Real Assets Like Gold Are Poised To Benefit From Fed Tightening Cycle

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsJudging by the stormy volatility we’ve seen in financial markets so far in 2022, you’d think the Federal Reserve was getting ready to hike rates. In all seriousness, it now appears that liftoff will happen as soon as March, after which the Fed will reportedly start unwinding its $9 trillion balance sheet.

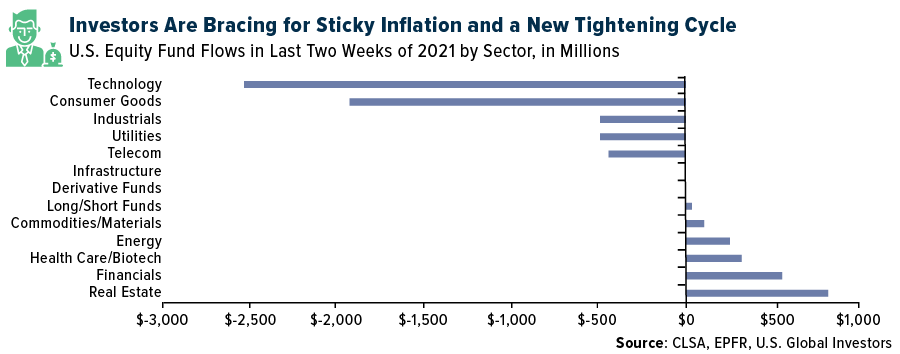

None of this should come as a surprise to most of you. Investors, in fact, have already begun teeing things up for a new tightening cycle as well as sticky inflation. 2021 was a record year for U.S.-listed ETFs, attracting over $900 billion in net flows, and the chart below, courtesy of CLSA, shows where investors were allocating capital in the final two weeks of the year. As expected, technology saw the heaviest outflows, as the sector tends to be highly capital-intensive and has among the most elevated valuations.

It also makes sense for financials to attract some of the biggest inflows in anticipation of higher rates. However, some may initially scratch their heads to find real estate in the number one spot. Don’t higher rates increase borrowing costs and decrease property values?

Although that’s generally true, real estate investment trusts (REITs) have historically done well in periods of not just rising rates but also higher inflation, both of which are typically associated with economic growth. (Sure enough, the U.S. economy grew 5.7% in 2021, its best showing since 1984.)

This, in turn, implies greater occupancy rates. Property owners have also demonstrated strong pricing power and, as we all know, aren’t shy about increasing rents.

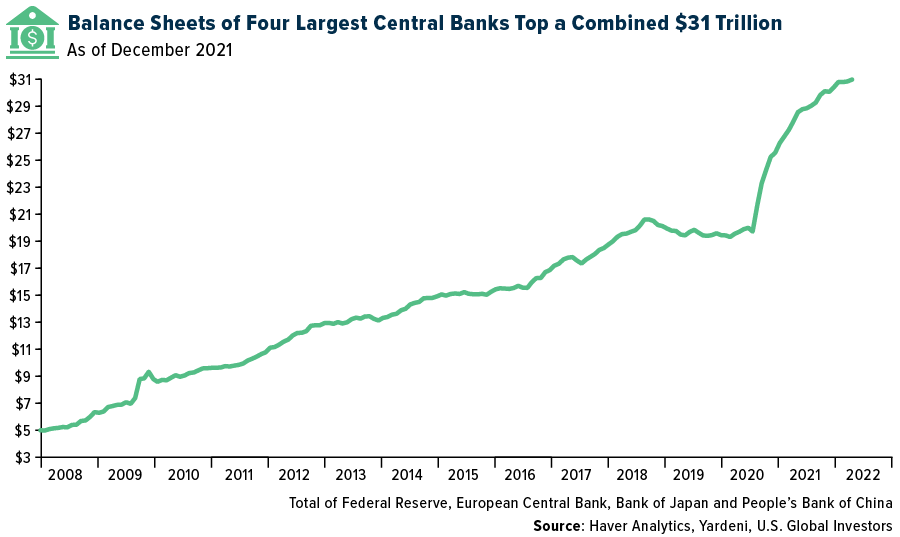

Staring Down $31 Trillion in Central Bank Assets

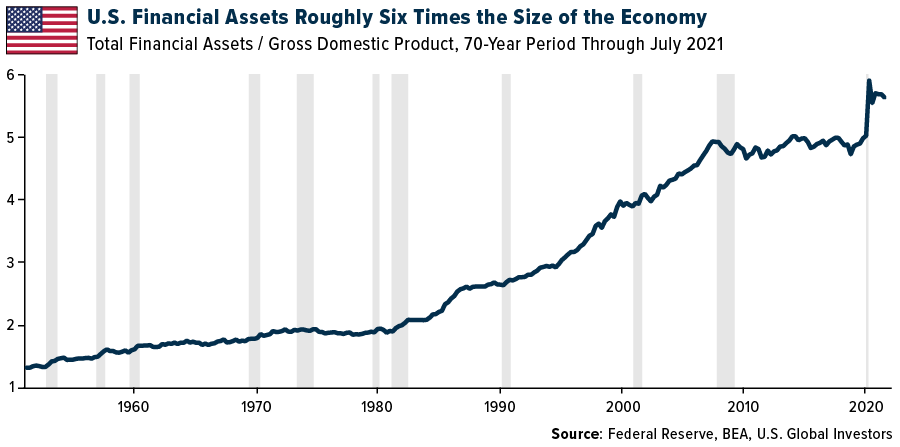

I believe real estate’s key appeal right now is that it’s a real asset, the same as commodities, metals, gold and other materials, which also saw positive flows in the last two weeks of 2021. You may not know this, but the U.S. is shockingly financialized, with financial assets at roughly six times the size of the economy.

The size of the Fed’s balance sheet, as I said, has ballooned to an unheard-of $9 trillion, and if you include the assets of the central banks of the European Union (EU), China and Japan, you’re looking at a combined $31 trillion as of the end of 2021.

Taking all of this into account, I think it’s only prudent to have some exposure to real assets, which have inherent value outside of the traditional financial system. That’s especially the case now on the eve of rate hikes.

Gold Has Performed Well in Times of High Inflation and Rising Rates

In full disclosure, commodities experienced net outflows of $4.2 billion during calendar year 2021. Among the biggest asset-losing ETFs of the year were the bullion-backed SPDR Gold Trust (GLD), which lost $10.8 billion, and the United States Oil Fund LP (USO), which lost $2.8 billion.

But with inflation looking a lot stickier than expected, and with infrastructure projects around the country set to begin thanks to the $1.2 trillion Bipartisan Infrastructure Law, I believe 2022 will bring a reversal of fortune for commodity and metals funds. If it’s any indication, investors last Friday moved $1.63 billion into GLD, marking the ETF’s biggest one-day haul in its approximately 18-year history.

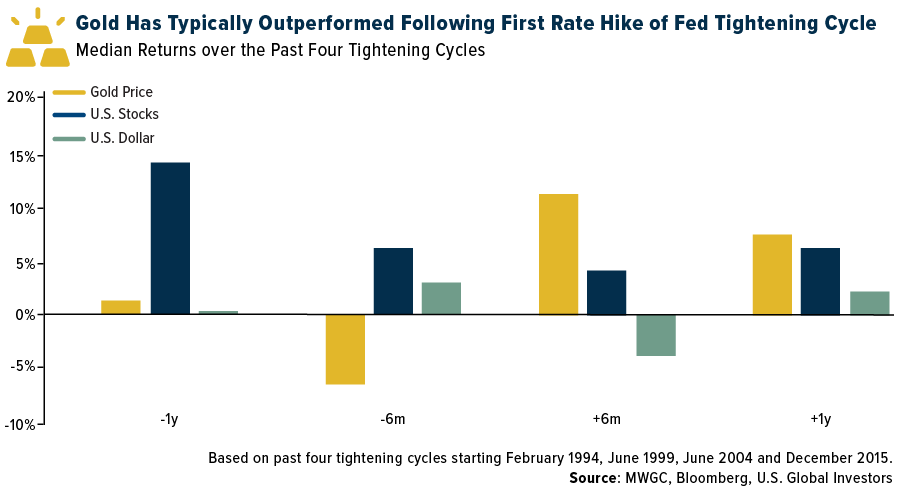

It’s a smart move. Gold has historically performed well in times of not only higher inflation but also rising rates, according to the World Gold Council (WGC). If we look at the past four Fed tightening cycles, between February 1994 and December 2015, the yellow metal underperformed in the months leading up to the Fed’s first rate hike but then outperformed U.S. stocks and the dollar six months and one year following liftoff.

The reason for this? The WGC believes a weaker greenback may have given a boost to gold, for one. And two, U.S. stock returns were not as strong as they were before the rate hike, which may have also favored gold as a safe haven.

This would suggest that the time to buy may be now, potentially less than two months before the Fed says it will take action. As always, I recommend a 10% weighting in gold, with 5% in physical bullion and 5% in high-quality gold mining stocks, mutual funds and ETFs. I also think an allocation of around 2% in Bitcoin, or “digital gold,” also makes sense, especially now with its price still significantly discounted from its all-time high.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 1.34%. The S&P 500 Stock Index rose 0.77%, while the Nasdaq Composite climbed 0.01%. The Russell 2000 small capitalization index fell 0.98% this week.

- The Hang Seng Composite fell 6.37% this week; while Taiwan was down 2.99% and the KOSPI fell 10.55%.

- The 10-year Treasury bond yield rose 1 basis point to 1.78%.

