Bitcoin Could Fix Turkey’s Currency Crisis

Membership required

Membership is now required to use this feature. To learn more:

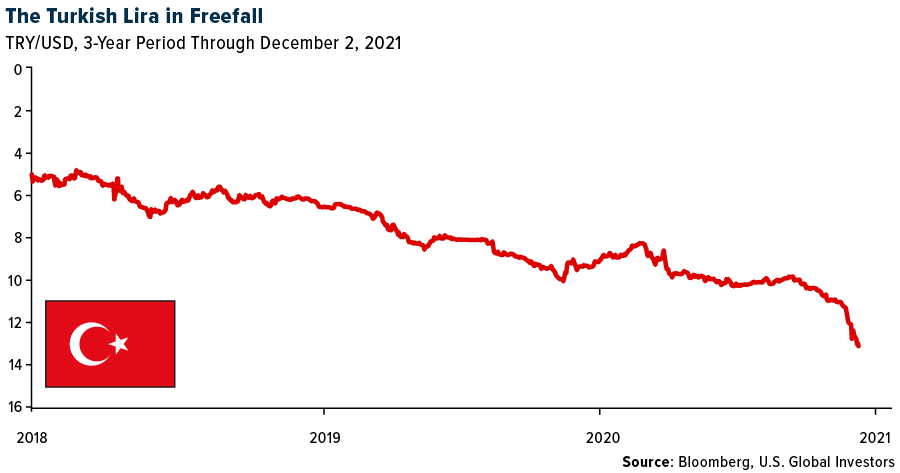

View Membership BenefitsIt’s December 2021, and the Turkish lira just hit a fresh all-time low against the U.S. dollar as President Recep Erdogan continues to implement what the Wall Street Journal calls “unconventional economic policies.” Turkish households saw the value of the national currency plunge nearly 30% last month alone, making everything from food to fuel significantly more expensive for already-struggling families.

Like many others, I believe Bitcoin could fix Turkey’s lira problem. And to understand why, it might be helpful to dust off a book written 45 years ago by Austrian economist Friedrich Hayek.

In the book, Denationalization of Money, the Nobel Laureate makes the case that a government’s monology over money is just as undesirable as any other monopoly. He argues against the creation of a shared European currency—something that would become a reality in 1999 when the euro was introduced—and he proposes that private institutions should be allowed to issue their own currencies.

It’s an idea that Hayek acknowledges is “too unfamiliar and even alarming to most people.” And yet, he says, those same people would eventually learn to see the benefits of a system that allows government-issued fiat currency to “compete for the favor of the public.”

But compete against what? Although written half a century ago, Hayek’s book seems to anticipate the rise of digital assets such as Bitcoin and Ether, which today are the closest thing we have, other than gold and silver, to “denationalized” money.

“When one studies the history of money, one cannot help wondering why people should have put up for so long with governments exercising an exclusive power that was regularly used to exploit and defraud them.”

– Nobel Laureate economist Friedrich Hayek (1899-1992)

“Bitcoin Fixes This”

As I write this, more than 15,000 different cryptocurrencies are available to trade, according to CoinMarketCap. Even Hayek would agree that’s too much competition. To keep things simple, we’ll stick to talking about Bitcoin.

As a decentralized asset, Bitcoin is precisely the kind of asset Hayek may have had in mind. It’s not issued by, nor does it belong to, any government. No central bank controls it. It’s completely border-agnostic. I can no longer send money to someone in Cuba using Western Union since operations ended there last year. But Bitcoin? No problem.

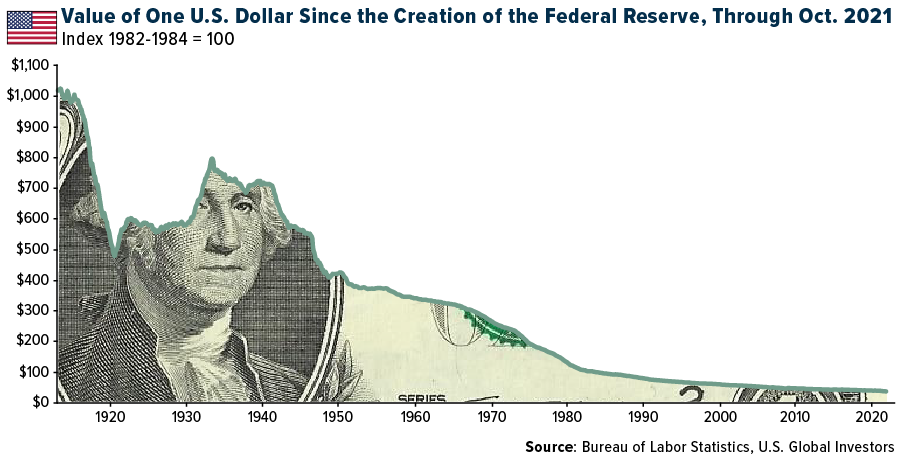

What’s more, Bitcoin has been a fabulous store of value compared to traditional currencies such as the Turkish lira and even the dollar, whose purchasing power has steadily deteriorated since the Federal Reserve’s founding in 1913. In the past 40 years alone, the greenback has lost two thirds of its value as Fed governors have pursued increasingly more unorthodox monetary schemes.

