The Crackdown on Canadian Truckers Shines a Spotlight on Bitcoin and Gold

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsHistory has shown us that the more socialist a country is, the more authoritarian it risks becoming. If you’ve been following the events of the Canadian trucker convoy protests against vaccine mandates, and the Trudeau administration’s crackdown on demonstrators’ basic liberties, you know this to be true.

The prime minister has invoked emergency powers that allow him to “commandeer” banks and insurers. Despite the fact that peaceful protest is constitutionally protected in Canada’s Charter of Rights and Freedoms, two key protest organizers were arrested in the capital of Ottawa on Thursday.

GoFundMe fundraisers have been shut down, bank accounts have been frozen without a court order, and for several hours this week, the five largest Canadian banks mysteriously went offline.

That leaves Bitcoin. Although Trudeau can’t prevent someone anywhere in the world from sending Bitcoin to protestors’ wallets, he’s made it more difficult for them to convert the digital assets into Canadian dollars.

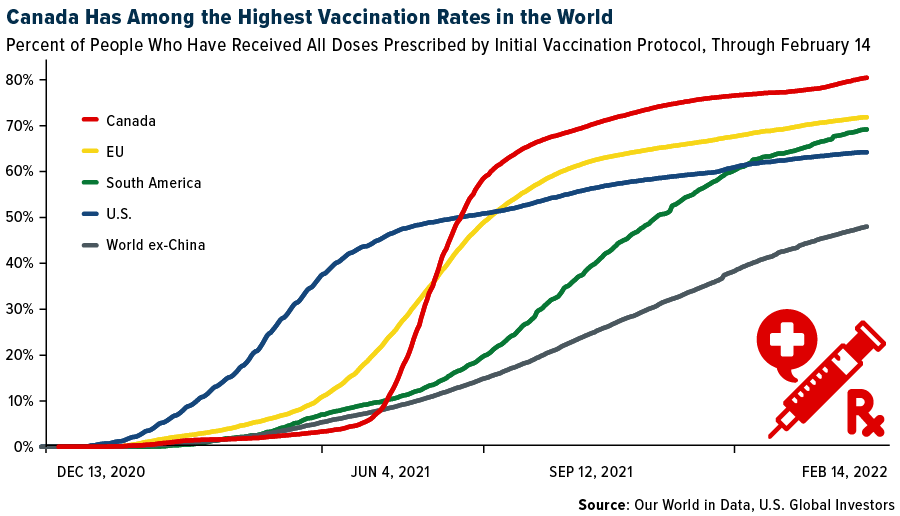

As a native Torontonian, I’m saddened to see that the administration has resorted to treating citizens with real concerns and grievances in ways you’d expect to find in Venezuela, Cuba and other oppressive countries. And for what purpose? Canada already has one of the highest vaccination rates in the world. Like many others, I happen to believe that the vaccines are safe and effective, but in a free country, it should be left to individuals to decide what they put in their bodies.

Justin Trudeau: The Greatest Bitcoin Salesman in Canada

If there’s anything edifying about this, it’s that authoritarianism and capital controls can happen anywhere, even in common law jurisdictions. In the past, people used gold to escape oppressive regimes and sidestep errant governments—consider the daring story of the Vietnamese boat people, many of whom paid their way out of the country with gold after the fall of Saigon—and today we’re witnessing Bitcoin’s use case play out in real time.

Many called (and continue to call) former U.S. president Barack Obama the “greatest gun salesman in America” due to his support of strict gun control measures. Similarly, I believe Justin Trudeau will be remembered as the greatest Bitcoin salesman in Canadian history.

As gold, silver and crypto investor Mark Jeftovic said in a recent blog post, “It’s never been riskier to NOT own Bitcoin.” Unlike fiat currency, the digital asset is decentralized and cannot be controlled by any central bank or politician, making it a powerful peer-to-peer payment network. Why else are some lawmakers and bureaucrats so eager to regulate or outright ban it?

