The most significant risk to stocks is not the Fed.

Over the next few months, you will see a lot of articles suggesting that initial rate hikes from the Fed don’t impact stocks. Such as this one:

“Historical analyses put together by Evercore ISI’s Ed Hyman and The Sevens Report’s Tom Essaye show that the S&P 500 typically fares well when the Fed raises rates for the first time in a tightening cycle.

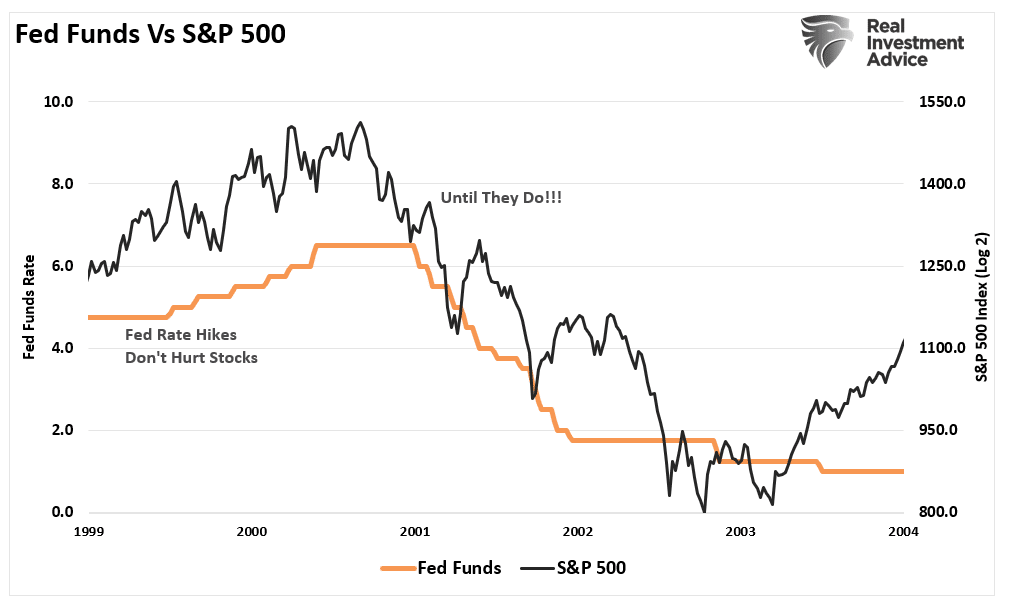

For example, the Fed embarked on a rate hike cycle on June 30, 1999, when it raised rates by a quarter-point to 5%. The S&P 500 rose 7% from there to post a gain of 19.5% for the year.” – Fred Imbert, CNBC

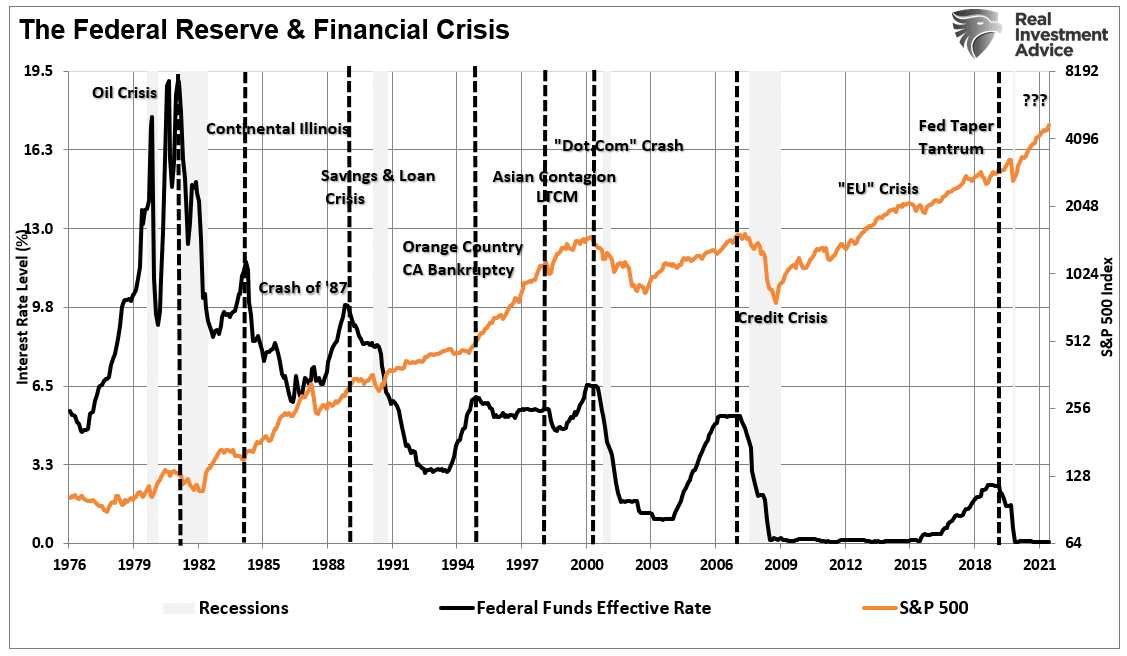

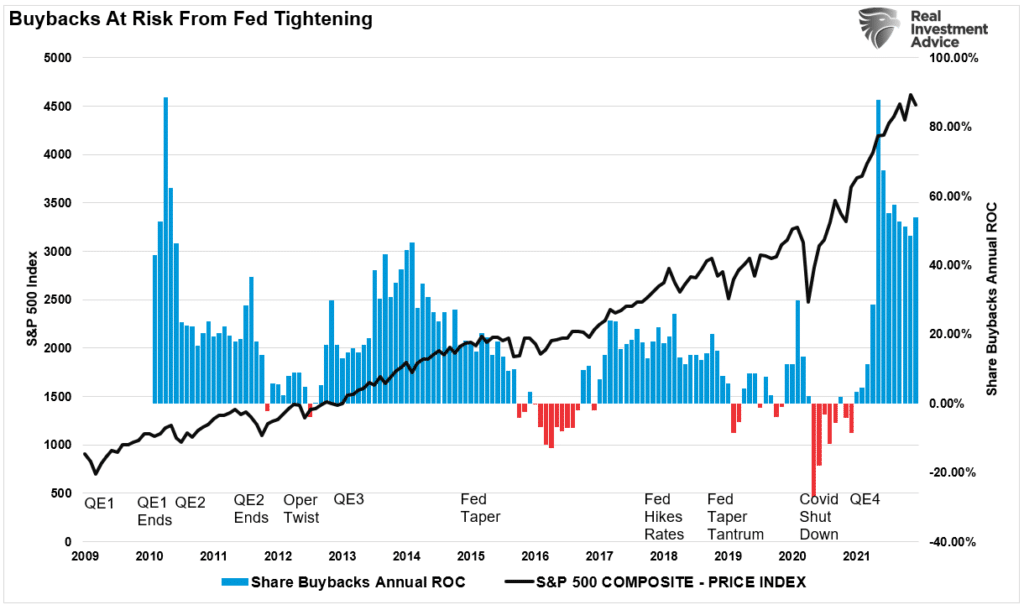

That is a true statement. When the Fed initially starts hiking rates, it is usually during a strongly trending bull market. Much like a car rolling downhill in neutral, tapping the brakes initially doesn’t do much to curb the momentum. However, keep pushing on the brake pedal long enough, and the car will slow to stop. There are two things to take away from the chart below.

The risk is not the initial rate hike, the second, or even the third for stocks. It is the point where the increase in rates causes something to break either in the economy, credit markets, or a change in bullish psychology. Secondly, without exception, rate-hiking campaigns led to a negative outcome. Furthermore, the negative impact occurred at consistently lower levels.

So, while Fred is right that stocks rose 7% in 1999 after the Fed hiked rates, in 2000 when the Fed finished hiking rates, the stock market fell nearly 50% over the next two years.

Clearly, the Fed is a risk to stocks.

A Bigger Risk To Stocks

I recently discussed the misuse and abuse of stock buybacks. While the topic of share buybacks remains one of great debate, the magnitude of the impact on the financial markets remained somewhat obscure. However, the use of buybacks to artificially inflate earnings was not. To wit:

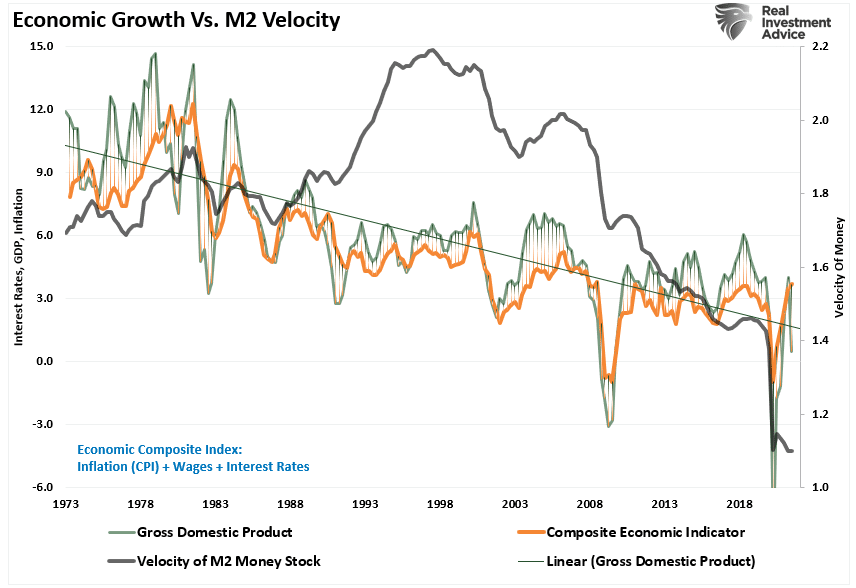

“As we now know, there is a point where low rates deter economic activity. Companies become unwilling to ‘invest’ due to the low return environment. The chart shows the problem of economic growth ratesand monetary velocity.“

The problem for companies in a weak economic environment is the lack of topline revenue growth. Given higher stock prices compensate corporate executives, it is not surprising to see companies opt for a short-term benefit of buybacks versus investment.

The surge in the repurchase of shares over the last decade remains one of the more significant supports to the financial markets. (Such is because it is mostly the major market-cap-weighted names that can afford multi-billion share buybacks.)

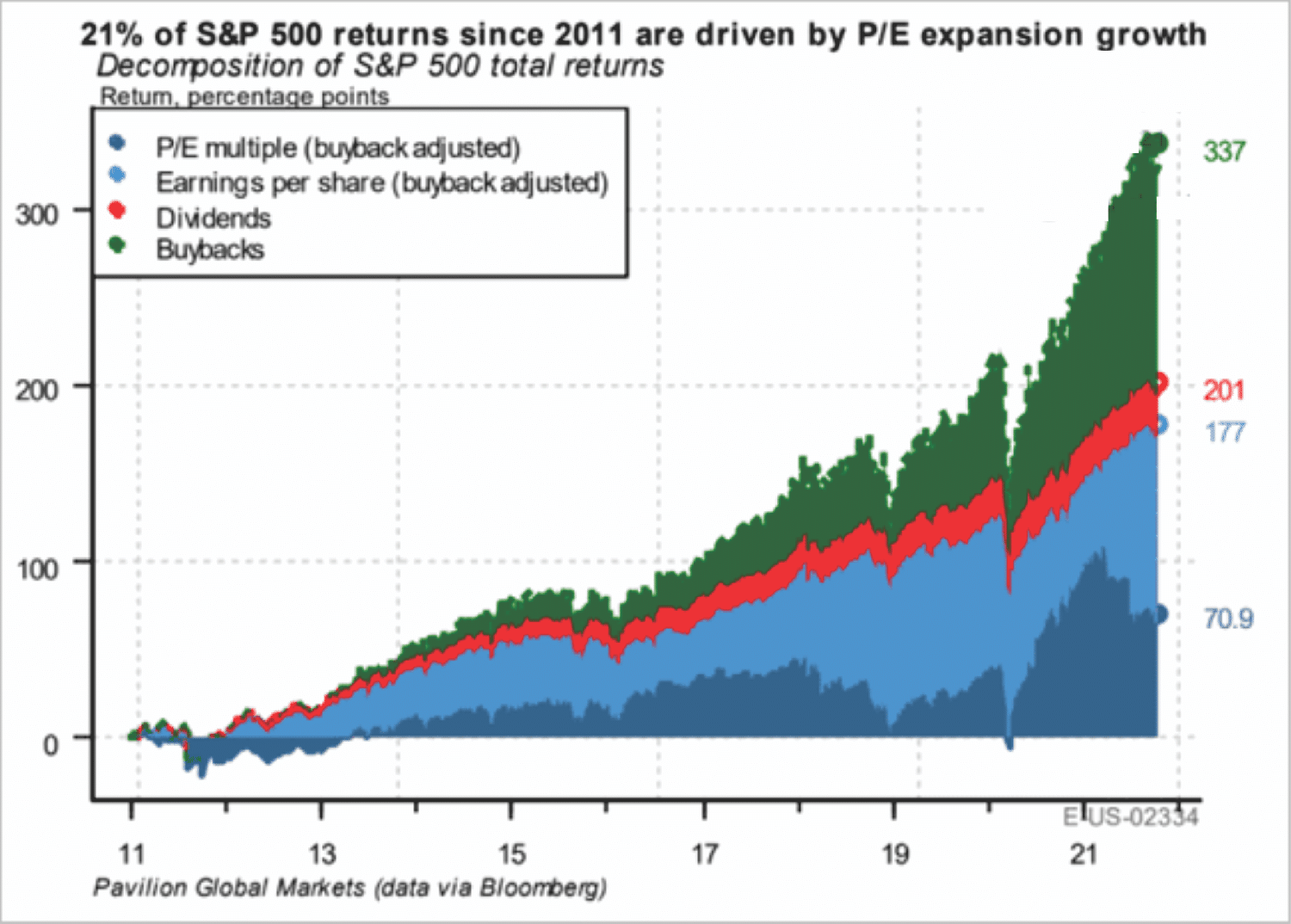

The chart below via Pavilion Global Markets shows the impact of buybacks on the market over the last decade. The decomposition of returns for the S&P 500 breaks down as follows:

21% from multiple expansion,

31.4% from earnings,

7.1% from dividends, and

40.5% from share buybacks.

In other words, in the absence of share repurchases, the stock market would not be pushing record highs of 4700 but instead levels closer to 2800.

The risk to stocks is a reversal of that support from the Fed.

Taper & Tightening Ahead

So, let’s “review the tape” of the rationalizations of the bull market to date.

Low rates justify high valuations.

Low inflation justifies high valuations.

The Fed’s monetary liquidity supports stock prices.

The Fed’s zero-interest policy supports the bull market.

There is no alternative to stocks when rates are zero.

Etc.

We now know that it isn’t all of these rationalizations supporting higher stock prices but rather stock buybacks.

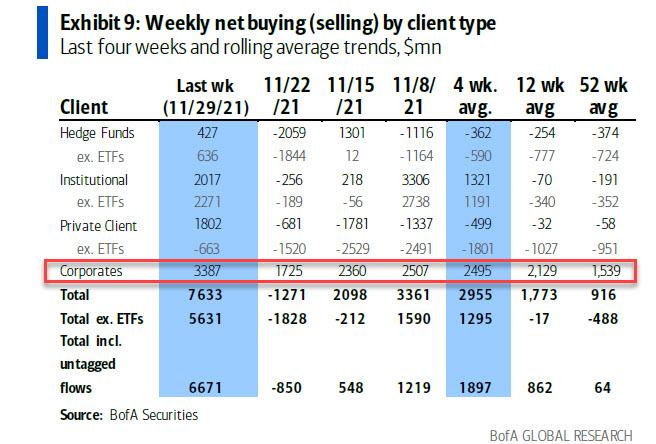

BofA recently reported that buybacks by corporate clients picked up to their highest weekly level since March. The bank calculated that corporations bought back $3.4 billion worth of their own stock, twice the level from the previous week and well above the recent weekly averages.” – Zerohedge

“The return of buybacks is a big antidote to market scares over the withdrawal of Federal Reserve monetary stimulus and the emergence of a new Covid-19 variant. Since the start of January, U.S. companies have announced plans to buy $1.1 trillion of their own shares, almost triple the level at this time last year, data compiled by Birinyi Associates and Bloomberg show.” – Bloomberg

While the surge in buybacks may temporarily ease concerns over the withdrawal of monetary support, such will likely not last. Historically, the reversal of Fed policy to a tighter regime slows stock buybacks and tempers stock market returns.

With the Fed on deck to start tightening policy heading into 2022, there is a significant risk that buybacks will slow. Such was the case when the issuance of cheap debt provided the funding for many of these repurchases.

2022 Could Be A Bumpy Year

The Fed recently highlighted the most salient risks that could undermine the financial system. Those included “structural vulnerabilities” in money market funds, valuations, “stable coins,” a generic warning about risks associated with cryptocurrency adoption, inflation, and fading fiscal support.

But, as always, the Fed hopes they can orchestrate a “soft-landing” for the stock market.

Unfortunately, as shown in the first chart above, the Fed has a miserable track record of such outcomes.

Richard Thaler, the famous University of Chicago professor who won the Nobel Prize in economics, stated:

“We seem to be living in the riskiest moment of our lives, and yet the stock market seems to be napping. I admit to not understanding it.

I don’t know about you, but I’m nervous, and it seems like when investors are nervous, they’re prone to being spooked. Nothing seems to spook the market.”

Such is always the case, just before something does.

But, heading into 2022, significant headwinds face a highly valued market.

As noted, tighter monetary policy, and high valuations.

Less liquidity globally as Central Banks slow accommodation.

Less liquidity in the economy the previous monetary injections fade.

Higher inflation reduces consumption

Weaker economic growth

Weak consumer confidence due to inflation

Flattening yield curve

Weaker earnings growth

Profit margin compression

Weaker year-over-year comparisons of most economic data.

I am sure I have forgotten a couple of things. However, the point is that many of the tailwinds that have existed since March of 2020 will now become headwinds. Importantly, companies that performed un-economic buybacks will find themselves with financial losses, more debt, and fewer opportunities to grow in the future.

The most considerable risk for investors betting on higher stock prices isn’t the Fed. Instead, it is the reversal of “stock buybacks.”