As for the problem of monetary manipulation, Hayek sees competing currencies as the solution. If people had a choice, he believes, this would “prevent governments from ‘protecting’ the currencies they issue against the harmful consequences of their own measures.” In other words, central bankers and finance ministers would have a harder time “concealing” measures to depreciate the value of their currencies.

It should start to make sense, then, why countries like China and Turkey have effectively banned Bitcoin, and why bureaucrats and policymakers in the U.S. and Europe are eager to regulate it.

Free Markets, Free Currencies

Despite the crypto ban, many Turks have reportedly turned to Bitcoin, not to mention gold, as the lira continues to sink due to Erdogan’s insistence on lowering interest rates to combat out-of-control inflation. Yes, central banks ordinarily hike rates to control higher prices, not lower them, but Erdogan allegedly does not want to risk economic momentum for economic stability. And before you say it, no, heads of government are not typically put in charge of monetary policy.

The country’s finance minister, Lutfi Elvan, resigned in protest this week, and Erdogan immediately replaced him with a loyalist. This tells me he won’t be abandoning his easy money scheme anytime soon, which is bad for consumer prices but good for Bitcoin’s use case.

I’m a believer in free markets, as I assume you are. Competition benefits consumers not just because it gives them choices; it also breeds innovation and helps keep price in check.

Monopolies generally have the opposite effect, but for some reason, we generally don’t think of the lira or the dollar or any other fiat currency as being a “monopoly.” Perhaps it’s time we should.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.91%. The S&P 500 Stock Index fell 1.22%, while the Nasdaq Composite fell 2.62%. The Russell 2000 small capitalization index lost 3.86% this week.

- The Hang Seng Composite lost 1.41% this week; while Taiwan was up 1.89% and the KOSPI rose 1.09%.

- The 10-year Treasury bond yield fell 12 basis points to 1.347%.

Airline Sector

Strengths

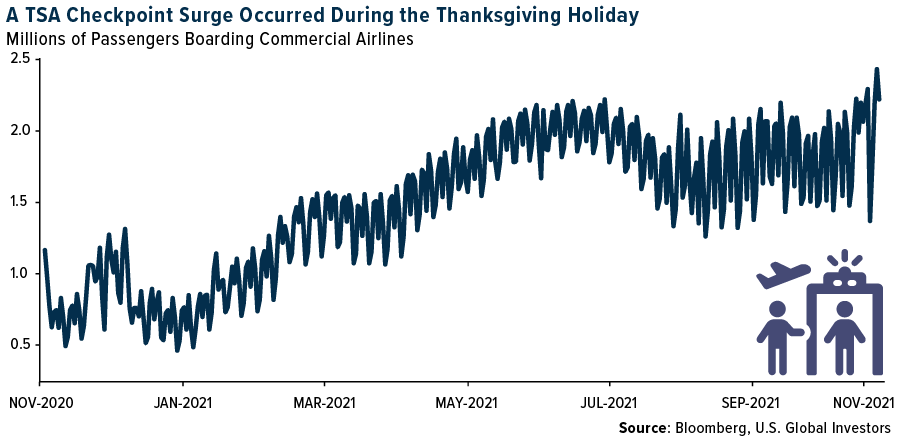

• The best performing airline stock for the week was Wizz Air, up 14.9%. Thanksgiving air travel doubled compared to last year and came in slightly below 2019 levels. For seven consecutive days, daily airport passenger volumes exceeded 2 million people, according to the Transportation Security Administration (TSA). This is a streak that has not occurred since before the pandemic. On the day before Thanksgiving, 2.3 million travelers passed through TSA checkpoints, which is more than twice the number of travelers in 2020.

• Corporate bookings through large and small corporate channels improved to -39.2% (versus -41.8% last week) and -11.5% (versus -13.8% last week), respectively. While there has been a faster recovery in bookings through small corporate channels, over the past month, large corporate bookings improved faster at 7% while small corporate bookings improved 5%.

• Airlines passed the first holiday test after few operational disruptions and cancellations occurred over Thanksgiving week. The holidays are the true test of whether airlines are prepared for a surge in travelers, especially after several airlines have had to offer incentives for employees around the holidays to ensure availability of resources and network integrity. For the most part, the Thanksgiving travel week ran smoothly.

Weaknesses

• The worst performing airline stock for the week was El Al, down 11.8%. European airline bookings showed a large decline in the week, with both intra-Europe and international net sales falling sharply. This is likely driven by a resurgence of COVID cases and re-imposed restrictions across Europe. Intra-Europe net sales were down by 10 points to -54% versus 2019 (versus -44% in the prior week), and fell by 15% this week, continuing a declining trend. International net sales fell by 9 points to -49% (versus -40% in the prior week) and were down by 13% this week after a strong rebound from mid-September. This led to an 8-point decline in system-wide net sales for flights booked in Europe, to -49% (versus -41% in the prior week).

• Daily website visits for EU airlines declined by 6 points to -11% versus 2019 (and versus -5% in the prior week). Ryanair declined the most by 17 points, while British Airways increased by 16 points.

• Last week, the Biden Administration announced additional air travel restrictions from South Africa and seven other countries as the new Omicron variant emerged. In addition to South Africa, affected countries include Botswana, Zimbabwe, Namibia, Lesotho, Eswatini, Mozambique, and Malawi. These new restrictions took effect on November 29, and it remains unclear how long these travel bans will remain in place. This announcement comes less than three weeks after the United States lifted COVID-19 travel restrictions for fully vaccinated international travelers, including South Africa. These newly imposed restrictions will likely have more of an impact on larger carriers such as United Airlines, who recently announced a codeshare agreement with Airlink, a South African airline.

Opportunities

• LATAM’s Chapter 11 proceeding and its recent Plan of Reorganization do not favor Azul’s initial plan to pursue consolidation opportunities; however, there is still a probability that an Azul and LATAM merger could materialize. If LATAM’s plan is not approved, Azul’s merger proposal could materialize, potentially leading to one of the largest cross-border airline consolidations after the TAN and LAN merger in 2012, which could lead to significant revenue and cost synergies.

• At this point, if LATAM’s Plan of Reorganization is approved by the court as proposed (dismissing the potential merger opportunity of Azul and LATAM), it could be somewhat positive for Gol, since Gol would avoid facing increased competition.

• EasyJet is continuing to invest in its fleet. The airline’s capital spending should rise from GBP900 million in fiscal year 2022 to GBP1.0 billion in fiscal year 2023, and GBP1.3 billion in capex for fiscal year 2024. This comes as it confirms 19 aircraft deliveries over Fiscal years 2025-2028 on top of a fiscal year 2024 fleet plan of up to 328 units. Threats

Threats

• The arrival of the new COVID variant has caused many governments around the world to restrict travel to and from southern Africa. With a very busy start to the holiday season and case counts already rising in the U.S. before Thanksgiving, these new headlines could begin to weigh on consumers’ willingness to book air travel in the near term.

• Europe recorded its first case of the new coronavirus variant in Belgium, which sparked dozens of countries in Europe and Asia to enact travel restrictions to/from the region. While the new travel bans are so far limited to flights coming from countries that drive a relatively low percentage of international travel, the severity of the new variant could bring about more restrictions or impact bookings

• British Airways has launched a suit against the city of Chicago, requesting over $3 million in damages, reports Simply Flying. Almost one year ago, three BA Dreamliners sustained engine damage from foreign object debris while at Chicago O’Hare. The resulted in the airline needing to perform heavy maintenance, which then resulted in unforeseen costs and canceled flights. In its suit, BA claims that the city of Chicago was negligent in not checking the taxiways and runways of the airport for debris, the article continues.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 7.5%. The best performing country in Asia this week was Taiwan, gaining 2.3%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 2.33%. The South Korean won was the best performing currency in Asia this week, gaining 1.03%.

- Final Eurozone Manufacturing PMI for November was reported at 58.4 versus under the preliminary reading of 58.6, and above October’s reading of 58.3. Poland, Russia, the Czech Republic, and Turkey all reported stronger manufacturing activity despite a spike in COVID cases across Europe.

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 0.11%. The worst performing country in Asia this week was the Philippines, losing 3.03%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 10.18%. The Thailand baht was the worst performing currency in Asia this week, losing 0.74%.

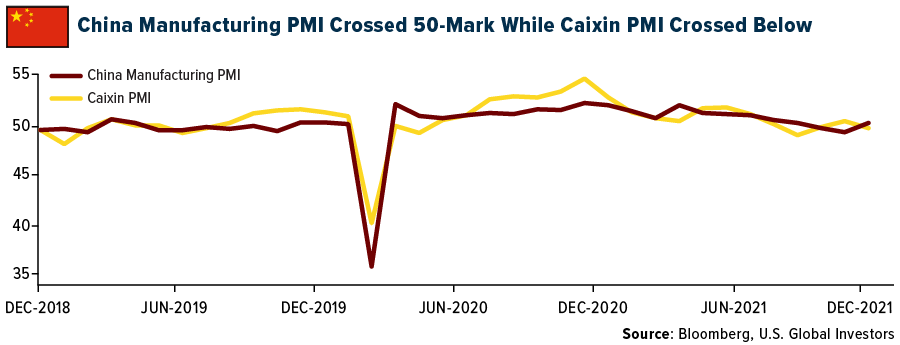

- China Manufacturing PMI crossed below the 50-mark that separates growth from contraction. However, the Caixin Manufacturing PMI, which measures production among smaller non-state-owned companies, crossed above the 50-mark. China’s Manufacturing PMI is weaker than Europe’s or the United States’.

Opportunities

- Bloomberg reported that Vice Premier of China Liu He said he is confident about the economy’s outlook next year, pledging support for small and foreign businesses. China will focus on expanding market access and promoting fait competition to create a better business environment next year.

- The European Central Bank (ECB) is expected to keep an accommodative policy next year, continuing bond buying in 2022. The policy beyond 2022 is unclear, however, the ECB will act on inflation if needed.

- Domestic demand for financial assets in China is strong. Shanghai-based Foresight Fund launched a new equity fund and was able to attract orders worth $16 billion over one day. This is not the first time China’s investors have piled into Foresight’s products. The company’s first fund lured $10 billion in orders within 10 hours in 2019. The second one attracted $17 billion worth of bids in a single day.

Threats

- China developers are facing $12 billion payments coming due in December. In October, developers defaulted on some payments, but there were no defaults in November. At the same time, data showed that home sales in China by the top 100 developers plunged 38% from a year earlier, sharper than the 32% drop in the previous month.

- Inflation spiked in Poland to 7.7% in November, above the expected 7.3% and October’s 6.8%. Neighboring countries similarly are experiencing rising prices. Russia will release inflation next week. Bloomberg economists expect CPI at 8.1%, well above the central bank’s target. Inflation in Turkey spiked to 21.31% in November. Inflation in Hungary could increase as well once data is released on December 8. The Czech Republic, Russia, Hungary, and Poland will continue to hike rates.

- More travel restrictions are expected due to the spread of the Omicron variant. Hong Kong has banned non—residents from entering the city from four African countries and plans to expand that to travelers who have been to Austria, Canada, Israel and six European countries. Vaccinated Hong Kong residents can return but will have to quarantine for seven days in a government facility and another two weeks in a hotel. Additional travel restrictions are being imposed globally.

Energy & Natural Resources

Strengths

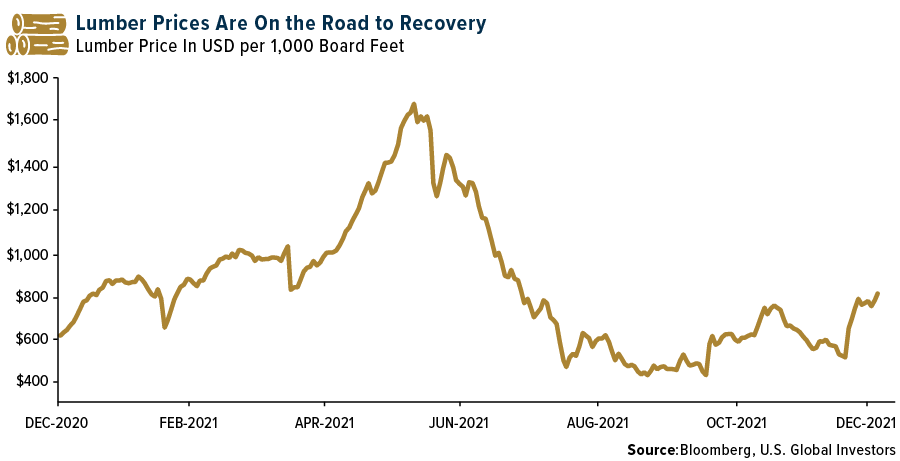

- The best performing commodity for the week was lumber, up 18.39%. According to Random Lengths, the Framing Lumber Composite increased $21 to $611 as transportation issues in British Columbia continue to be a catalyst for pricing. The U.S. Department of Commerce announced finalized softwood lumber duty rates, which brought expected increases. For next week, RBC forecasts that the RL Framing Lumber Composite will increase $23 to $634.

- Iron ore futures in Singapore jumped nearly 10% on optimism over a bout of restocking by China’s steel producers. Prices rebounded from Friday’s pandemic-driven losses alongside a rally across commodities from nickel to crude oil on bets the impact of a new coronavirus variant may not be as severe as initially feared. Iron ore is benefiting from signs that pressure on China’s steel production is gently easing.

- Urea prices took a dive on Friday on speculation that some major buyers are staying on the sidelines. Crop nutrient prices have more than doubled so far this year. Green Markets analyst, Alexix Maxwell, noted that the decline in urea was perhaps just one buyer stepping back from the market, but urea’s decline did not reflect that we had seen a top in fertilizer prices.

Weaknesses

- The worst performing commodity was natural gas, down 25.34% for the week. Natural gas futures plummeted as much as 12% in the U.S. as forecasts shifted warmer through the middle of next month, allaying concern about tight domestic supplies amid a global shortage of the heating fuel.

- Oil continues its sharp selloff marking its sixth consecutive week of decline. At the same time, time spreads declined sharply, product crack spreads rolled over, implied volatility spiked and put skew increased sharply. This broad-based correction reflected fears that the Omicron variant would turn into a major headwind to oil demand.

- UBS will leave its forecast of $3.50 per pound unchanged for copper, implying 15% downside versus spot. The group feels it is generally too early to increase exposure to copper equities as several large new projects are set to drive healthy supply growth over the next two to three years, and many of the large-cap copper stocks already discount prices close to spot.

Opportunities

- Bank of America sees OPEC’s preparedness to intervene as pivotal to market confidence in its ability to hold oil prices within a range. The delay of the Joint Ministerial Monitoring Committee (JMMC) may perhaps indicate some hesitation on its planned return of production. If so, the move on Black Friday may prove another example of the two steps forward, one step back trajectory of the investment case for the U.S. oils.

- According to Credit Suisse, oil will be supported by international jet fuel demand during the holiday season. With diesel demand above pre-pandemic levels and gasoline demand almost at pre-pandemic levels the group sees a lot of support for Brent at $75 per barrel.

- Brent prices will reach $125 a barrel in 2022 and $150 a barrel the year after due to a lack of spare capacity, (especially among OPEC+), JPMorgan equity analysts, including Christyan Malek, wrote in a report. “True” OPEC+ spare capacity next year will be 2 million barrels per day. This is below consensus estimates of 4.8 million barrels per day.

Threats

- Both the IEA and EIA currently forecast no growth in the call-on-OPEC in 2022, which is at odds with OPEC’s own objective to increase production by 400,000 barrels per day, per month next year. As 2022 is coming closer, this has already weighed on oil market expectations in recent weeks.

- As the latest in a complex series of twists and turns, nuclear negotiations between Iran and major powers are resuming this week following a hiatus since Iran’s presidential election in June. At stake is the full return of Iranian crude exports – approximately 1.5 million barrels per day above the current run-rate – onto the global market, provided that Trump-era U.S. secondary sanctions end up being lifted by the Biden administration. While it seems likely that Iranian production will continue to rebound from the Trump-era trough, both timing and magnitude are far from clear-cut.

- The oil outlook remains constructive for 2022, with OPEC’s meeting a near-term catalyst to watch. That said, MS Oil Strategist Martijn Rats estimates that oil prices already reflect a sharp weakening in demand. As he highlighted in his latest note, Omicron Correction, Friday’s move was consistent with a 4 million barrels per day fall in oil demand or a 180-million-barrel rise in OECD inventories, an outcome which he views as unlikely. Looking ahead, Martijn expects OPEC+ to shelve its planned January output increase of 400 kb/d.

Domestic Economy & Equities

Strengths

- Employers added 534,000 jobs in November, following 571,000 jobs created in October. Gains were widespread across the economy, led by firms that employ more than 1,000. The services sector had the strongest increase, with 424,000 jobs added.

- November’s Markit Manufacturing PMI was reported at 58.3, below the prior month’s reading of 59.1. However, the service PMI increased to 58.0 from 57.0 and Composite PMI increased to 57.2 from 56.5.

- Vertex Pharmaceutical was the best performing S&P 500 stock for the week, increasing 11.01%. Shares gained almost 10% on Wednesday when the company reported positive phase 2 results for a drug to treat a rare genetic kidney disease.

Weaknesses

- November non-farm payrolls increased 210,000 month-over-month below consensus for 530,000 and October’s upwardly revised 546,000. It was the lowest monthly reading since December 2020.

- Initial jobless claims went up by 28,000 week-over-week to 222,000, beating consensus of 240,000. The prior week’s number was revised down by 5,000 to 194,000, and the lowest since 1969.

- Etsy, an e-commerce platform, was the worst performing S&P 500 stock for the week, losing 20.61%. Shares declined as UBS rated the company a “sell” and rated other e-commerce platforms such as Amazon, Ebay and Fartech as “buys.”

Opportunities

- Initial jobless claims and continuing claims will most likely decline next week, despite more negative news related to the spread of the Omicron variant. The upcoming shopping season should support the job market. Americans plan on spending $998 on average this year buying holiday gifts, food, decor, and other expenses, according to a new survey conducted by the National Retail Federation (NRF).

- Corporate layoffs are falling to their lowest level in nearly 30 years. The number of announced job cuts in November fell to 14,875, according to outplacement firm Challenger, Gray & Christmas. That’s the lowest figure since May 1993. This week’s unemployment rate was reported at 7.8 in November, down from 8.3 the prior month.

- Bloomberg economists predict the University of Michigan Consumer Sentiment Index to increase to 68.0 in December’s preliminary reading from 67.4 in November. Data will be released December 12.

Threats

- Cleveland Fed President Mester said she is “very open” to accelerating the taper pace to give the Fed more flexibility on rate hikes next year. She favors ending tapering in March, leaving the Fed in a position to raise rates twice in 2022, according to Bloomberg. Earlier this week, Powell said that it may be appropriate for the Federal Reserve to consider wrapping up its taper program a few months sooner than initially proposed.

- The United States announced its first Omicron case this week. It was found in California from a passenger traveling back from South Africa. More cases have been reported in New York, Minnesota, Hawaii, and Colorado since; the rapid spread is due to this strain’s ability to spread quickly. A Pfizer executive said that he expects the company’s vaccine to hold up against the Omicron variant and is not expecting a significant drop in effectiveness of its shot.

- Inflation data will be released next week, and we will likely see further price increases. CPI in October was at 6.2% on year-over-year basis, and CPI, excluding food and energy, in October was at 4.6%. Data will be released December 10.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Mars Space X (MPX), rising 1,594,336.52%.

- one, a software company backed by Peter Thiel and hedge fund managers Alan Howard and Louis Bacon, will offer trading on Bitcoin, Ether, Eos and USDC. The platform isn’t available in the U.S. just yet but will be open in other countries including the U.K., Germany, and Brazil, according to a recent Bloomberg article.

- Bloomberg reports this week that MercadoLibre, an Argentine marketplace company, will offer Bitcoin, Ethereum and Pax Dollar (USDP) trading next week to a select few Brazilian clients. Through a partnership between Mercado Pago and Paxos, the goal is to eventually offer cryptocurrency trading to around 20 million clients throughout Brazil.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Spice DAO (SPICE), down 100.00%.

- Cryptocurrency company executives have been called to testify in U.S. Congress, according to an article published by Cryptopolitan. The meeting will take place next Wednesday, December 8. This meeting could result in either heavy regulations on the cryptocurrency market or new developments in cryptocurrency trade.

- At the Sohn conference in Sydney this week, billionaire investor Charlie Munger says he wishes cryptocurrencies had ‘never been invented,’ and that he admires China for banning them, writes CNBC. “I don’t welcome a currency that’s so useful to kidnappers and extortionists…nor do I like just shuffling out billions of dollars to somebody who just invented a new financial product out of thin air,” Munger added.

Opportunities

- 2TM Participacoes SA, the owner of the biggest Brazil-based cryptocurrency brokerage, raised $50 million dollars as it hunts for acquisitions to expand into other Latin American markets. The company is backed by Softbank Group Corp, 10T Holdings, and Tribe Capital, according to Bloomberg. The proceeds will be used for new products and growth, including expanding into Chile, Colombia, Mexico, and Argentina, according to 2TM co-founder Gustavo Chamati.

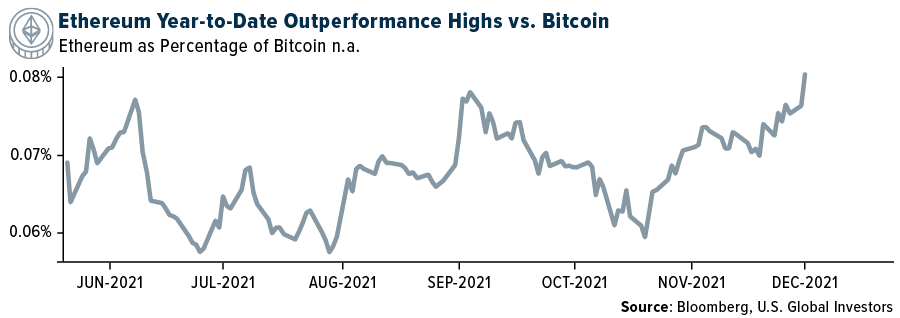

- Ether is outperforming Bitcoin by a large amount this year, since the native token of the Ethereum network’s launch in 2015. Ether has gained about 530% since December, compared with a doubling in value by Bitcoin. This widens the performance gap between the two by more than 400 percentage points.

- American Latino rapper, Pitbull, has reportedly signed a multiyear deal with music oriented NFT platform OneOf, to facilitate the NFT sale and purchase, according to a recent Bloomberg article. The platform is diversifying its artist portfolio and has deals with artist from all genres.

Threats

- BadgerDAO, a decentralized finance platform, suffered a $120 million hack this past Wednesday, reports The Verge. Users claimed that they were sent notifications about allowing new permissions while carrying out activities on the platform. According to the investigation team, the malicious code the hackers used to drain wallets appeared as early as November 10, running the code at seemingly random intervals to avoid detection.

- The SEC is charging a man for defrauding crypto investors out of $7 million, writes Bloomberg. The agency filed a civil complaint against Ivars Auzin for running two fraudulent digital asset securities offerings. Auzin, a citizen of Latvia, allegedly used fake names, profiles, and fabricated entities to carry out the fraud against U.S. and foreign investors.

- The Swedish government wants the European Union to ban cryptocurrency mining, reports Fortune. The government of Sweden believes that Bitcoin mining isn’t just bad for the climate, but it’s bad for worldwide efforts to convert the global energy system to renewables. Currently, Bitcoin mining emits as much CO2 as the entire country of Ireland or Greece, the article claims. Sweden argues that Bitcoin production devours electricity that’s sorely needed to wean bigger industries from fossil fuels, potentially forcing host nations to import dirty energy from abroad, making carbon emissions far worse.

Gold Market

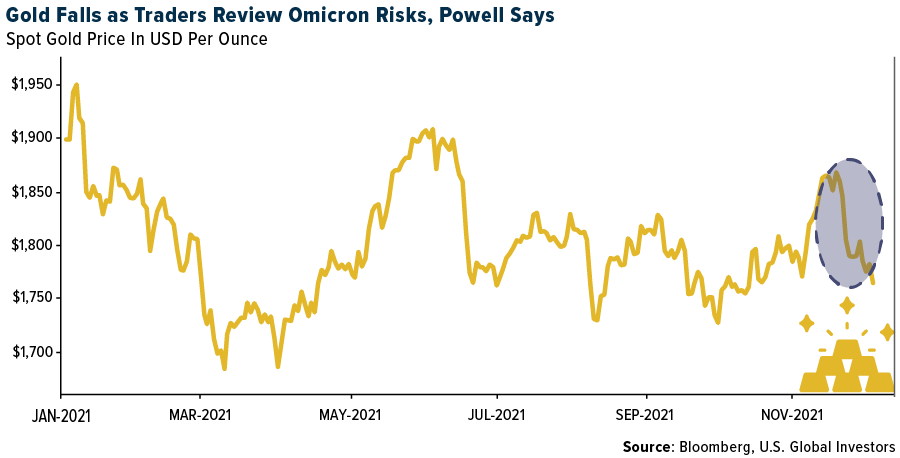

This week spot gold closed the week at $1,768.03, down $7.78 per ounce, or -0.44%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.60%. The S&P/TSX Venture Index came in off 4.97%. The U.S. Trade-Weighted Dollar fell 0.42%.

| Nov-29 | Germany CPI YoY | 5.0% | 5.2% | 4.5% |

| Nov-30 | Eurozone CPI Core YoY | 2.3% | 2.6% | 2.0% |

| Nov-30 | Conf. Board Consumer Confidence | 110.9 | 109.5 | 111.6 |

| Nov-30 | Caixin China PMI Mfg | 50.6 | 49.9 | 50.6 |

| Dec-1 | ADP Employment Change | 525k | 534k | 570k |

| Dec-1 | ISM Manufacturing | 61.2 | 61.1 | 60.8 |

| Dec-2 | Initial Jobless Claims | 240k | 222k | 194k |

| Dec-3 | Change in Nonfarm Payrolls | 550k | 210k | 546k |

| Dec-3 | Durable Goods Orders | -0.5% | -0.4% | -0.5% |

| Dec-7 | Germany ZEW Survey Expectations | 25.0 | — | 31.7 |

| Dec-7 | Germany ZEW Survey Current Situation | 5.0 | — | 12.5 |

| Dec-9 | Initial Jobless Claims | 230k | — | 222k |

| Dec-10 | Germany CPI YoY | 5.2% | — | 5.2% |

| Dec-10 | CPI YoY | 6.7% | — | 6.2% |

Strengths

- The best performing precious metal for the week was palladium, up 2.40%, recovering some of its 14% drop in the prior week. Singapore increased its gold reserves by about 20% in a largely under-the-radar move that saw holdings expand for the first time in decades. The purchases totaled about 26.3 tons, according to data from the Monetary Authority of Singapore’s International Reserves and Foreign Currency.

- Osisko Mining announced that it has signed an agreement for a private placement of $154 million in a convertible senior unsecured debenture due December 1, 2025, with Northern Star Resources Limited. The debenture bears interest at a rate of 4.75% per annum payable semi-annually in arrears, which may be accrued at the option of Northern Star. In addition, Osisko and Northern Star have agreed to negotiate the terms of a joint venture on up to a 50% interest in Osisko’s Windfall Project.

- Credit Suisse has previously written extensively about gold’s role as an inflation hedge, which is particularly relevant in the current inflationary environment (6.2% inflation in the U.S.; 4.7% in Canada), but it is also important to note gold’s role as a defensive asset, especially when there are renewed concerns about COVID-19. Historically, when investors are “risk-off” they seem to gravitate toward gold.

Weaknesses

- The worst performing precious metal for the week was silver, down 2.67%, along with gold and platinum. Newmont Mining has provided clear expectations for 2022 guidance revisions, outlining lower production, a large increase to costs, and relatively stable capital spending. Management indications for 2022 outline production of 6.2 million ounces, stable costs year-over-year of $1,050 per ounce. In December 2021, Newmont guided to 2022 output of 6.2-6.7 million ounces at AISC of $850-$950 per ounce. Long-term budget prices of $1,200 per ounce have been guided to remain unchanged. Industry cost inflation is also guided to have had a positive 5% impact, while interim productivity challenges due to COVID could represent an additional factor in the near-term.

- As posted to the Mining Journal, Hummingbird Resources has taken its Yanfolila gold mine in Mali offline after political unrest. “In recent days there has been unrest and illegal roadblocks in the region,” Hummingbird said. “This activity has impacted the company’s ability to safely continue operations at the mine and as such Yanfolila is temporarily offline until conditions allow.” Yanfolila is located in southern Mali, near the border of Guinea. Hummingbird said the situation on site “remains calm and orderly with all employees and contractors safe and accounted for,” adding that “the current illegal action is from a small minority and not representative of the communities where the company operates and is damaging for all concerned.” The gold miner said it had escalated the issue to the national government, who it said were “in the process of working through the situation and resolving it”. As are result of the suspension, 2021 production is now expected to miss previous guidance of 100,000 – 110,000 ounces.

- Gold fell to the lowest in a month with bond yields rebounding as traders continue to assess the threat of the Omicron variant to the economic recovery. Bullion has been whipsawed recently by statements from health authorities and vaccine makers on the level of risk posed by the new variant, as well as more hawkish comments from Federal Reserve Chair Jerome Powell.

Opportunities

- Impala Platinum Holdings revived its pursuit of Royal Bafokeng Platinum Ltd., seeking control of the smaller South African miner in an escalating battle with Northam Platinum Holdings Ltd. Implats, as the miner is known, offered 150 rand in cash and shares to RBPlat shareholders, valuing the company at about 43.4 billion rand ($2.7 billion). That comes after Northam Platinum Holdings earlier this month agreed to pay 180 rand a share for a 32.8% stake in RBPlat, thwarting Implats’ initial approach.

- Kirkland Lake Gold and Agnico Eagle Mines said shareholders approved the proposed merger of the two companies. Earlier this month, proxy advisory firm Glass Lewis & Co. LLC recommended shareholders of the two companies to vote in favor of the proposal, which is expected to create the largest gold producer in Canada. Under the proposal, Agnico will acquire all of the issued and outstanding shares of Kirkland Lake. Each Kirkland Lake share is equal to 0.7935 Agnico Eagle share. The merger is expected to be completed in the first quarter of 2022, pending final order by the Ontario Superior Court of Justice, approval of the Australian Foreign Investment Review Board, and the satisfaction of other conditions.

- Amarillo Gold Corporation has entered into an agreement with Hochschild Mining PLC, whereby Hochschild will acquire all of the outstanding shares of Amarillo by way of a plan of arrangement under the Business Corporations Act (British Columbia). Pursuant to the arrangement, each share of Amarillo will be exchanged for cash consideration of C$0.40 and one share of a new Brazil-focused exploration company, Lavras Gold Corp., based in Toronto, Ontario.

Threats

- The London Bullion Market Association canceled its annual dinner this week over concerns about the new coronavirus variant, signaling the potential for wider disruption to the corporate events calendar. The black-tie event for gold bankers, refiners and traders was due to take place at London’s Natural History Museum. Instead, an online seminar will be held, replacing an in-person version that was to precede the dinner.

- Impala Platinum Holdings Ltd. said three of five workers who went missing on Sunday after a mud rush at one of its mines in Rustenburg have died. South Africa’s mines ministry said that 58 workers died in industry accidents so far this year due to a deterioration in safety. The rising fatalities indicate that miners’ safety is worsening for a second year, after 60 deaths in 2020, according to Minerals Council South Africa, an industry lobby group.

- A top Swiss gold trader is targeting industrial clients as banks back away from the precious metals business. MKS PAMP Group said it was merging its refining and trading operations. The company plans to lure more customers from the electronics and industrial sectors — offering hedging services and supply contracts — after banks cut back or withdrew from precious metals in recent years.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits