Commodities Notched Their Best Year Since 2009, Despite Precious Metals Weakness

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEvery year around this time, we update our always-popular Periodic Table of Commodities Returns. I invite you to compare the returns to previous years, download a PDF of the table and more by clicking here.

Commodities as a whole had their best year in over a decade, due in large part to inflation triggered by unprecedented global monetary and fiscal stimulus. The Bloomberg Commodity Spot Index ended 2021 with a gain of 27%, the biggest yearly jump since 2009, when the financial crisis similarly prompted governments and central banks to flood their economies with liquidity.

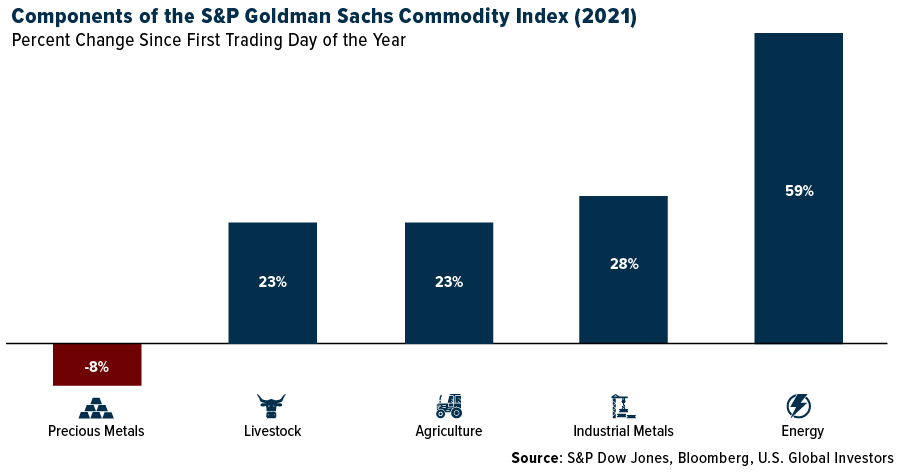

The best performing commodity component was energy, with natural gas up close to 47%, crude oil up 55% and Powder River Basin coal up an eye-popping 160%. Energy increased at double the rate as the second-best category, industrial metals. Aluminum led these materials with an increase of 42%, followed by zinc (up 31%), nickel (26%), copper (26%) and lead (18%).

A Challenging Year For Precious Metals, Gold Greatly Undervalued

As expected, precious metals were the worst-performing category, down 8%. None of the constituents ended the year in positive territory. That includes gold, which was the best performer of the bunch with a loss of 3.6%, despite inflation at a decades-long high.

Platinum and palladium’s slump are easily explained. The two metals, as you may be aware, are used in the production of pollution-scrubbing catalytic converters in automobiles. However, carmakers were hampered by the global semiconductor chip shortage, which slowed the output of new vehicles and hurt platinum and palladium demand. Looking ahead, demand could take a more significant hit as electric vehicles (EVs), which do not need catalytic converters, enter the mainstream.

The main headwind slowing gold in 2021 was the belief that the Federal Reserve would raise rates sooner than expected and reduce its asset holdings to tame inflation. I’ve seen forecasts of as many as four rate hikes in 2022, but I don’t believe the Fed will be that aggressive and risk crashing the economy and stock market.

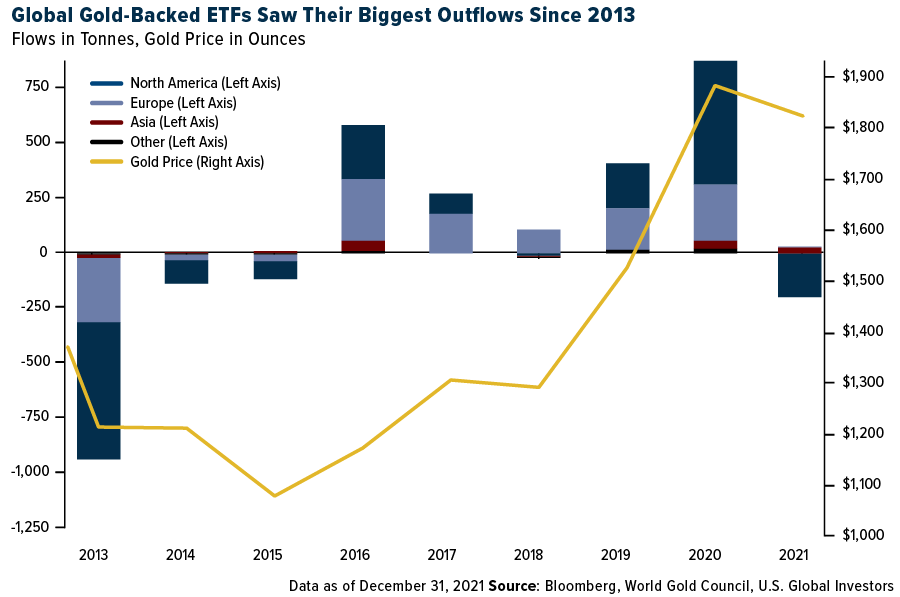

Nevertheless, investors shunned the yellow metal in 2021. Gold-back ETFs saw outflows of $9 billion, with much of that rotation occurring in North American funds, according to the World Gold Council (WGC). This represented the biggest annual outflow since 2013. The WGC points out, though, that despite the selling, gold ETF holdings remained significantly above pre-pandemic levels, as funds experienced record inflows of $49 billion in 2020.

I believe gold is greatly undervalued right now, and as I told Investing News Network’s Charlotte McLeod this week, it should really be about $1,000 an ounce higher than it currently is. Gold’s standard deviation over the rolling 12-month period is approximately 20%. At today’s prices, a one-standard deviation move would put the metal’s value at around $2,150, which would be a new all-time high.

I’m not projecting this will happen. It’s just math and probability. That said, we could be looking at another challenging year as the Fed is set to tighten monetary policy. This would strengthen the U.S. dollar, a headwind for the gold price.

Comeback Kid: Fossil Fuels Surged On Stronger-Than-Expected Demand

Let’s return to energy. An interesting article appeared in the Wall Street Journal this week, penned by Bjorn Lomborg, author of False Alarm: How Climate Change Panic Costs Us Trillions, Hurts the Poor and Fails to Fix the Planet. Lomborg believes that today’s soaring energy prices are “likely a sign of things to come,” thanks to world governments’ climate policies. Specifically, he takes aim at unreasonable decarbonization efforts:

“Limiting the use of fossil fuels requires making them more expensive and pushing people toward green alternatives that remain pricier and less efficient.”

Indeed, I’m sure you felt the pain at the pump this past year, and families in Europe continue to deal with all-time high energy prices.

You might think that coal use is rapidly on the decline, but believe it or not, coal-fired power generation reached an all-time high last year, driven by demand for cheap energy in China, India and other emerging economies. Because production has not kept up with demand, this pushed coal prices to record highs in 2021, making electricity, not to mention food and transportation, even less affordable for families residing in countries that haven’t fully phased out fossil fuels.

Consider Germany. Coal was its primary source of electricity generation in 2021, a year that also saw wind energy drop to its lowest level since 2018. And yet the country—now under the control of the Social Democrats, Free Democrats and Greens—is still on track to phase out coal by the end of this decade.

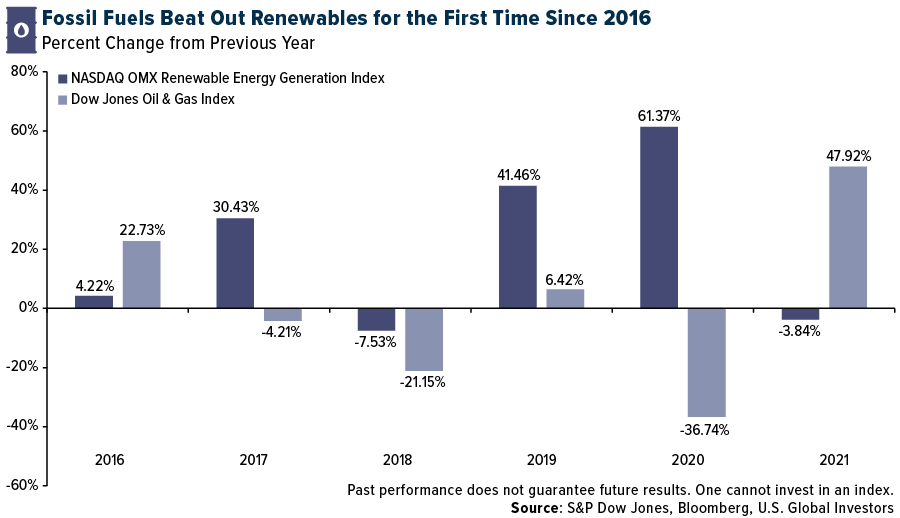

As a result of renewed demand for fossil fuels, companies involved in oil and gas saw their stock surge nearly 50% last year, beating renewable energy companies for the first time since 2016.

Explore the Periodic Table of Commodities Returns, updated for 2021, by clicking here!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.29%. The S&P 500 Stock Index fell 1.87%, while the Nasdaq Composite fell 4.53%. The Russell 2000 small capitalization index lost 2.92% this week.

- The Hang Seng Composite lost 0.72% this week; while Taiwan was fell 0.27% and the KOSPI fell 0.76%.

- The 10-year Treasury bond yield rose 25 basis points to 1.77%.

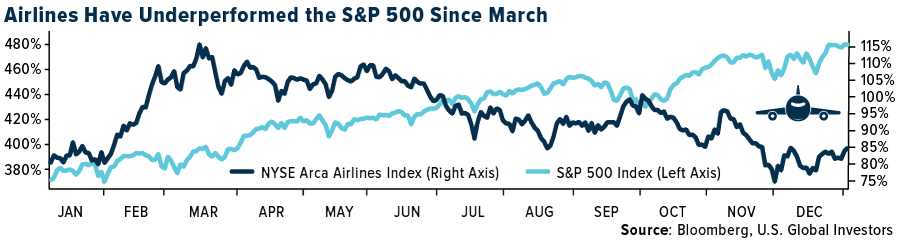

Airline Sector

Strengths

- The best performing airline stock for the week was El Al, up 9%. Over the recent holiday travel period, U.S. domestic air traffic turned positive versus 2019 for the second time in 2021. On December 22, TSA checkpoint travel numbers hit over 2 million.

- European airline bookings enjoyed a surprise improvement in the week, with a sharp increase in both intra-Europe and international bookings, as a percentage of 2019 levels. Bookings over the December Christmas period tend to decline sharply as people take vacation but remained stable in 2021, marking a departure from seasonal trends. Intra-Europe net sales were up by 47 points to -3% versus 2019 (and versus -51% in the prior week) and increased by 35% during the week. Intra-Europe ticket volumes were higher than 2019 levels for the first time since the start of the pandemic. International net sales improved by 10 points to -48% (versus -58% in the prior week) but fell by 10% this week. This led to a 19-point increase in system-wide net sales for flights booked in Europe to -38% (versus -56% in the prior week).

