2022: Back to the Future

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Transitory” was not a word generally associated with investing until the Fed started to use it to describe its recent forecasts for inflation. So far, the Fed’s forecasts have proven incorrect as inflation has been higher for longer than the Fed anticipated, and they have decided to drop the word from their communication.

But, the US and global economies might indeed be in a transitory state, and the important investment question is transitioning to what? It seems highly unlikely the economy will return to its pre-pandemic state.

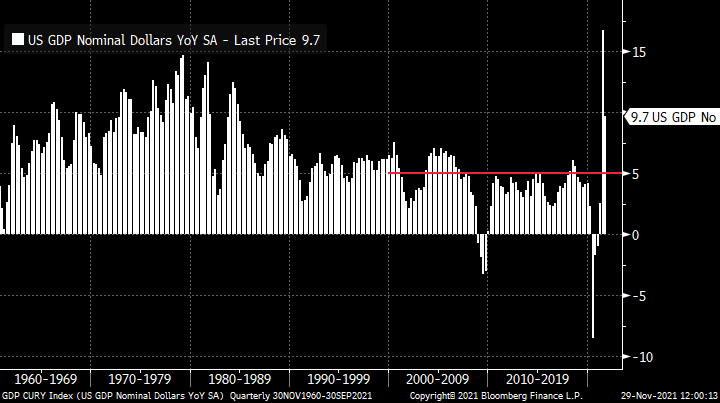

Many investors are apparently assuming economic growth will return to the sub-5% nominal GDP growth that existed during the majority of the past 20 years (See Chart 1). Absent of a full-fledged recession, the pandemic after-shocks are so far suggesting such slow nominal growth seems increasingly unlikely. 2022 might be a year of transitioning back to some sort of pre-1980, or at least pre-2000, economy. Investors’ asset allocations seem ill-prepared for such a change in nominal growth.

Chart1: US Nominal GDP Growth (12/31/1960 – 9/30/2021)

Source: Bloomberg Finance L.P.

The US is a price-taker not a price-setter

Because the US imported so much oil, the 1970s oil embargos illuminated the stark reality that the US was a price-taker and not a price-setter for oil. The US may be a bigger price-taker for a broader range of goods today.

The massive and seemingly ever-growing US trade deficit indicates the US is increasingly a price-taker rather than a price-setter. In other words, the US’s inflation rates may have been influenced more by globalization than by US monetary or fiscal policies.

Basic economics highlights the advantage of open trade is production shifts to where it is most efficient. As the number of suppliers grows around the world and competition increases, countries’ and companies’ battle for market share is deflationary as prices are repeatedly under-cut. Such intense competition forces less productive manufacturers with rigid cost structures to eventually go out of business. Of course, there were political interventions, but manufacturing primarily left the US because US manufacturing, infrastructure, and logistics were very inefficient relative to that found in other economies.

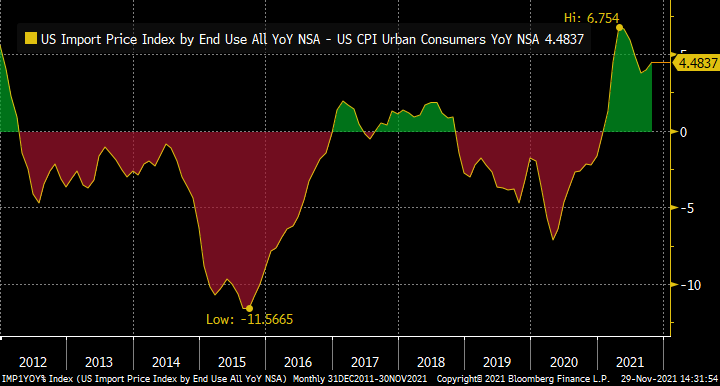

The fight for global market share exerted significant deflationary forces on the US economy as import prices rose more slowly than the overall Consumer Price Index (CPI). It was widely thought the US was “importing deflation” as the trade deficit grew and import prices were upward sticky.

