The Biggest Investment Themes Heading Into 2022

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsNo matter how old I get, it never ceases to amaze me how much can happen in a year.

Exactly 12 months ago today, inflation was running at only 1.1%, oil was still under $50 per barrel and Bitcoin was trading at $18,260. Virtually no one had been vaccinated against COVID-19, and even fewer people had ever heard of the word omicron – let alone that it is a letter in the Greek alphabet.

Try to imagine, then, what we’ll be talking about 12 months from now. No one can predict the future, of course; otherwise, we’d all be multi-billionaires.

At the same time, there are a number of key investment themes for 2022 I feel most people would agree on. Below are just a handful.

Inflation will stick around a little while longer.

Did anyone really think inflation would be “transitory”?

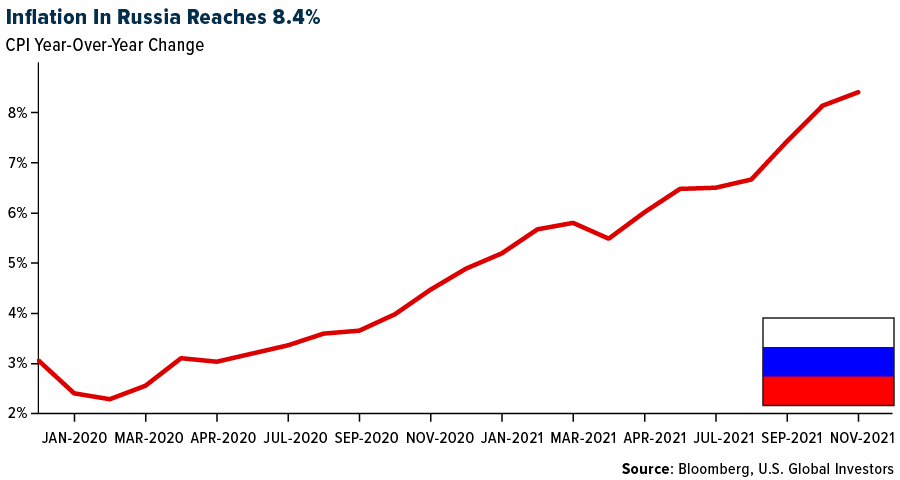

Today the Bureau of Labor Statistics (BLS) reported that consumer prices rose at their fastest annual pace in about 40 years. The consumer price index (CPI) increased 6.8% year-over-year in November, the highest of such a reading since June 1982. Among the biggest contributors to higher inflation were gasoline (up 58.1%), natural gas (25.1%), used cars and trucks (31.4%) and clothes (5%).

But as I’ve said before, the official CPI reading could be understating inflation. Prices may very well have increased even more than we’re being led to believe.

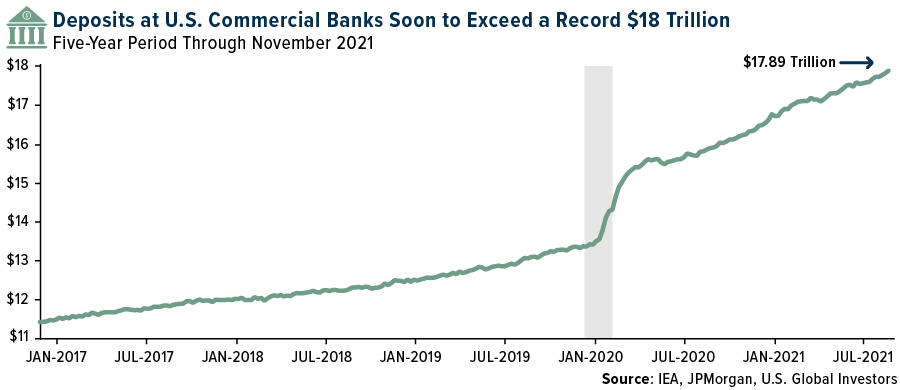

By now, you should know what solutions are available to combat inflation’s deleterious impact on your wealth. It’s slightly distressing to look at the following chart, which shows that the total value of deposits in U.S. commercial banks is about to exceed $18 trillion. Inflation is melting away people’s cash faster than the Federal Reserve can print more of it.