Airline Sector

Strengths

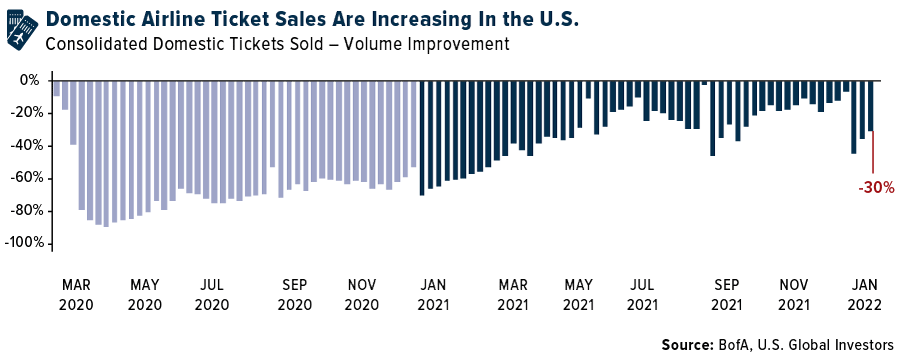

- The best performing airline stock for the week was Grupo Aeromexico, up 11%. System net sales improved to -60.3% versus 2019 levels for the week (and versus last week at -64.4%). Domestic volumes improved to -30.4% versus 2019 (and versus -35.5% last week) while domestic leisure (tickets sold through online travel agency channels) and corporate bookings (tickets sold through large travel agencies) stepped up to -17.7% and -57.5%, from -26.3% and -59.2%, respectively, last week.

- Southwest Airlines reported fourth-quarter results that topped expectations as higher revenue more than offset higher costs which were driven by fuel and profit sharing. JetBlue reported fourth-quarter results that came in above consensus, with the headline figure being a $0.13 beat on earnings versus consensus. Revenues of $1.83 billion came in a touch above consensus on better capacity as unit revenue was in-line.

- European airline bookings rebounded in the week, driven by easing travel restrictions in Europe. Intra-Europe net sales were up by 15 points to -56% versus 2019 levels (and versus -71% in the prior week) while increasing by 52% week-on-week. International net sales grew by 11 points to -63% versus 2019 (and versus -73% in the prior week) and were up by 40% this week. This led to a 12-point improvement in system-wide net sales for flights booked in Europe.

Weaknesses

- The worst performing airline stock for the week was Hawaiian Holdings, down 13.6%. Since Omicron was a large unknown when Hawaiian Holdings provided its initial 2022 outlook, the company has lowered capacity and increased its unit cost guidance given: 1) B-787 deliveries delayed to the first half of 2023 from the second half of 2022, 2) a slower international recovery, and 3) other inflationary cost pressures.

- First-quarter planned growth for U.S. carriers based on current scheduling data is 60 basis points lower versus the last update at down 8% (-3% domestic, -22% international) versus down 14% (-6% domestic, -34% international) in the fourth quarter.

- According to the International Air Transport Association (IATA), on a two-year average basis, December international air travel growth decelerated to 48.8% from 72.9% in November. Domestic U.S. air traffic slowed sequentially and was down -13% versus 2019 levels, a 700 basis points sequential deceleration versus November. Overall, the data shows the early impacts of the Omicron variant on global air traffic with a sequential moderation versus November.

Opportunities

- Lufthansa continues to be linked with investing in ITA (the successor to Alitalia), with Reuters reporting discussions over a 40% stake. There is strong interest in support from ITA, given a range of comments from the company and media reports on the topic of investment and partnership from an industry leading airline such as Lufthansa or even Delta. However, given Alitalia’s loss-making history, as the industry recovers it may make more sense for Lufthansa to develop a strategic partnership with ITA.

- Europe is making meaningful reopening progress with some timelines accelerated this past week, although testing and vaccine requirements for international travelers still broadly remain. The U.K. will end its COVID restrictions on January 27. France is also lifting most of its restrictions for those vaccinated.

- Hawaiian Airlines is seeking to ramp up its limited flight service to Japan in the second quarter, an omicron variant-linked delay from the carrier’s earlier goal of returning to a fuller slate of flights by late March. Japan represents the largest foreign market for Hawaiian, which had about a quarter of its business outside the U.S. before the pandemic struck in early 2020.

Threats

- According to Bank of America, the themes from its year ahead outlook remain the same: 1) unit cost structures are bloated and will pressure 2022 CASM-ex fuel (cost per available seat mile, excluding fuel), 2) consensus estimates still seem high, and 3) demand will continue to be driven by the consumer with corporate travel accelerating as offices re-open in the second half of 2022.

- U.S. airlines’ trailing seven-day website visits decelerated to -3% for the week compared to +7% last week. All the U.S. carriers either declined or were flat compared to last week. One of the weakest booking periods seasonally is exacerbated by cancellations and high COVID case counts, but visitation is likely to pick up in the coming weeks based on positive demand commentary during the start of earnings season.

- European flight activity continued to decline, down by seven points to -35% in the week (versus -28% last week). Ryanair and Wizz Air showed the largest declines at over 20 points each and are now both below 2019 levels. Airlines ex-Wizz have cut their first quarter 2022 schedules by an average of nine points since Omicron started.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 2.0%. The best performing country in Asia this week was the Philippines, gaining 0.30%.

- The Russian ruble was the best relative performing currency in emerging Europe this week, losing 0.40%. The Philippine peso was the best performing currency in Asia this week, gaining 0.20%.

- Taiwan’s GDP expanded the most in 11 years in 2021, a better-than-expected 6.3%. Growth was 4.9% on a year-on-year basis last quarter, up from 3.7% in the prior three months and well ahead of estimates.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 3.7%. The worst performing country in Asia this week was South Korea, losing 5.4%.

- The Polish zloty was the worst performing currency in emerging Europe this week, losing 2.9%. The South Korean won was the worst performing currency in Asia this week, losing 1.4%.

- The Shanghai Shenzhen CSI 300 Index is down more than 20% since its mid-February peak last year. Now Hong Kong and mainland equites are trading in a bear market.

Opportunities

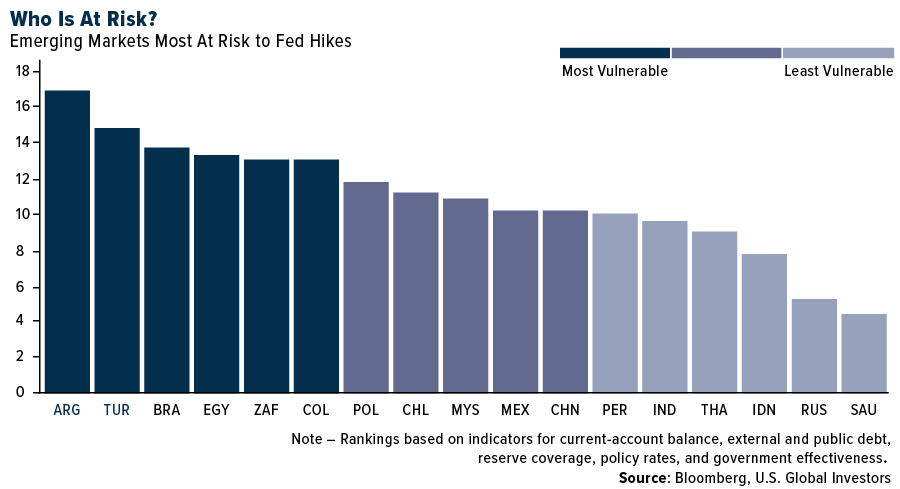

- The two most negatively exposed emerging market countries to rising rates in the United States are Argentina and Turkey. On the other hand, Saudi Arabia and Russia would be less impacted by raising rates due to the countries’ strong balance sheets along with higher commodity prices. Russia currently is negatively affected by geopolitical tensions and Russian equites may continue to drop sharply in case Russia invades Ukraine. However, if current tensions ease, Russia could present a buying opportunity after a healthy correction of 27% since the peak back in October 2021.

- According to a Bloomberg survey, the European Central Bank (ECB) is still more than 18 months away from raising rates. Respondents said that an end to bond-buying in March next year would pave the way for a hike in September 2023. Most said the current inflation of 5% in the euro-area will fall below the ECB’s 2% target next year, easing pressure on officials to act.

- China will likely report weaker Manufacturing and Service PMIs this weekend. Bloomberg economists expect the Manufacturing PMI to drop to 50.0 in January from 50.3 in December. The Service PMI could decline to 51.0 from 52.7.

Threats

- China will be closed next week in celebration of the Lunar New Year. The government expects 36% more trips this year but is recommending people stay home and avoid travel to minimize the spread of COVID. Hong Kong airport traffic dropped to 1.3 million in 2021, the lowest level since 1967.

- Hungary raised its key rate for an eighth consecutive month to 2.9% from 2.4%, a bigger jump than was forecast. It also lifted the ceiling on its interest-rate corridor to 4.9% from 4.4%, making way for more monetary tightening.

- The IMF cut its world economic growth forecast for 2022, citing weaker prospects for the U.S. and China along with persistent inflation. Global GDP will expand 4.4% this year, down from October’s 4.9% estimate, the fund economists said. The 2023 forecast was raised to 3.8%. While the Omicron variant will weigh on growth in the first quarter, fund economists expect the negative impact to fade starting in the second quarter, Bloomberg reports.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was natural gas, up 22.95%, as prices surged on an upcoming storm that will deliver blizzard-like conditions from Virginia to Maine over the weekend. Wind gusts up to 70 miles per hour are forecast along the coastline. Flights across the region have already been cancelled over the upcoming weekend.

- Lithium prices are continuing their break-neck ascent in China, with surging electric-vehicle sales underpinning a five-fold gain over the past year. Chinese lithium carbonate prices tracked by Asian Metal Inc. rose to a fresh record, with data showing a 35% month-on-month jump in electric-vehicle registrations in December. 400,000 EVs were registered during the month, according to the China Automotive Technology and Research Center. Tesla Inc. supplied about 18% of the total. The sales figures offer the latest evidence that the electric-vehicle revolution is now arriving in full force, fueling sharp gains in the shares of carmakers and mining equities alike.

- World steel output rose 7% this month due to higher Chinese output (+20% this month, (a trend already seen in the CISA data) while the rest of the world was -5% this month. Production fell most in Europe ( -15% this month) and Brazil (-18% this month) due to holiday and import pressure along with high inventories in Brazil. Declines elsewhere were modest.

Weaknesses

- The worst performing commodity for the week was lumber, down 10.39%, marking two weeks of double-digit declines. Traders cited weather headwinds on demand and with domestic supplies up. Rising interest rates are also a headwind to the housing market.

- Sibanye-Stillwater cancelled its $1 billion acquisition of the Santa Rita nickel and Serrote copper mines in Brazil, walking away from assets that were key to its expansion into battery metals. The deal was terminated after a “geotechnical event” at Santa Rita, Johannesburg-based Sibanye said in a statement on Monday. That is a setback for Sibanye’s dealmaking Chief Executive Officer Neal Froneman, who is driving the South African platinum and gold miner to join the rush into metals that are key to powering electric vehicles and the wider green revolution.

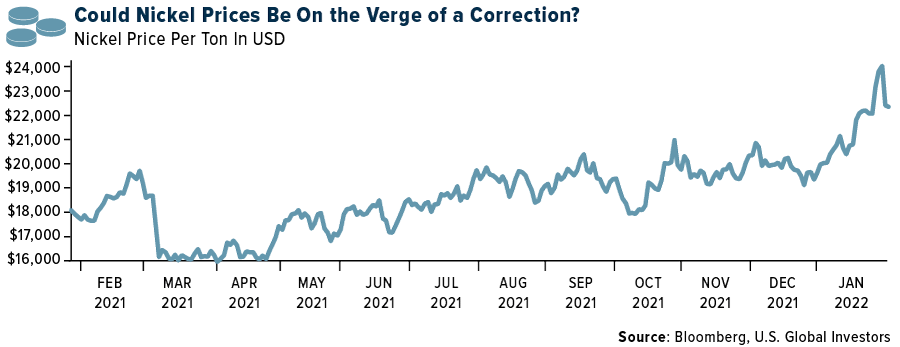

- Nickel dropped from the highest level in more than a decade after a major producer began boosting shipments to meet demand for electric-vehicle batteries, helping to ease concerns over a historic squeeze in the metal. China’s Tsingshan Holdings Group Co., the world’s largest stainless-steel producer, is shipping its first cargo of nickel matte to the country from its operations in Indonesia, researcher Mysteel reported, a move that will help alleviate bottlenecks to meeting battery demand.

Opportunities

- According to Bank of America, two decades of consolidation in industrial gases has created a quasi-duopoly, with Air Liquide and Linde being over 50% of the global market (versus only 30% in 2000). Both have recently digested major deals and are now changing their CEOs, creating an opportune time for a comparison. Bank of America reiterated “buy” ratings on both as they believe growth prospects have structurally improved versus history, due to superior pricing power, significant energy transition opportunities, and self-help margin improvement.

- Oil in London traded near $88 a barrel as increasing geopolitical risks vied with broadly weaker equities markets. Crude’s rally has been buoyed by a combination of robust demand in the face of the Omicron variant, while disrupted supply in countries including Libya has also tightened the market. This is now being compounded by heightened political risk as Russia amasses troops near Ukraine, and the United Arab Emirates comes under attack from Yemen’s Houthi rebels.

- Surging energy prices and a tight rein on spending have driven “Big Oil’s” cash flow to a new high, enticing investors back despite concerns about climate change. The stellar fourth-quarter performance expected from the world’s five super-majors caps an extended period when they had fallen out of favor amid the shift to cleaner forms of energy. Some investors are now rethinking their rejection of the industry as tight markets send fossil fuel prices soaring.

Threats

- China’s Tangshan city announced a new round of steelmaking production cuts starting on Sunday January 23 and with no confirmed end date, due to the possibility of further heavy pollution in the near term. The move dampened sentiment in the iron ore market and prompted prices to ease on Monday, market sources told Fastmarkets. At the same time, overall transactions of iron ore decreased significantly on Monday amid a lack of buying interest after futures fell and because most steel mills have finished restocking their inventories ahead of the Lunar New Year holiday, a trader from Shandong port said.

- According to Morgan Stanley, the Mining Committee of the upper chamber of Chile’s legislature approved an amended version of the country’s mining royalty bill. The amended bill proposes a 1-3% ad valorem tax on copper, depending on the average LME copper price for the year. While the news adds a layer of uncertainty for miners, they see limited impact in terms of copper production even if the law is enacted, as it is unlikely that copper miners will decide to halt operations as a result of the higher tax burden — certainly not with copper closer or above $4 per pound.

- While it is true that Henry Hub gas around $6/Mcf was lofty by the standards of recent years, this is a bargain compared to the situation in the European gas market, where current pricing is closer to $25/Mcf, equating to $150 per barrel oil. The overarching context for Europe’s gas price spike is the volatile state of relations with Russia, including vis-a-vis the Nord Stream 2 pipeline. But Russia should be careful what it wishes for since prices at current levels for an extended time would have serious economic consequences and transform the market landscape for European gas.

Domestic Economy & Equities

Strengths

- The U.S. economy surprised to the upside this week. GDP grew an annualized 6.9% last quarter from 2.3% previously.

- Initial jobless claims declined to 260,000 for the latest week versus consensus for 265,000, and last week’s upwardly revised 290,000.

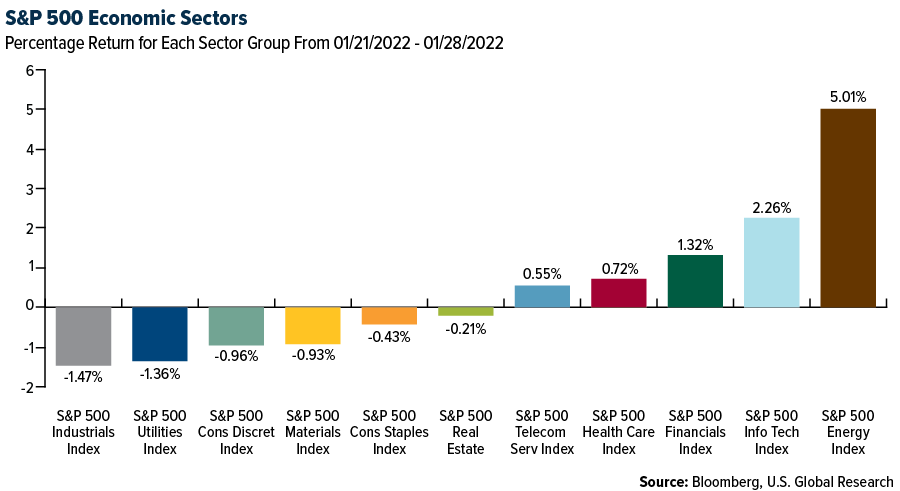

- Corning, a communication equipment producer, was the best performing S&P 500 stock for the week, increasing 19.40%. Shares jumped more than 10% on Wednesday after the company posted strong fourth-quarter earnings.

Weaknesses

- January’s IHS Markit Flash Manufacturing PMI fell 2.7 points month-over-month to 55.0, below the 56.1 consensus, making this the lowest reading in 15 months. Service PMI corrected to 50.9, below the 55.4 consensus.

- December pending home sales declined 3.8% in December, missing the consensus of a 0.3% decline. Higher mortgage rates seem to be pushing some buyers away.

- Teradyne, a semiconductor producer, was the worst performing S&P 500 stock for the week, losing 23.60%. Shares declined more than 20% on Thursday after the company projected a weak outlook for the first quarter.

Opportunities

- Despite the negative sentiment surrounding equities, some strategists and industry articles continue to highlight select bullish talking points. For example, Jefferies noted that the S&P 500 was higher in the 12 months following the start of each of the last seven Fed rate hike cycles. Bloomberg also noted that stocks have risen at an annualized rate of 9% during the 12 tightening cycles since the 1950s, with positive returns in 11 of those instances.

- Next week will be busy in terms of fourth-quarter earnings releases. Big technology names including Amazon, Facebook and Google are due to report. There are also semiconductor names reporting, including Qualcomm and AMD. Starbucks and Clorox are some of the higher-profile consumer companies to release earnings. Automobile names like Ford and GM also report next week, while UPS will be one of the highlights in the industrials sector.

- The job market will likely continue to show improvement next week. Bloomberg economists expect jobless claims and continuous claims to decline further.

Threats

- On Monday, NATO said that member countries are putting forces on standby, sending additional ships and jets to Eastern Europe on growing fears that Russia will enter Ukraine. Great Britain followed the United States’ move to pull diplomats from Ukraine, citing growing threats from Russia. CornerStone Macro Team this week commented that “A full-scale invasion could reset the policy debate in Washington, resulting in more funding for the Pentagon and cyber defenses, even lowering the odds of Biden passing any core elements of his domestic agenda.”

- This week investors were awaiting the FOMC rate division. As expected, rates were left unchanged, but Jerome Powell said the Federal Reserve is ready to raise rates in two months and may start shrinking the central bank’s $8.9 trillion balance sheet sooner and faster than expected. After Powell spoke on Wednesday, the S&P 500 fell almost 1% after being up as much as 2.2% before the decision.

- IMS Manufacturing and Service PMIs are due to be released next week. We will likely see weaker datapoints for both. The Manufacturing PMI will come out on February 1 and Service PMI will follow on February 3.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Crypto Rocket Launch, rising 561%.

- Adam Dell, former head of product at Marcus by Goldman Sachs, is launching Domain Money, a new cryptocurrency platform that will be using social sentiment to help investors, reports Bloomberg. The new platform targets retail users and raised $33 million from investors including Bessemer Ventures and Marc Benioff, the co-founder of Salesforce.com.

- Cathie Wood’s Ark Invest is forecasting ether to soar over 7,000% and hit a $20 trillion market cap by 2030, reports Yahoo! Finance. At that target, ether would be priced around $170,000-$180,000 per coin. The group is also predicting the price of a single Bitcoin could reach $1 million by 2030.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Crazy Miner, down 97%.

- The price of Bitcoin has fallen by more than 50% from its peak in November, and the cryptocurrency market as a whole has lost more than $1 trillion in value over that time frame, writes Bloomberg. For institutions that have bought into Bitcoin, the downturn could prove costly and may create regulatory headaches.

- A hefty debate is underway in the crypto space about whether Bitcoin is mired in a drawn-out bear market or not, writes Bloomberg. Proponents of the token believe a bounce could be around the corner after it shed half of its value from an all-time high in November. However, according to market-intelligence firm Glassnode, a few industry metrics suggest a crypto winter is already here.

Opportunities

- The Diem Association, the Meta Platforms (formerly Facebook)-led group seeking to create a stablecoin, is considering a sale of its assets to return money to investors, according CoinDesk. Diem is reportedly in talks with investment bankers about next steps, including how to sell its intellectual property and find a new home for the engineers who developed the technology, in an effort to capture whatever values is left.

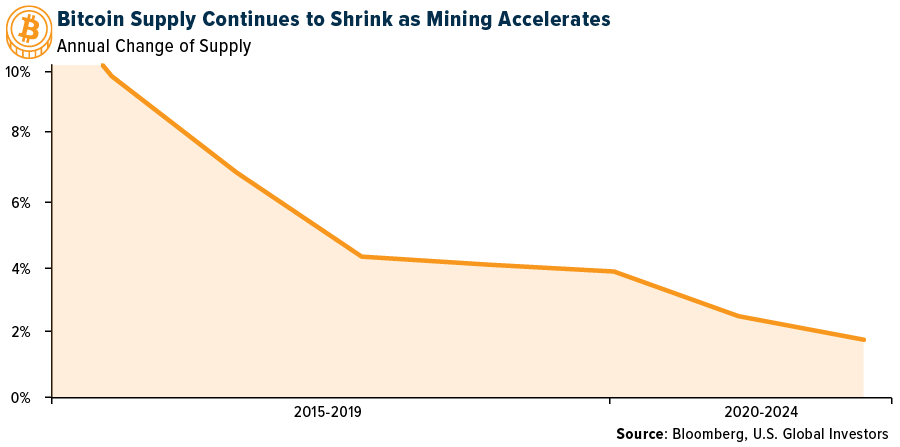

- Bitcoin and Ethereum remain in early adoption days, which means increasing demand versus declining supply. As coded, Bitcoin’s supply is straightforward. Only 900 coins can be mined a day until 2024, then the daily discovery limit halves. The chart below shows Bitcoin dropping to less than 1% of the total by the year 2025.

- Russian President Vladimir Putin has backed a Russian government proposal to tax and regulate the mining of cryptocurrencies, rejecting the central bank’s proposal to ban it completely, according three people familiar with the matter, writes Bloomberg. Putin’s support means mining could continue, as Russia has many regions with a surplus of electricity.

Threats

- The International Monetary Fund is urging El Salvador to end its recognition of Bitcoin as legal tender. Adopting a cryptocurrency in this way “entails large risk for financial and market integrity, financial stability and consumer protections,” the funds executive board wrote.

- IRS criminal investigators see cryptocurrencies and NFTs as ripe for fraud, including money laundering, market manipulation and tax evasion, writes Bloomberg. Digital assets have been a growing concern for government agencies as they’ve become more mainstream, with regulators grappling over how to police the tokens and carry out enforcement activities to deter investors from engaging in criminal activity.

- According to an article posted by Bitcoinist, several YouTube accounts of some of India’s major crypto exchanges and influencers have been compromised. The breech was identified when hackers uploaded videos on the YouTube channel to promote a fake coin named “One World Cryptocurrency.”

Gold Market

This week spot gold closed at $1,791.53, down $43.85 per ounce, or 2.39%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 7.64%. The S&P/TSX Venture Index came in off only 2.14%. The U.S. Trade-Weighted Dollar surged 1.64%.

| Date | Event | Survey | Actual– | Prior |

|---|---|---|---|---|

| Jan-25 | Conf. Board Consumer Confidence | 111.2 | 113.8 | 115.2 |

| Jan-26 | New Home Sales | 760 | 811k | 725k |

| Jan-26 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Jan-27 | Hong Kong Exports YoY | 16.3% | 24.8% | 25.0% |

| Jan-27 | Initial Jobless Claims | 265k | 260k | 290k |

| Jan-27 | Durable Goods Orders | -0.6% | -0.9% | 3.2% |

| Jan-27 | GDP Annualized QoQ | 5.5% | 6.9% | 2.3% |

| Jan-29 | Caixin China PMI Mfg | 50.0 | — | 50.9 |

| Jan-31 | Germany CPI YoY | 4.4% | — | 5.3% |

| Feb-1 | ISM Manufacturing | 57.6 | — | 58.8 |

| Feb-2 | Eurozone CPI Core YoY | 1.9% | — | 2.6% |

| Feb-2 | ADP Employment Change | 220k | — | 807k |

| Feb-3 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Feb-3 | Initial Jobless Claims | 250k | — | 260k |

| Feb-3 | Durable Goods Orders | — | — | -0.9% |

| Feb-4 | Change in Nonfarm Payrolls | 175k | — | 199k |

Strengths

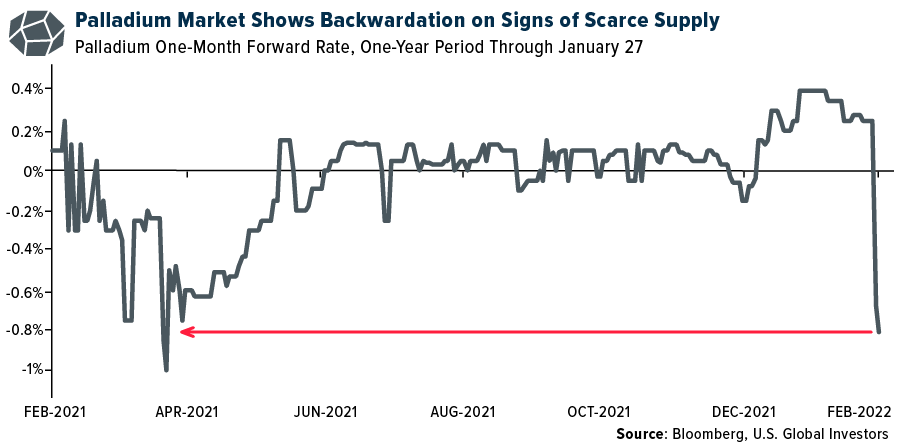

- The best performing precious metal for the week was palladium, up 12.68%. Palladium soared to the highest in four months, writes Bloomberg, with traders looking to secure supplies amid growing tensions over Ukraine as Russia, the top metal producer, amassed troops near the border. The metal that is mostly used in catalytic converters rose as much 8.3% on Wednesday, extending this year’s rally to almost 25%. Looking at the over-the-counter market, Bloomberg notes that the metal has sunk into backwardation, which is a market structure in which spot prices are higher than those for forwards. This signals tightening availability.

- Gold imports by India accelerated to the highest level in a decade last year as jewelry sales almost doubled, with the demand outlook remaining bright, according to the World Gold Council. Demand revived after two bleak years as Indians once again flocked to jewelry stores in 2021 as fears of the pandemic eased. Weddings and celebrations picked up in full swing in the three months through December, more than doubling full-year imports to about 925 tons, the highest since 2011, according to the council data.

- Endeavour Mining provided formal 2022 production guidance of 1,450,000 ounces, ahead of 1,410,000-ounce consensus. Fourth-quarter production was 398,000 ounces, a beat versus the 370,000-ounce consensus. Full-year 2021 production was 1,536,000 ounces, above the top end of guidance (1,495,000 ounces).

Weaknesses

- The worst performing precious metal for the week was silver, down 7.51%, falling at a more volatile factor of three times the price drop of gold. Gold extended losses, after falling the most in two months, as a more hawkish-than-expected U.S. Federal Reserve underscored the central bank’s aggressive approach to tackling inflation. A stronger U.S. dollar on Thursday pressured bullion, which plunged 1.5% Wednesday, as Fed Chair Jerome Powell did not rule out raising interest rates at every meeting to rein in the fastest inflation in a generation.

- West African Resources took a +20% hit to its share price as a new military coup emerged in Burkin Fasso Western Africa. Their Sanbrado Gold Mine is reported to be operating without interruption. Notably, this is the sixth coup in Africa in the past 18 months, of which four were in West Africa.

- Gatos Silver lost more than 70% of its share price this week after the company concluded that there were errors in its technical report from July 2020, as well as “indications that there is an overestimation in the existing resource model.” On a preliminary basis, the company estimates a potential reduction of the metal content of Cerro Los Gatos’s mineral reserve ranging from 30% to 50% of the metal content remaining after depletion, it said in a statement.

Opportunities

- Bank of America is bullish on uranium, aluminum, nickel, silver, and gold for 2022. Cost inflation for the miners in 2022 is real. However, Bank of America finds those with volume growth tend to be shielded from cost inflation, in that per-unit costs are expected to decline despite higher absolute costs, thus protecting margins. Free cash flow (FCF) for the group’s coverage is forecast to rise 69% to $12.3 billion in 2022.

- Despite the negative price action around gold this week, Goldman Sachs Group raised its 12-month price target for the yellow metal on expectations of slower growth, a rebound in emerging markets, and higher inflation. The group’s expectations are now $2,150 an ounce versus $2,000. Contrary to conventional opinion, gold prices tend to go up when the Fed is raising interest rates.

- With much of the retail money allocated to gold stocks held by passive ETFs, capital is not getting allocated efficiently in the gold sector. New cash allocations are just proportionally allocated to the same names. This is creating a field day for the royalty companies to currently be the sole providers of risk capital to structure royalties and or streams with companies that need cash now. Some recent deals even involve placing a royalty and stream on the same asset. If gold continues to move higher over the year with rising rates and passive money moves over to actively managed mutual funds, a significant amount of value could be unlocked.

Threats

- Fresnillo shares fell as much as 15%, the most since November 2020, as the company cut its silver production forecast for the full year. “This negative outlook has been caused by ongoing operational challenges with staff availability as well as new geotechnical constraints at Saucito,” writes Panmure Gordon analyst Kieron Hodgson.

- The end of an easy-money era should normally spell bad news for gold, explains Bloomberg. But right now, fund managers are keeping their holdings. At a time when equities and Bitcoin — often touted as digital gold — are sinking as loose monetary policy draws to a close, bullion exchange-traded fund holdings are proving resilient. Despite expectations for multiple U.S. interest-rate hikes this year, bets for real rates to stay negative and demand for an inflation hedge are supporting the appeal of the time-honored haven, the article continues.

- Illegal artisanal gold mining in the Madre de Dios region of Peru has surged in recent years leaving behind toxic levels of mercury in the Peruvian Amazon. The mercury is used to absorb the gold from the ores. Unfortunately, the gold is then separated from the mercury by evaporating the later away over a fire, spreading the mercury out over the immediate environment. In 2016, the Peruvian government declared a health emergency when 40% of the people tested in the region across 97 villages showed dangerous levels of mercury in their systems.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All