- Chinese domestic air traffic recovered to 64% of normal (from 52% in early December) with local COVID outbreaks confined to just a few provinces, reports Bank of America. This has led to better domestic unit revenues at 82% of normal (from 77% in early December) with domestic yields already back above normal and higher seat loads at 67%.

Weaknesses

- The worst performing airline stock for the week was Air Berlin, down 12.5%. According to Bank of America, in December, airline stocks underperformed for a third straight month at +2.6% versus the S&P 500 +4.5%. Airlines underperformed the S&P in eight of 12 months in 2021, and each month in the fourth quarter, which is historically the strongest quarter of the year for airline stocks (outperformed the last three months to end the year 64% of the time). As long as variants remain, it could be challenging for airline stocks to trade at multiples at the higher end of historical ranges as was the case through much of 2021.

- Global scheduled flight capacity ended 2021 up 11% from 2020 but only at 54% of 2019 levels through the month of December. For January, scheduled flight activity was cut by 2% with capacity now at 70% of 2019 (still up 1% sequentially). Europe cut January ASMs by 3% versus last week (now only at 68% of 2019), while Africa was cut by 5%. February saw a 1% cut in flight activity with capacity now at 74% of 2019 levels.

- Airlines face thousands of cancellations due to bad weather and an increase in COVID case counts amid a busy holiday travel season. Severe weather and a winter storm caused carriers to cancel hundreds of flights at Chicago’s two main airports on Saturday, while disruptions continued on Sunday with other cancellations in Atlanta, Denver, and the New York City area. In addition to the bad weather, several major airlines blamed an increase in COVID infections amongst crew members for the disruptions.

Opportunities

- According to Credit Suisse, after a decent month for consolidated traffic during November, it expects solid traffic volumes during December due to the high seasonality brought by the holiday season. For Mexico, the group expects solid performance as high demand led airlines to increase capacity more aggressively than in previous years posting a high-teens growth.

- System net sales improved to -42.7% versus 2019 for the week (versus last week of -46.3%). During December, system net sales have fluctuated between down -42% to -46%, versus 2019 levels, and remain off the pre-Thanksgiving holiday levels of -33%. Domestic bookings improved this week to -6.1% versus 2019 (versus -11.6% last week) while international bookings modestly improved to -35.6% versus 2019 (versus -36.5% last week). There is more softness in international bookings than domestic bookings amid the omicron variant headlines.

- According to Bank of America, corporate bookings through large travel agencies took a significant step up to -18.0% versus 2019 (versus -36.3% last week), but this can likely be explained by the timing of the 2021 data versus 2019 data. Given the omicron variant has delayed return to office plans and has also caused other companies that were previously in the office to ask employees to work from home to start the year, it anticipates corporate bookings will take a step back in the coming week’s data.

Threats

- S. airlines warn that more flight disruptions may occur if the launch of the new 5G wireless service is not delayed. Earlier this week, Verizon and AT&T rejected a request by the U.S. Government and Airlines for America (A4A) to delay the rollout of the new 5G wireless service. After the two major wireless carriers refused requests to delay the January 5 launch, the A4A trade group warned that the activation of the new 5G services could result in widespread disruptions as airplanes divert to other cities and/or flights are cancelled.

- In the past three weeks, domestic net sales have been flat or improved, primarily driven by lower ticket pricing to stimulate demand as domestic ticket prices have decelerated to -19.1% versus 2019 (versus -14.6% two weeks ago).

- Delta has been more proactive in cutting capacity than its peers as it lowered its March domestic schedules to -7.8%. This month, American and United cut their March domestic capacity by -16.4% and -5.2%, respectively. For the first quarter, the network carriers and Southwest Airlines are showing domestic schedules at 96% of 2019 levels while the ultra-low cost carriers are currently planning to fly 123% versus 2019 levels.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 9.5%. The best performing country in Asia this week was India, gaining 2.86%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 2.54%. The Vietnamese dong was the best performing currency in Asia this week, gaining 0.53%.

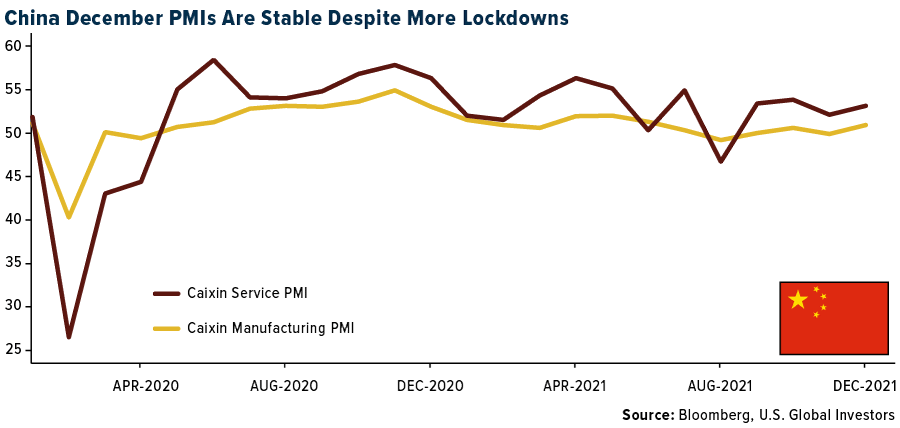

- Despite additional lockdowns due to the growing number of COVID outbreaks across China, Caixin PMIs remained strong in the month of December. The Caixin China Manufacturing PMI increased to 50.9 from 49.9 in November, and the Caixin Service PMI spiked to 53.1 versus 52.1 in November.

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 0.40%. The worst performing country in Asia this week was Malaysia, losing 2.55%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 3.8%. The Thailand baht was the worst performing currency in Asia this week, losing 1.3%.

- Violent protests erupted in Kazakhstan after the government hiked fuel prices, which later turned into large-scale operations including citizens asking for free elections along with moves against corruption. The country’s largest airport was seized, banks and stock exchanges were closed, and the internet was shut down. Russia, Kazakhstan’s major trading partner, sent peacemakers to bring order to the country.

Opportunities

- Goldman strategists see European stocks as a promising investment amid rate hikes. On Wednesday, the U.S. Federal Reserve signaled that interest-rate hikes could be more aggressive than many had expected. Goldman argues that valuations in European markets are not as stretched as they are in the U.S. European shares have consistently underperformed their U.S. peers since the global financial crisis but now is the time to focus on Europe.

- China’s Securities Regulatory Commission said, without giving details, that it will adopt various measures to avoid volatility and prevent fluctuations in the stock market following a difficult start to the year, reports Bloomberg. Chairman Yi Huiman’s comments came after the CSI 300 Index fell for the first four trading days of the year before a modest recovery on Friday.

- China will likely continue to provide its support to the economy. Bloomberg economists predict money supply to increase 7.4% in December versus 7.2% in November on a year-over-year basis. The People’s Bank of China (PBOC) announced a 50-basis point cut reserve requirement ratio, effective from December 15, and will likely ease again soon.

Threats

- Poland was the first country in the world to increase rates this year. The central bank hiked its main rate by 0.50% to 2.25%, setting the stage for other players to do the same. Inflation could reach 8% in June and additional hikes will be needed to bring it down.

- If order is not restored in Kazakhstan, important players in the oil market, producing around 2 million barrels of oil per day, could lead to production distributions. Russia and Turkey are major trading partners with Kazakhstan. Lukoil has minority stakes in two of the three largest oil fields, and Sberbank is the second largest bank in Kazakhstan. There are a handful of other Russian and Turkish companies connected with Kazakhstan through business partnerships.

- With the Omicron variant spreading throughout the European Union, daily cases of coronavirus exceeded 1 million on Wednesday for the first time since the start of the pandemic. Omicron symptoms are relatively mild compared to other variants, but governments still worry about pressure on the healthcare system. Italy made vaccines mandatory for all citizens over 50 years of age.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was uranium, as proxied by the Sprott Physical Uranium Trust, up 8.55%, on unrest in Kazakhstan. Lumber trading finished off a record year with quotes continuing to move higher despite softening momentum. Prices ended the week up better than 8%.

- The average price of lithium, a key material in electric vehicle (EV) batteries, surged 434% year-over-year to a record $43,143. The increase was boosted by strong demand for EV batteries as carmakers transition to clean-energy vehicles.

- The U.S. was the world’s biggest exporter of liquefied natural gas last month for the first time ever, as projects ramped up production and deliveries surged to energy-starved Europe. Output from American facilities edged above Qatar in December due largely to a jump in exports from the Sabine Pass and Freeport facilities, according to ship-tracking data compiled by Bloomberg. Cheniere Energy Inc. said last month that it achieved its first cargo from a new production unit at its Sabine Pass plant. A shale gas revolution, coupled with billions of dollars of investments in liquefaction facilities, transformed the U.S. from a net LNG importer to a top exporter in less than a decade.

Weaknesses

- The worst performing commodity for the week was sugar, down 4.40% on increasing global supplies pushing down prices to their lowest in nearly five months. Protests have swept through Kazakhstan due to government subsidies on fuel prices ending. Kazakhstan produces more than 40% of the world’s uranium. Uranium prices jumped to $45.25 a pound from $42, according to UxC LLC, which noted there isn’t a shortage of uranium right now but people are trading on the potential of a shortage.

- Factory activity and commodities demand in China, which had showed signs of stabilizing in December, could face fresh headwinds in the New Year as key producing provinces jack up power prices. Last month’s PMI readings put the manufacturing sector in expansion just as inflationary pressures on the economy eased. But a round of power hikes designed to counter the kind of outages that plagued the country in the autumn, could stifle the recovery.

- Bloomberg reported that for the first time in roughly half-century of the liquified natural gas (LNG), China has overtaken Japan as the world’s largest importer of the supper-chilled fuel. Analysts have been surprised by the surge in LNG demand by China over the last five-years, but the country is pivoting to use cleaner natural gas and cut back on coal use to limit pollution.

Opportunities

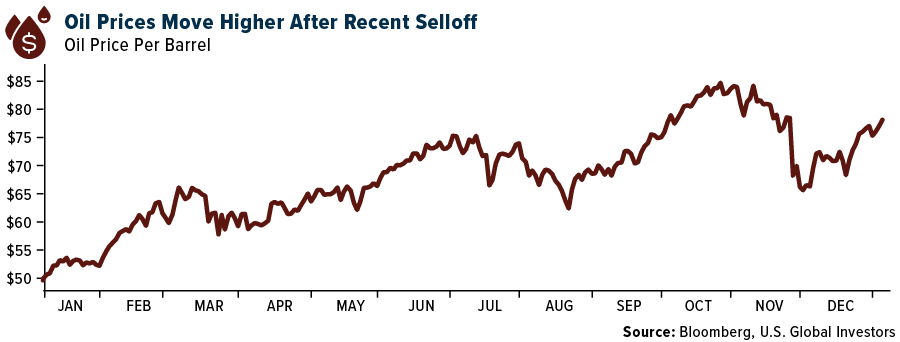

- The energy sector remains “primed for another good year” as crude and oil product prices are likely to benefit from demand topping 2019 levels, according to UBS analysts including Giovanni Staunovo. Brent crude is seen between $80-$90 per barrel in 2022. Oil demand may see robust growth of 3.4 million barrels per day in 2022, bringing full-year demand to 100.2 million barrels per day, slightly above the 2019 average. According to Raymond James, a more balanced market could be seen in both 2022 and 2023. The group forecasts WTI averaging $75 per barrel and ending 2022 at $80, followed by an average of $80 in 2023, with Brent at a modest premium.

- Bloomberg writes that a large dividend and a robust pivot toward clean-energy products could make United Kingdom–based diversified miner Rio Tinto a good bet for investors. In December, the company, which currently gets three-fourths of its Ebitda from iron ore, announced that it would buy the Argentina-based Rincon lithium project for $825 million. The deal, which needs regulatory approval, would make Rio Tinto a major battery-grade lithium producer. “What’s interesting is that they have proactively gone out and found this deal, and they will continue to look for similar opportunities,” Sophie Lund-Yates, a senior equity analyst at U.K.-based broker Hargreaves Lansdown, tells Barron’s. “Not everyone has the firepower to make those changes.” In other words, Rio Tinto has the desire and the financial strength to pull off the green switch.

- The boards of Firefinch and Jiangxi Ganfeng Lithium approved the final investment decision for the Goulamina lithium project in Mali. The 2.3 million-tonne-per-year operation is now expected to cost $255 million, up from a prior estimate of $194 million, partly due to costs associated with making Goulamina’s production readily expandable to 4.0 million tonnes per annum. Jiangxi Ganfeng Lithium agreed to either provide a $40 million loan or arrange up to $120 million in third-party debt. This was higher than the previously agreed upon funding of up to $64 million. Firefinch plans to spin out ownership of Goulamina to current shareholders of Firefinch.

Threats

- A new report on copper refining from the world’s biggest supplier of the metal underscores the challenges for mining nations looking to capture more value from their mineral exports. Producer nations from Indonesia to Peru have been pushing to build more of their own smelting and refining capacity rather than just shipping out semi-processed ore to plants in China and Japan. Going downstream means more local investment, jobs, and export revenue — benefits that play particularly well when high prices spur resource nationalism as politicians look to close equality gaps.

- Changes being considered to mining laws and mine ownership in Chile after the election late last year of populist president Gabriel Boric have sent shockwaves through the country’s mining industry, especially its world-leading lithium sector. A proposal by the new president to create a state-controlled National Lithium Company is a direct threat to SQM, one of Chile’s biggest lithium producers, and can be measured in the company’s share price, which has crashed over the past six weeks even as the price of lithium has boomed.

- Amos Hochstein, the U.S. envoy for energy security, said Europe wasn’t doing enough to prepare for the dark and cold season ahead, writes Bloomberg. The continent is grappling with a supply crunch that’s caused benchmark gas prices to more than quadruple from last year’s levels, squeezing businesses and households. The crisis has left the European Union at the mercy of the weather and Russian President Vladimir Putin’s wiles, both notoriously difficult to predict. “The energy crisis hit the bloc when security of supply was not on the menu of EU policymakers,” says Maximo Miccinilli, head of energy and climate at consultants FleishmanHillard EU. He expects the energy crunch to keep prices volatile and also trigger more political tension between regulators in Brussels and the leaders of the bloc’s 27-member states.

Domestic Economy & Equities

Strengths

- The unemployment rate continues to move lower toward the pre-pandemic level. December’s reading showed the unemployment rate at 3.9%, below consensus of 4.1% and November’s 4.2% reading.

- Private sector employment data increased by 807,000 jobs from November to December, according to the December ADP National Employment Report. That is almost double the expected number of 410,000 new job added.

- Discovery, a pharmaceutical company, was the best performing S&P 500 stock for the week, increasing 28.12%. Shares gained more than 16% after Bank of America upgraded its price target from $34 to $45, saying the company’s merger with WarnerMedia could potentially create a global media powerhouse.

Weaknesses

- Initial jobless claims for the latest week came in at 207,000, above the prior week’s upwardly revised 200,000 level. Continuing claims rose to 1,754,000 from last week’s upwardly revised 1,718,000.

- December’s ISM Manufacturing PMI registered its biggest sequential decline in more than a decade. December’s ISM Services PMI was reported lower by 7.1 points month-over-month at 62, missing the 66.7 consensus. However, this reading represents the nineteenth straight month of growth for the services sector, which has expanded for all but two of the last 143 months.

- Humana Inc. was the worst performing S&P 500 stock for the week, losing 28.0%. Shares declined more than 19% on Thursday after the health insurer cut its forecast for Medicare membership growth by about half. The insurer cited higher-than-expected terminations during the recent enrollment window for 2022 Medicare coverage.

Opportunities

- Despite hawkish Federal Reserve comments this week, JPMorgan has pointed out that the G5 (United States, United Kingdom, France, Germany, and Japan) central bank balance sheets are still expected to continue growing faster than nominal GDP in the first half of 2022.

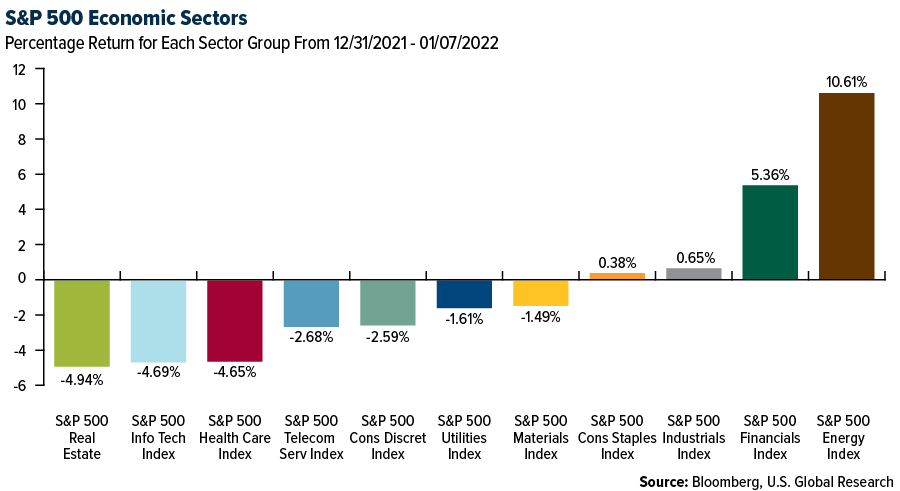

- According to FactSet, S&P 500 earnings are expected to increase by just over 21% year-over-year in the fourth quarter. This would mark the fourth consecutive quarter of earnings growth above 20%, though it represents a slowdown from the nearly 40% growth seen in the third quarter, 91% in the second quarter, and 52% in the first quarter. Nine of the 11 sectors are projected to report year-over-year earnings growth in the fourth quarter, with Energy, Materials, and Industrials as the standouts.

- Retail sales will likely be released stronger for the month of December, supported by the year-end busy shopping season. Data will come out on December 14.

Threats

- Fewer jobs were added in December than expected, however, October and November’s payroll was revised higher. The main disappointment was service sector employment, which will likely be negatively impacted if COVID cases continue to rise. Omicron is the dominant variant, but delta is still responsible for a large number of cases in the U.S., according to the latest data from the CDC.

- Bond yields broke out to the upside this week. The 10-year Treasury yield rose as high as 1.75% on Thursday, as the rate spike in the new year resumed with investors assessing the Federal Reserve’s faster-than-expected policy tightening. The market is now priced for three rate hikes this year and there has been a pickup in speculation about the potential for the Fed to start quantitative tightening much sooner than expected.

- Prices could continue to spike. Inflation is likely to reach 7.1% on a year-over-year basis, higher than the 6.8% reported in November.

Blockchain And Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Aigang (AIX), rising 3,208.68%.

- Goldman Sachs predicts Bitcoin could hit $100,000 within the next five years, writes CNN Business. Co-Head of Global Foreign Exchange says that Bitcoin’s market share will rise over time as a byproduct of broader adoption of digital assets.

- In a recent interview with CoinTelegraph, Kevin O’Leary revealed his cryptocurrency portfolio. O’Leary shared that in individual tokens and chains, he has about 33 different positions with a wide range of diversity. He also stated that his Ethereum position is larger than his Bitcoin position, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Escrowed Illuvium (SILV), down 99.82%.

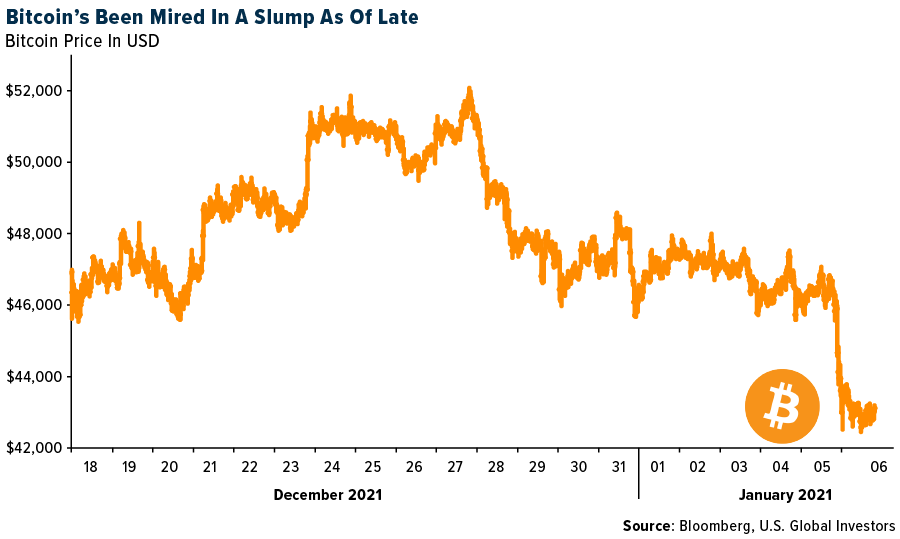

- Bitcoin slid sharply this week after the Federal Reserve released minutes of its December meeting, with policymakers indicating growing unease over inflation and the potential for interest rates to start rising as soon as this March, writes Bloomberg.

- Bitcoin declined to its lowest level since December’s flash crash, writes Bloomberg, after growing expectations of rising borrowing rates weigh on some of the best-performing assets of the past few years. Other cryptos tumbled this week as well, including Ether which took out its own flash-crash bottom to reach prices not seen since October 13, the article continues.

Opportunities

- Developers are flooding into crypto projects even during this price swoon, writes Bloomberg. In fact, the number of monthly active software developers in crypto hit an all-time high in December, despite prices retreating from record levels.

- Crypto company BTCS soared 67% on Wednesday after it announced it will pay the first-ever Bitcoin dividend, writes Markets Insider. This makes it the first Nasdaq-listed company to ever pay a Bitcoin dividend, which the company calls a “bividend.” According to the company, the move will help promote the adoption of cryptocurrency and help build its shareholder base, the article continues.

- According to a new survey from technology-powered real estate brokerage Redfin, roughly on in nine first-time homebuyers said selling cryptocurrency during the fourth quarter of 2021 helped them save for a down payment on their home.

Threats

- Kazakhstan’s government has cut internet access due to escalating protests, and the country’s Bitcoin mining operations appear to be caught in the middle, writes The Block. The situation is notable given that Kazakhstan is home to as much as 18% of the world’s Bitcoin hash rate, as estimated by Cambridge Centre.

- Bitcoin traded near the lowest levels seen since September after an earlier swoon extended its weeks-long decline from an all-time high to about 40%, writes Bloomberg. Ethereum, the second-largest crypto, dropped as much as 9% to its lowest level since September 30.

- According to CoinTelegraph, Hong Kong-based Coinsuper allegedly blocked customer’s withdrawals this week. Five clients reportedly filed police complaints after token withdrawals were apparently halted, leaving them unable to reclaim around $55,000 in cryptocurrency and fiat.

Gold Market

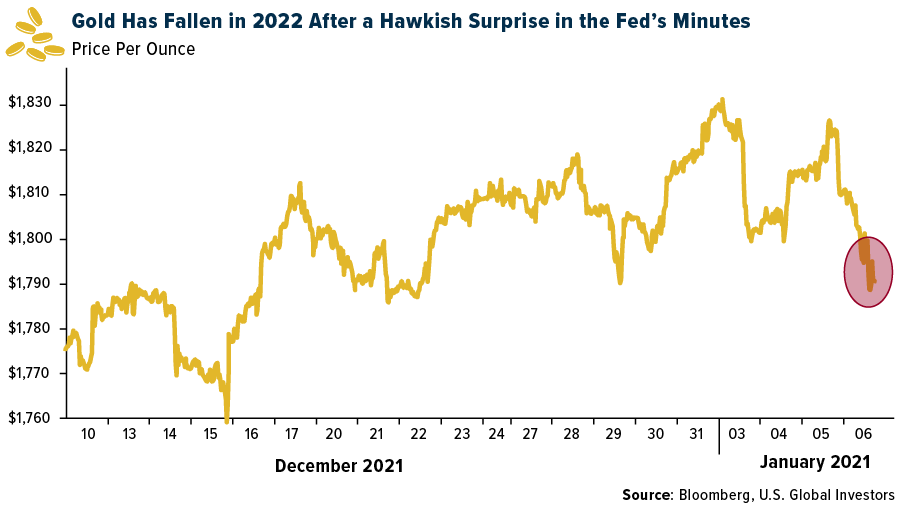

This week spot gold closed at $1,796.55, down $32.65 per ounce, or -1.78%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 6.14%. The S&P/TSX Venture Index came in off 2.95%. The U.S. Trade-Weighted Dollar rose just 0.08%.

| DATE | EVENT | SURVEY | ACTUAL | PRIOR |

|---|---|---|---|---|

| Jan-3 | Caixin China PMI Mfg | 50.0 | 50.9 | 49.9 |

| Jan-4 | ISM Manufacturng | 60.0 | 58.7 | 61.1 |

| Jan-5 | ADP Employment Change | 410k | 807k | 505k |

| Jan-6 | Germany CPI YoY | 5.1% | 5.3% | 5.2% |

| Jan-6 | Initial Jobless Claims | 195k | 207k | 200kk |

| Jan-6 | Durable Goods Orders | 2.5% | 2.6% | 2.5% |

| Jan-7 | Eurozone CPI Core YoY | 2.5% | 2.6% | 2.5% |

| Jan-7 | Change in Nonfarm Payrolls | 450k | 199k | 249k |

| Jan-12 | CPI YoY | 7.1% | — | 6.8% |

| Jan-13 | PPI Final Demand YoY | 9.8% | — | 9.6% |

| Jan-13 | Initial Jobless Claims | 208k | — | 207k |

Strengths

- The best performing precious metal for the week was palladium, up 1.59%, perhaps on the threat of labor negotiations breaking down in South Africa. Gold stabilized largely by Friday after disappointing hiring figures came in at half of what was expected. However, this marks the worst weekly loss in the past six on the 10-TIPS yield, climbing from -1.032% to -0.747%, becoming less negative.

- Exchange-traded funds (ETFs) added 71,225 troy ounces of gold to their holdings in the week. The purchases were equivalent to $128.3 million at yesterday’s spot price. The Perth Mint’s sales of gold coins and minted bars hit a decade high in 2021, thus showing retail interest in the physical metal. More significantly, Ireland has added about 3 tonnes over the past three months to its gold reserves, a 60% increase from the amount held a decade ago, according to Bloomberg.

- Centerra Gold Inc. confirmed that it is engaged in negotiations with representatives of the Kyrgyz Republic to resolve disputes related to Centerra’s Kumtor Mine and the seizure of control of the mine by the Kyrgyz government in May 2021. Centerra expects that the framework for any resolution would involve Centerra receiving the approximately 26.1% in Centerra common shares held by Kyrgyzaltyn JSC (an instrumentality of the Kyrgyz Republic) and upon receipt, Centerra would cancel the shares. The Kyrgyz Republic would assume all responsibility for Centera’s two Kyrgyz subsidiaries and the Kumtor Mine.

Weaknesses

- The worst performing precious metal for the week was silver, down 4.03%, which was expected alongside the hit that gold took. Gold and base metals slid for a second day after minutes from the Federal Reserve highlighted prospects of faster monetary tightening. A strengthening U.S. economy and higher inflation could lead to earlier and faster interest-rate increases, with some policymakers also favoring starting to shrink the balance sheet soon after, according to minutes of the Fed’s December 14-15 meeting. Gold slid as Treasury yields climbed to the highest since April, pressuring non-interest-bearing assets.

- Pure Gold announced fourth-quarter production figures, first-quarter guidance, a change in some executive management, and numerous operational updates. Although fourth-quarter production and first-quarter guidance were both below expectations, the change in management with a strong focus on operational execution is a very welcome change.

- Last week, MAG Silver and partner Fresnillo announced that full load commissioning of the 4,000 tons per day Juanicipio plant will be delayed by at least six months due to additional blackout-prevention requirements and delays in inspections from the Mexican electrical authority. Early ore will be processed at 1,300 tons per day at nearby Fresnillo mills until grid power can be connected, decreasing MAG’s attributable 2022 free cash flow by 50%. While MAG recently secured an additional $80 million in liquidity, this delay does increase the risk to the company’s balance sheet.

Opportunities

- Bank of America forecasts gold and silver to average $1,925 and $30.13/ounce in 2022, +7.0% and +15.1% year-to-year. Gold historically has been a useful portfolio diversifier and hedge against risk uncertainty. A headwind for gold now is the Fed delivering a hawkish shift in late 2022. Aggregate gold equivalent ounce (GEO) output for the North American gold producers is forecast to increase 4% year-to-year to 23.9 million GEO in 2022. During 2021, production was impacted by COVID issues at a number of mines and several companies experiencing operating issues at key mines.

- The Board of RTG Mining reported that the Department of Environment and Natural Resources (DENR) of the Philippines has lifted the four-year-old ban on the open pit method of mining gold and other ores. The lifting of the ban was meant to revitalize the mining industry as there are significant economic and social benefits to be realized, according to the DENR.

- Investors should expect more acquisitions during 2022. According to Bank of America, the race to replace reserves mined has led to accelerated M&A in the global gold sector in the fourth quarter of 2021. There were 11 deals announced (versus a quarterly average of nine deals) at a total value of $5.36 billion (the seventh highest quarterly total since the fourth quarter of 2012). During the fourth quarter of 2021, 8.9 million ounces of gold reserves were acquired, bringing the 2021 total to 18 million ounces. Despite exploration success, they still had to acquire 30% of their reserve ounces through acquisitions, just to stay flat for the year on reserves.

Threats

- According to Bank of America, sector average all-in-sustaining-cost (AISC) could increase 3.8% year-to-year to $1,078 per ounce in 2022. On a third-quarter 2021 results calls, gold company CEOs were expecting cost escalation of around 3% to 7% for materials (steel, copper, and lumber), energy, and labor into 2022. In addition, royalty and production taxes are seen adding up to $30 per ounce to cost structures. Sustaining capital spending is forecast to be over 10% year-to-year.

- Goldman sees oil and copper as better hedges against inflation than gold. Jeff Currie is “extremely bullish” on commodities in general, saying the market is at the beginning of a super cycle that could go on for a decade amid underinvestment in production and spending on green technologies.

- Naysayers who say gold was perhaps the greatest disappointment of 2021 may be missing the boat. For 2021, an inflation hedge that pays no yield, the uber-low real-rate environment offered an almost ideal environment for bullion to rally. Yet the spot metal fell 3.6%. Of course, these pontificators won’t offer up the facts that the gold price was up 18% in 2019 and another 25% in 2020, long before inflation showed up. Oh! But they got one more ace in the hole; the Fed is going to raise interest rates later this year, perhaps as early as March. Trouble is, everybody that is buying gold already knows that.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2021):

Alaska Air Group Inc

American Airlines Group Inc

Delta Air Lines Inc

Deutsche Lufthansa AG

Goldman Sachs Group Inc

Singapore Airlines Ltd

Spirit Airlines Inc

Southwest Airlines Co

SPDR S&P 500 ETF Trust

Tesla Inc.

Alibaba

Kirkland Lake Gold

Sibanye Stillwater

Pretium Resources

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The CSI 300 is a capitalization-weighted stock market index designed to replicate the performance of 300 A-share stocks traded in the Shanghai and Shenzhen stock exchanges.

M2 Money Supply is a broad measure of money supply that includes M1 in addition to all time-related deposits, savings deposits, and non-institutional money-market funds.

Free Cash Flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base.

The Bloomberg Commodity Index is a broadly diversified commodity price index distributed by Bloomberg Index Services Limited.

The S&P GSCI is a composite index of commodities that measures the performance of the commodities market.

The standard deviation is a statistic that measures the dispersion of a dataset relative to its mean and is calculated as the square root of the variance.

The NASDAQ OMX Renewable Energy Generation index is a primary sector index of the Green Economy Index designed to track companies that produce energy through renewable sources such as solar, wind, geothermal, wave and fuel cells.

The Dow Jones U.S. Oil & Gas Index is designed to measure the stock performance of U.S. companies in the oil and gas sector.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All