These Were the Biggest Investment Stories of 2021

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAny way you look at it, 2021 was an eventful year—from a new president to new virus variants to new all-time highs for Bitcoin and the S&P 500 (70 record closes!). We even saw the rise of a whole new asset class: non-fungible tokens, or NFTs, with annual trading volume between $22 billion and $24 billion this year, up from only $100 million last year.

Based on our own data analytics, readers of the Investor Alert and Frank Talk were most interested in stories on gold mining, precious metals, natural resources and emerging markets (no surprise, as our firm is well-known for our expertise in those sectors). But there was also interest in macroeconomic topics (inflation, mostly) as well as Bitcoin and cryptocurrencies.

That said, below are what I believe were the biggest investment stories of 2021.

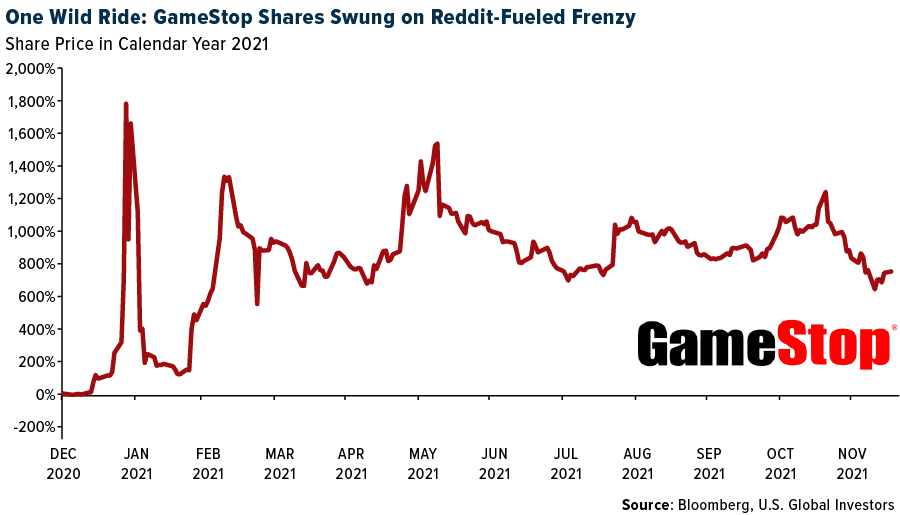

Game “Stonks”

What do you get when you combine Reddit, Robinhood and hundreds of thousands of retail investors?

One of the wildest episodes in public markets, of course, which pitted amateur millennial and Gen Z traders’ David against Wall Street’s Goliath. Hedge funds that bet against struggling video game retailer GameStop lost billions after do-it-yourself investors, getting their cues from organizers on Reddit, bid up the distressed stock, forcing the hedgers into a short squeeze.

Personally, I’ve never seen anything like it. Nearly 1.3 billion shares of GameStop were traded in January alone. That’s the kind of volume you’d expect from the massive SPDR S&P 500 ETF, not a barely mid-cap company that hasn’t posted a profitable year since 2018.

Although the trading frenzy has cooled somewhat, GameStop is still up around 700% for the year. Other so-called “meme stocks,” most notably AMC Entertainment, also saw eye-popping returns in 2021.

Read the full Frank Talk here:

Reddit Investors Who Played GameStop Are Now Upvoting Silver

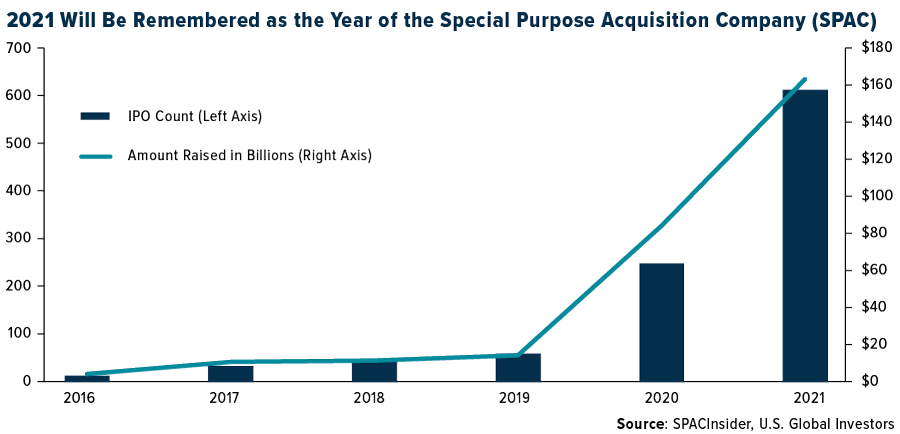

SPAC Attack

2021 will undoubtedly be remembered as the year of the SPAC, or special purpose acquisition company. Also known as blank check companies, SPACs have no business objective other than to buy or merge with another company and bring it to market. Last year, SPAC listings outnumbered traditional IPOs for the first time ever, a trend that’s continued in 2021.

It’s likely we’ll continue to see a healthy stream of SPACs. Compared to traditional IPOs, they’re easier and less costly to close, with fewer disclosures. This is good news for investors, who have seen a steady decline in the number of initial public offerings over the past few decades due to stricter regulations.

These types of deals have tended to attract unexpected names, and this year was no different. Former President Donald Trump’s Trump Media & Technology Group, which plans to launch a social media platform to compete with Twitter and Facebook, announced in October that it would merge with Digital World Acquisition Corp., which currently trades on the Nasdaq under the ticker DWAC. The transaction could be at risk, however, as it’s come under investigation by federal regulators.

Read the full Frank Talk here:

What Are SPACs, and Why Is Everyone Talking About Them Right Now?

Planet Bitcoin

This list wouldn’t be complete without mentioning Bitcoin, the world’s first and largest cryptocurrency by market cap. Where do I even begin?

2021 began with Elon Musk announcing that Tesla had as much as $1.5 billion in BTC on its balance sheet, representing the latest example of a large company using the asset as a store of value. Musk’s love affair with the crypto later became complicated, however, when he halted BTC payments over concerns that it used too much dirty energy to mine, a presumption that was proven false by the Michael Saylor-headed Bitcoin Mining Council. (HIVE Blockchain Technologies is a founding member.)

Companies investing in Bitcoin is nothing new, but countries adopting it as legal tender? That was unheard of—until El Salvador did just that in June. The Central American country made history by becoming the first to recognize the digital asset as currency, alongside the U.S. dollar. A Bitcoin City, to be built at the base of a volcano, has also been proposed.

Oh, and don’t forget that 2021 also saw the launch of the very first Bitcoin ETFs.

After all this, what could 2022 possibly have in store for the crypto? I hope you’re as excited as I am to find out!

Read the Frank Talks:

Note to Elon: Crypto Miners Are Part of the Solution to Curbing Greenhouse Gases

El Salvador Just Adopted Bitcoin as Legal Tender. Here’s Why Other Countries May Follow Suit

Shipping Rates and Inflation

I’m conflating shipping rates and inflation into one story because the former is a major contributor to the latter. This year, global shipping rates reached all-time highs as consumers shifted much of their spending from services (dining out, going to the theater) to goods. Although rates have rolled over from their September and October peaks, they still remain highly elevated. According to data provided by Freightos, the average global rate to ship a 40-foot container was up a head-spinning 200% in December 2021 compared to the same month in 2020.

At the same time that this has fattened container shipping companies’ coffers, it’s also had a huge impact on consumers’ pocketbooks as prices have soared at a pace unseen since the first Reagan administration. In November, the consumer price index (CPI) advanced 6.8% over last year, with gasoline, natural gas and clothes recording some of the biggest increases.

Read the Frank Talks:

Shipping Bottlenecks Could Last Well into 2022. That’s Good News for Investors

Shadow Inflation Could Be a Bigger Problem Than You Realize

Watch the video:

Bad News Is Good News for Shipping Bottlenecks

Honorable Mention: Texas Freezes

Back in February, U.S. Global Investors’ home state of Texas experienced a once-in-a-century winter storm that exposed the vulnerabilities of its standalone power grid, overseen by the Electric Reliability Council of Texas (ERCOT). Millions of Texans, myself included, went without water and electricity for days at a time as “Snovid,” an apt play on Covid, froze un-winterized natural gas pipelines and wind turbines.

So, is the Lone Star State ready for the next monster storm? Like everything else, it depends on who you ask. Legislation signed by Governor Greg Abbott in June requires providers to update their infrastructure and operations, and about 80% of power plants within the state managed to meet the December 1 deadline to report on preparedness. “The lights will stay on,” one official reassured Texans in early December.

Read the Frank Talk:

A New Commodities Supercycle Could Be Powering Up After a Long Freeze

Sending you a happy, healthy, prosperous New Year! What do you think was the top finance story of 2021? Share your thoughts by emailing me at [email protected].

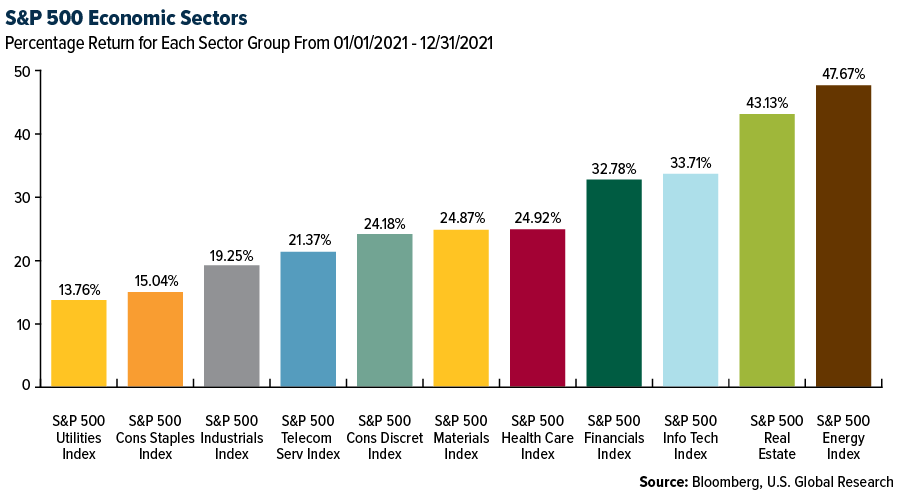

- The major market indices finished up this year. The Dow Jones Industrial Average gained 18.97%. The S&P 500 Stock Index rose 27.10%, while the Nasdaq Composite climbed 21.90%. The Russell 2000 small capitalization index gained 13.80% this year.

- The Hang Seng Composite lost 15.56% this year; while Taiwan was up 23.66 this year% and the KOSPI fell 5.27%.

- The 10-year Treasury bond yield 58 basis points to 1.503%.

Airline Sector

Strengths

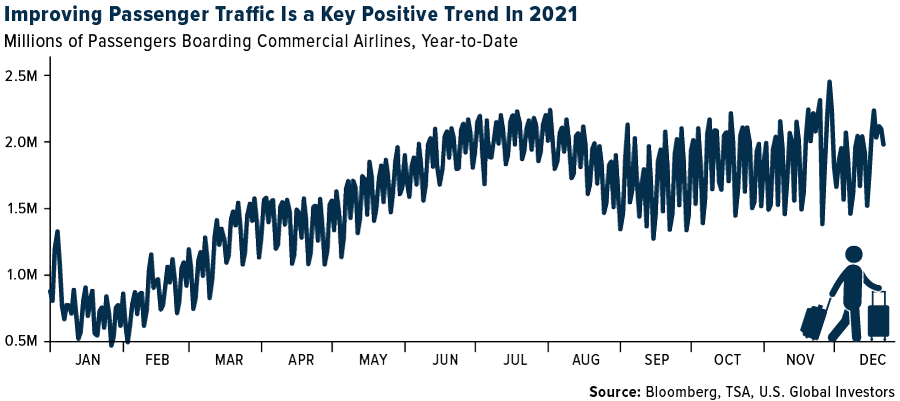

- Airline traffic, as measured by the Transportation Security Administration (TSA) checkpoint data, continued to improve during 2021, and continues to improve with the holiday season. The Thanksgiving holiday air travel doubled when compared to last year and came in slightly below 2019 levels overall. For seven consecutive days, daily airport passenger volumes exceeded 2 million people, according to the TSA. This is a streak that has not occurred since before the pandemic started two years ago. The TSA checkpoint numbers hit record highs during the pandemic. TSA data continues to trend positively in North America, which should bode well going into 2022. Stifel Financial Corp. has a proprietary airline demand model that suggests that retail demand is 80 to 85% recovered compared to pre-pandemic levels.

- Chase card spending on air travel continued to improve in 2021 and, on an indexed basis, is approaching levels not witnessed since 2019. A similar positive momentum was seen with combined Bank of America debit and credit card data, with daily airline spending above 2019 levels.

- According to Seaport Research, Southwest Airlines is the industry’s pricing leader, and its cost challenges in 2022 could lead to a better pricing environment for Spirit Airlines and other such carriers.

Weaknesses

- According to Goldman Sachs, labor inflation has been called out across the industry as the main driver of higher-than-expected costs exiting the year 2021. For example, many carriers have had to raise minimum wage for relevant employees to attract and keep talent and have had wage inflation through third-party suppliers passed on, too. Additionally, with labor shortages for trained pilots and mechanics widespread in the U.S., the group expects to see continued upward rate pressure as labor contracts are re-negotiated.

- Airline shares underperformed the market due to fears that a surge in oil prices will inflate the price of jet fuel, undermining a recovery in air travel. Crude had topped $80 a barrel recently. With shortages of natural gas and coal raising the possibility of a full-blown energy crisis, analysts say it could go higher still. Fuel expense accounts for 25% of an airlines’ overall expense.

- European airlines are far more exposed to the higher fuel prices than pre-pandemic as they have reduced hedging during the crisis. Prior to the pandemic, European airlines hedged 50 to 90% of their 12-month jet-fuel consumption. However, the grounding of fleets during the crisis has resulted in large hedging cash losses and most companies have reduced hedging levels as a result. For example, British Airways will shrink its hedging to 60% of its requirements. They were 90% hedged when oil prices collapsed last year, which created losses. Lufthansa is cutting their fuel hedges by 20%. While most of the U.S. airlines no longer hedge fuel, Southwest and Alaska Airlines are 69% and 52% hedged, respectively. Among the Asian airlines, only Singapore Airlines and most Japanese airlines are fully hedged.

Opportunities

- According to the Bank of America, bookings across the U.S. and Europe improved following the COVID-19 Delta variant outbreak over the summer of 2021. 27% of global business travelers have already started to travel again, and 46% now expect to be on the road in 2022. U.S. business travelers appear eager to get back on the road, with 29% responding that they expect to take their next trip in the first quarter of 2022 and another 23% later in the year.

- The recently passed bipartisan Infrastructure Bill will help improve the nation’s airports. As part of this new infrastructure deal, $25 billion USD will be invested in airports to address repair and maintenance backlogs, reduce congestion and emissions near ports and airports, and drive electrification and other low-carbon and carbon-free technologies.

- The TSA extended its travel mask mandate through January 18 to minimize the spread of COVID-19 on public transportation. Dr. Anthony Fauci, the U.S.’s top infectious disease doctor, supports a vaccine mandate for air travel, but not all airlines are on board with this. Dr. Fauci told the Washington Post that he is supportive of a vaccine mandate for air travel but is not actively endorsing it. However, if President Biden wanted to enforce vaccines for air travel, Dr. Fauci said he would be supportive of it.

Threats

- UBS, a Swiss multinational investment bank, analyzed 247 countries and regions (covering roughly 60,000 travel routes), and continued to show elevated levels of travel restrictions. Global travel restrictions remain high at 84% of global routes. Intra-EU travel restrictions remain close to 100% of routes.

- Travel budgets may not recover to 2019 levels. The expectation is for an average of 29% of 2022 travel budgets to be allocated instead to virtual meetings. ‘Virus concerns’ were the primary reason cited for using virtual meetings. Chairman and CEO of American Airlines, Doug Parker, stated that he remains bullish on business travel and believes video communication platforms such as Zoom can and will co-exist with corporate travel, rather than compete. Delta Airlines has indicated that corporate travel could resume as corporate offices and borders reopen. 80% of Delta’s corporate accounts are seeing increases in ticketing already.

- COVID-related negative headlines are likely to continue to pressure airlines shares in the near term, until more is understood about the Omicron variant or until U.S. and European COVID cases start to decline again. This includes new travel restrictions that, except for those placed on travel to-and-from certain African countries, have been restrained in most cases in North America and Europe.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Czech Republic, gaining 38.84%. The best performing country in Asia this week was Taiwan, gaining 25.91%.

- The Russian ruble was the best relative performing currency in emerging Europe this week, losing 1.35%. The Taiwan dollar was the best performing currency in Asia this week, gaining 2.95%.

- Within emerging markets, the Czech Republic was the best performing country, rebounding sharply in 2021. The country was among the first nations to hike rates due to spiking inflation, setting the stage for a shift in global monetary policies. In Asia, Vietnam and Taiwan outperformed due to strong exports, supported by strong demand for electronic products during the pandemic. Geographically, Vietnam has a strategic location for its high-performing export sector. Samsung, the South Korean multinational manufacturing conglomerate, allocates over half of its mobile phone manufacturing capacity to Vietnam.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Russia, gaining 15.15%. The worst performing country in Asia this week was Hong Kong, losing 13.37%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 44.12%. The Thailand baht was the worst performing currency in Asia this week, losing 9.74%.

- At the end of 2021, The Hang Seng Index was trading at its lowest level relative to the MSCI All Country World Index in over two decades. The losses have been the deepest and broadest in the technology sector amid Beijing’s clampdown on big technology names. Among the worst-hit tech giants, Alibaba Group Holding Ltd. has tumbled about 50%, while Xiaomi Corp. has dropped 45%.

Opportunities

- The World Health Organization suggested 2022 will see the end of the acute stage of the COVID pandemic, as the world knows the virus well and has all the tools to fight it. These comments come as recent studies suggest Omicron may lead to lower hospitalization rates than previous variants.

- China’s central bank pledged greater support for the real economy and said it will make monetary policy more forward-looking and targeted. The PBOC has so far taken a restrained approach to monetary stimulus, but expectations are growing that it will do more in the new year, especially if property market problems and slowing private consumption continue. Asset managers expect China’s stock market to outperform the U.S. market in 2022. It will be a year of the tiger in China.

- Goldman Sachs predicts a new high in oil demand in 2022, and again in 2023. Oil demand was already at record levels before the latest Omicron variant hit, and furthermore, demand for air travel should continue to recover, Damien Courvalin, the investment bank’s head of energy research said. Countries producing this commodity should benefit from higher prices. Russia could continue to strengthen its balance sheet next year and the country’s commodity producers could continue to pay record high dividends, assuming there will be no escalation of tensions on the border with Ukraine.

Threats

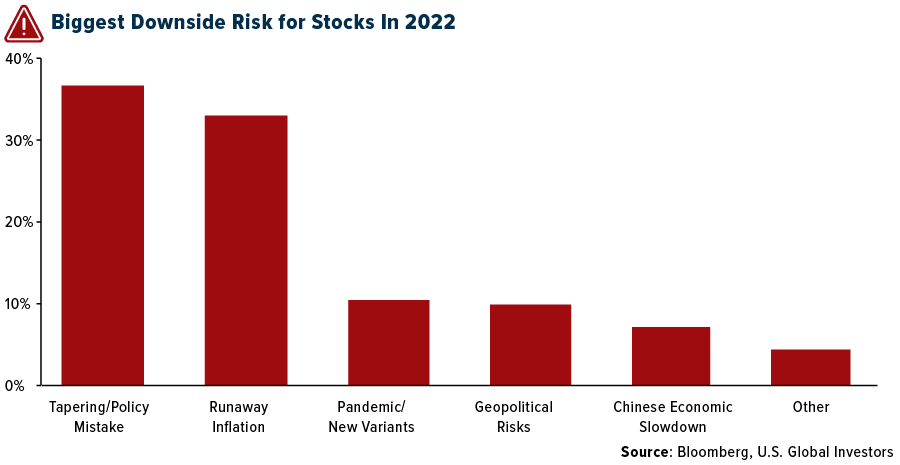

- A policy mistake by central banks due to surging inflation will present the biggest risk for global stocks in 2022, according to a survey of more than 100 fund managers. Monetary policy is the top concern for nearly 37% of those surveyed, followed by runaway inflation.

- Turkey experienced extreme volatility in equities and currency at the end of the year. This month, the Borsa Istanbul Stock Exchange has gone from a record high to a bear market in less than a week. The Turkish lira is the world’s worst performing currency. The government announced measures to protect its currency, but volatility in Turkish markets could continue into 2022.

- China’s property downturn is expected to continue into the first half of 2022, with home prices and sales falling as tight credit policies and a looming property tax dampen demand, a Reuters poll showed. The property sector is a key driver of growth in China, but it has slowed sharply in recent months due to tight regulations and a growing liquidity crisis.

Energy & Natural Resources

Strengths

- U.S. coal prices surged to the highest in more than 12 years, threatening to bloat America’s already soaring electricity bills and signaling the dirty fuel is not getting phased out anytime soon. Prices for coal from the Powder River Basin soared over 160% for 2021. That is the highest since 2009, when a spike in exports boosted domestic prices for the power-plant fuel.

- Tin jumped more than 90% but there are few public ways to get direct exposure. Palm oil approached a 70% gain for the year, moving higher with crude oil but also from strong demand from the food industry. Coffee prices climbed better than 65%, its best year in more than a decade, on weather related crop damage in Brazil, which decimated coffee plantations. Shipping and supply constraints also contributed to its scarcity value.

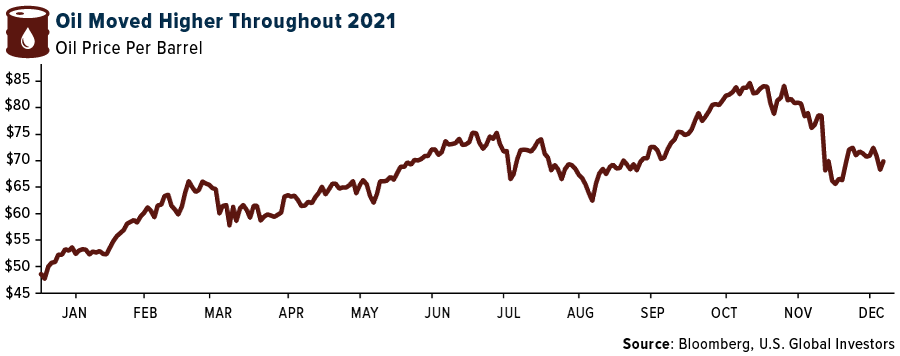

- Oil prices gained about 60% over the course of 2021. Oil prices in the $70 to $80 a barrel range are once again spurring a revival of shale drilling in America’s biggest oil field, where production is expected to return to pre-pandemic highs. Saudi Arabia’s energy minister warned traders against shorting oil, saying OPEC+ could react quickly to any fall in prices. OPEC+, a 23-nation group led by Saudi Arabia and Russia, decided on December 2 to raise daily crude output by 400,000 barrels in January. But it kept the meeting open and said it would be able to reconvene at short notice to change course.

Weaknesses

- Precious metals had some excitement earlier in the year, but as other sectors such as energy offered more visible returns in the short term, money largely left the precious metals sector. Palladium was hit the worst, down about 24% on substitution to platinum which also fell close to 11%. Silver fell about 12% and gold looks to finish the year off about 4%.

- Of the major global commodities only one had negative returns; iron ore looks to finish 2021 down about 23%. Iron ore prices are falling as China appears to be enforcing its target of steel production being flat in 2021. This has resulted in mills destocking and iron ore prices falling sharply in a thin spot market.

- The base metals performed well but were largely in the bottom half of the returns for commodities. Zinc gained about 31%, copper fell back some, but still was up 26%. Lead rose nearly 18%, while uranium, proxied by the price of the Sprott Physical Uranium Trust, finished the year up 11% after a strong spike earlier in the year.

Opportunities

- Saudi Arabia said global oil production could drop 30% by the end of the decade due to falling investment in fossil fuels. “We’re heading toward a phase that could be dangerous if there’s not enough spending on energy,” Oil Minister Abdulaziz bin Salman said in Riyadh. The result could be an “energy crisis,” he said. According to Raymond James, its bullish oil view over the next few years is supported by 1) low global inventories, 2) visible recovery in demand, 3) the coming collapse in OPEC+ spare capacity, and 4) the need for a higher price to further incentivize U.S. supply.

- Aluminum prices rose about 43% in 2021. This is due to increases in costs of energy and raw materials used to make the metal and output cuts by the biggest producer, China. China’s production, already curbed by a government anti-pollution drive, has been further hit by power shortages gripping the country. China’s measures to control energy use and prevent pollution are setting up a tighter market. Demand will exceed production by 1.5 million tons in 2022, Aluminum is heading for a seismic shift as a long-running supply glut starts to fade, setting the stage for shortages and a price rally that could run for years.

- Lumber prices moved up about 60% this year, but in hindsight it was a roller coaster ride. Lumber prices soared about 140% until about halfway into May then tumbled about 73%, bottoming in mid-August. Then lumber prices saw another 143% rally to close the year, still with a nice gain. Lumber could still remain strong in the future if interest rates remain low with modest growth.

Threats

- Cotton, corn, sugar, soybeans, and wheat all jumped in price, with cotton at the top with a 50% gain and wheat pulling up the low end with a 20% gain. Global fertilizer inventory levels are not just tight, but for many countries are simply unavailable and/or too expensive for small traders. This is set to intensify because of shuttered nitrogen production in the EU from high gas costs, along with the export bans imposed by China and Russia. Crop yields could be impacted, resulting in potential food supply issues and ultimately political instability.

- Cracks are emerging in the global solar industry, threatening to flatten its growth trajectory just as the world needs clean power more than ever. A barrage of obstacles is slamming the sector, with rising materials costs, forced labor accusations and a worsening trade war all hitting at once. This year marks the first-time solar costs have increased since 2007. “This year is a perfect storm,” said Xiaojing Sun, head of solar research at Wood Mackenzie, pointing to a triple whammy of contributing factors: a sharp rise in component prices; tariffs and sanctions; and soaring shipping costs. Polysilicon, an essential component for solar panels, has tripled in price since January, with increased demand and power shortages in China responsible for the rise.

- The Baltic Dry Index, which tracks the cost to ship major raw materials including coal and iron ore by sea, has climbed to its highest level since late-2009. The index has been rising since bottoming out in mid-2020 due to strong demand on increased consumer spending, as well as supply constraints related to COVID-19 and a lack of investment in new capacity following the last down cycle (per the Economist). While the strong demand is a positive signal for metals end-use, rising shipping prices and constraints could signal that further logistical challenges and cost inflation are on the horizon.

Domestic Economy & Equities

Strengths

- The economy has stayed on the path of recovery throughout 2021, and the United States labor market is experiencing a near-record number of job openings. The unemployment rate continued the slow throughout the year and is on the path to pre-crisis levels.

- Manufacturing activity remained strong in 2021 as well. The IHS market hit a record-high in July, with a reading of 63.4, supported by stronger expansions in output and new orders. December’s reading came in weaker, at 57.8, but continues to stay well above the 50 level that separates growth from contraction.

- Devon Energy, an oil and gas exploration and production company, was the best performing S&P 500 stock for the week, increasing 186.87%. Shares gained with higher oil and gas prices.

Weaknesses

- In 2021 pandemic disruptions have seen costs soar, with annual consumer price inflation growing at its fastest pace in nearly 40 years. Inflation surged 6.8% in November, even more than expected, to the fastest rate since 1982.

- The shortage of chips needed for everything from cars to fridges has dragged on for more than a year now. Entire industries have been pitted against one another in fierce competition for chip supplies. Technological warfare between the U.S. and China has created semiconductor tension.

- Penn National Gaming Inc., an online gaming and sport betting company, was the worst performing S&P 500 stock for the week, losing 39.92%. Shares declined as momentum in its core business slowed.

Opportunities

- Investors are too bearish, according to JPMorgan, noting that hawkish central bank and bearish Omicron narratives have gone too far. The bank sees no reason to fear an end to the U.S. stock market rally, saying conditions for a selloff are not in place given already low positioning and record buybacks, among other things. It also noted the equities rally may become broader in January.

- Total nonfarm payrolls have made a remarkable recovery since the trough in April 2020 but remain below the pre-pandemic peak. The participation rate has room to increase in 2022, boosted by stronger business capital spending and a broadening out in job creation. The climb will likely continue although it could be slow.

- The global economy is set to surpass $100 trillion for the first time in 2022, two years earlier than previously forecast, according to the Centre for Economics and Business Research. Global GDP will be lifted by continued recovery from the pandemic, but if inflation persists it may be hard for central bankers and politicians to avoid hiking rates. The London research firm predicted China will overtake the U.S. in 2030, two years later than it forecast just a year ago.

Threats

- The virus, and this year’s inflation surge, have put a dent in broader measures of consumer confidence. Consumer confidence about the present situation has weakened this year, but there’s been an even greater deterioration in expectations for the future. Elevated inflation may continue to put pressure on goods consumption.

- The healthy recovery combined with persistent price pressures has prompted the Federal Reserve to start withdrawing support that helped the American economy to boom. The Fed announced a pace of reduction of balance sheet additions of $15 billion per month but only for November and December. The big question heading into 2022 is whether the Federal Reserve will speed up the pace of tapering or not. For now, the Fed plans to complete tapering before it begins hiking rates.

- S&P 500 earnings have been on fire since mid-2020, with a sharp v-recovery into the second quarter peak. Earnings growth is expected to decline in the first half of next year, according to Goldman Sachs’ 2022 U.S. Outlook.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by Messari, the best performer for 2021 was PieDAO Metaverse, rising 291,592.72%.

- One of the major stories in crypto this year happened on June 5, when El Salvador President Nayib Bukele declared that Bitcoin would become legal tender in El Salvador. Just a few days later the law was passed and scheduled to take effect on September 7. In El Salvador, all businesses are now required to accept Bitcoin as payment.

- The first Bitcoin ETF in the United States launched on October 19, 2021. The ProShares Bitcoin Strategy ETF, trading under ticker symbol BITO, offers investors an opportunity to gain exposure to Bitcoin returns through futures contracts traded at the CME.

Weaknesses

- Of the cryptocurrencies tracked by Messari, the worst performer for 2021 was Cardstack, down 99.99%.

- China’s most powerful regulators intensified the crackdown on cryptocurrencies this year, with a blanket ban on all crypto transactions and mining, hitting Bitcoin and other major coins hard. Beijing-based regulators, in particular, joined forces to explicitly ban all cryptocurrency-related activity in the country.

- Elon Musk had a sudden change of heart over accepting Bitcoin to buy his electric vehicles, citing concerns over “rapidly increasing use of fossil fuels for Bitcoin mining and transactions.” According to some sources, at current rates Bitcoin mining uses the same amount of energy annually as the Netherlands, and depending on the mining company, can rely on fossil fuels, particularly coal.

Opportunities

- India’s highly anticipated crypto regulation bill will probably be introduced to Parliament in late January or early February 2022. The Cabinet has already had informal discussions around the draft bill. Once the bill is approved by the Cabinet, it is likely to go to the standing committee on finance in parliament.

- Web 3.0 has yet to come but is the next step to web evolution, making the internet more intelligent. Web 3.0 should also be able to process information with near-human-like intelligence through the power of A.I. systems that run smart programs to assist its users. Content creation and decision-making processes will involve both humans and machines. This would enable the intelligent creation and distribution of highly tailored content straight to every internet consumer.

- 2022 could be the year that the SEC approves the first spot Bitcoin ETF. The CEO of Grayscale is among a few others that are very optimistic about the acceptance of such an ETF in the new year.

Threats

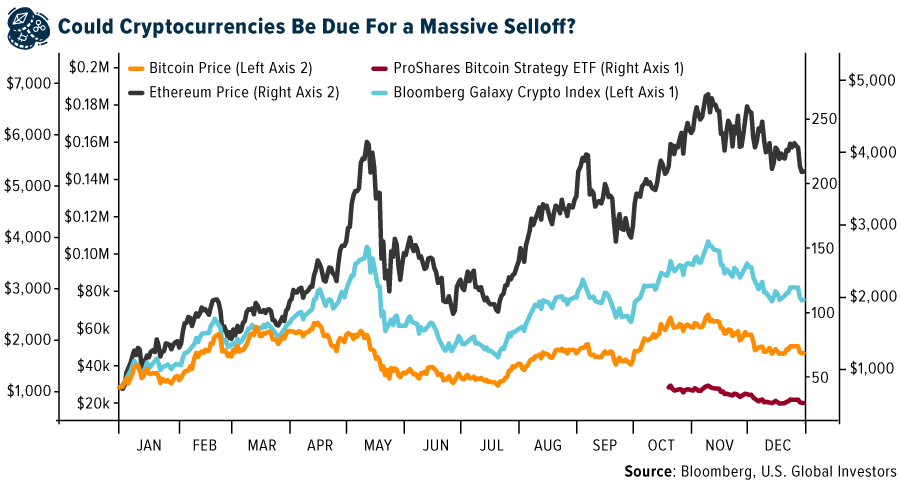

- Some experts believe that Bitcoin is due for a sharp decline in the coming months. The cryptocurrency surged to a record high of $69,000 in November 2021 to retrace back under $50,000, down almost 30% from its peak. Some believe that Bitcoin will drop to as low as $10,000 in 2022 wiping out all of its gains in the past year and half.

- According to Palo Alto Network, an increase in scams related to cryptocurrency, data breaches, and frequent identity thefts and frauds, are top cyber security threats for 2022.

- The aggregate growth of stablecoins could have important implications for the financial system and the macroeconomy. If insured depository institutions lose retail deposits to stablecoins, and the reserve assets that back stablecoins do not support credit creation, the aggregate growth of stablecoins could increase borrowing costs and impair credit availability in the real economy.

Gold Market

This holiday-extended week spot gold closed at $1,829.21, up $20.40 per ounce, or 1.13%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.10%. The S&P/TSX Venture Index came in up 1.12%. The U.S. Trade-Weighted Dollar fell 0.40%

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-22 | GDP Annualized QoQ | 2.1% | 2.3% | 2.1% |

| Dec-22 | Conf. Board Consumer Confidence | 111.0 | 115.8 | 111.9 |

| Dec-23 | Initial Jobless Claims | 205k | 205k | 205k |

| Dec-23 | Durable Goods Orders | 1.8% | 2.5% | 0.1% |

| Dec-23 | New Home Sales | 770k | 744k | 662k |

| Dec-28 | Hong Kong Exports YoY | 18.0% | 25.0% | 21.4% |

| Dec-30 | Initial Jobless Claims | 206k | 198k | 206k |

| Jan-3 | Caixin China PMI Mfg | 50.0 | — | 49.9 |

| Jan-4 | ISM Manufacturing | 60.2 | — | 61.1 |

| Jan-5 | ADP Employment Change | 360k | — | 534k |

| Jan-6 | Germany CPI YoY | 5.1% | — | 5.2% |

| Jan-6 | Initial Jobless Claims | 200k | — | 198k |

| Jan-6 | Durable Goods Orders | — | — | 2.5% |

| Jan-7 | Eurozone CPI Core YoY | 2.5% | — | 2.6% |

| Jan-7 | Change in Nonfarm Payrolls | 400k | — | 210k |

Strengths

- The best performing precious metal for the year was gold, but still down 3.64% on the threat of the Federal Reserve beginning to raise interest rates in 2022 and that inflation will subside substantially in the second half of 2022 as supply bottlenecks are cleared. That perceived outlook as we close out the year is the base case, but as we know, there are always deviations and unexpected events to look forward to in the precious metals space in 2022.

- Gold exploration budgets have increased 43% year-over-year to a total of $6.2 billion in 2021, outpacing the 35% increase in the global nonferrous exploration budget. Gold’s surge has been driven by higher junior company financings and exploration plans carried over from 2020. Funds raised by junior and intermediate companies totaled $5.5 billion in 2021, the most since 2012 and a clear sign of heightened investor confidence in the yellow metal. This has allowed the junior sector, which had been on a general downtrend in terms of exploration since 2012, to fund its exploration plans. There are more than 200 additional companies exploring for gold in 2021 than in 2020.

- Retail gold sales in China have rebounded with bracelets, pendants, earrings, and necklaces that draw on dragons, phoenixes, peonies and other traditional Chinese patterns and symbols being strongly desired by consumers. Sales are strongest to those in their 20s and 30s, helping drive a rebound in gold demand in the country after a pandemic-induced slump. Chinese consumers must be doing better economically as a rise in demand for what is known as “heritage” gold jewelry, which requires intricate craftsmanship and can command premiums of 20% or more over conventional gold jewelry, are finding willing buyers.

Weaknesses

- Palladium was the worst performing precious metal, down 22.35% for 2021. Substitution for palladium by platinum is the cure for high prices and has become a stronger force as we closed out the final quarter of the year. In addition, gasoline car sales, where palladium is used to clean emissions, have been impacted by COVID related work issues including no computer chips to build the car with.

- Silver was the second worst performing precious metal for the year, falling 11.74%, on somewhat lighter solar cell supply. The U.S. dollar regained almost all the 6.69% fall it experienced in 2020 with this year’s bounce back from coming out of the throws of the pandemic.

- While the dollar moved higher, surprisingly the real rate on the generic 10-year TIP started the year at -1.087 and finished 2021 at -1.099, essentially the same place we began. Yet, gold is around 3% lower. The Fed may have real issues getting rates up and the workforce, our labor supply, has much more to say about where the economy is going. Labor is now more likely to make gains in unionizing in order to have more bargaining power.

Opportunities

- Industry consolidation began to take place in more earnest this year. Size matters, and that’s what may have been behind Agnico Eagle Mines’ bid to buy Kirkland Lake Gold. There certainly are operational synergies that can be garnered from the deal. It does give Agnico access to the Detour Lake assets which are likely to be long lived but could see some issues if energy prices rise too much.

- In another move to acquire more assets in mining jurisdictions, Newcrest Mining agreed to buy Pretium Resources Inc. in a cash and shares deal valuing the Canadian gold producer at about $2.8 billion. Newcrest and others were patient to wait out the story and really see what the mine was capable of before inking the deal. This gives Newcrest a strategic view to other major mineral discoveries in the region.

- Scarcity. Is that the new issue in the industry that the majors are contending with? Can’t find enough +10-year life mines that can produce 300,000 ounces of gold per year? You do that by exploring or buying ounces in the ground or in the most recent example, Kinross Gold buying Great Bear, you bought exploration. What is fascinating is there is no publicly calculated resource on the discovery, but the drill data is available on the company’s website, so it really wasn’t a black box acquisition. However, it does signal the gold industry may be more willing to do deals more aggressively in the future. There are plenty of good assets in the junior miners and the explorers too that are likely to be on the wish list for next year.

Threats

- Bitcoin remains a key competitor to gold. Like gold, Bitcoin functions as an absolute store of value. Most analysts expect gold to gradually decline over the next few years. The post-pandemic recovery, Fed tapering, and a stronger dollar will all weigh on the metal, which will fall to $1,700 an ounce by year-end and then decline further in 2022, UBS Group AG strategists including Wayne Gordon and Giovanni Staunovo, said in a note. However, new government regulation over Bitcoin and other electronically traded crypto assets could change their desirability for ownership.

- Exchange-traded funds have been selling gold, with this year’s net sales being 9.24 million ounces, according to data compiled by Bloomberg. Total gold held by ETFs fell to 97.82 million ounces. Rising real rates are the ultimate threat to gold prices but there is great concern that the U.S. can withstand rising rates. Who can take the medicine? It took 20-years to leave Afghanistan, how easy is it going to be to walk away from “easy money”?

- Demand for platinum group metals (PGMs) are facing decline due to the growth of battery electric vehicles. Sibanye Stillwater CEO Neal Froneman said palladium could decline to about $1,000 an ounce after 2025 as automakers switch to using more platinum in auto catalysts used to curb pollution from vehicles. If platinum prices rise with a pickup in fuel cell use, the change in the two PGMs prices may balance out somewhat on their income statement.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All