Investment Strategy Commentary: Market Pullback

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOur outlook for 2022 was focused on the transitions the economy and markets were facing — including fading fiscal stimulus, reversal of monetary accommodation and a maturation of the COVID pandemic. Our constructive outlook on risk taking was, and remains, based on a constructive outlook for corporate earnings and interest rates.

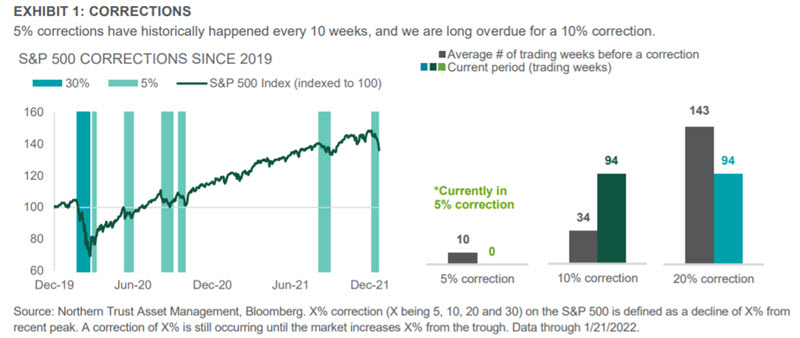

The recent sell-off has put us into another 5% correction — something that has historically happened every 10 weeks (see Exhibit 1). Today markets almost closed in 10% correction territory — something that has historically happened every 34 weeks, and of which we are well overdue (current stretch is 94 weeks). Weakness can be attributed to a combination of concerns about rate hikes, economic growth and corporate earnings. There is also the unquantifiable risk surrounding Russia’s intentions toward Ukraine.

The concern about interest rates seems overblown. Market expectations for the Fed funds rate at the December 2022 meeting have only increased by 25 basis points over the last month and the 10-year Treasury yield is right in the middle of our 1.5%—2.0% forecasted range.1 We think the Fed will manage its balance sheet with a strong aversion to inverting the yield curve. Moreover, some further upward move in long-rates, if driven by the real component versus inflation, is unlikely to spell the end of the bull market or expansion.

We think concerns about economic growth are inflated. Omicron is peaking in key parts of the U.S., so the weakness in high frequency data should start to reverse. Consumers have $2 trillion of excess savings, and corporate inventories are near historic lows — both of which should underpin growth. The start of earnings season has seen some high profile companies warn about their outlooks (banks on costs, pandemic winners on future demand). We don’t yet think these are valid read-throughs to the broad markets, and don’t expect material negative revisions. We think the strong demand outlook should help offset cost pressures from areas like wages.

We assess the outlook for geopolitical risks like the current Russia/Ukraine situation through evaluating the sustaining risks toward global growth and/or inflation. Geopolitical risks tend to not have lasting impacts on asset prices. In fact, over the last twenty years only one geopolitical risk became concrete enough that it became a formal risk case for us. Maybe coincidentally, it was when Russia annexed Crimea and we were concerned about the security of energy supplies and further geographic expansion. As developments quickly settled down, this risk case also quickly disappeared. As there is no way to confidently forecast what will happen among Russia, Ukraine and the West, we will just have to “monitor the situation” (as much as we dislike that phrase). The current risk cases to our positive outlook are: 1) Persistent inflation that justifies a more hawkish Fed; and 2) China growth disruption from their economic policies and zero-tolerance COVID policy.

