Reflation, supply chains, China's slowdown, labor markets, living with COVID-19 and bigger government were prominent stories of the year.

Editor’s Note: This week, we look back on the most prominent stories we covered this year. Somehow, we suspect we’ll be talking about them even more in 2022.

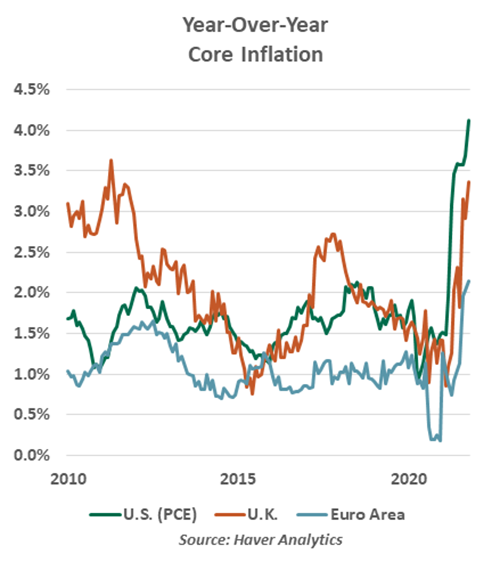

Reflation

For a decade prior to the pandemic, inflation was quiescent. During that time, economies around the world enjoyed very strong growth that brought unemployment down to very low levels. Monetary policy tightened, but money supply growth remained robust. These two factors, which have historically been triggers for higher inflation, proved much less potent.

Secular factors such as keen competition, supply chain efficiencies and e-commerce were credited for keeping a lid on prices. While good for consumers, these elements frustrated central bankers seeking to reach inflation targets. To reinforce their commitment to heading off disinflationary expectations, monetary authorities have changed their operating principles over the past several years to allow inflation to run high after long periods of running below target. Those new principles are being sternly tested, much sooner than anticipated.

When inflation began to surge as the economy reopened in 2020, it was easily dismissed as fleeting. Only a handful of categories were stressed. Demand had been boosted by stimulus, but supply would certainly rise to the occasion. Eighteen months later, the supply of goods and labor still has not fully responded; inflation has broadened and increased. The Chairman of the Federal Reserve conceded recently that it was time to retire the word “transitory” when describing the current condition.

The changing calculus around the price level was arguably the most significant economic story of the year. Assumptions made by businesses about costs and by investors about real returns are undergoing important recalibration. And major central banks are scurrying to change their timelines for removing policy accommodation: the Bank of England is likely to raise its interest rates within the next few months, while we now expect the Fed to follow at midyear 2022.

Our global forecast for the new year anticipates that inflation will settle over the coming quarters as supply chains unkink and idle workers return to the labor force. As well, the secular forces which were so powerful in the last decade should eventually reassert themselves. But the risks to inflation seem aligned to the upside, which could land this topic back on the top stories list twelve months from now.

Supplies Chained

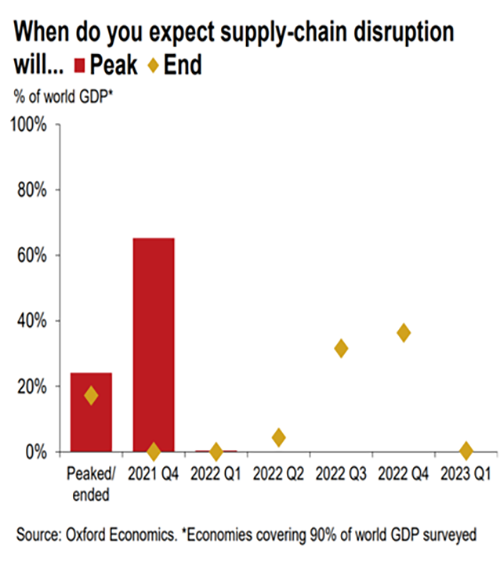

Ever since COVID-19 first surfaced in China, global supply chains have been in a state of turmoil. The disruption to the global flow of goods began with an outbreak in China ─ the world’s factory, but as the virus spread to other parts of the world, it became apparent that China wasn’t the only player with the potential to create bottlenecks. This year’s supply-side problems have been aggravated by closures of plants and ports amid outbreaks in other hubs.

For most of the year, businesses depleted their inventories, with blockages limiting manufacturers’ ability to get goods out of their factory gates. Delivery and lead times stretched out to new highs. Container shortages complicated the flow of parts and finished goods, leading to skyrocketing shipping costs. Idiosyncratic events like a cargo ship blocking the important Suez Canal for more than a week only made matters worse.

With demand for everything from raw materials to semiconductor chips to finished goods running well ahead of supply, production networks have come under persistent pressure. Many corporations have been passing on higher costs to consumers, contributing to a surge in inflation in several major economies.

|

It may take quite a while to untangle supply chains.

|

Re-shoring of supplier networks has garnered increased attention. However, it is easier said than done. No nation is self-sufficient, and each country enjoys a comparative advantage in producing certain types of goods. Moving production lines out of low-cost centers will add to the burden for businesses. Rearranging value chains can also be a time-consuming process that requires coordination, collaboration across markets and big financial investments.

Supply chain disruptions are likely to persist well into 2022, partly because of the resurgence of COVID-19. Over the longer term, expect a reshuffling of trade strategies, but a complete overhaul is unlikely. A return to normal may also weaken our resolve to make changes. As stated by Willy C. Shih, an international trade expert from Harvard Business School: “consumers won’t pay for resilience when they are not in crisis.”

China Changes Gears

For many years, the Chinese government apparatus has given priority to accelerating growth in gross domestic product (GDP) to highlight the country’s economic development. However, in recent times, Beijing has refocused on quality over quantity. Unfortunately, the emergence of new challenges has periodically pushed policymakers backwards.

2021 could be regarded as the year of regulatory reset in China, as the government embraced the program of “common prosperity” and attempted to reign in financial excesses. However, the ongoing pandemic and spillover effects from reform efforts have complicated the transition.

Tighter rules on the property market and a focus on deleveraging have taken a toll on the Chinese economy. Pursuing climate/energy efficiency goals has contributed to widespread power shortages, which have forced some producers to cut back output. Uncertainty around COVID-19 and the effectiveness of domestically produced vaccines has held consumption back. Concerns over rising defaults and the ongoing Evergrande crisis triggering a systemic financial risk have left market participants jittery. Shortages and higher input costs amid supply-side challenges have added to the economic strain.

The downward pressure on the economy appears to be driving another policy U-turn. The People’s Bank of China cut banks’ capital requirements this week, the second reduction this year. China faces a prolonged period of slower growth, and the risks of a hard landing could force the government to ease policy more forcefully than it may have preferred. Looser restrictions on the important housing market, including lowering mortgage rates, and a return to setting growth targets, cannot be ruled out in 2022.

Firm guidance is easy to announce but painful to execute. Chinese policymakers are learning this the hard way as they continue to buckle under the threat of immediate economic slowdown. By doing so, they may be altering their longer-term prospects.

Labor Leverage

Worker empowerment is an important topic in U.S. history classes. Curricula often include Sinclair’s The Jungle and accounts of the rebellions a century ago yielding worker protections that persist to this day, like minimum wages, overtime limits and occupational safety regulations. Before the pandemic, the labor market had settled into a less contentious equilibrium, with employers in control of hiring, wage-setting, and termination. Today, those rules are changing.

Newly empowered workers are setting their own paths. Much coverage throughout the year focused on the “Great Resignation,” a trend of workers quitting, but not all quits are alike. A portion of those resignations were early retirements, older workers taking COVID-19 (and rapid asset appreciation) as their cue to step out of their jobs. Retirement need not be permanent; after a hiatus, many of those workers may find themselves back to work as opportunities beckon and savings are depleted.

|

Many workers quit their jobs, but often to take better roles.

|

Rates of quitting and vacancies (job leavers and job openings as a share of total employment) are certainly elevated across most economies. Observing quits alone obscures the other side of employment: Hires have also risen. Many of the quits represent workers moving on to take other opportunities. For example, through October, the U.S. leisure and hospitality sector witnessed an estimated 7.8 million quits but also 12.6 million hires. Higher turnover is a sign of spirited competition, not dysfunction.

Employers struggled to recruit lower-paid and seasonal workers. The year-ago debate about the appropriate federal minimum wage was answered by the market, as employers are advertising high starting wages, benefits, and flexibility. When one prominent employer raises wages, all employers in that market must respond or risk attrition. Teenagers had their best summer of employment in 20 years, and now are even being recruited for previously off-limits work like truck driving. Low immigration flows are also depleting the supply of workers.

Temporary supports like stimulus payments, expanded unemployment, furloughs and work-sharing have run their course. The labor market is recovering, but it will remain more competitive. While it is too soon to call this a realignment for the history books, workers have the upper hand for the first time in a long time.

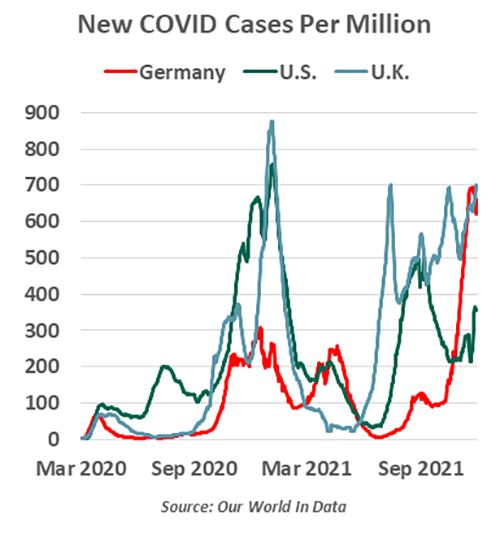

COVID-19: From Carrots To Sticks

Germans have experienced COVID-19 very differently than Americans have. Proof of vaccination or recovery is required everywhere, from Christmas markets to pubs. Their experience is one of a range of data points that illustrate how the world is seeking to live with COVID-19.

A repeated refrain in Germany is 3G: Geimpft, Genesen, Getestet—vaccinated, recovered, and tested. Employees of every restaurant, nonessential retailer, and tourist attraction ask for evidence of vaccination or recovery. Some crowded quarters require a negative test; testing centers are free and ubiquitous, with results sent in 15 minutes. All children are tested regularly at school. Local residents show their status with an app; tourists present paper documents, which are inspected closely.

|

COVID-19 is not going away quietly, and we’ll have to learn to live with that.

|

In areas that adopted 3G controls, life mostly returned to normal. Ubiquitous masks and checks of paperwork were a change but did not impair the reopening. A sense of confidence was starting to return, until recently. Despite Germans taking every reasonable measure to manage the pandemic, the nation has entered a winter viral surge. Local activity restrictions are returning; most regrettably, some of the nation’s iconic Christmas markets have now been closed for two years.

Across the world, COVID cases are on the rise again, especially among the unvaccinated. Mild infections are livable, but increased hospitalizations and excess deaths suggest COVID is not a uniformly mild disease. Countries that tried to power through the pandemic, like the U.K., are once again resorting to reduced activity. Vaccination is an important measure to reduce infections, but a vocal minority in most nations have resisted, leading to plateaus in vaccination rates. This week, Austria and Greece announced broad vaccine mandates, an extreme measure being contemplated in other places.

Widespread vaccination and improvements in testing have enabled most economies to learn to cope with COVID-19. Most of us can live productively with the virus, which is fortunate: the pandemic still has no end in sight.

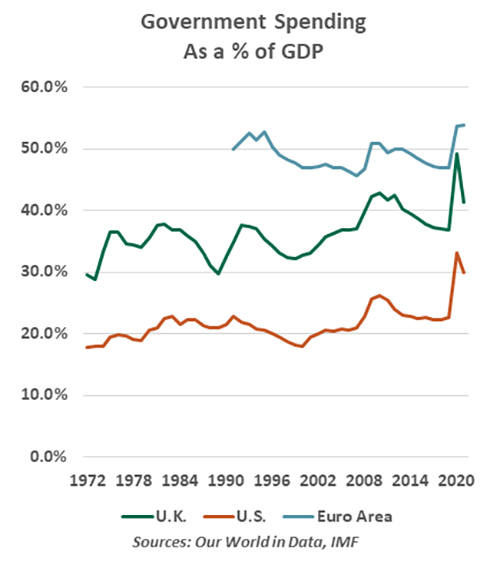

Big Government Is Back

In the western world, government involvement in the economy came under question in the early 1980s. At his first inauguration, former U.S. President Ronald Reagan famously observed, “Government is not the solution to our problem, government is the problem." His platform, which was copied by other nations, was to reduce regulation, control federal spending, and thereby release the power of the private sector.

Shortly thereafter, a decades-long bull market began. Expansions lengthened, trade expanded, and unemployment fell. The cause-and-effect of limited government and economic success is still the subject of vigorous debate, but the experience led populations around the world to develop a more narrow view of what government ought to do.

The pandemic provided a poignant counterargument. The manner in which governments were able to marshal resources and mobilize solutions to address COVID-19 has been immensely impressive. Not every step has been perfect, but many contend that the private sector would have struggled to act with the necessary speed and scale. The cost has been substantial, and government debt has mushroomed. But with interest rates low and the dividends of recovery being reaped, there seems little appetite for austerity.

|

Government is being seen more often as a solution than a problem.

|

This more recent experience has emboldened voices around the world to suggest that government can be a more constructive contributor to economic outcomes in more settled times. Infrastructure is a case in point: while some has been privately financed, governments are in a strong position to design and implement broad-based solutions. The U.S. Congress passed a large public works bill in November, and similar measures are on offer in other parts of the world.

Some progressives in some countries would like the pendulum shift even further towards a pre-Reagan equilibrium. They look enviously at the measures that the Nordic countries, for example, apply to manage their economy and society. While the progressives may not get everything that they want, the battle now centers on how big government should be, not how fast it should shrink.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

More Global Markets Topics >