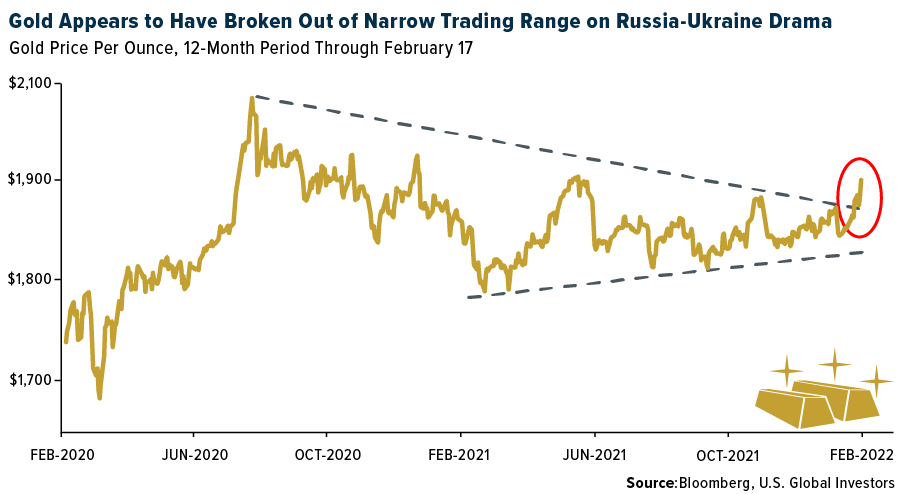

Gold Just Broke Out on Geopolitical Risks and Recession Fears

Speaking of “classic” Bitcoin, gold had a constructive week on Russian-Ukraine tensions, which continue to heat up, and jitters over a possible upcoming recession. The yellow metal broke out of its narrow trading pattern as it climbed above $1,900 an ounce in intraday trading for the first time since June 2021.

Intense fighting is being reported in Eastern Ukraine between Ukrainians and Russia-backed separatists, which some Western analysts fear Putin could use as pretext for a full-blown invasion. As I wrote in this week’s Frank Talk, I still believe an all-out war can be avoided, but should it happen—heaven forbid—you may expect to see the gold price surge and possibly test its all-time high of around $2,070.

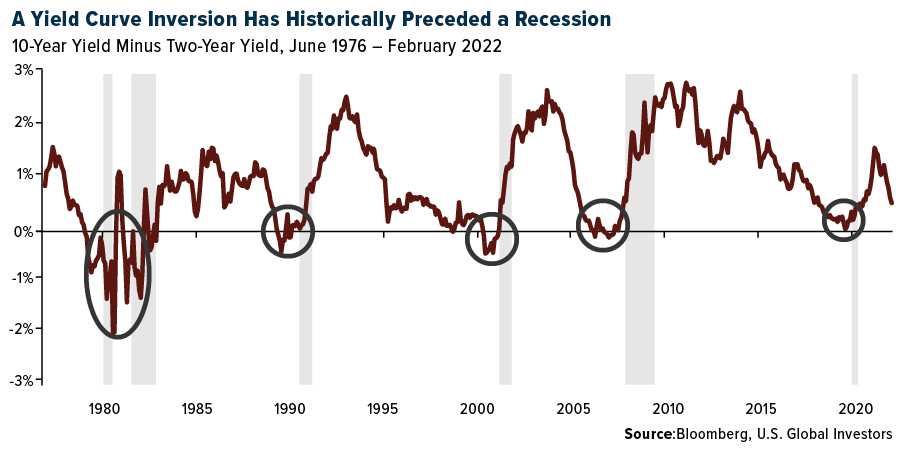

There’s another reason why gold could be rallying right now, and that has to do with what the bond market is telling us. Going back to the 1950s, every time the two-year Treasury yield has exceeded the yield on the 10-year Treasury, a recession wasn’t far behind. The last time such an inversion occurred, briefly, was in August 2019, and we all know what happened the following year. Although there’s no way the pandemic could have been predicted, an economic pullback was highly probable.