However, recent global supply disruptions have restricted or even reversed the benefits of globalization. Chart 2 shows US import prices are now rising faster than the overall CPI. Unlike during much of the past decade, the US is now importing inflation.

Because the US is a price-taker, there is little monetary and fiscal policy can do in the short- or intermediate-term to combat inflation other than to curtail demand. Surely, inflation would abate if the Fed severely restricted liquidity or tax rates significantly rose for lower income brackets with high spending propensities, but those solutions are politically unpalatable. Inducing a recession isn’t an outline for successful re-election.

Chart 2: US Import Prices to CPI (Y/Y, 12/31/2011-11/30/2021)

Source: Bloomberg Finance L.P.

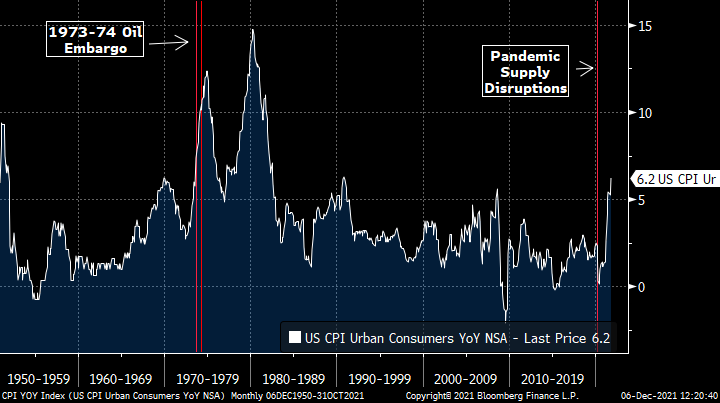

The 1973/74 Oil Embargo was an important historical supply disruption. It was, of course, a political supply disruption, but was nonetheless a supply disruption. That embargo basically set the base for higher inflation and wage expectations for the next decade.

The current supply disruptions within the global economy have lasted considerably longer than the 1973-74 Oil Embargo. The 73-74 embargo lasted less than 6 months whereas the current disruptions are approaching two years (See Chart 3). It seems unrealistic that the severity and length of the current supply disruptions won’t raise secular wage and price expectations.

Chart 3: Inflation & Supply Disruptions (12/31/1950 – 10/31/2021)

Source: Bloomberg Finance L.P.

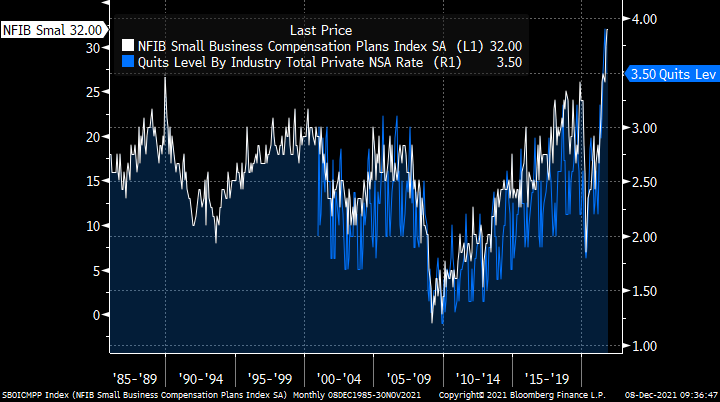

In fact, wage expectations are rapidly rising according to some data. Chart 4 highlights that the NFIB Compensation Index is at an all-time high reflecting small businesses plans to raise compensation. In addition, the JOLT Survey shows that employee’s plans to quit their jobs are also at an all-time high which reflects a very tight labor market. Whereas it may be unrealistic to expect such extreme data to continue, it does appear the very early-stages of a wage-price spiral appear to be forming.

Chart 4: NFIB Compensation Index vs. JOLT Quits (12/31/1985-11/30/2021)

Source: Bloomberg Finance L.P.

It’s an over/under bet

Whereas economists are encouraged to forecast economic data with decimal point precision, investors generally have to look at economic data as an over/under bet, i.e., will economic growth be stronger or weaker than is forecasted.

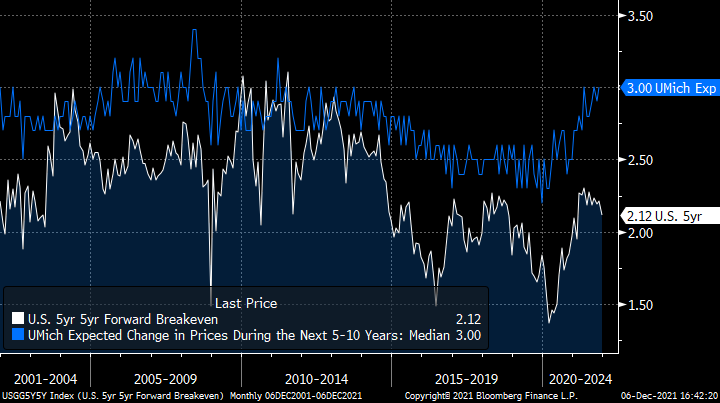

Current longer-term inflation expectations currently range between 2.0% and 3.0% (See Chart 5). So, investors have to choose whether they think secular inflation will be higher or lower than that range. Given the backdrop of contracting globalization, an extremely tight labor market and rising wage rates, and an inefficient US economy, investors may want to take the “over” on that range.

Chart 5: US Inflation Expectations 12/31/2001 – 11/30/2021

Source: Bloomberg Finance L.P.

Technology isn’t the hero riding in on the white horse

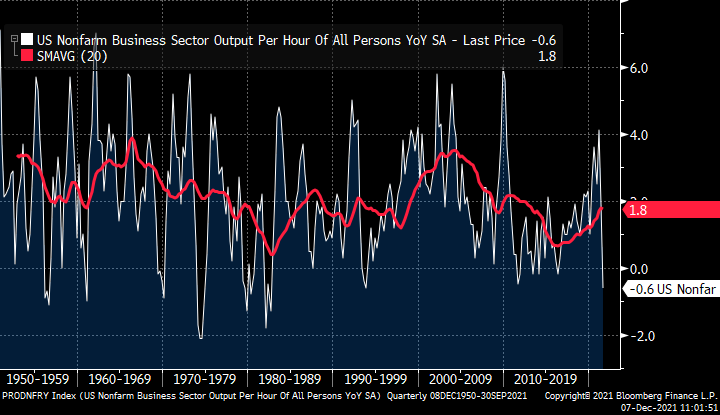

Some have suggested technological innovation has curtailed inflation, but productivity data strongly refute that assertion. Whereas there is considerable anecdotal evidence regarding technology aiding service industries, Chart 6 shows there has been no meaningful productivity improvement in overall US productivity.

There have been periods of improving and deteriorating productivity during the last 60 years, but the overall trend in US output per hour hasn’t secularly changed. Perhaps most revealing, productivity has marginally decreased since the Technology Bubble in 1999/2000 despite the widespread use of the internet and cellular communications. The slight improvement in the last five year has so far not been powerful enough to offset inflationary forces.

These data imply that US competitiveness remains challenged, the US will continue to be a price-taker, and US inflation will likely remain hostage to the expansion or contraction of globalization. The ballooning US trade deficit clearly shows the technology has not improved US competitiveness because the US continues to lose market share.

Chart 6: US Productivity 12/31/1950 – 9/30/2021

Source: Bloomberg Finance L.P.

The outlook for 2022

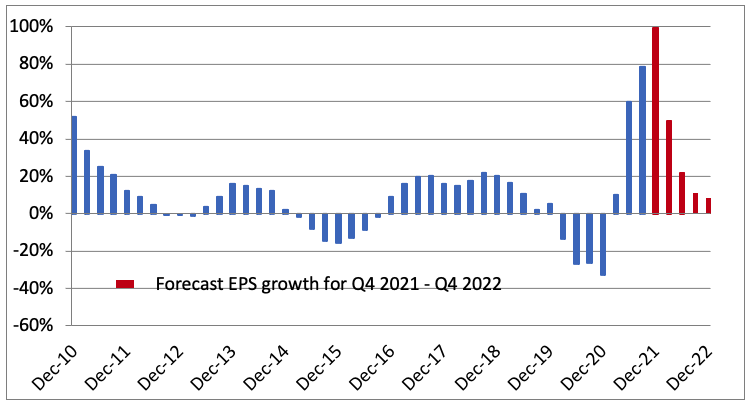

2022 will likely be a year of slowing but not slow nominal economic growth and earnings growth. Chart 7 shows S&P 500® reported earnings growth, and 2021’s outsized earnings rebound seems likely to slow as comparisons become more difficult. However, there is presently nothing in our work forecasting a full-blown earnings recession during 2022.

Chart 7: S&P500® Reported Y/Y Trailing GAAP EPS Growth (12/31/2010 – 9/30/2021)

Source: Richard Bernstein Advisors LLC, S&P Global

Barring a recession, nominal growth could positively surprise during 2022. Worrying whether nominal growth is comprised of real growth, inflation, or some combination of the two seems to miss the overall point about nominal growth possibly being stronger than expected.

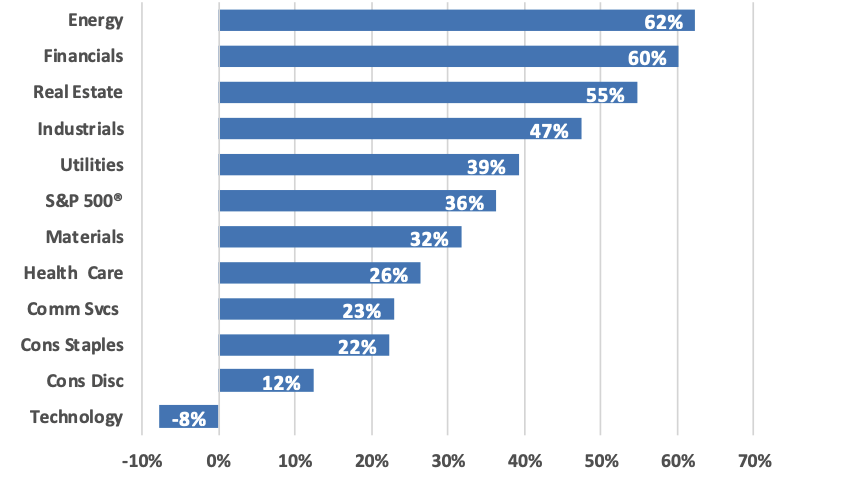

If we are correct that nominal growth could be stronger than currently forecasts, then it implies consensus sector allocations might be improper because the sectors most tied to nominal growth don’t appear to be household favorites.

Chart 8 shows sectors’ correlations to nominal GDP growth. Technology, currently the darling in most growth-oriented portfolios via public and/or private exposure, has historically been the worst sector during upturns in nominal growth. That should not be surprising because the previously mentioned period of slow nominal growth was perhaps the main driver of growth stock outperformance. Investors have historically gravitated to growth stocks when growth itself has been scarce. The economy and the resulting stock performance during the past 5-10 years has fit that historical mold.

However, if nominal growth begins to accelerate, then Technology seems very unattractive, whereas more traditionally cyclical sectors could outperform.

Chart 8: 5-Year Correlation of S&P 500® Sector Total Returns to Nominal GDP (Past 20 quarters thru 9/30/2021)

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

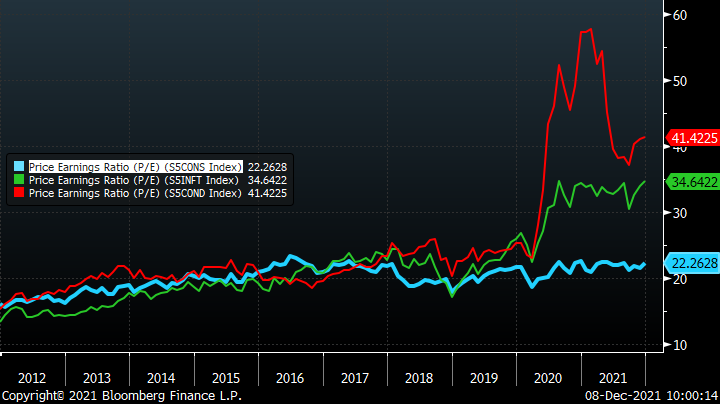

Consumer Staples might be an interesting sector as a barbell to nominal growth-sensitive sectors. Consumer Staples traditionally perform well during periods of slowing nominal growth or recessions, and they are also considerably cheaper than the Technology or Consumer Discretionary sectors (See Chart 9). Consumer Staples currently sell at a 35% discount to Technology and 46% discount to Consumer Discretionary. Thus, Staples might be a good spare tire to keep in a portfolio because of its combination of defensive characteristics and relatively conservative valuations.

Chart 9: P/E Ratios: Consumer Staples vs. Consumer Discretionary and Information Technology (12/31/2011 – 12/08/2021)

Source: Bloomberg Finance L.P.

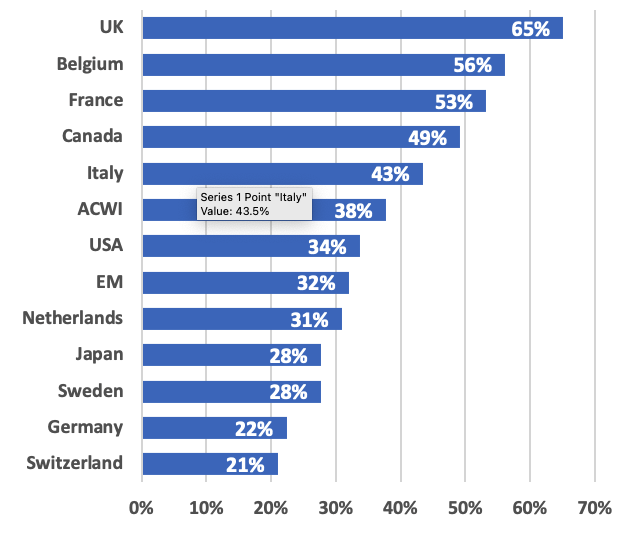

Chart 10 shows the correlations of countries’ performance to US nominal GDP. Some countries are more correlated to US nominal GDP than is the US, and ACWI overall is slightly more correlated. This is important because most investors are currently underweighted non-US equities, but the analysis shows some non-US markets might benefit from stronger-than-expected nominal growth in the US.

Chart 10: 5-Year Correlation of G10, ACWI & EM Total Returns to Nominal GDP (Past 20 quarters thru 9/30/2021)

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

It’s been very easy to be a capital preservation investor for the past 40 years, but an increase in secular US nominal growth might present significant challenges. For many years, capital preservation strategies could easily focus on treasuries. The success of the famous 60/40 portfolio (one comprised of 60% stocks and 40% bonds) has largely been attributable to the secular decline in long-term interest rates.

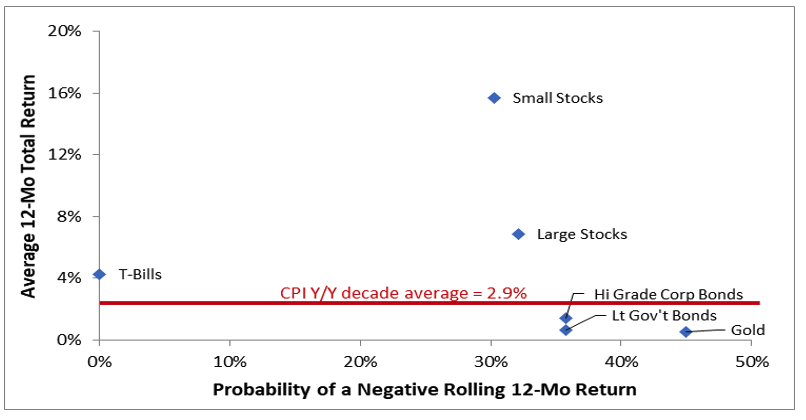

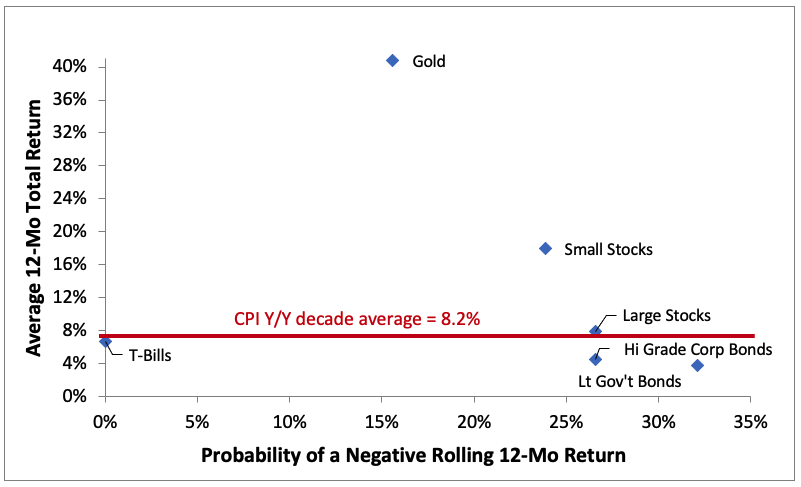

However, as Charts 11 and 12 highlight, Treasurys were the worst asset class during the 1960s and 1970s. They provided low returns and high volatility. Small stocks, an asset class generally ignored today, were a very good performing asset class as inflation ramped up. They provided higher returns and lower probabilities of losing money than did Treasurys over the 20-year period.

Superior real returns (i.e., returns less inflation, which is important for maintaining purchasing power) was also easy over the past several decades. But during the 1960s and 1970s Treasurys didn’t provide returns to keep up with inflation, and bond investors lost purchasing power.

It’s certainly hard to imagine retirees’ portfolios including substantial allocations to small stocks rather than to fixed-income, but that’s what history suggests might be the appropriate if inflation does continue to increase.

The conclusion from these charts is if nominal growth does positively surprise or if inflation is higher than investors expect, then 2022 could be the beginning of the end of easy diversification.

Chart 11: Risk/Return of Asset Classes for the Decade of the 60's

Chart 12: Risk/Return of Asset Classes for the Decade of the 70's

Source: Richard Bernstein Advisors LLC, Roger G. Ibbotson, Duff & Phelps SBBI®. For Index descriptors, see "Index Descriptions" at end of document.

The 60/40 portfolio might not be dead, but it could be a lot harder to construct and might have to be more actively managed. If inflation surprised, then it could be beneficial to err towards lower quality and shorter duration. Of course, recessions would argue for the exact opposite.

Active management relative to the cycle might be crucial. A simple buy-and-hold or ladder approach, which worked so well during the period of secular disinflation, might have to be replaced with active strategies that shift credit and duration depending on inflation cycles.

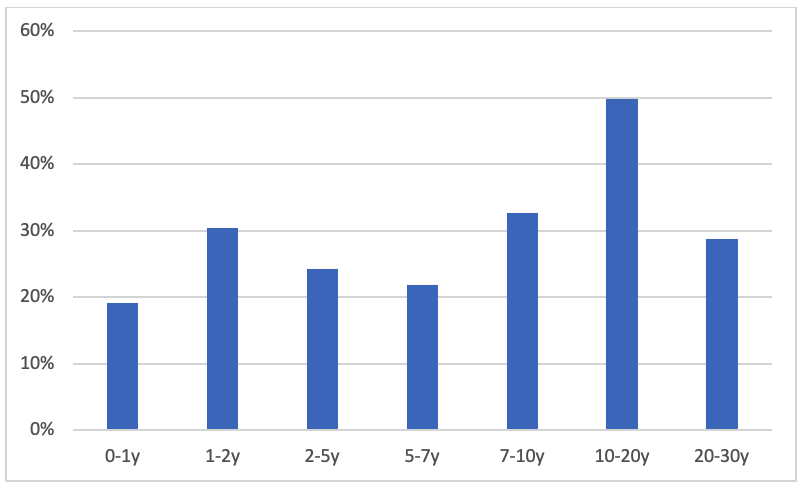

Besides the possibility that inflation could upside surprise, the probability seems high that long-term interest rates will be increasing during 2022 as the Fed tapers its buying of long-term interest rates. This point cannot be understated as the Fed currently holds over 50% of the 10-20 year Treasury market as shown in Chart 13. So, the long-end of the yield curve could be hit with a double whammy of tapering and inflation surprises.

Chart 13: Fed Ownership as a Percent of Treasury Market as of Sep. 2021

Source: Richard Bernstein Advisors, NY Federal Reserve Bank

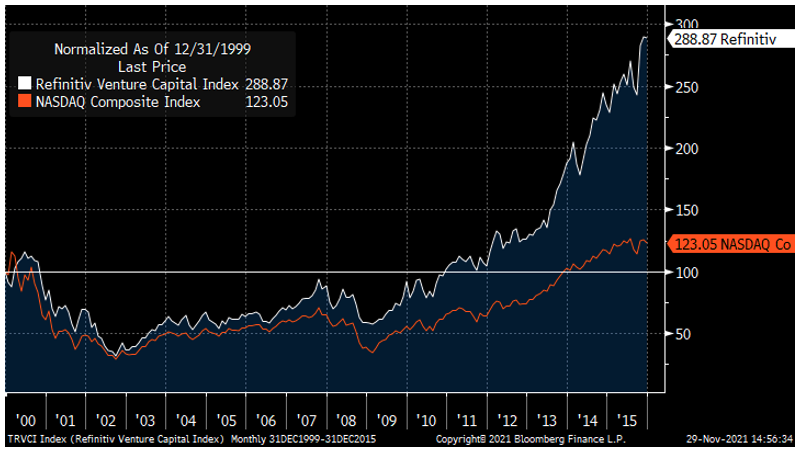

The longest duration assets in the global markets today are probably highly valued technology shares and venture capital investments. PE ratios tend to contract as interest rates and inflation rise, and investors need to consider whether the PE of their investments will contract because the denominator “E” will go up or whether the numerator “P” will do down. Investments that have no near-term return or cash flow, have historically seen their “P” contract because there is no incremental “E” to offset the negative effects of rising rates. That is the risk to long-duration equities.

If interest rates do indeed increase and valuations contract, then the time horizon of venture capital exits could lengthen. In other words, taking a company public might take years instead of what today seems like an hour-and-a-half. If that happens, venture capital returns could have significant negative convexity because their time horizons could increase as interest rates go up.

This has nothing to do with whether the technologies associated with such investments is real or not. The technologies associated with the Technology Bubble did come to fruition in the decade after the bubble burst and those technologies did have a meaningful impact on the overall economy. However, as Chart 14 shows, venture capital investments made during the bubble didn’t break even for a decade and those in public technology shares didn’t break even for 14 years. A combination of lengthening time horizons and rising interest rates doesn’t sound like a good mix.

Nominal growth sensitive asset classes seem underappreciated relative to long-duration strategies. Rhetorically, are institutions allocating more to venture capital or to commodities? Of course, it’s not even close with venture capital winning that popularity contest. This suggests pro-inflation asset classes might be a worthwhile contrary.

Chart 14: Venture Capital and Nasdaq Performance Post Tech Bubble (12/31/1999 – 12/31/2015)

Source: Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

Back to the future

Barring a recession, 2022 could be the continuation of the early stages of a new inflation paradigm. Globalization seems to be contracting, wage rates seem to be rising as labor markets remain tight, and productivity doesn’t seem to be meaningfully improving to offset these other factors. Supply disruptions already are bigger than the 1973-74 oil embargo. At the same time, neither monetary nor fiscal policy makers want to significantly curtail demand and slow the economy. Absent a recession, it’s hard for us to imagine the economy soon returning to sub-5% nominal growth.

Accordingly, we prefer sectors and countries that are positively correlated to nominal growth: Energy, Financials, Industrials, and non-US stocks. Consumer Staples, a sector typically hurt by inflation, seems a reasonable spare tire for portfolios in case growth demonstrably slows. Long-duration equities seem the riskiest portion of the global financial markets.

For fixed-income, we continue to believe buy-and-hold strategies will underperform and are focusing on the flexible active management of quality, credit, and interest rate shifts.

With respect to asset classes, the widespread underweight of pro-inflation assets seems to be a contrary signal supporting positions in commodities, gold, and potentially real estate. Non-US stocks might provide opportunities as fundamentals continue to improve and valuations remain conservative relative to US valuations.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

ACWI: MSCI All Country World Index (ACWI®): The MSCI ACWI® Index is a widely recognized, free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets.

S&P 500®: S&P 500® Index: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

EM: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

Belgium: MSCI Belgium Index. The MSCI Belgium Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Belgium.

Canada: MSCI Canada Index. The MSCI Canada Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Canada

France: MSCI France Index. The MSCI France Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of France.

Germany: MSCI Germany Index. The MSCI Germany Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Germany.

Italy: MSCI Italy Index. The MSCI Italy Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Italy.

Japan: MSCI Japan Index. The MSCI Japan Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Japan.

Netherlands: MSCI Netherlands Index. The MSCI Netherlands Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of the Netherlands.

Sweden: MSCI Sweden Index. The MSCI Sweden Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Sweden.

Switzerland: MSCI Switzerland Index. The MSCI Switzerland Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Switzerland.

UK: MSCI UK Index. The MSCI United Kingdom (UK) Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of the United Kingdom.

USA: MSCI USA Index. The MSCI USA Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of USA.

Nasdaq: The Nasdaq Composite Index: The NASDAQ Composite Index is a broad-based market-capitalization-weighted index of stocks that includes all domestic and international based common type stocks listed on The NASDAQ Stock Market.

Sector/Industries: Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s.

Large Stocks: The SBBI® Large Company Stock Index is represented by the S&P 500® Index: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

Small Stocks: The SBBI® Small Company Index: From 1926 to 1981 are composed of stocks making up the fifth quintile (ninth and 10th deciles) of the NYSE by market capitalization. From 1981 thru March 2001 the series is comprised of the DFA U.S. Small Company 9-10 (ninth and tenth deciles) Portfolio. From April 2001-current, the series is represented by the DFA U.S. Micro Cap Portfolio. For more detail see the current SBBI® Yearbook’s description of the basic series.

T-Bills (Cash): ® BofAML 3-Month US Treasury Bill Index. The BofA Merrill Lynch 3-Month US Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. The Index is rebalanced monthly and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date.

LT Government Bonds: The SBBI® Long-Term Government Bonds Index: From 1926 to 1976 the series uses data from the Center for Research in Security Prices (CRSP) at the University of Chicago Booth School of Business. From 1997 on the series are constructed using data from The Wall Street Journal. For more detail see the current SBBI® Yearbook’s description of the basic series.

High Grade Corporates:. The SBBI® Long-Term Corporate Bonds Index: From 1926 to 1968 the series was derived from the Ibbotson and Sinequefield (1976) backdate of the Salomon brothers index. From 1969 thru current the series is represented by the FTSE USBIG Corp AAA/AA 10+ Yr (formerly the Citigroup Long-Term High-Grade Corporate Bond Index). For more detail see the current SBBI® Yearbook’s description of the basic series.

Gold: Gold Spot USD/oz Bloomberg GOLDS Commodity. The Gold Spot price is quoted as US Dollars per Troy Ounce.

Refinitiv Venture Capital Index: The Thomson Reuters Venture Capital Index (the "Index") is designed to measure the value of the US-based venture capital private company universe in which venture capital funds invest.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All