IMPACT OF RECENT SELL-OFF ON SELECT ASSET CLASSES

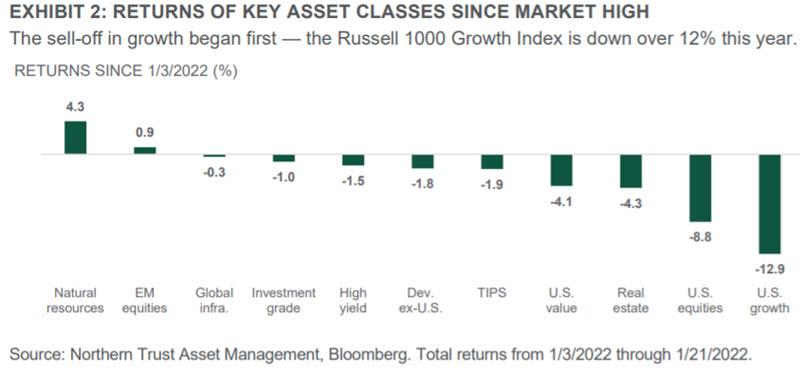

As depicted in Exhibit 2, the recent sell-off has hit growth stocks hardest. While the first stage of this underperformance has been attributed mostly to rising interest rates, the recent weakness is also attributable to some high-profile earnings misses. Financial markets have shown moderate weakness since January 3, likely driven primarily by the increased odds of Fed rate hikes (possibly as early as its March 15-16 meeting) and the resulting impact on the yield curve and corporate profits. U.S. equities were most hit (down 8.8%) — driven by the fact that it is the Fed raising rates (hometown central bank) and the impact higher interest rates can have on “longer duration” equities (the stocks of those companies with higher growth rates such that a larger percentage of aggregate cash flows come in future years). For those companies, higher interest rates mean a higher discount rate for those future cash flows and a bigger resulting impact on the stock’s present value and current price. To wit, U.S. value stocks (“shorter duration” equities) have managed this drawdown better. The Russell 1000 Value Index is down 4.1% in comparison to the Russell 1000 Growth Index being down 12.9%.

Similarly, Developed ex-U.S. Equities — more value-oriented than the U.S. given its sector mix (with a much lower weight in Technology, for example) — has only lost 1.8%. Meanwhile, Emerging Market Equities have actually gained during this period — likely a result of the pain experienced in that asset class for much of 2021, much more attractive valuations and the fact that the catalyst here is mostly the Fed and not further exacerbation of the issues hitting Emerging Market Equities hardest — namely COVID (less vaccine efficacy and more willingness to shut down the economy — notably in China) and broader regulatory concerns (again, mostly focused in China). Other asset classes of note include High Yield, which has provided more downside protection than it normally does (its 1.5% drawdown is 17% of the U.S. equity drawdown, which is lower than the ~35% drawdown historically). Also, noteworthy has been the performance of Natural Resources — an asset class that usually suffers more than broad equities during downturns. This time it has put up some fairly robust positive returns at 4.3%. Interestingly, it has not been unusual for Natural Resources to perform well at the start of a rate hiking campaign — its average 12-month return after the first rate hike of the past 4 cycles has equaled 25%.1

IMPACT OF RATE HIKES ON STOCKS AND BONDS

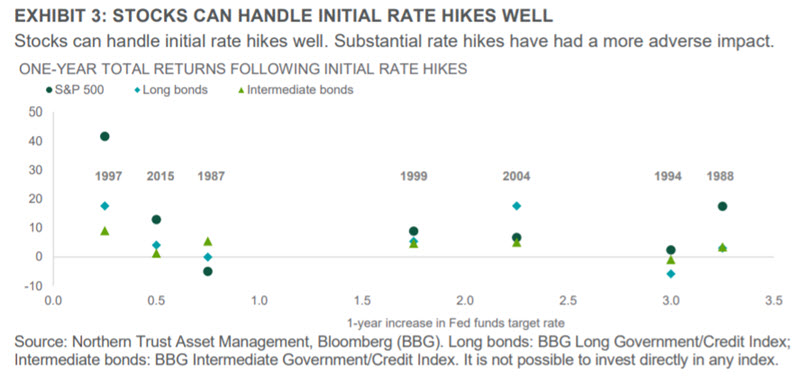

Exhibit 3 shows the returns of select asset classes from the date of the first Fed rate hike. Stocks have generally produced fine results during rate hike cycles. What we need to worry about is a Fed that loses sight of its impact on the equity and bond markets — and charges ahead with rate hikes that invert the yield curve. We think a materially flattening yield curve will temper the Fed’s actions.

UPDATE ON TECHNOLOGY AND CORPORATE EARNINGS

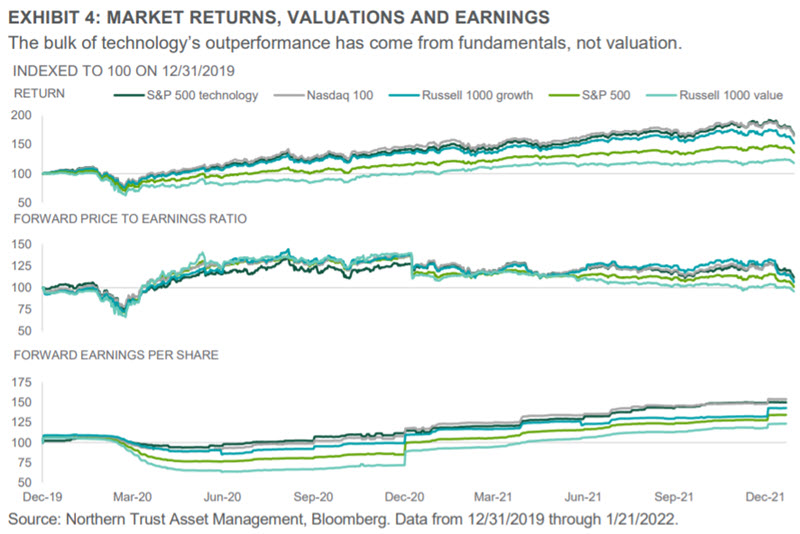

Since pre-pandemic (12/31/2019), the S&P technology sector and the Nasdaq 100 have seen their year-forward earnings estimates improve 50% and 54%, respectively, versus 35% for the S&P 500. Over the same time, the forward P/E ratio of the technology sector has expanded 12% versus 1% for the S&P 500 (see Exhibit 4). So, most of technology’s outperformance has come from fundamentals, not valuation. Moreover, the relative forward P/E ratio between technology and the broader market doesn’t indicate that there is a big tech bubble that needs to continue to deflate in the large cap space.

It is still very early in the fourth quarter 2021 earnings season (~13% of companies have reported), but aggregate sales and earnings are tracking above expectations. However, for a market looking for negatives to justify shifting sentiment, there have been some validating data points. Several banks disappointed with respect to expense guidance, though not a great read-through for margins for the broader market. Pandemic winners have suffered significantly as the market reassesses what a steady state business looks like — for example, Netflix, Peloton and dragged down names such as Amazon. There haven’t been substantive changes to forward estimates more broadly yet, but we do expect more company guidance this earnings season, which should be biased conservatively. We continue to expect the demand backdrop to offer substantial cushion against potential margin pressure, allowing for earnings to remain durable, and would be surprised by materially negative revisions.

CONCLUSION: BENEFITS TO STAYING INVESTED

Don’t ever agree to a debate with Jeremy Grantham. One of the most uncomfortable professional experiences we have ever had was watching him eviscerate Jeremy Siegel of Wharton (Stocks for the Long Run) in a debate. Jeremy Grantham won the debate, but the performance of stocks has probably resembled more closely the long-term expectations of Jeremy Siegel.

For those who didn’t see Jeremy Grantham’s press appearances last week, he is predicting that we are at the end of a superbubble in stocks, bonds, real estate and commodities. He asserts that we are facing the largest markdown of wealth in history (likely in nominal terms, not percentages, but the former makes a better headline). This is based on a return of valuations two-thirds of the way back toward norms.

We don’t debate his conclusion that there has been bubble-type behavior in markets since the pandemic. But we would describe them as occurring more in sub-asset classes than in the broad markets. Areas such as money-losing IPOs, meme stocks, cryptocurrencies (e.g., those created as a joke and gaining billion-dollar-plus market caps) and high growth speculative stocks have all inflated and then had rolling deflations. As noted in the equity commentary above, the broad technology sector doesn’t appear to be in a bubble. For the broad stock market to be in a bubble that will deflate like Jeremy G. predicts, one or two things will likely need to occur: (1) A crash in the economy; or (2) A big jump in interest rates. We don’t see either across the tactical (12-month) or strategic (5-year) horizon. The return of valuations two-thirds of the way back to historical levels must assume a significant jump in interest rates, which we think ignores the global wall of savings that has suppressed rates for years.

We do, however, predict subpar equity returns over the next five years due to slowing growth and some valuation compression. But note that we and others had a similar view five years ago only to witness an 18% annualized return out of U.S. equities. Our analysis is that 14% of this annualized return was tied to pre-pandemic conditions, with the additional 4% attributable to the pandemic monetary and fiscal response. While Jeremy Siegel’s debating skills didn’t carry the day, the benefits of staying fully invested have proven out over time.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.

IMPORTANT INFORMATION. For Asia-Pacific markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Opinions and forecasts discussed are those of the author, do not necessarily reflect the views of Northern Trust and are subject to change without notice.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. Information is subject to change based on market or other conditions.

Past performance is no guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by Northern Trust. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc. Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K, NT Global Advisors Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All