In any case, if you look at the chart above, you’ll see that the yield curve may be trying to invert once again. This week the Bank of America, among other financial institutions, sounded the alarm bell, telling clients it expects an inversion to occur sometime this year as the Federal Reserve raises rates to slow inflation and, simultaneously, the U.S. economy. With inflation running at a scorching 7.5% over last year, Fed governors may be compelled to hike rates more aggressively than initially planned, which could potentially shock economic growth.

If you recall in an earlier Frank Talk, I showed you that gold has historically performed well following Fed tightening cycles, so now may be a good time to accumulate. I’ve always recommended a 10% weighting, with 5% in physical gold bullion and the other 5% in high-quality gold mining stocks and ETFs. A position in Bitcoin of around 2% may also be appropriate at this time.

Missed the earnings report for the third fiscal quarter of 2021? Review the press release by clicking here.

Airline Sector

Strengths

- The best performing airline stock for the week was Sabre, up 25.7%. System net sales improved for the fifth straight week to -44.6% versus 2019 (versus last week of -51.1%). While still below the November average of down -35%, net sales are back in line with the December average of -44%, and there should be continued improvement ahead for the spring/summer travel season.

- Domestic leisure volumes (tickets sold through online channels) improved to -8.8% versus 2019 versus -12.6% last week, while consolidated domestic tickets sold improved to -19.0% versus -24.2% last week. From a corporate perspective, bookings through large travel agencies and small travel agencies improved to -45.9% versus 2019 (versus -52.2% last week) and -13.1% versus 2019 (versus -18.3% last week), respectively.

- European airline bookings showed continued improvement in the week, after a big step-up last week. Intra-Europe net sales were up by six points to -52% versus 2019 (versus -58% in the prior week) and increased by 10% this week. International net sales improved by two points to -53% versus 2019 (versus -55% in prior week) and grew by 4% this week. This led to a three-point increase in system-wide net sales for flights booked in Europe to -53% versus 2019 (versus -56% in the prior week).

Weaknesses

- The worst performing airline stock for the week was SAS AB, down 25.5%. According to Bank of America, Air Canada will soon report fourth quarter results. The bank forecasts fourth quarter capacity/revenues of down -48%/-45% versus 2019 with EBITDA of C$(159) million versus consensus at C$60 million. The group expects similar commentary to U.S. network carriers: a delayed demand recovery due to omicron, higher unit costs ex-fuel given inflationary pressures, and a positive bookings recovery as pandemic headwinds fade.

- Travel to and from Asia continues to be impacted by COVID. The Greater China region (Hong Kong and Mainland China) is sticking to a stringent COVID-19 zero tolerance policy, while South Korea and Japan are waiting out the current omicron infection surge. Hong Kong is grappling with its fifth COVID-19 wave, which led to introduction of the city’s strictest social-distancing measures and calls for a switch to “Live with COVID.”

- European carriers took further steps to avoid Ukraine, while airline shares sank after tensions mounted over the weekend over Russia’s troop buildup on the border. KLM stopped flying to Ukraine on Saturday after the Dutch government raised its alert to red after Ryanair Holdings reduced frequencies last month. Shares of Hungary’s Wizz Air Holdings slid as much as 11%, the biggest drop since November, which led to a decline in European airline stocks.

Opportunities

- The budget airline Wizz Air is planning its first transatlantic flights, The Telegraph revealed. The London-listed carrier has made an application to Washington for an “initial foreign air carrier permit.” Wizz said the license was being sought solely to begin a cargo operation between Hungary and the U.S. However, the application will stoke fears among long haul operators such as British Airways and Virgin Atlantic that Wizz is limbering up to launch a price war following the demise of long-haul budget airline Norwegian.

- Morgan Stanley remains bullish on the near- and medium-term outlook for ultra-low-cost carriers (ULCCs), expecting continued capacity growth coupled with continued yield traction and manageable CASM in 2022. The bank continues to like the ULCC’s differentiated and unique business models but expect the focus to shift toward capacity discipline and competition into the second half as the recovery and outcome of the Frontier/Spirit merger comes into clearer focus.

- The Evercore ISI Airline Survey rose each of the past four weeks, moving up from 40.0 to 41.3, as contacts report improvement in bookings for both business and leisure travelers. Domestic leisure demand is back to levels reported before omicron, while business demand is improving, but has been slower to return. After holding steady for four weeks, international activity moved up for a fourth consecutive week, increasing from 30.0 to 32.5, as consumers are getting more comfortable with booking international travel.

Threats

- After Volaris’ stock price declined 15% over the last five months, underperforming the Mexican Stock Exchange Index, which increased 4% in the same period. Aeromexico has emerged stronger but not enough to recapture the market share that Volaris has been able to consolidate. However, it is emerging from bankruptcy as a formidable competitor.

- The Canadian travel recovery has lagged the U.S. in terms of throughput and domestic capacity (Canada fourth quarter capacity was -24% versus 2019 while U.S. was -7%) given a slower vaccine rollout and travel restrictions.

- The largest U.S. airlines have been working with the Biden administration for months on creating a nationwide no-fly list that would ban from commercial carriers the worst of unruly passengers, as attacks on flight attendants, airport gate agents and fellow travelers increase. Seventy-two percent were related to masks, according to the Federal Aviation Administration.

Emerging Markets

Strengths

- The best relative performing country in emerging Europe for the week was Turkey, losing 0.91%. The best performing country in Asia this week was Malaysia, losing 1.5%.

- The Czech koruna was the best performing currency in emerging Europe this week, gaining 0.84%. The Thailand baht was the best performing currency in Asia this week, gaining 1.78%.

- Hungary posted the fastest gross domestic product (GDP) growth in 30 years. The economy grew 7.2% in 2021. Poland reported strong preliminary growth as well, reaching economic expansion of 7.3% last year.

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 4.32%. The worst performing country in Asia this week was Hong Kong, losing 1.60%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 1.17%. The Vietnamese dong was the worst performing currency in Asia this week, losing 0.60%.

- China reported weaker inflation this week. CPI in January fell to 0.90% versus 1.50% recorded in December. Bloomberg economists predicted inflation to increase to 1%.

Opportunities

- Russian equites have lost more than 20% since the peak back in October of last year. Equites have been trying to climb higher since the current low in January of this year, but stocks remain volatile due to ongoing negations between Russia, Ukraine, and the West. Historically, Russia has been trading with the price of oil, and when the Russia/Ukraine tensions end the gap between these two could close.

- China did not cut rates again this week, leaving its one-year, medium-term facility lending rate unchanged at 2.85%, after cutting it 10 basis points at the end of January. More rate cuts will likely follow in March or in early April. The People’s Bank of China (PBOC) is planning to increase support for key areas and weak links in the economy. Inflation in China was reported at 0.90%, below the expected 1%, and December’s reading of 1.5%, paving the way for more cuts.

- In a DayBreak news release, Bloomberg reported that the European Central Bank (ECB) is moving closer to normalizing policy but should do so carefully to avoid derailing the post-pandemic recovery, Pablo Hernandez de Cos said. The ECB is expected to remain more dovish for longer, but inflation will play an important role in determining the bank’s policy.

Threats

- Hong Kong has been reporting more COVID cases. The entire city will have to be tested with the help of the mainland. The Hong Kong Stock Exchange could close if cases continue to surge.

- Poland and Hungary lost a top court challenge regarding a budget dispute. The eurozone won the right to use tough new powers to deny Poland and Hungary billions of euros of European Union (EU) funding due to both countries breaking EU standards. The EU Court of Justice issued a binding decision on Wednesday.

- Turkey’s central bank left its one-week repo rate unchanged at 14.0%, which remains way below inflation. The Turkish lira has been trading in a tight range in the past few months, due to the bank’s continued support. We do expect to see further weakness in the lira.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was natural gas, up 12.21%, on a colder-than-normal weather forecast that will boost demand in the coming week as back-to-back storms will push through the Planes, Midwest and into Texas. In a strategic move, Woodside Petroleum Ltd. plans to link as much as 25% of its natural gas production to spot prices tied to gas hubs around the world. Barrenjoey Markets PTY analysts Dale Koenders and Jock Traveerungroj estimate this change could add an additional $1 billion in annual revenue versus their legacy oil-linked contract prices.

- Lumber futures rose to the highest in a month as some of Canada’s biggest producers reduce output and transportation snags disrupt shipments to customers. March futures rose by the exchange limit of $45 Wednesday to $1,336 per $1,000 board feet in Chicago before paring gains. The surge comes as firms such as Canfor Corp. announce supply cuts in British Columbia, while port congestion and a lack of rail cars and trucks make it harder for Canadian companies to get timber to buyers.

- Lithium is proving to be a stand-out commodity across raw materials. The vital ingredient in rechargeable batteries just racked up a 50% gain since December in China, adding to a powerful 400% surge in 2021, according to one price gauge from Asian Metal Inc. Global buyers are grappling with tight supply of the commodity while demand holds a rapid expansion. Potash is also on the minds of many buyers and sellers, particularly the extent of the disruption to Belaruskali’s 12 million tons of global shipments due to its inability to ship material through the port of Klaipeda in Lithuania. Discussions point to a $575-$600/t range.

Weaknesses

- The worst performing commodity for the week was DCE Iron Ore May 2022 futures, down 19.02%. Iron ore futures in China extended their retreat after Dalian’s commodity exchange raised transaction fees in Beijing’s latest move to check the metal’s rally. The bourse increased the fees for some iron ore futures and said efforts to supervise market orders and halt the spread of false information would be stepped up.

- The province of Alberta will toughen its greenhouse gas emissions standards for oil sands mines, closing a loophole that rewarded some of Canada’s highest-emitting facilities with millions of dollars’ worth of tradeable credits, its environment ministry told Reuters. Alberta is updating industry benchmarks that set emissions reduction requirements per unit of production for mines and upgraders, the ministry said. Canada’s oil sands produce some of the world’s most carbon-intense crude.

- Albermarle, the world’s largest lithium miner, fell the most ever with a 19% one-day decline after its profit forecast left investors stunned in the face of such high lithium prices. Ebitda margins of 89% were expected by analysts but the company guided toward 65%- 85%. Albermarle raised its demand outlook by more than 30% to 1.5 million tons by 2025 and potentially another 3 million tones by 2030. Lithium is a key ingredient in batteries powering electric cars.

Opportunities

- Copper inventories slumped to the lowest in more than 16 years on the London Metal Exchange, with booming demand and supply-chain snarls leaving buyers exposed to shortages of one of the world’s most important industrial commodities. Inventories dropped to 72,225 tons on the bourse, continuing a steady run of declines that is stoking concerns that the copper market could soon be plunged into a major supply squeeze like one that roiled markets last year.

- The U.S. Energy Department announced billions of dollars in new funding to support clean energy technologies as part of the Biden administration’s push to decarbonize the power sector and broader economy. The initiatives were authorized and funded by the Infrastructure Investment and Jobs Act, which President Joe Biden signed in November 2021. Leading the announcements was the Energy Department’s launch of a $6 billion civil nuclear credit program aimed at supporting financially struggling nuclear plants in competitive power markets.

- Citigroup expects LME cash aluminum prices to reach $3,400 a ton within three months on a larger global supply deficit. Cash prices at that level would be the highest since 1988 and compare with a closing high of $3,282.75 earlier this month.

Threats

- A Peruvian community said on social media on Sunday that it will restart a road blockade against MMG’s Las Bambas mine, even as a second community agreed to a 45-day truce in its blockade. Las Bambas, which produces 2% of the world’s copper supply, has said it will have to suspend production on February 20 if the road is not cleared by then. The threat leaves Las Bambas still at risk of suspending operations, even as the road was being cleared on Sunday. Leaders in the Capacmarca district agreed to lift their blockade for 45 days following a meeting with new Prime Minister Anibal Torres.

- Oil’s surge toward $100 a barrel for the first time since 2014 is threatening to deal a double-blow to the world economy by further denting growth prospects and driving up inflation. According to Bloomberg Economics’ Shock model, a climb in crude to $100 by the end of this month from around $70 at the end of 2021 would lift inflation by about half a percentage point in the U.S. and Europe in the second half of the year. More broadly, JPMorgan Chase & Co. warns a run-up to $150 a barrel would almost stall the global expansion and send inflation spiraling to over 7%, more than three times the rate targeted by most monetary policy makers.

- In Chile, a $4.50 per pound tax proposal would increase the effective tax rate for copper mines in Chile by 20%. However, whilst the tax debate in Chile is still a long way from being final, if the tax rate increased to 50-60% it would delay/discourage some projects in Chile, and this is bullish for copper supply and demand and for prices medium-term.

Domestic Economy & Equities

Strengths

- January retail sales were reported notably higher than consensus after December’s pullback. Sales grew by 3.8% month-over-month in January while Bloomberg economists expected an increase of only 2.0%. This was a positive reversal from a disappointing December reading where sales were downwardly revised to -2.5%.

- Continuing claims declined to 1,593,000, (while consensus was calling for 1,617,000) coming in below the 1,619,000 reported the prior week.

- Kraft Heinz Inc., a food producer, was the best performing S&P 500 stock for the week, increasing 10.48%. Kraft Heinz and Google announced a new, multi-year strategic partnership. The company also released strong earnings this week.

Weaknesses

- February’s Philadelphia Fed. Manufacturing Index was reported at 16.0, below consensus for 20.0 and January’s 23.2. New orders and shipment components fell while prices paid and received both increased. The Empire Manufacturing Index was reported lower as well in February, at 3.1 versus the 12.0 expected.

- Weekly initial jobless claims came in at 248,000, above forecasts for 220,000 and the prior week’s upwardly revised 225,000.

- Paramount Global, a media company, was the worst performing S&P 500 stock for the week, losing 20.82%. Shares declined more than 16% on Wednesday despite better-than-expected revenue in the last quarter of 2021. The company’s name was changed from ViacomCBS Inc. to Paramount Global.

Opportunities

- AxiosPro reported this week that COVID cases are declining all across the United States. Nationwide, the U.S. is now averaging roughly 140,000 new cases per day, which is a 64% drop over the past two weeks. New York, New Jersey, and Connecticut are all averaging fewer than 25 new cases per 100,000 people per day. The pace of new infections is declining in every state.

- The jobless rate should continue to improve next week. In addition, Bloomberg economists project the U.S. to record a 7.0% annualized growth. Both datapoints will come out on February 24.

- February Preliminary Manufacturing PMI is due to be released next week. In January, the Markit Manufacturing PMI was reported at 55.5, above the 50 level that separates growth from contraction. Bloomberg economists project the Manufacturing PMI to increase to 56.0 in February, reconfirming resilience in the U.S. market.

Threats

- Financial headlines continue to focus on the Russia-Ukraine conflict. Equites have been volatile, and we anticipate they will remain that way until there is a firm de-escalation. This week, reports emerged that Russia started to pull some military personnel back to its bases after some of the military drills performed with Belarus have been completed. However, mid-week the U.S. had not yet verified any pullback of Russia’s troops.

- January FOMC minutes flagged expectations for a faster tightening cycle than last time around, along with a significant cut to the balance sheet. A Reuters poll revealed just over 75% of economists surveyed expect the Fed to raise rates by 25 basis points next month, with the remaining portion looking for a 50 basis points increase. The Fed is expected to take the funds rate to 1.25-1.50% by December. Economists expect the Fed to start reducing the size of its portfolio by $60 billion a month, with forecasts ranging from $20 to $100 billion.

- January new homes sales and personal income are due to be released next week. Bloomberg economists predict home sales to decline to 805,000 in January from 811,000 in December. Consumer household income is expected to decline by 0.30% in January.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Spook Inu (SINU), rising 1,971.90%.

- Cryptocurrency companies and fintech firms are joining to meet an anti-money laundering rule, reports Bloomberg. Coinbase, Gemini and Robinhood are among the firms helping to build a platform to comply with a U.S. money-laundering rule as they seek to satisfy existing requirements and head off stricter oversight.

- The Justice Department named a veteran cybersecurity prosecutor to lead a new team dedicated to investigating and prosecuting illicit cryptocurrency schemes carried out by cyber criminals and nation states including North Korea and Iran, writes Bloomberg. Eun Young Choi will be the first director of the National Cryptocurrency Enforcement Team which will identify and dismantle the misuse of cryptocurrencies and other digital assets.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was CryptoGuards (CGAR), down 99.82%.

- Investors stuck in the biggest Bitcoin fund, the Grayscale Bitcoin Trust (GBTC), are flooding the U.S. SEC with letters, writes Bloomberg, following a tweet from Grayscale Investments LLC. The tweet encourages investors to share their thoughts on the firm’s application to convert the $26 billion GBTC into an exchange-traded fund (ETF). More than 170 letters have been submitted to the agency so far this month.

- Bitcoin briefly fell below $42,000 this week, testing its 50-day moving average, as renewed fears of a possible Ukraine invasion by Russia weighed on global markets including risk assets. The biggest cryptocurrency on the market dipped as much as 5.4% while Ethereum fell 5.7%.

Opportunities

- Coinbase Global (COIN) is aiming to take a bite out of the $700 billion U.S. remittance market to allow users in Mexico cash out in Bitcoin, Ethereum and Dogecoin. Recipients of cryptocurrencies in Mexico will be able to generate a redemption code on their Coinbase app which can then be used to receive cash at 37,000 retail and convenience stores across the country.

- Berkshire Hathaway’s CEO Warren Buffett initiated a position in the Brazilian-Bitcoin friendly Nu Holdings while dumping shares of Visa and MasterCard in the previous quarter. According to Bloomberg, Berkshire said in a filing made with the SEC on Monday that it purchased $1 billion worth of Nubank shares in the fourth quarter of 2021.

- Bit2Me is the first cryptocurrency platform in the world recognized by the Bank of Spain. The exchange received the “green light” because, as explained by the company itself, it was the first to have conversations and request registration from the Bank of Spain. “Being the first company in the world to achieve this recognition speaks for itself about the security with which our service is developed,” said CEO Leif Ferreira.

Threats

- BlockFi, a company that paid cryptocurrency investors high interest rates for lending out their digital assets, has agreed to pay $100 million in fines to the SEC and 32 states over charges that it violated securities laws and made false statements about the riskiness of its activity, writes Bloomberg. The case marks the federal market regulator’s first against a crypto lending platform, SEC Chair Gary Gensler said in a statement.

- Binance U.S. is allegedly under investigation by the SEC over its relationship with two market makers. A report from the Wall Street Journal says that the SEC believes the company’s CEO, Changpeng Zhao, is affiliated with these trading firms.

- India’s central bank reiterated concerns over cryptocurrency trading, comparing the virtual coins to Ponzi schemes, writes Bloomberg. Seeking a ban on cryptocurrencies, the Reserve Bank of India Deputy Governor Rabi Sankar said the digital coins threaten “financial sovereignty” and “undermine financial integrity” of a country, given that there are no underlying cash flows.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits