When I was a kid, one of my favorite toys was a top. For younger viewers, a top is a spheroid with a point at the bottom. You wind a string around it, unfurl it quickly, and it spins…like a top. If my description leaves you confused, this YouTube video shows a live demonstration.

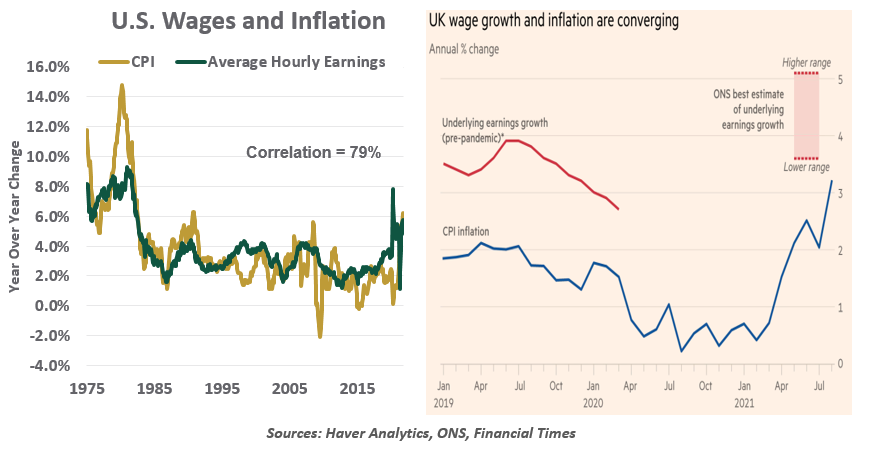

The world’s labor markets are beginning to generate a spiral of a different kind. Wages and prices have been rising briskly in tandem, initiating a feedback loop that could make temporary inflation more permanent. This is a risk that bears close watching.

Labor shortages are widespread. Demand for workers has mushroomed as economies have reopened, but the pandemic is still limiting labor supply. Record fractions of American workers are quitting their jobs for better ones (and better paying ones). The result is wages which are escalating at their highest rate in many years.

To pay those wages and preserve profit margins, companies are pushing through price increases. Prior to the pandemic, consumers were resistant to such efforts, but today, they seem willing to pay. Measures of corporate pricing power are at multiyear highs.

As the prices of goods and services go up, workers will want their pay to keep pace. Employees will raise their wage demands to sustain purchasing power. If companies pass those higher labor costs to customers, the process begins all over again.

In this fashion, a feedback loop between wages and prices can become entrenched. Once it starts, it can be hard to arrest. A wage/price spiral was one of the drivers of the high inflation rates seen in Western countries a generation ago, and it took painful policy forces to slow it down.

Prior to the pandemic, workers had little leverage. In the U.S., the wage share of national income had fallen to a 45-year low. Union representation was in steep decline, and labor market mobility was very limited.

COVID-19 has apparently produced a paradigm shift on this front, at least temporarily. Forced separation from pre-pandemic roles has produced a large class of free-agent workers, who are being very choosy about when and where they seek employment. The rise of remote work has broadened options for service occupations. Reduced immigration during the pandemic has limited the pools of available candidates in a range of occupations; given lingering public health apprehension, borders may remain restricted to new permanent residents for some time to come.

|

Once started, wage/price spirals are hard to stop.

|

The technology that underpins the labor market is also abetting the drive for better pay. It’s easier than ever for candidates to find, apply for, and compare opportunities. For some skill sets, in some places, competitive conditions resemble the frenzy that currently surrounds housing; if hiring managers aren’t ready with a good offer on the spot, they risk losing out.

To be sure, the current set of circumstances is extraordinary, and unlikely to persist. Labor supply is expected to improve in the coming months, and supply chains should start to unkink. As well, it is said that the cure for high prices is high prices: when things get too expensive, people purchase less of them, which can take pressure off scarce supplies.

Another natural governor comes from technology. Faced with persistent labor shortages, firms will apply capital where they can to keep expenses in line. Making workers more productive will allow them to earn higher wages without placing as much pressure on profit margins and product prices.

Once a top is set into motion, it can spiral around for a very long time, unless something intervenes to stop it. If the forces of wages and prices continue to reinforce one another, inflation could hit new tops.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust