Muni Impact of US Infrastructure Bill Could Prove Longer Term

On November 15, 2021, US President Joe Biden signed into law HR3684, the Infrastructure Investment and Jobs Act. This bipartisan infrastructure bill includes $1.2 trillion of federal spending over the next five years. Of the $1.2 trillion, $550 billion is new spending, while the remainder will fund the reauthorization of the Highway Trust Fund. The final bill did not contain certain municipal bond market-related initiatives such as advance refunding, Build America Bonds (BABs) or elimination of the state-and-local tax (SALT) deduction cap.

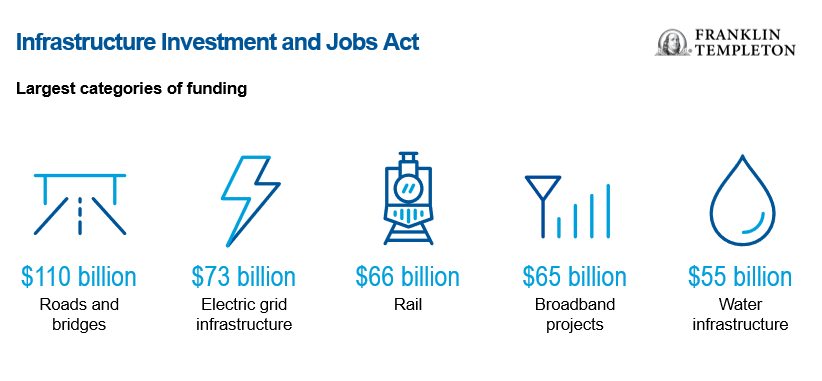

The $550 billion in new spending is spread out over a number of transportation subsectors. The largest spending categories include $110 billion for roads and bridges, $73 billion for electric grid infrastructure, $66 billion for rail, $65 billion for broadband projects and $55 billion for water infrastructure. Moneys will be allocated using various formulas and distribution methods to states, local governments and agencies that will ultimately determine how the money is spent.

This bill comes on the heels of three rounds of federal stimulus in response to COVID-19, much of which is also being spent on infrastructure and/or directed at municipal sectors.

We don’t expect the new bill to inject the economy with $1.2 trillion right away. Funds will be available in increments over the next five years. We think that this could result in additional municipal debt issuance, but that will take time as projects are selected and plans are created and executed. With funding coming in over several years, the impact on the muni market is also expected to play out over several years.

Although the ultimate amount of this package is less than what Biden had initially sought out, we do think this smaller amount is far more manageable. Given the multitude of government entities across three levels of government required to carry out a package of this type, we think this smaller package has a better chance of being implemented in its entirety. A larger package might have proved too onerous to execute in the time frame.

We continue to watch as the president and Congress discuss the Build Back Better Act, targeting social infrastructure as well as the budget reconciliation process for additional funding. Market-favored programs like Build America Bonds and advance refunding might not make it into legislation, but removal or adjustment of the SALT deduction cap appears to be back on the table. Either way, the muni market continues to be an important part of how the country addresses infrastructure while providing investors an opportunity to earn tax-free income.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Because municipal bonds are sensitive to interest rate movements, a municipal bond portfolio’s yield and value will fluctuate with market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the portfolio’s value may decline. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the author and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this presentation has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Franklin Distributors, LLC. Member FINRA/SIPC. Prior to July 7, 2021, Franklin Templeton Distributors, Inc., and Legg Mason Investor Services, LLC served as mutual fund distributors for Franklin Templeton.