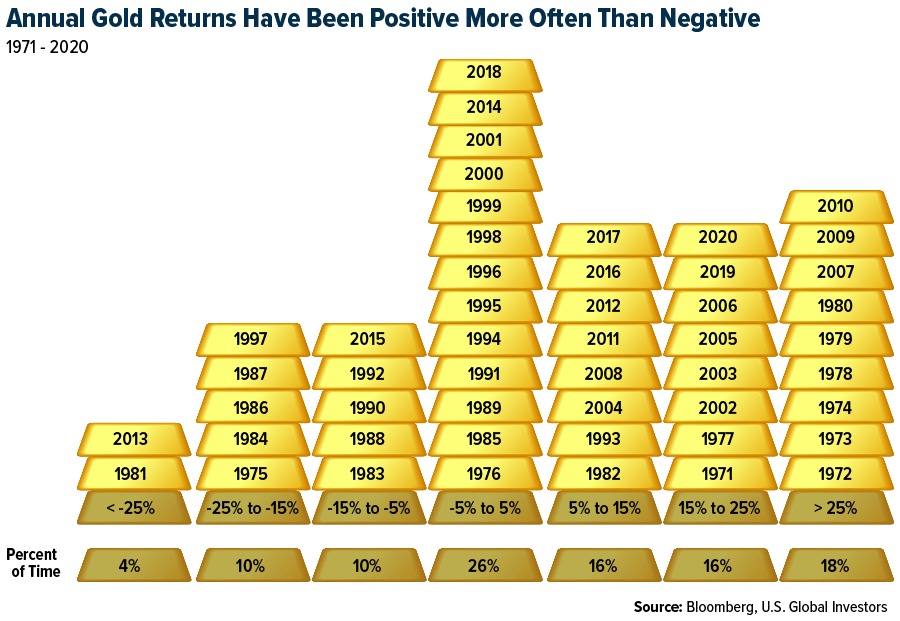

As you know, I’ve always recommended a 10% weighting in gold and gold mining stocks for this very reason. Some readers may rightfully point out, though, that gold is set for a loss this year. As of today, it’s down about 5.8% year-to-date, which would be the metal’s deepest plunge since 2015.

However, if we step back, we see that gold has been positive for the year far more often than it’s been negative. In several instances, it’s significantly outperformed inflation. In fact, had inflation been at 6.8% every year from 1971 to 2020, gold would have beaten it half of the time. Since 2000, 62% of the time.

Bitcoin adoption will accelerate even more.

That brings me to Bitcoin, which I also believe is a fabulous hedge against inflation. The cryptocurrency saw an incredible surge in adoption in 2021, and I see the rate accelerating even more in 2022.

A new survey by Grayscale Investments appears to confirm this. More than half (55%) of all current Bitcoin investors said they began participating in just the last 12 months, the firm found. Let’s say another 55% admits to the same at the end of 2022. The compounding effect would be incredibly massive as even more people joined a network for an asset whose supply is capped at 21 million.

As Bloomberg’s Mike McGlone put it in a note to investors this week, “Demand and adoption are rising and still appear in the early days versus supply, which is declining.” The analyst sees $100,000 Bitcoin as “good target resistance,” which I agree with.

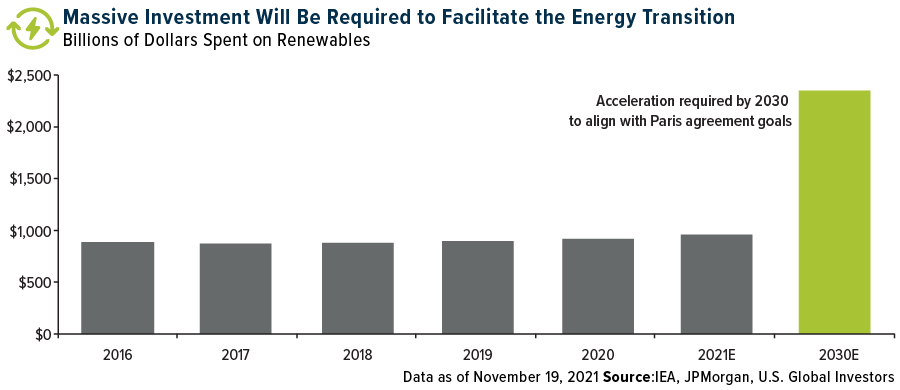

Spending on the energy transition is about to blow up.

The transition to net-zero carbon pollution energy has been with us for years now, but 2022 may be a red-letter year for federal spending on renewables, battery technology and more, with huge implications for investors.

This week, President Joe Biden signed an executive order directing the federal government to invest in renewables in its quest to go completely “green.”

It won’t be an easy (or cheap) task. The government owns some 300,000 buildings and controls a fleet of more than 600,000 cars and trucks.

Each goal has a different due date. By 2030, 100% of the federal government’s electricity must be generated through carbon pollution-free means (think wind and solar). Five years later, all new vehicle purchases must be of zero-carbon emission cars and trucks. By 2045, all federal buildings must be retrofitted and refurbished.

The U.S. isn’t alone, of course. Germany’s new chancellor, Olaf Scholz, vows to expand spending on renewable energy and phase out coal by 2030. It’s been estimated that for renewables to replace fossil fuels, global investment must triple between now and the end of the decade to around $2.3 trillion per year.

As I’ve said many times before, the opportunities aren’t limited to the companies that manufacture and install wind turbines and solar panels, though we like a few of them, including Canadian Solar and Siemens Gamesa.

Remember, these projects will require incredible amounts of strategic metals and minerals, and this should benefit producers and explorers. Our favorites include Ivanhoe Mines (copper), NanoXplore (graphene) and Standard Lithium (lithium), as well as battery materials and technology companies First Cobalt and Nano One Materials.

Supply chain issues will persist.

A huge contributor to inflation right now is the ongoing supply chain snarls that were trigged by the pandemic and that have caused all sorts of shipping and logistics delays across the globe. U.S. ports, and those in Los Angeles and Long Beach in particular, are at a disadvantage compared to others because they have not yet embraced robotics and automation. Most ports around the world use automated cranes and trucks, something U.S.-based longshoreman unions have resisted. As a result, it can take twice as long to unload a ship in L.A. as it does in Rotterdam or Shanghai.

This has given container shipping companies a major headache, but it’s also helped fill their coffers. This year, the industry is set to make a collective $150 billion in profits, a new record, according to maritime research firm Drewry. Next year, earnings could be even more, analysts believe, so there could still be time to start participating.

Click here to watch our video on the four reasons why we’re bullish on global cargo and shipping names!

Index Summary

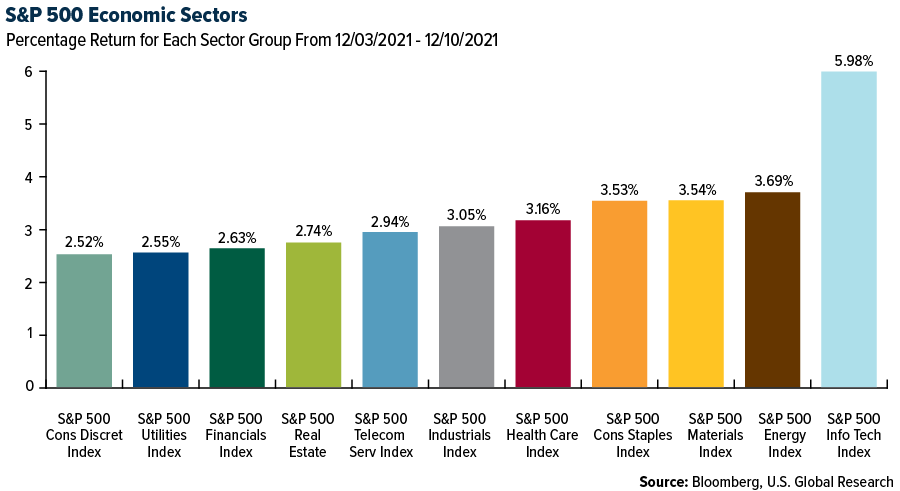

- The major market indices finished up this week. The Dow Jones Industrial Average gained 4.02%. The S&P 500 Stock Index rose 3.82%, while the Nasdaq Composite climbed 3.61%. The Russell 2000 small capitalization index gained 2.43% this week.

- The Hang Seng Composite gained 0.77% this week; while Taiwan was up 0.73% and the KOSPI rose 1.41%.

- The 10-year Treasury bond yield rose 0.14 basis points to 10.41%.

Airline Sector

Strengths

- The best performing airline stock for the week was GOL, up 7%. European airline bookings were sharply up in the week, with strong growth in both intra-Europe and international. This is despite ongoing concerns over the spread of the Omicron variant, which has led to increased travel restrictions. Intra-Europe net sales increased by 7 points to -40% versus 2019 (versus -47% in the prior week) and grew by 15% this week. International net sales were up by 2 points to -42% versus 2019 (versus -44% in the prior week) and increased by 17% this week to reach a new post-pandemic peak. This led to a 4-point increase in system-wide net sales for flights booked in Europe to -42% (versus -45% in the prior week).

- Overall fare trends surveyed for the scheduled domestic U.S. air travel this week showed a sharp surge as average close-in (one-week out) fares gained 54.3% this week, albeit off a low base and ahead of the peak year-end holiday travel season. Notably, the leisure (4-week out) fares reflecting the peak year-end holiday booking period partly explains the exceptionally strong fare momentum this week. The current level also reflects a resilient domestic U.S. demand (in business and leisure) with airlines able to push through higher fares, helped in part by a pent-up demand from a depressed 2020 holiday season and with capacity levels still slightly below 2019.

- Southwest Airlines increased its fourth quarter revenue outlook from down 10% to -15% versus 2019 compared to its initial guide of down 15% to -25%, driving profitability in the fourth quarter. Strong leisure demand, (a positive for all airlines), and a solid operation had the company tracking towards the better end of its prior revenue outlook, while a new credit card agreement with Chase drove the upside to its original guide.

Weaknesses

- The worst performing airline stock for the week was Mesa Air, down 15.7%. European flight activity declined by 2 points to -25% versus 2019 in the week (from -23% in prior week), with low-cost carriers and Austrian Airlines showing the largest declines. Wizz Air’s European flight traffic is now trending at 72% of 2019 levels, down from 110% in October. Daily website visits for E.U. airlines were down by 7 points to -19% versus 2019 (versus -11% in the prior week). Traffic declined for all airlines except easyJet, which had a 3-point increase likely due to its full year results announcement.

- Flight interest, based on Google search trends data on a year-to-year basis, trended down across the board globally. Since the bottoming in overall year-to-year search trends early this year, the U.S. has consistently fared better than Canada and China.

- System net sales decelerated to down 36.5% versus 2019 (versus the prior two weeks of down 32%). Over the past week, TSA throughput has eased back to 80 to 85% of 2019 levels after reaching a peak of 90% of pre-pandemic traffic over the Thanksgiving holiday weekend.

Opportunities

- According to International Statistical Institute (ISI), airlines remain early cycle from a demand recovery perspective, (upside based on normalization, recoupling with strong nominal GDP). Many innings remain in their view. The tougher buckets to normalize, (corporate, long-haul international), remain sources of longer-term potential, in their view.

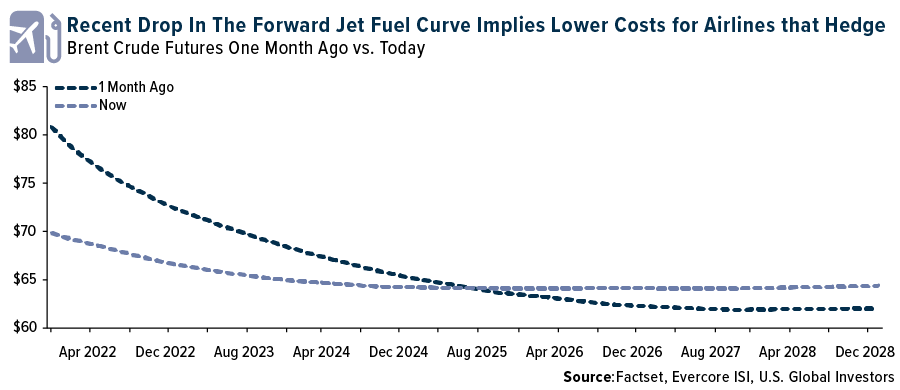

- Oil, which is a raw material for jet fuel, has come down dramatically over the past two weeks. The following graph shows that expected prices over the next four years have come down dramatically. This could benefit airlines that hedge.

- According to Bank of America, they attended Azul’s investor day, with the presence of its entire top management team. Overall, Azul provided a positive message, despite sector headwinds. Key topics included: 1) an upbeat tone on capacity recovery and yields performance; 2) the benefits from its fleet transformation program; and 3) possible tailwinds from the Congonhas auction, (which would add more slots). Management continued to share a positive view on the market recovery, with Azul reaching 120% of fourth quarter of 2019 capacity in the fourth quarter of 2021, while decent yields are likely to continue, given pent-up demand on the leisure side and the needs for fare readjustments.

Threats

- EasyJet has seen a recent softening of demand from the new variant, but a smaller impact than with previous new strains. Ryanair expects a challenging Christmas period but is optimistic about next summer with pent-up demand. Wizz Air noted that passengers are booking at even shorter notice. Meanwhile, United has warned that Omicron is a threat to transatlantic travel and the airline could have less flying in January. Countries continue to tighten travel restrictions, with France requiring all non-E.U. arrivals to provide a test, Ireland mandating a test for all arrivals and the U.S. shortening the time window for testing, although all accept rapid antigen tests. The U.K. introduced a requirement for pre-departure tests for all arrivals and added Nigeria to its ‘red list’.

- COVID-related negative headlines are likely to continue to pressure airlines shares in the near term, until more is understood about the omicron-variant or possibly until U.S./Europe COVID cases peak and start to decline again. This includes new travel restrictions that, except for those placed on travel to/from select African countries, have been relatively restrained/reasonable in most cases in North America and Europe. U.S. airline exposure is minimal to Africa, particularly Southern African countries subject to newly implemented travel restrictions, while European airline exposure is more material, particularly at Air France-KLM and IAG. Schedule data this week shows notable close-in December cuts to/from Africa among European airlines, most pronounced at Ryanair.

- The United States tightened Covid testing requirements for all international inbound air travelers. Last week, the Centers for Disease Control and Prevention (CDC) announced the revision of the Global Testing Order amid the recently detected Omicron variant, shortening the timeline for Covid testing to one day prior to departure for U.S.-bound international air travelers. Previously, in-bound international travelers were required to receive a negative Covid-19 test no more than three days before departure. This strengthens already strict protocols that have been put in place for international travelers, including requirements of being fully vaccinated. The shorter timeline for receiving a negative Covid test could pose challenges in some parts of the world as some travelers may not have access to fast and reliable tests.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 6.55%. The best performing country in Asia this week was Thailand, gaining 2.7%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 0.59%. The Thailand baht was the best performing currency in Asia this week, gaining 0.80%.

- The year-to-date budget balance in Russia increased to 2,337.6 billion rubles in November from 2,140.1 billion in October, well above the expected balance of 1,904.1 billion rubles.

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 3.9%. The worst performing country in Asia this week was Malaysia, losing 0.19%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 1.1%. The Vietnamese dong was the worst performing currency in Asia this week, losing 0.74%.

- The European Sentix Investor Confidence Index fell from 18.3 to 13.5 for December, however, the latest reading was better still than the estimate that it would fall to 12.5.

Opportunities

- There has been a positive spin surrounding the recent headlines out of China. On Monday, the People’s Bank of China (PBOC) cut the reserve requirement ratio (RRR) for banks by 50 basis points, a move that will set free liquidity and provide support for small businesses.

- S. President Biden held a video summit this week with Russian President Putin. Biden voiced “deep concerns” about the Russian forces around Ukraine and said the U.S. and its allies would respond with strong economic and, possibly, martial measures should the situation escalate. This could be a first step to end the recent geopolitical tensions created through the news that Russia is building up its military presence on the border with Ukraine to potentially overtake the nearby nation.

- Olaf Scholz is now officially chancellor of Germany, concluding Angela Merkel’s 16-year governance. He was elected on Wednesday by Germany’s federal parliament with 395 votes in favor, 303 votes against and six abstentions. Scholz has promised to make Germany, (currently Europe’s biggest economy), greener, fairer, and more modern.

Threats

- In China, Kaisa Group shares were halted in Hong Kong as concerns grow over its ability to make a repayment on a $400M note due December 7. Evergrande is planning its restructuring, meanwhile Aoyuan, along with several other Chinese developers, warns they may also not be able to make interest repayments.

- The European Union (EU) is unlikely to approve the disbursement of pandemic aid to Poland and Hungary this year, a top official said on Tuesday, in a sign that the conflict over the rule of law is not yet close to resolution. Poland’s request for 36 billion euros from the EU’s recovery fund has been locked in a dispute over the government’s judicial revamp. The EU is also in talks with Hungary to address some outstanding elements before it approves its 7.2-billion-euro request for grants.

- According to Bloomberg, White House Press Secretary Jen Psaki told reporters that U.S. government officials will boycott the Beijing Winter Olympics in February 2022, due to concerns about “crimes against humanity” and other human rights abuses. Stopping short of a full-blown boycott, a diplomatic boycott means that athletes are free to compete. Psaki said that the officials staying home sends a “clear message” that “business as usual” isn’t appropriate in this case and won’t be accepted due to the U.S.’s concerns over human rights violations reportedly happening in China.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was lumber, up 17.93%. Lumber continued to record strong gains as mill supplies tightened with producers extending order files into early January. Lumber ended the week up 16% at $745, up 22% relative to the third quarter and up 14% year-to-year. Pricing picked up steam in the back half of the week, fueled by ideal weather generating increased lumber consumption while staffing issues and log shortages continued to weigh on inventories at the mill level.

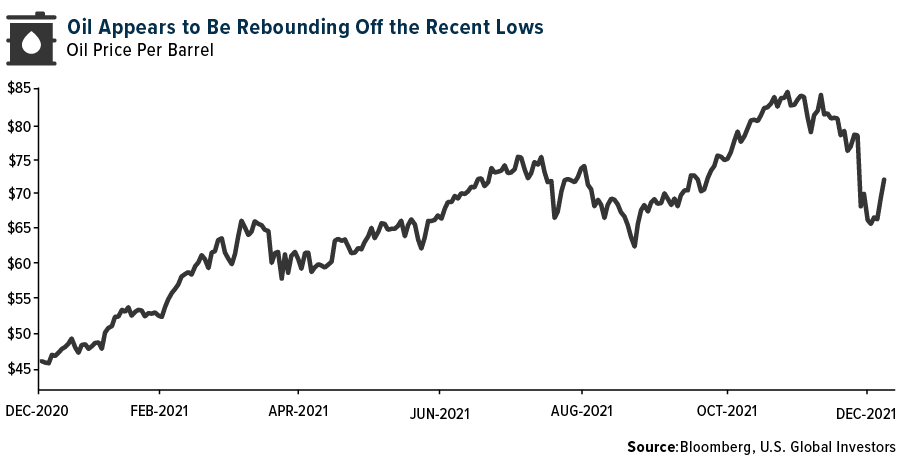

- Oil rose after Saudi Arabia boosted the price of its crude, signaling confidence in the demand outlook despite the spread of the omicron variant of the coronavirus. Futures in New York advanced near $68 a barrel. The kingdom increased its oil prices for customers in Asia and the U.S. for January, just days after the OPEC+ alliance agreed to boost output for the same month. Prices for its high-sulfur barrels in Asia were the highest since at least 2000.

- Firefinch Ltd. completed a $100 million placement to go towards its regional development of its gold project Morilla and exploration and other costs at lithium project Goulamina. Plans are to spin out the Goulamina asset to current shareholders as a separately listed company early next year. The Goulamina Lithium Project (GLP) was the subject of a recent Definitive Feasibility Study (DFS) which delivered a Net Present Value (NPV) of A$4.1 billion with 83% Internal Rate of Return (IRR). GLP has the potential to be the third largest lithium producer globally.

Weaknesses

- The worst performing commodity this week was uranium, down 30.73%, failing to maintain the price levels attained at the start of the of the month when Uranium Royalty Corp. entered into a stream agreement referencing $47.74 per pound for 500,000 pounds.

- European natural gas futures jumped as traders weighed the risk of fresh international sanctions against top supplier Russia should it invade Ukraine. President Joe Biden warned Russian President Vladimir Putin against the move or risk severe economic penalties, including banking sanctions. The increased tension adds to existing worries over Russian supplies to the European Union, which has already been sharply curtailed in recent months.

- Tsingshan Holding Ground brought new nickel production online in Indonesia, which could upend the nickel market with more supply coming online to service the nickel demand the battery industry is seeking. Nickel prices slid 2% on the news.

Opportunities

- Raymond James says its bullish oil view over the next few years not only remains firm but is increasing. The firm’s new price deck envisions West Texas Intermediate (WTI) crude starting 2022 at $70/barrel, averaging $75 for 2022, reaching $80 by the fourth quarter and staying at that level for 2023. There are several reasons for remaining bullish in the face of current uncertainty: (1) Low global inventories, (2) visible recovery in demand, (3) the coming collapse in OPEC+ spare capacity and (4) the need for a higher price to further incentivize U.S. supply.

- According to Morgan Stanley, milder weather and rising supply have driven Henry Hub prices lower, with the 2022 strip now close to its unchanged $3.75 forecast. The bank’s weather scenario assessment shows risks skewing to the downside, but some potential for upside volatility remains.

- China’s stainless-steel output reversed up in November after sliding for four months, with the total volume jumping by 15.2% from October to 2.6 million tons, according to Mysteel’s latest survey among the country’s 32 domestic stainless mills. The easing of power curbs in many regions was behind the rise, sources said. Production of all grades of stainless increased to varying degrees last month as power rationing among stainless producers eased further in provinces such as Southeast China’s Fujian, South China’s Guangdong and Southwest China’s Guangxi.

Threats

- The three to four times increase in fertilizer prices in the last year has increased the challenges for traders to secure bank financing. For potash sourced from Belarus, this challenge has increased further from new U.S. sanctions against Belarus by the U.S. Treasury’s Office of Foreign Assets Control (OAFC). This is likely to impact traders’ access to bank financing in many regions of the world, not just for U.S. imports. This creates further challenges for Belaruskali beyond the limited access to E.U. ports.

- Anglo American lowered production guidance for most of its commodities for next year and flagged that capital spending will rise higher than previously expected. This comes on the heels of Rio Tinto and Vale SA having missed or cut their forecasts recently.

- Elon Musk recently commented about how a future scenario with China. Its economy is on a path to be three times the size of the U.S. and those currently in power came of age when its economy was small and they may have felt “pushed around a lot.” “They haven’t fully appreciated the fact that China really is going to be the big kid on the block,” Musk said. “You can really be pretty chill about things. Other countries are not really a threat to you if you’re by far the biggest kid on the block. That’s an important mindset change.” This sheds some light on why China has been so aggressive in acquiring access to natural resources around the globe. With lithium, the new energy metal of the future, Chinese companies have interest and or offtake agreements with nearly every new project to supply its future needs.

Domestic Economy & Equities

Strengths

- October job openings were reported up 595,000 month-over-month to 11,033,000 breaking two-straight monthly declines and beating estimates for 10,425,000.

- The Market Composite Index, a measure of mortgage loan application volume, increased 2.0% on a seasonally adjusted basis from one week earlier. Mortgage rates declined for the first time in a month, prompting a pickup in refinancing, with government refinances increasing more than 20% over the week. While the 30-year fixed mortgage rate and 15-year fixed mortgage rate both declined only one basis point.

- Norwegian Cruise Liner was the best performing S&P 500 stock for the week, increasing 17.91%. Cruise-ship operators led a rally in travel-company stocks, followed by airlines, casinos, and hotels, on reopening optimism after Pfizer and BioNTech said initial lab studies show a third dose of their Covid-19 vaccine may be effective at neutralizing the omicron variant.

Weaknesses

- Inflation increased to 6.8% in November from 6.2% in October on a year-over-year basis. Inflation, excluding energy and food process, rose to 4.9% from 4.6% on a year-over-year basis.

- Initial jobless claims for the latest week came in at 184,000, better than the consensus of 224,000 and last week’s upwardly revised 227,000. It is the lowest weekly level since September 1969.

- Moderna, a pharmaceutical company, was the worst performing S&P 500 stock for the week, losing 16.78%. Shares declined after results from its experimental seasonal flu shot appeared similar to another vaccine on the market.

Opportunities

- Manufacturing PMI should stay well above the 50-mark, a level that separates growth from contractions. The preliminary December manufacturing data will be released December 16.

- Pfizer and BioNTech issued a release on Wednesday morning that noted that preliminary laboratory studies demonstrate that three doses of their Covid-19 vaccine neutralize the Omicron variant. In addition, the White House has ruled out the need for lockdowns or restrictions in response to the current COVID-19 trends.

- The Senate voted to allow Congress to raise the debt ceiling with a simple majority vote. The Senate and House will have to hold separate votes to increase the debt ceiling. Both chambers are expected to hike the limit early next week before the December 15 deadline.

Threats

- Goldman Sachs cut its forecasts for U.S. growth, alluding blame on the Omicron variant. Gross domestic product (GDP) will rise 3.8% this year, down from 4.2%. The bank’s 2022 estimate was cut to 2.9% from 3.3%.

- Bloomberg cited a non-peer reviewed study by a Japanese scientist showing the Omicron variant to be four times more transmissible than the Delta variant. The results were based on an analysis of genome data from South Africa’s Gauteng province and shows that Omicron evades immunity acquired naturally and through vaccines.

- Despite initially announcing plans to taper asset purchases just five weeks ago, we expect the Federal Open Market Committee (FOMC) to start reducing its asset purchases at a faster pace at next week’s meeting. Wall Street is looking for Fed to reduce purchases by $30 billion a month, double the pace it announced at the last meeting, FactSet reported.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Prince Floki V2 (PrinceFloki), rising 26,594.31%.

- Bitcoin gains after consumer price index (CPI) increase renews, further fueling the inflation-hedge argument, writes Bloomberg. The largest cryptocurrency has long been touted as an inflation hedge, in part because of its fixed supply.

- Nigel Green, the CEO of deVere Group, is confidently buying the recent dip on Bitcoin, writes Value Walk. Green’s comments come after Bitcoin slipped around 6% on Thursday, following its inability to hold at the 50K level.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was GMR Finance (GMR), down 98.01%.

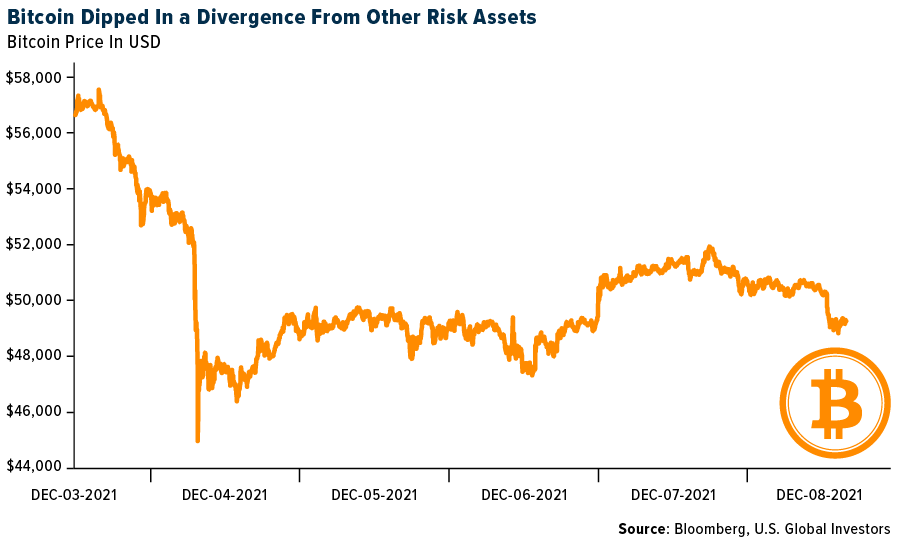

- Bitcoin resumes its slide after breaking back below the $50,000 level. The largest cryptocurrency by market value declined as much as 3.7% to $48,685 this week. Ethereum, Solana, Cardano and Shiba Inu tokens also fell this week. The Bloomberg Galaxy Crypto Index slumped about 1.8%, writes Bloomberg.

- Bitcoin and other cryptocurrencies dove this weekend as much as 20% amid a greater risk-off sentiment that also encompassed selloffs in many areas of the U.S stock market. It happened as spiking inflation is forcing central banks to tighten monetary policy, threatening to reduce the liquidity tailwind that lifted a wide range of assets, writes Bloomberg.

Opportunities

- Coinbase Global Inc launched its first yield product that allows users outside the U.S to earn interest from their holdings in stablecoin through a third-party decentralized finance platform, writes Bloomberg.

- Binance is seeking to establish an exchange in Indonesia with recent partnerships. Binance has announced it is in talks with Indonesia’s PT Bank Central Asia and PT Telkom, according to an article published by Inside Bitcoins.

- Indian Prime Minister Narendra Modi will take the final decision on cryptocurrency regulation, according to Bitcoin News. A high-level meeting is reportedly being held on cryptocurrency regulation in India. All options are being explored, including full and partial regulation as well as potentially a complete or partial ban.

Threats

- Thieves siphon $196 million of crypto from Bitmart, according to an article published by Bloomberg. The hackers helped themselves to $100 million worth of cryptos on the Ethereum network and $96 million on the Binance Smart Chain, by stealing a private key that gave them access to two of their hot, or active, wallets.

- Bitcoin’s latest plunge highlights the danger of a crypto salary. If you’re paid in Bitcoin, then your entire paycheck shrank by more than 20% when the token fell that much on Saturday. That rapid plunge highlights just one peril of a nascent trend that’s being hyped up by politicians and celebrities who are currently being paid in digital currencies, writes Bloomberg.

- Cryptocurrency is the ‘Top Contender’ for correction, money managers say. By many counts, 2021 was the year cryptocurrencies were finally embraced by institutions. Now those same money-managers say the asset class is ripe for a big selloff next year. Digital assets will have a major correction in 2022 with nearly three-quarters of institutions saying they’re not an appropriate investment for most retail investors.

Gold Market

This week spot gold closed the week at $1,782.84, down $0.45 per ounce, or 0.03%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.72%. The S&P/TSX Venture Index came in up 1.32%. The U.S. Trade-Weighted Dollar rose/fell 0.05%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-7 | Germany ZEW Survey Expectations | 25.4 | 29.9 | 31.7 |

| Dec-7 | Germany ZEW Survey Current Situation | 5.7 | -7.4 | 12.5 |

| Dec-9 | Initial Jobless Claims | 220k | 184k | 227k |

| Dec-10 | Germany CPI YoY | 5.2% | 5.2% | 5.2% |

| Dec-10 | CPI YoY | 6.8% | 6.8% | 6.2% |

| Dec-14 | PPI Final Demand YoY | 9.2% | — | 8.6% |

| Dec-14 | China Retail Sales YoY | 9.2% | — | 8.6% |

| Dec-16 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Dec-16 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Dec-16 | Initial Jobless Claims | 200k | — | 184k |

| Dec-16 | Housing Starts | 1,568k | — | 1,520k |

| Dec-17 | Eurozone CPI Core YoY | 2.6% | — | 2.6% |

Strengths

- The best performing precious metal for the week was platinum, up 1.01%, likely responding to substitution demand. The Perth Mint said gold coin and minted bar sales totaled 115,872 ounces last month, the highest since March, according to figures on its website. Sales surged 94% in November from 59,750 ounces in October, according to previously released data. Sales rose due to an increasing appetite for physical bullion and the release of the Perth Mint’s 2022-dated Australian Kangaroo series, said Neil Vance, general manager of Minted Products.

- Bloomberg reported Former Treasury Secretary Lawrence Summers said that U.S. policy makers, by allowing the economy to overheat, have likely cemented inflation rates of 4% or higher, way beyond their long-term target. Summers said on Bloomberg Television’s “Wall Street Week” with David Westin. “We’re going to entrench inflation way above 2% – perhaps in the 4% or even higher range.”

- Nomad has agreed to co-invest with Orion Mine Finance in a $200 million gold stream on the Platreef PGM project in South Africa. Nomad will pay $75 million for its portion of the gold stream. Platreef is a top tier asset with multi-decade mine-life and potential upside on exploration and future production expansion to become among the largest gold producers. Phased development is targeting initial production by 2024.

Weaknesses

- The worst performing precious metal for the week was palladium, down 2.92%, still trading off on the switch to platinum for some of the loading of auto catalyst. Deaths in South African mines, which include the world’s deepest gold and platinum operations, rose for a second consecutive year as worker safety deteriorated. The toll so far in 2021 was 69, up from 48 a year-earlier, the Department of Mineral Resources and Energy said in a statement Monday. In 2019, 51 people died over the whole year, the lowest number of fatalities on record, before climbing to 60 last year.

- The head of the Ministry of the Environment (Semarnat), María Luisa Albores, affirmed that the illegal methods that mining companies have used to establish themselves, with the complicity of past governments, have generated socio-environmental conflicts in various regions in Mexico. She stressed that in the current administration no new mining concessions have been granted and that, as ratified by President Andrés Manuel López Obrador in his message on December 1, it is not planned to do so for the rest of the six-year term.

- Ascot Resources announced the B.C. Ministry of Energy, Mines and Low Carbon Innovation has issued the Mines Act Permit for construction and operation of the Premier Gold Project. The long-awaited permit was originally expected in the summer and allows underground development. However, management is pushing back full-scale construction and underground development to April 2022 due to high snowfall levels. As well, the clarifier and thickener components were lost at sea enroute from China and additional time is required to fabricate and ship replacement components.

Opportunities

- Dolly Varden Silver Corporation and Fury Gold Mines Ltd are pleased to announce that the companies have entered into a definitive agreement pursuant to which Dolly Varden will acquire from Fury, through the acquisition of Fury’s wholly owned subsidiary, a 100% interest in the Homestake Ridge gold-silver project located adjacent to the Dolly Varden Project in the Golden Triangle. The Homestake Project hosts a resource estimated to contain 165,993 ounces of gold and 1.8 million ounces of silver.

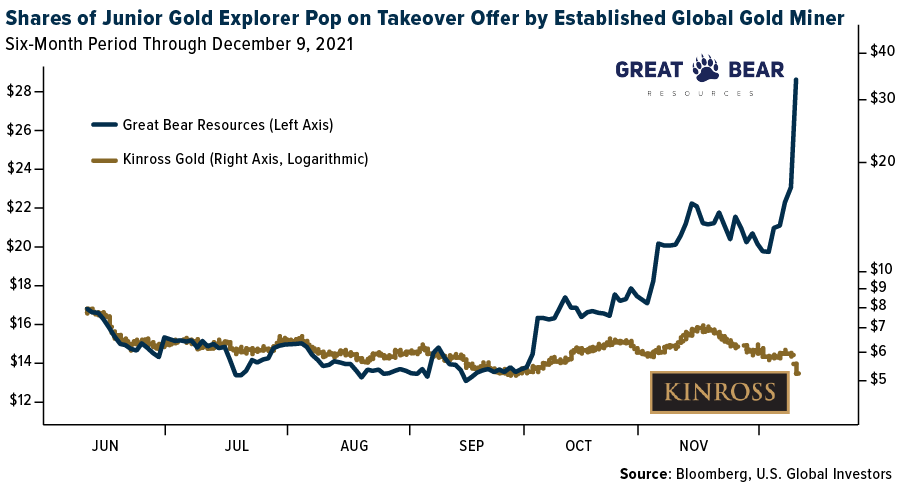

- The major miners have returned to the bidding table to acquire assets. Kinross announced it entered into a definitive agreement to acquire Great Bear Resources, which owns the Dixie project in the Red Lake district in Ontario, Canada. Kinross will pay $1.4 billion upfront, representing C$29.00 per Great Bear share, a 26% premium to the closing price. Great Bear shareholders will have the option to determine the cash/stock split of the $1.4 billion upfront payment (up to a maximum of 75% cash and 40% Kinross shares). The share price chart below shows the relative performance that investors experience leading up to the takeout announcement. Currently, there are no true junior mining ETFs available for investors but some mutual funds in the precious metals category do have significant exposure to their tier of the market.

- Nano One recently added Dr. Gao as a strategic advisor on the cathode business and supply chain. Dr. Gao is also an internationally recognized expert in lithium-ion battery materials with over a hundred patents issued around the world, dozens of journal publications and his innovations are at the core of today’s lithium-ion batteries. “As the global production of lithium-ion battery materials grows to millions of tons,” said Dr. Gao, “we will need technological innovation to eliminate environmental waste, economic inefficiencies, and complexity that persist in today’s battery supply chain. For this reason, I am inspired by what I’ve seen at Nano One over the years, and I am pleased to be collaborating with them on their technology and commercialization efforts.”

Threats

- The Court in Turkey’s Canakkale province canceled a positive environment impact assessment report given by government for the Karapinar gold and silver mine project, Koza Altin said in exchange filing.

- Bitcoin remains a key competitor to gold. Like gold, Bitcoin functions as an absolute store of value. There is a finite amount of gold in the earth’s crust, and it becomes progressively more difficult to mine over time, just like Bitcoin. Gold also serves as protection against the systematic abuse of fiat currencies by governments and central banks, which tend to create progressively more supply.

- As posted to the Mining Journal this morning, miners’ unions in South Africa have come out swinging against Sibanye-Stillwater, suggesting a business rescue plan and slamming its vaccination policy and increase in fatalities. The National Union of Mineworkers has joined Solidarity in suggesting the miner might need business assistance, as gold wage claims remain unresolved and headed for strike action. Sibanye-Stillwater has said it would not be intimidated into acceding to above-inflation demands that would compromise the sustainability of its gold operations and stakeholders.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits