The Metaverse Is a $1 Trillion Revenue Opportunity. Here’s How to Invest

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsQuick: What do Mickey Mouse, the Gucci bee and Snoop Dogg have in common? Besides being animal-themed, all three are coming to a metaverse near you.

The metaverse, as I’ve explained before, is part of the next iteration of the internet some are calling Web 3.0—and it promises to upend everything as we know it. Within the next few years, we will all work, play, socialize and invest in this all-encompassing ecosystem, whether that means attending a professional conference at a virtual Four Seasons hotel, shopping for a new designer handbag for our digital avatar or swinging through the New York City skyline with Spider-Man.

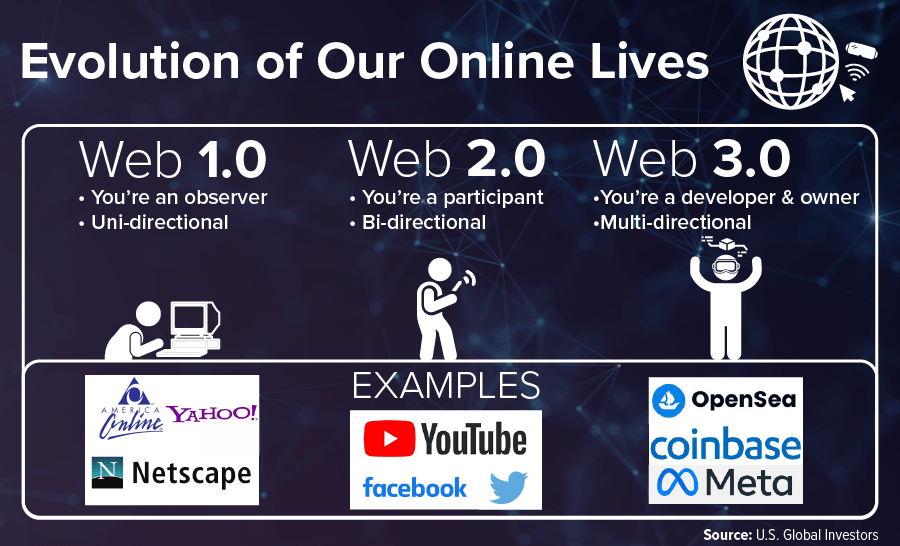

First, a short primer on the history of the internet and where we believe it’s headed. The earliest days of the internet, known as Web 1.0, were characterized by static, one-way webpages—think Netscape and Yahoo. Users were little more than passive observers.

Next came Web 2.0, the period we’re currently in. Controlled by a disproportionately small number of companies (Facebook, YouTube, etc.), the internet of today is highly centralized despite users’ role as an active participant.

That brings us to Web 3.0, which will usher in a whole new level of experience that, to some people, may sound more like Tron than real life.

Here’s a somewhat plausible scenario of what I’m talking about: It’s the year 2026, and you’re about to go on a first date with someone you met on Planet Theta, a virtual reality (VR) dating platform set to launch next year.

You strap on a VR headset—perhaps one made by Meta Platforms, formerly known as Facebook—and because you want to make the best possible first impression, you dress your avatar in an Armani suit and pair of Ray-Ban non-fungible token (NFT) sunglasses that you purchased with Ether (ETH). After spending some time strolling through an enchanted forest, you and your date watch the latest Disney movie, projected against the wall of a magical castle.

Confused? Don’t worry, you’re in good company.

Everything Old Is New Again

If you’re of a certain age, you probably recall feeling similarly lost when the internet came to prominence in the 1990s. (I recommend watching this clip from 1994 of Today anchors Katie Couric, Bryant Gumbel and Elizabeth Vargas arguing comically over what the @ sign means. “What is internet anyway?” a clearly perplexed Gumbel asks.)

Fast forward to now, and the internet’s value to the world economy is incalculable. Internet-native companies such as the FANG stocks—Facebook, Amazon, Netflix and Google—are among the largest and most influential in human history.

It’s no wonder, then, why many companies and investors are scrambling to gain a foothold in the emerging digital ecosystem that is the metaverse, estimated by Grayscale Investments to be a trillion-dollar revenue opportunity. Investment banking group Jeffries believes investing in the metaverse will be like investing in the earliest days of the internet. Head of thematic research Simon Powell says investors should focus first on hardware providers, then software providers, then on companies that operate within the metaverse.

Initially that may mean considering traditional tech companies like Nvidia, Intel, Cisco and Apple, which are well positioned to reap the benefits of increased demand for semiconductor chips, processors, cloud services and the like.

Initially that may mean considering traditional tech companies like Nvidia, Intel, Cisco and Apple, which are well positioned to reap the benefits of increased demand for semiconductor chips, processors, cloud services and the like.

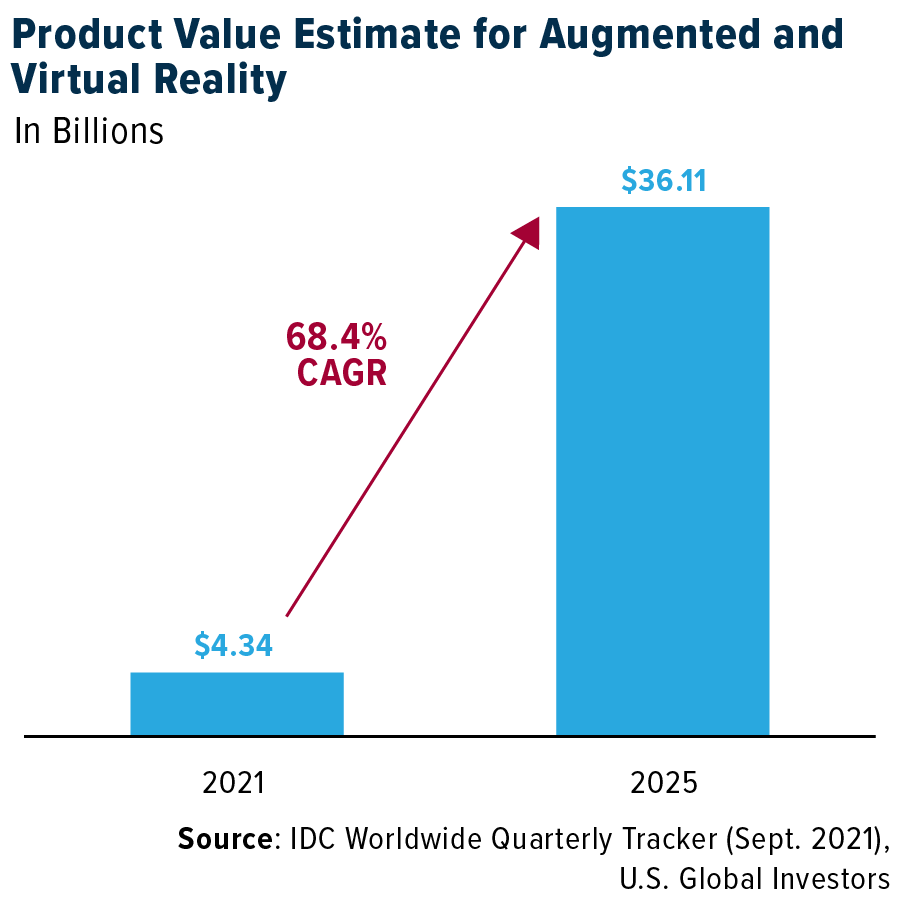

VR headsets have already become must-have gadgets – sales for which are expected to go mainstream as soon as this decade. Remarkably, Meta’s Oculus Quest 2 headset is believed to have outsold Microsoft’s Xbox gaming console this year. And by 2025, the total value of augmented and virtual reality products, including the Oculus, is forecast to hit $36 billion, according to market research firm International Data Corporation (IDC). That would be a ninefold increase from $4 billion this year, representing an incredible compound annual growth rate (CAGR) of 68%.

Not Just for Gaming

I should reemphasize the point that VR headsets and goggles will not just be for gaming, though that will be an increasingly attractive investment case, with gaming companies such as Roblox, Electronic Arts, Activision Blizzard and others expected to be big players.

In an end-of-the-year blog post, Bill Gates says he believes that in the next “two or three years,” most virtual meetings will move from two-dimensional, Zoom-style interfaces to the metaverse. “There’s still some work to do, but we’re approaching a threshold where the technology begins to truly replicate the experience of being together in the office,” Gates writes. He adds that Microsoft, whose board Gates stepped down from in May, is working on its own “interim” VR tools next year in conjunction with its planned virtual workspace, Mesh for Microsoft Teams.

Looking Sharp in the Metaverse

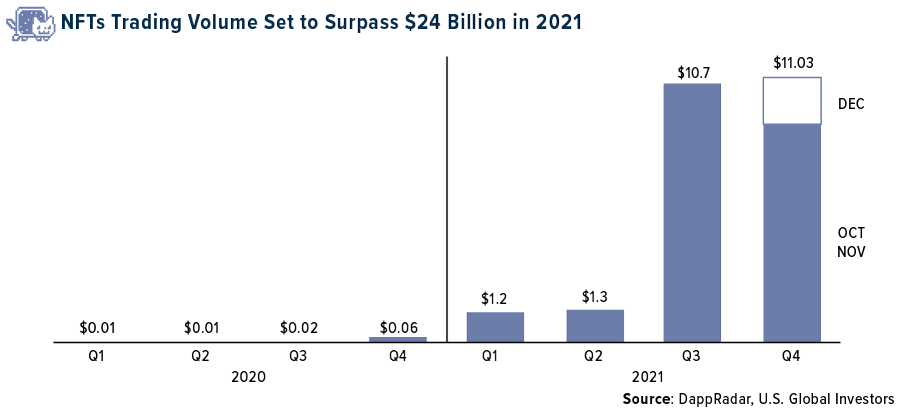

And then there’s NFTs, which are digital certificates that prove ownership of property, digital as well as analog. If Ether, Bitcoin and other cryptos are the money of the metaverse, then NFTs represent the stuff that fill up the metaverse.

NFTs are already high in demand, with new entrants arriving every day. This year alone, NFTs trading volume is estimated to surpass $24 billion, up massively from only $0.1 billion last year, according to DappRadar.

I find it particularly interesting that luxury goods companies have been among the most aggressive in terms of releasing new NFTs. Luxury designers and retailers tend to be very traditional and have historically resisted digitization. Many of them missed the e-commerce surge of the 1990s and 2000s.

Understandably so, they don’t want to make the same mistake. We’ve seen Gucci, Burberry, Nike, Adidas and many more announce plans to offer digital versions of their apparel to consumers who seek to turn heads in the metaverse. And with no raw materials for companies to buy, no warehouses or overstock to account for, profit margins have been considerable.

Not to be outdone, former First Lady Melania Trump is launching her first NFT platform, which will release new NFTs on a regular basis. That includes “Melania’s Vision,” a watercolor project that began trading on Thursday of this week.

U.S. Global Investors believes so strongly in the future of NFTs that, in October, we announced our investment in Network Entertainment, a Vancouver-based media production company that plans to create and distribute NFTs using its rich library of award-winning content.

Virtual Real Estate

Believe it or not, NFTs can also include virtual real estate. According to UBS, investment firms have been investing millions in digital land across a number of metaverse platforms, including Decentraland and The Sandbox.

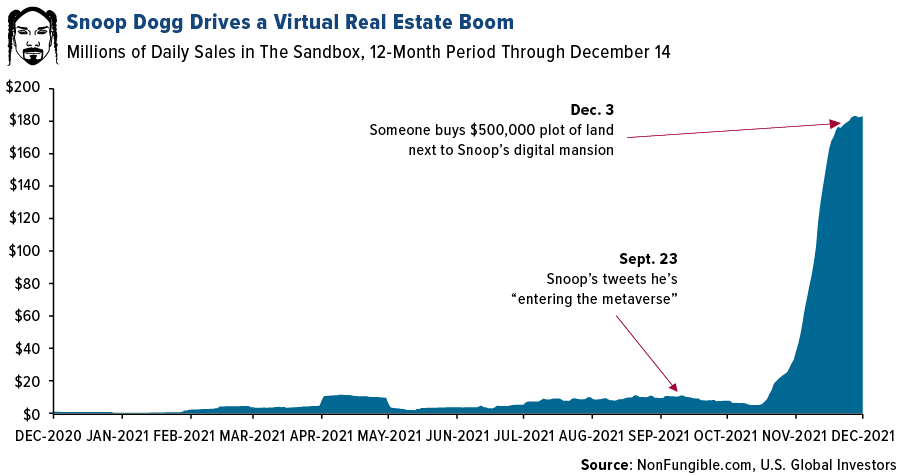

At the moment, the spotlight is on Snoop Dogg. Back in September, the legendary rapper announced via Twitter that he was “entering the metaverse” on Sandbox, a blockchain-based mobile game that allows players to buy and sell digital assets, including real estate. An anonymous Sandbox player made headlines earlier this month when he purchased an in-game plot of land next to Snoop Dogg’s virtual mansion for nearly $500,000. Yes, that’s half a million real USD.

Total sales within the virtual world of The Sandbox, in fact, have surged since the Doggfather made his announcement. Daily trading volume of NFTs exceeded $180 million this month, up from around $800,000 just a year earlier.

Once you have the land, then comes development. Again, according to UBS: “Architects are creating office buildings, luxury villas, entertainment complexes and even malls”—all of which people will be able to visit and enjoy in three dimensions without leaving their homes.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.68%. The S&P 500 Stock Index fell 1.94%, while the Nasdaq Composite fell 2.95%. The Russell 2000 small capitalization index lost 1.71% this week.

- The Hang Seng Composite lost 3.72% this week; while Taiwan was down 0.08% and the KOSPI rose 0.25%.

- The 10-year Treasury bond yield fell 0.7 basis points to 4.92%.

Airline Sector

Strengths

- The best performing airline stock for the week was Volaris, up 5.6%. Demand trends in Canada were up 4 points compared to last week, with the seven-day average of passengers being down 47% versus 2019, per data by CATSA. Demand in Canada has surged from -90% versus 2019 in early June and reached a new peak at -46% versus 2019 in mid-November.

- Excluding the distortions last week, average close-in (one-week out) fares increased 31% this week compared to two weeks ago while the average leisure (four-week out) fares, which are now lapping peak year-end holiday travel season, also gained 5.8% this week. The fare data is a good indication that directionally peak December holiday fares are stronger than 2019 levels. The current level also reflects resilient domestic U.S. demand (in leisure) with airlines able to push through higher fares, helped in part by pent-up demand from a depressed 2020 holiday season and the capacity levels still slightly below 2019.

- Hawaiian Airlines improved its December revenue guidance, now expecting a 30.5% decline versus 2019 at the midpoint, versus -34.5% prior, calling out stronger-than-expected demand throughout the network. With respect to the Omicron variant, management noted that they had yet to see anything that would drive them to reevaluate their current capacity plans, which indicates there is likely little-to-no impact to bookings as of now.

Weaknesses

- The worst performing airline stock for the week was Aeromexico, down 74.0%. Mesa Airlines reported a disappointing fourth quarter, with the $(0.06) EPS well below consensus of $0.21. The fourth quarter miss is a result of higher heavy maintenance and parts expenses.

- European airline bookings were sharply down in the week, after a surprising rebound last week, with a larger fall in international than in intra-Europe. Intra-Europe net sales declined by 5 points to -45% (versus -40% in the prior week) and fell by 18% this week. International net sales were down by 14 points to -56% versus 2019 (versus -42% in the prior week) and declined by 33% this week. This led to an 11-point decline in system-wide net sales for flights booked in Europe to -53% (versus -45% in the prior week), with a 2-point decline in the four-week trailing average to -45% versus 2019.

- The U.S. airline market is seeing some slowing. International tickets sold declined to -41.4% versus 2019 (and versus -34% last week) and bookings on an absolute level are 11.5% below the four-week average prior to the Thanksgiving holiday. Meanwhile, domestic tickets declined to -18.9% versus 2019 (versus -13.7% last week), but bookings on an absolute level are only -1.1%, below the four-week average prior to the holiday. The increasing case counts globally, and ever-changing travel restrictions, likely impact international demand more than domestic demand in the near term.

Opportunities

- According to Seaport Research, Southwest Airlines is the industry’s pricing leader, and its cost challenges in 2022 led them to conclude that Spirit Airlines, similar to other airlines, should benefit from a better pricing environment, hence its increased comfort with revenue execution. Spirit has significant market overlap with Southwest.

- Airlines with less reliance on state wage support programs have made larger redundancies and changes to staff contracts. Those airlines are likely to see more permanent cost reductions even after staff are rehired, as terms and conditions have changed. It appears legacy airlines remain far more attractive for potential employees, with ULCCs more likely to face challenges recruiting cabin crew.

- Delta Air Lines is planning additional investments with three partner airlines, strengthening its existing global platform. Earlier this week, Delta issued a press release stating the airline will make additional investments in Virgin Atlantic, Aeromexico and LATAM to reinforce its global strategy that fueled record international growth pre-pandemic. Delta is already an investor in these three carriers, but this announcement comes at a time when each carrier is emerging from restructuring or recapitalization. According to management, Delta is targeting a 20% equity stake in Aeromexico, a 10% equity stake in LATAM and will maintain its 49% equity stake in Virgin Atlantic. Upon completion, DAL’s investment in these carriers will be $1.2 billion. These partnerships will expand DAL’s growth potential by adding new routes, increasing customer connectivity, and creating new jobs.

Threats

- Goldman Sachs expects to see a more robust recovery in both international and corporate travel in 2022 following the strong rebound in domestic/leisure travel observed in 2021. If its current outlook is proved correct, Goldman is still cautious on the pricing environment into 2022. The group expects capacity to come back online faster than demand and while it is forecasting a step-function improvement in corporate travel from 2021, Goldman does not expect to see a full recovery to 2019 levels, driving a negative mix-shift to pricing. However, the graph below indicates that the rate of improvement in the U.S. has far outpaced the global recovery in the airline market.

- According to Goldman Sachs, labor inflation has been called out across the industry as a main driver of higher-than-expected costs exiting 2021. While the group does expect elevated levels of training to be transitory and normalize over the back half of 2022 into 2023, there are other drivers of labor cost pressure that could be permanent. For example, many carriers have had to raise minimum wage for relevant employees to attract/keep talent and have also had wage inflation at third party suppliers passed on. Additionally, with labor shortages prevalent in the U.S. overall and in particular for trained pilots/mechanics, Goldman expects to see upward rate pressure as labor contracts are renegotiated over the short-term.

- On Thursday, four Democratic lawmakers introduced the Forbidding Airlines from Imposing Ridiculous (FAIR) Fees Act, which according to Aviation Daily has been proposed in a near identical format during previous Congresses but never passed and seeks to have the U.S. DOT rein in the ancillary fees. While unlikely to pass, what is worth watching more closely is the DOT’s reviving of plans to introduce the Enhancing Transparency of Airline Ancillary Service Fees rule, opposed by airlines for reason other than transparency. The goal of the rule is to ensure that consumers have ancillary fee info (e.g., baggage/change/cancellation fees) at the time of ticket purchase and to examine whether fees for certain ancillary services should be disclosed at the first point in a search process where a fare is listed.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 2.41%. The best performing country in Asia this week was Thailand, gaining 1.4%.

- The Czech Koruna was the best performing currency in emerging Europe this week, gaining 0.15%. The Philippine peso was the best performing currency in Asia this week, gaining 1.0%.

- Preliminary December Manufacturing PMI for Eurozone was released at 58.0 above expected 57.8. Activity remains high in the region despite reports of increased restrictions due to the spike in COVID-19 cases.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 1.8%. The worst performing country in Asia this week was Hong Kong, losing 3.8%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 15.5%. The South Korea won was the worst performing currency in Asia this week, losing 0.50%.

- China November activity data came out mostly softer. Industrial production came in a bit better with help from a further easing of power and semi shortages, along with strong export growth. However, retail sales missed, with catering, autos and clothing being the main drags. Fixed asset investment growth slowed more than expected, consistent with the softness in the real estate market.

Opportunities

- Last week Wood & Company held its 10th Emerging Europe Conference hosting 220 companies. It was well attended event with many investors expressing interest in emerging Europe. Russian equities, especially commodity producers, recorded strong results in the current year – many paid record high dividends. Russia will continue to present a buying opportunity next year. The Greek economy is turning around. Greek economic growth is stronger than Spain or Italy. The country had deflation for so long, that the current inflation pressure now may benefit. Lastly, Turkey will present a buying opportunity once the right time comes and its currency stabilizes.

- Taiwan’s central bank kept interest rates unchanged for seventh consecutive quarter at 1.125%. Its central bank also forecasts the economy to grow 4.03% in 2022 from previous 3.45% estimate made in September. Taiwan also raised its 2021 fiscal year forecast to 6.09% from 5.74%. Taiwan will continue to benefit from strong exports.

- Goldman is back with its bullish outlook on oil, predicting Brent at $100 in 2023. While the bank’s base forecast is for Brent to stay around $85 for the next two years, prices may breach triple digits through either higher cost inflation for drillers or an unexpected supply shortfall. It also sees the recent selloff as overdone and expects investors to buy the dip in the new year. Stronger oil price will support lift in Russian equities.

Threats

- China’s economic growth is set to decelerate further in the fourth quarter. Economists forecast growth to slow to 3.1% in the current quarter, a deceleration from 7.9% in the April-June period and 4.9% in the last quarter. Economists also predict that China will start adding fiscal stimulus in early 2022 after the country’s top officials said their key goals for the coming year include counteracting growth pressures and stabilizing the economy.

- Central bank in Turkey cut its main by one hundred basis points, despite inflation at 21%. Lira reached a new record low against the dollar and may continue its down trend. Government plans to inject capital into state-owned banks to ensure they keep lending to businesses as the lira’s record drop erodes their buffers. The exact size of the capital boost and its funding method are still being ironed out. The government also raised the monthly net minimum wage to 4,250 liras ($275) from 2,826 liras for 2022.

- Central banks are becoming more hawkish. The Bank of England surprised with its first-rate hike since the pandemic struck, lifting borrowing costs 15 bps to 0.25%. Norges Bank raised its key rate 25 bps to 0.5% and flagged another hike in March. ECB left rates unchanged but phases out its emergency debt-buying program while increasing pace of regular bond purchases for half a year. Alongside central emerging Europe, Hungary and Russia also hiked rates.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was DCE Iron Ore Futures May 22, up 7.23% and a fifth consecutive week of gain on China’s steel output rebounding. Six months ago, the Sprott Physical Uranium Trust didn’t exist. Now it holds almost a third of the world’s annual supply—and it’s getting bigger. The fund’s arrival and explosive growth is sending waves through the market for nuclear fuels and has helped spur a 50% rally in uranium this year. Behind the surge is a race to bet on a nuclear future, with everyone from hedge funds to day traders jumping on board. The Canadian-listed trust, which launched in July, is the only publicly listed fund in North America that invests in physical uranium. Sprott has scooped up roughly 41 million pounds of uranium since the summer, which is roughly 30% of annual production.

- Lumber prices continue to move up rapidly. According to Random Lengths, the Framing Lumber Composite increased $113 this week to $786 as comparisons to last spring’s intense price increases have begun. In OSB markets, the OSB Composite increased $36 this week to $636. For next week, RBC Elements forecasts that the RL Framing Lumber Composite will increase $112 to $898 and that the RL OSB Composite will increase $46 to $682.

- Saudi Arabia’s energy minister warned traders against shorting oil, saying OPEC+ could react quickly to any fall in prices. OPEC+, a 23-nation group led by Saudi Arabia and Russia, decided on Dec. 2 to raise daily crude output by 400,000 barrels in January. But it kept the meeting open and said it would be able to reconvene at short notice to change course. Saudi Arabia said global oil production could drop 30% by the end of the decade due to falling investment in fossil fuels. “We’re heading toward a phase that could be dangerous if there’s not enough spending on energy,” Oil Minister Abdulaziz bin Salman said in Riyadh. The result could be an “energy crisis,” he said.

Weaknesses

- The worst performing commodity for the week was natural gas, down 6.37%, marking a third weekly loss on milder weather. International markets are losing their help to support the price as LNG cargos bound for Asia are now being diverted to Europe as it appears China has already built up its reserves for the coming winter. European buyers are struggling to replenish inventories in light of the uncertainty surrounding natural gas deliveries out of Russia.

- According to Platts, U.S. PVC import prices have fallen $150/ton from the previous week to $1,850/ton. The decline is not especially surprising since it reflects a drop in prices in Asia and elsewhere overseas, and there was a big gap between prices in the U.S. and Asia. While Shin-Etsu Chemical’s subsidiary Shintech plans on adding new PVC capacity in January-March 2022, PVC supply should stay somewhat constrained due to maintenance at Shintech and Formosa Plastics USA. The Egyptian Ministry of Trade and Industry announced it will impose a 9% anti-dumping duty on PVC imports from the U.S. Egypt accounted for 5% of U.S. PVC exports in 2021.

- Late last month, news of the Omicron variant of Covid-19 triggered a mini-plunge in oil prices as traders and investors fretted about its impact on petroleum demand. Since then, prices have recovered some of their lost ground, but remain well down on their highs for the year amid ongoing uncertainty about just how the virus will cut consumption. On Tuesday, the International Energy Agency, an adviser to oil consuming nations, gave its take on the situation through its monthly report on the oil market. The IEA’s analysis of the shorter-term outlook suggests the hit falling almost squarely on international travel and, consequently, jet fuel consumption.

Opportunities

- In a uranium related trade, that will get glossed over as another small tailwind for the sector, NuScale Power LLC is going public via a merger with special-purpose acquisition corporation Spring Valley Acquisition Corp. (SV), in a deal with a pro forma enterprise value of about $1.9 billion, the companies said in a joint statement Tuesday. These small-scale plants may be how the industry grows where the initial investment and timeline to cash flow are not decades.

- The COVID-driven energy price collapse in 2020 brought the end to a cycle defined by overinvestment, weak returns, and persistent underperformance for the energy sector. Concurrently, it ushered in a new period of pervasive capital discipline and rising shareholder returns. This new value proposition for the sector has not only proved supportive of oil and gas markets, but also helped drive record free cash flow for E&Ps and Integrated Energy stocks in 2021. This may support a further re-rating in the sector’s still discounted valuation.

- Goldman remains bullish on oil even as prices have pulled back on the recent Omicron variant contagion fears. Oil at $100 a barrel cannot be ruled out for 2023 as supply additions are anticipated to be too slow to keep up with record demand. Goldman noted investments in long-cycle oil project have also dipped as investor favor more clean energy use in the future.

Threats

- According to a recent report by the Solar Energy Industries and Wood Mackenzie Ltd., U.S. solar installs to slump 15% next year as prices surge. Higher input cost for panels and supply chain constraints have been a headwind and the Build Back Better Act will drive more demand in the future. However, California is considering reducing subsidies for solar and may introduce a monthly fee for residential solar systems. That could meaningfully cut volumes and curtain roof-top power.

- Strong electricity demand has led coal-fueled generation to jump about 9% this year, marking a new peak in coal’s use in the energy mix. The U.S. and Europe led the increase with 20% jumps and for India and China, their demand rose 12%. Coal is the single largest contributor to global carbon emissions and this data reminds us just how hard it is going to be to achieve a net-zero carbon footprint in the future.

- Oil held steady as the International Energy Agency said the global oil market has returned to surplus with the omicron variant curbing international travel. Brent crude futures were near $74 a barrel, paring earlier gains, as the Paris-based IEA, which advises major economies, said that rebounding supplies from numerous producers are creating a new oversupply, which is likely to swell further early next year.

Domestic Economy & Equities

Strengths

- Jobless claims increased to 206,000 after dropping to a revised 188,000 in the prior period, the lowest in five decades. Continuing claims dipped more than expected to 1,845,000 million from a revised 1,999,000 million.

- November housing starts came in at a 1,679,000, well ahead of consensus for 1,570,000 and October’s downwardly revised 1,502,000.

- Cerner Corporation, was the best performing S&P 500 stock for the week, increasing 20.54%. Shares of Cerner Corp. were up 16% in premarket trading Friday following a report that Oracle Corp. is in talks to buy the medical-records company for about $30 billion, part of the software maker’s push into healthcare.

Weaknesses

- November retail sales missed. Sales increased 0.3% month-over-month, below consensus for a 0.8% monthly increase and October’s upwardly revised 1.8%. Sales slipped for electronics and appliances and in department stores, while sales were somewhat better across sporting goods and hobby stores and clothing and accessories, FactSet reported.

- December’s U.S. flash manufacturing PMI missed, falling to a 12-month low, while the flash services PMI also missed. Manufacturing PMI was reported at 57.8 below expected 58.5, and Service PMI was released at 57.5 below expected 58.8.

- Adobe Inc., was the worst performing S&P 500 stock for the week, losing 14.95%. Shares declined after Adobe Inc. projected revenue for the first fiscal quarter and full year 2022 below analyst estimates.

Opportunities

- In a 50-49 vote on Tuesday evening, the Senate voted to extend the federal debt ceiling beyond 2022 midterm elections, raising the limit by $2.5 trillion. The House followed by passing the bill as well as sending it to President Biden’s desk for his signature. The focus now moves squarely onto Senate Majority Leader Chuck Schumer’s prior pledge to pass the $1.7 trillion Build Back Better bill by year’s end.

- Initial jobless claims most likely will remain at a record low level next week, and we expect the jobless claims to decline. Data will be released December 23.

- According to BofA’s latest Flow Show report, global equities saw $31.6 billion of inflows in the week ended December 15, the most in three months. Tech saw its biggest inflow since February while consumer goods saw the biggest inflow since December 2020. Credit Suisse pointed out that over the past four cycles, the S&P gained 9.5% in the 12 months prior to the first hike and 26% over the subsequent three years, FactSet reported.

Threats

- The CDC warned that the Omicron variant is spreading rapidly in the United States with modelling showing worst-case scenario could overwhelm health systems, particularly in under-vaccinated communities, reports the Washington Post. Latest studies show the two-dose Pfizer vaccine regimen still provided 70% protection against severe illness, while a booster shot would strengthen protection against infection, which fell to just 33% with two doses, states Wall Street Journal.

- The Federal Open Market Committee’s (FOMC) December policy statement said the Fed would begin reducing asset purchases by $30 billion per month, up from the previously announced $15 billion and in line with projections. New Summary of Economic Projections showed the median Fed projection for three rate hikes in 2022 (up from September forecast that was split on zero or one hike) and three rate hikes in 2023.

- The latest Investor Sentiment Survey showed bullish sentiment at 25.2% for the week ended December 15, down from 29.7% in the prior week and below the 38.0% historical average. Bearish sentiment pushed up to 39.3% from 30.5%, which is also the historical average. We could see some profit taking toward the end of the year.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Anti-Lockdown (FREE), rising 41,501.58%.

- Bitcoin has retreated 30% from an all-time high, but the cryptocurrency is still about 60% so far in 2021. This return exceeds traditional assets like global stocks, commodities, and gold, writes Bloomberg economists.

- Crypto wealth is minting the next generation of super spenders, according to a recent Bloomberg article. It is not all due to the post-pandemic pent-up demand though, suggests Jefferies International Ltd. No, instead, there seems to be significant impact from cryptocurrency wealth that is situated to benefit luxury good producers. Some of the luxury brands posed to benefit the most include Louis Vuitton and Gucci, writes Jefferies analyst Flavio Cereda.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Crimecash (CGOLD), down 99.27%.

- According to a Bloomberg article, Binance has dropped its Singapore cryptocurrency application to run a bourse in the city-state, ending an effort that started last year to win approval from Singapore’s authorities. The fiat-to-cryptocurrency trading platform, Binance.sg, will close by February 13, 2022. The company was among 170 other firms that applied to the Monetary Authority of Singapore for a permit to provide cryptocurrency services.

- CEO Richard Bernstein of Richard Bernstein Advisors told CNBC this week that “cryptos are the biggest financial bubble ever in history.” In an article published by Forbes, Bernstein also said “This is a monster one [bubble].” Bernstein places his faith, instead, in the energy sector, believing it to be a much safer, smarter bet than cryptocurrency and innovation disruption.

Opportunities

- Crypto-themed hedge funds outperformed Bitcoin’s year-end slump, says Bloomberg. Hedge funds offering a more diverse portfolio of cryptocurrencies got a leg up on Bitcoin this last month.

- WAGI United says it’s in the advanced stages of purchasing an English Football League club. The investors are believed to be the first group to buy a major sports franchise with cryptocurrency serving as a significant funding source, according to a Bloomberg article.

- Reddit co-founder creates $200 million fund with Polygon for Web 3, writes Bloomberg and CoinDesk. Alexis Ohanian’s venture capital firm Seven Seven Six and the Polygon Network have created this initiative to invest in social media and Web 3-based projects. “The initiative will back projects that explore better ways for humans to connect online,” announced Polygon last Friday.

Threats

- Bitcoin’s slide from a record high extended into a fifth week on Monday. The largest cryptocurrency fell below $48,000 and on the breach of its closely watch 200-day moving average, writes Bloomberg. “The idea that as it matured, the volatility would ease has not really materialized,” said Marc Chandler, chief market strategist at Bannockburn Global Forex.

- According to an article published by CNBC, the IRS has its eyes on crypto investors. Investors must report taxable 2021 transactions involving Bitcoin, Ethereum, Dogecoin and other cryptocurrencies to the U.S. federal government.

- Shares of Coinbase Global Inc. fell on Wednesday after prices of cryptocurrencies went haywire, wrote Bloomberg. It is unknown whether the cryptocurrency trading platform will recover if and when Bitcoin and other crypto coins bounce back into a more bullish rally versus its current slump.

Gold Market

This week spot gold closed the week at $1,198.84, up $15.27 per ounce, or 0.86%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.41%. The S&P/TSX Venture Index came in off 1.67%. The U.S. Trade-Weighted Dollar fell 0.22%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-14 | PPI Final Demand YoY | 9.2% | 9.6% | 8.8% |

| Dec-14 | China Retail Sales | 4.7% | 3.9% | 4.9% |

| Dec-16 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Dec-16 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Dec-17 | Eurozone CPI Core YoY | 2.6% | 2.6% | 2.6% |

| Dec-22 | GDP Annualized QoQ | 2.1% | — | 2.1% |

| Dec-22 | Conf. Board Consumer Confidence | 110.6 | — | 109.5 |

| Dec-23 | Initial Jobless Claims | 203k | — | 206k |

| Dec-23 | Durable Goods Orders | 1.5% | — | -0.4% |

| Dec-23 | New Home Sales | 770k | — | 745k |

Strengths

- The best performing precious metal for the week was palladium, up 1.38%, after falling over 14% in the past five trading days. Three central banks met this past week and all said that rates will go up to fight inflation. Rhona O’Connell of StoneX commented that the lack of sustained selloff following the hawkish shift “demonstrates the market is still pretty robust.”

