Patience, we are taught, is a virtue. Good things come to those who wait. Look before you leap. Haste makes waste. There are a host of adages that advise us to reflect, so as not to be rash.

This is the approach the Federal Reserve took for most of 2021. They remained relaxed, even amid mounting evidence that more urgency was needed. As the year ends, however, the Fed has been forced into a change of pace.

Inflation around the world has been rising rapidly. Year over year changes in the price level now stand at nearly 7% in the United States, more than 5% in Britain, and more than 4% in the euro area. While each market has idiosyncratic factors at play, all have been affected by elevated prices for housing, supply chain disruptions, and rising labor costs. As we noted last week, inflation is the top story we covered in 2021.

When price increases first began to accelerate, they were largely viewed as the product of temporary imbalances between demand and supply. Pandemic-related stimulus has been massive; at the same time, the pandemic has constrained the availability of goods and labor. But those conditions weren’t expected to last; high prices tend to attract more supply and curb demand, leading to more settled conditions.

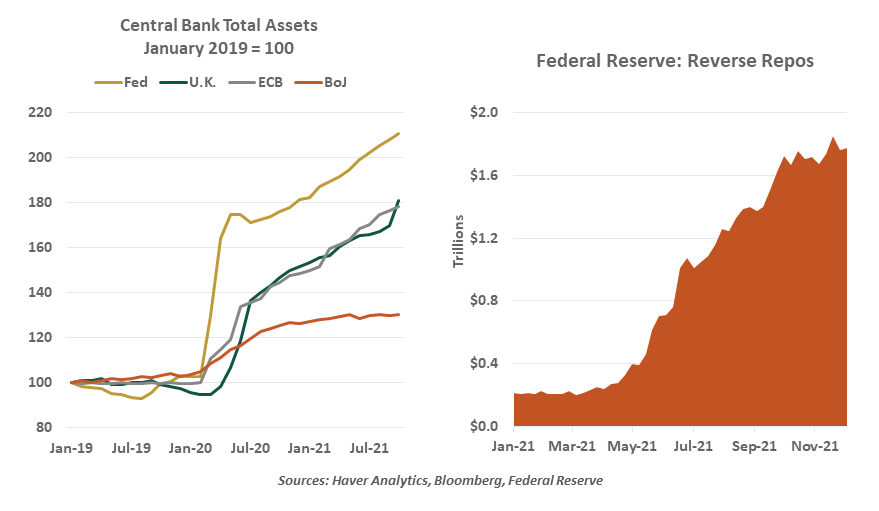

Central banks embraced this thesis more tightly than most. Not without reason: for most of the last decade, higher inflation was often expected, but never materialized. Powerful secular factors kept prices in check, anchoring inflation below the commonly-targeted level of 2%. The fear of deflation became more prominent than the fear of inflation. And so the printing presses pressed on; excess liquidity pooled throughout the economy.

The initial move upward in inflation earlier this year was actually cheered in some corners as a welcome overshoot of the targeted level, which would compensate for many years of below-target readings. Even as inflation continued upward, central bankers were reluctant to take action. Monetary policy is not as effective in addressing supply limitations, which have contributed significantly to the current situation. But monetary policy does drive demand, which has supported the buildup of price pressures.

|

The Fed has made a very sharp pivot over the past three months.

|

In light of all this, a number of the world’s central banks have hedged their bets. A number of them slowed or ended their quantitative easing programs, and a handful began raising interest rates. (The Bank of England announced a rate hike this week.) The Fed, however, walked on. Bond buying has been reduced, but the tapering of accommodation is not tightening.

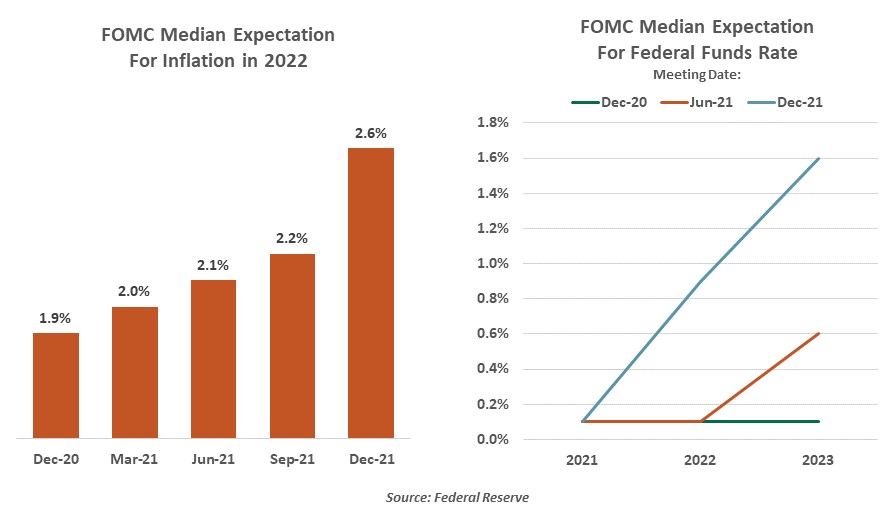

At the September meeting of the Federal Open Market Committee (FOMC), the members were evenly split as to whether interest rates should be lifted in 2022. But the tone has changed: all participants now expect higher interest rates next year. And the FOMC’s updated projections, released this week, call for much higher inflation over the next twelve months.

On this basis, the FOMC decided to accelerate the tapering of its asset purchases. On the current course, the Fed’s balance sheet will reach a steady-state level next March. Reaching that milestone is a prerequisite for potential interest rate increases; the median expectation within the Fed calls for three hikes in 2022 and three more in 2023. That is a much more aggressive line than we had previously expected.

Such a sharp pivot has the potential to unnerve markets. So far, reaction has been measured; the Fed has done a good job of signaling its intentions. But as time draws on and interest rate changes become more proximate, the Fed’s communication effort will have to be at its best. And if conditions warrant moving with more alacrity, it may throw markets off stride.

The race isn’t always to the swift. But sometimes, he who hesitates is lost.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

More Global Markets Topics >