange Binance on Twitter this past Tuesday. Musk tweeted that “Doge holders using Binance should be protected from errors that are not their fault.” This statement comes after an upgrade of the Dogecoin network appeared to have caused an issue with network withdrawals for users on the platform.

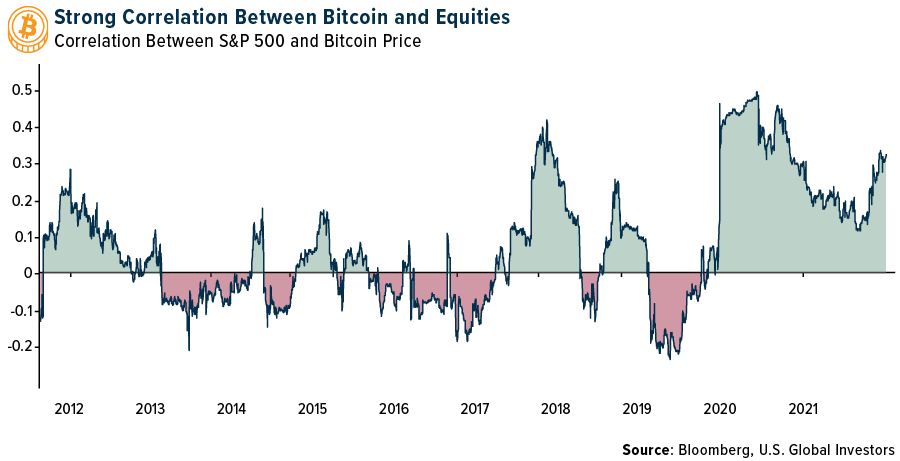

- Many speculative stocks had a rough day on Monday, as did Bitcoin and other cryptocurrencies, reports Bloomberg. The 100-day correlation coefficient of Bitcoin and the S&P 500 stands at 0.33, among the highest reading of the year. That means that when stocks move up, Bitcoin is likely to do the same, and vice versa, the article continues.

Opportunities

- NFL wide receiver Odell Beckham Jr. will take his new salary entirely in Bitcoin through a partnership with Cash App, he announced on Twitter this week. Beckham Jr. recently left the Cleveland Browns for the L.A. Rams, reports Bitcoin Magazine.

- A huge arbitrage opportunity just opened in the crypto community. After news that India’s government will regulate cryptocurrencies, Bitcoin was down 14% on WazirX, (India’s most trusted cryptocurrency exchange).

- Lancium Technologies, a Houston-based tech company, said it has raised $150 million to build a series of Bitcoin mines across Texas that will run on green energy. The company said its clean campuses will host Bitcoin mining, high throughput computing, and other clean energy-intensive applications, writes TheStreet.

Threats

- Hackers, for the most part, usually target institutional crypto investors and exchanges. But as the adoption of cryptocurrencies has become more mainstream, some have started targeting small retail investors, writes Bitconist. They do so through SIM swaps or switching phone numbers from one device to another. This gains them access to random retail investors’ crypto accounts on trading platforms, in which these hackers then proceed in emptying.

- The U.S. is pursuing a British man over allegations he helped hijack an American citizen’s identity to steal $8.5 million in crypto assets. Corey De Rose is facing extradition to the U.S. and is part of a team of hackers called “The Community,” which the U.S. identifies as the group responsible for stealing over $50 million in cryptocurrencies between 2017 and 2018, writes Bloomberg.

- Vitalik Buterin, the creator of Ethereum, had some strong words on Friday about the adoption of Bitcoin as legal tender in El Salvador, explaining why he thinks it’s a reprehensible endeavor, writes Medium.com. “Bitcoin has sprung as an idea not only to get free of government currencies, but to advance freedom in general when it comes to choosing money. Forcing people to accept Bitcoin (BTC) as a means of payment definitely speaks against that ethos,” he stated.

Gold Market

This week spot gold closed at $1,786.94, down $58.82 per ounce, or 3.19%, by Friday’s early market close. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.86%. The S&P/TSX Venture Index came in off 5.09%. The U.S. Trade-Weighted Dollar rose just 0.05%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-24 | Initial Jobless Claims | 260k | 199k | 270k |

| Nov-24 | GDP Annualized QoQ | 2.2% | 2.1% | 2.0% |

| Nov-24 | Durable Goods Orders | 0.2% | -0.5% | -0.4% |

| Nov-24 | New Home Sales | 800k | 745k | 742k |

| Nov-25 | Hong Kong Exports YoY | 20.7% | 21.4% | 16.5% |

| Nov-29 | Germany CPI YoY | 5.0% | — | 4.5% |

| Nov-30 | Eurozone CPI Core YoY | 2.3% | — | 2.0% |

| Nov-30 | Conf. Board Consumer Confidence | 110.7 | — | 113.8 |

| Nov-30 | Caixin China PMI Mfg | 50.5 | — | 50.6 |

| Dec-1 | ADP Employment Change | 515k | — | 571k |

| Dec-1 | ISM Manufacturing | 61.0 | — | 60.8 |

| Dec-2 | Initial Jobless Claims | 225k | — | 199k |

| Dec-3 | Change in Nonfarm Payrolls | 525k | — | 531k |

| Dec-3 | Durable Goods Orders | — | — | -0.5% |

Strengths

- The best performing precious metal for the week was gold, but still off 3.19%. Pasofino Gold published an updated mineral resource estimate for its Dugbe project in Liberia that includes an M&I and inferred resource of 3.9 million ounces of gold. CEO Ian Stalker commented that the robust higher-grade core of 2.88 million ounces grading 1.58 g/t should have good economics around it and that there is still room to grow the resources with potential grade surprises.

- South Africa ruled out challenging a High Court ruling that struck down some key changes to mining rules, specifically that govern black ownership targets, in a move that could potentially revive investor interest in the industry. In September, the High Court struck down some key provisions introduced to the mining charter in 2018 by Mines Minister Gwede Mantashe. It included a rule stipulating that an ownership target of 26% for black investors in South African mining companies would remain in perpetuity. That meant miners that had previously met the threshold would need to find new black shareholders if the original ones exited their holdings.

- Anglo American on Wednesday reported sales by its majority owned De Beers. De Beers sold $430 million of diamonds in the ninth sales cycle of 2021, compared with $492 million at the prior sale and $462 million a year earlier. “Sentiment continues to be positive on the back of strong demand for diamond jewelry from U.S. consumers and this was reflected in the demand we saw for rough diamonds during Cycle 9,” said CEO Bruce Cleaver.

Weaknesses

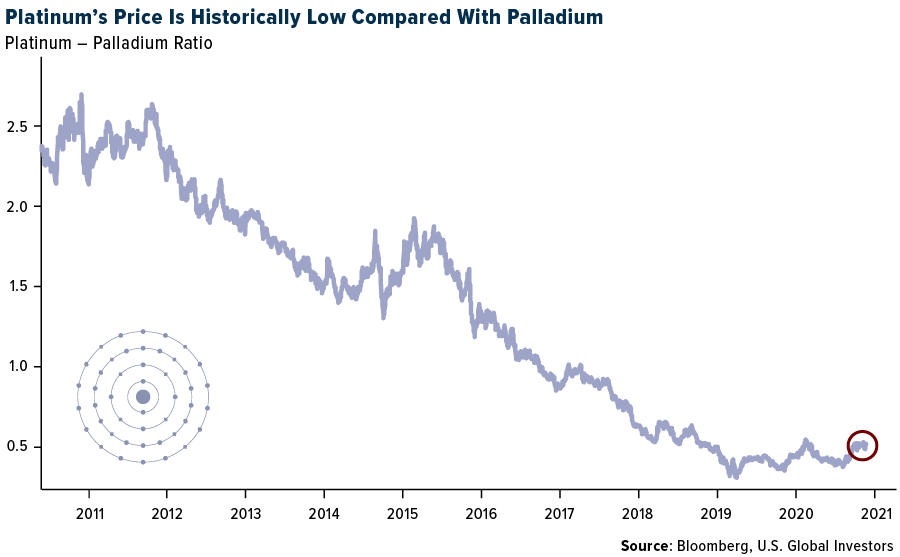

- The worst performing precious metal for the week was palladium, down 14.49%, largely on headlines stating that platinum demand from the car sector was expected to rise as they substitute the cheaper metal for palladium. Hochschild Mining plunged 34% on Monday after reports that Peru will no longer approve additional mining or exploration activities in a region with two of the company’s mines on environmental grounds. Peruvian Prime Minister Mirtha Vasquez said four mines that have been the subject of community protests will be closed as soon as possible. Analysts at Bank of America say those two mines represent 70% of Hochschild’s EBITDA.

- Gold extended its decline after the White House announced that President Joe Biden selected Jerome Powell for a second four-year term as Federal Reserve Chair while elevating Governor Lael Brainard to Vice Chairman. The move is keeping consistency at the U.S. central bank as the nation grapples with the fastest inflation in decades along with the lingering effects of COVID-10. The dollar strengthened in response while Treasury yields extended gains, weighing on bullion’s appeal to investors.

- MAG Silver announced a $40 million equity raise at $17.15per share, following a $40 million credit agreement last week. The additional liquidity needed is due to escalating initial capex requirements for Juanicipio (44% MAG/ 54% Fresnillo) and anticipated delays in returning profits from the JV to MAG’s balance sheet. Additional capital may be needed over the next several years as well.

Opportunities

- China’s gold imports spiked to the highest level in almost two years while imports of steel and copper scrap fell, according to the country’s customs data. Gold purchases totaled 122,659 kilograms in October, up 46% from a month earlier and the highest since December 2019.

- Silver Lake Resources has acquired credit facilities provided by BNP Paribas to Harte Gold. The facilities comprise a $41.3 million non-revolving term facility and a $22 million revolving facility, each of which are fully drawn, with outstanding interest of $2.32 million. The transaction was funded out of Silver Lake’s cash reserves. The consideration did not exceed the outstanding principal and interest balance. Silver Lake intends to work cooperatively with Harte Gold and its stakeholders to deliver an outcome that will provide the best opportunity to realize the full potential of the Sugar Zone mine and the associated land package. In the prior week, Silvercorp announced it had taken a 5.1% interest in Australian listed Chesser Resources which recently posted a resource update. Mark Connelly is the Chairman of Chesser and previously was the CEO of Papillion Resources, which was taken over by B2Gold to gain control of the Fekola gold project.

- Platinum is the rebound trade on a normalization of chip shortages in the auto industry; substitution from palladium should also help. Platinum demand from the auto sector is set to jump next year as makers of pollution-cutting auto catalysts switch to a cheaper alternative to palladium, according to the World Platinum Investment Council (WPIC). Platinum demand from the car industry is expected to climb 20% to 3.24 million ounces next year, the most since 2017, the WPIC said in a quarterly report.

Threats

- According to Credit Suisse, investors are more concerned on reserve replacement this year versus last year, as last year most companies were unable to achieve planned exploration drilling due to COVID-related shutdowns. This year, however, with more normalized exploration budgets and activity, there is a greater expectation to at least replace depletion, i.e., to maintain average mine life. Taking a step back, reserve replacement has become more challenging over the years as discovery grades are generally declining. This is also one of the reasons more gold companies are looking to M&As to grow reserves.

- B2Gold revealed it is considering investing in assets in Zimbabwe, which desperately needs new investment in the country and mining industry. B2Gold said it would consider buying operation assets in the country or a joint venture, perhaps even a milling facility. Currently, U.S.-listed Caledonia Mining is in operation in Zimbabwe successfully, showing good returns on invested capital and paying a quarterly dividend with an indicated yield of 4.38%.

- According to Morgan Stanley, the frequency of protests around the Peruvian mining industry has increased. The group counted three protests targeting the mining industry in Peru in October, some of which turned violent. This raises the question of whether such protest activity could result in mine supply disruptions, potentially impacting global supply/demand dynamics for metal markets.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All