- North American gold and silver miners closed the week up 2.10% on expectations that mining stocks have bottomed according to Roth Capital Partners. The buy in for higher prices may have been galvanized by the effort of central bankers to combat inflation. Roth believes silver is likely to outperform gold.

- Russian nationals have bought a record amount of gold since 2014, the Russian media has reported (Sputnik). They bought four tons of gold bullion and coins in the past nine months, which is around 8% more when compared to the previous year, the reports specified. Traditional gold investments have become very popular in other countries as well, with Americans having purchased 91.3 tons of the yellow metal in the past nine months (+79%), while in China and India gold buying has surged by 54% and 24% respectively.

Weaknesses

- The worst performing precious metal for the week was platinum, down 1.04%, after just gaining 1.01% in the prior week. The tape was negative for gold for most of the week, as everyone waited for the Federal Reserve. Gold declined as bond yields and the dollar pushed higher after a surge in U.S. producer prices added to concerns over inflation. Prices paid to U.S. producers posted a record annual increase of almost 10% in November, government data showed Tuesday. The increase was bigger than analysts expected and will sustain a pipeline of inflationary pressures well into 2022.

- Bloomberg reported that the Democratic Republic of Congo’s central bank failed to account for $530 million that the state mining company Gecamines says it paid to the government mostly during the former President Joseph Kabila’s final term in office, Congo’s top anti-corruption official said.

- Stillwater’s South African operations have recently suffered four fatalities at its Beatrix and Rustenburg mines. The group has decided to suspend operations at the Kloof 1 and Beatrix 3 shafts at the South African gold operations and the Rustenburg Khuseleka shaft at the gold operations until further notice. Additionally, the increase in COVID-19 infections in South Africa have resulted in a lack of senior management availability at the Rustenburg Thembelani shaft. As a result, the company has decided to suspend operations in that shaft too. Following these developments, the company now expects FY21 production for the gold operations to be at the low end of the previous guidance range of 884-948 thousand ounces while costs are expected to be at the top end of the guided range ($1,690-1,742 per ounce).

Opportunities

- Skeena announced a private placement of 1,471,739 flow-through shares at a price of C$21 per share for gross proceeds of C$30.9 million. Franco-Nevada is the end purchaser of the common shares and will own 2% of Skeena on closing. Skeena will grant Franco-Nevada a right of first refusal over the sale of a 0.5% net smelter return royalty over the Eskay Creek Gold and Silver Project.

- Wheaton Precious Metals announced the acquisition of a gold stream on Artemis’ Blackwater project in British Columbia, Canada, for $300 million, purchased from New Gold. The company also confirmed a prior announced silver stream on the project for $141 million. Positively, Blackwater is located in a favorable geographic location, features a long-duration 22-year mine life with reported exploration upside, and maintains an operator with development expertise. Once in production and fully ramped up, Blackwater is forecast to represent 5% of gold production for WPM.

- I-80 announced the signing of definitive agreements in connection with the previously announced financing package for aggregate proceeds of $135 million, and an accordion option to potentially access an additional $100 million. Under the $45 million Gold Prepay Agreement, commencing March 31, 2022, i-80 will deliver to Orion Mine Finance 32,000 troy ounces of gold. Sandstorm Gold also created a new royalty this week with their $37.5 million gold stream, and $22.5 convertible debenture with a 6% coupon, financing package they provided Bear Creek Mining to purchase the Mercedes gold-silver mine in Mexico from Equinox Gold.

Threats

- The Peruvian government seeks to increase mining taxes by 3 or 4 percentage points, Finance Minister Pedro Francke said in an interview to local TV. The International Monetary Fund (IMF) detailed in its preliminary report that the tax burden on the mining sector in Peru amounts to 41.7%, while in Chile this figure is up to 47.1% and in Brazil to 47.9%, Francke said.

- ESG remains a strategic priority for most gold producers – often one of the first few slides in company presentations, even before financial results. Over the past year, specific areas of focus are decarbonization (e.g., potentially using renewable power at the mines) and relationships with indigenous communities. Decarbonization is by far the most discussed ESG topic in company presentations, with many of the gold producers targeting net zero carbon emissions by 2050. The focus on decarbonization and exploring renewable power alternatives makes sense given that 80% of emissions for gold miners comes from the power used in mining operations, according to the World Gold Council. According to a recent EY survey, the top two business risks for miners in 2022 are 1) Environment and Social, and 2) Decarbonization.

- With the rewriting of the Chilen constitution there is a shift to enshrine water as a human right as waning supplies increase the scrutiny of the allocation process for water. Currently, Chile is the only country in the world to specifically state that water rights are treated a private property. By having the water rights treated as property to be bought and sold the industry in Chilie from agriculture, mining, and energy have benefited tremendously. With more that a decade of drought, some communities are coming up short on water and want to elevate the issue to a constitutional decree.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All