With Ukraine Under Siege, We’ve Dramatically Reduced Our Exposure to Russia

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Ukraine’s glory has not yet died, nor her freedom,” begins the beleaguered Eastern European country’s national anthem. It goes on to promise that Ukraine’s “enemies will perish, like dew in the morning sun, and we too shall rule, brothers, in our own land.”

These words are being challenged like never before in the 30+ years since Ukraine gained its independence following the collapse of the Soviet Union. I join millions of others around the world in hoping that the Ukrainian people can continue to “rule their own land” following a resolution to this crisis.

Here at U.S. Global Investors, we believe that government policies are a precursor to change, and President Vladimir Putin’s brazen, unprovoked decision to invade a sovereign nation is no exception.

In response, we have sold nearly all of our Russia-listed stocks, leaving only positions in oil producers Lukoil and Gazprom Neft and a very small position in Raspadskaya, a coal producer. U.S. sanctions have so far targeted Russian banks, not its energy sector.

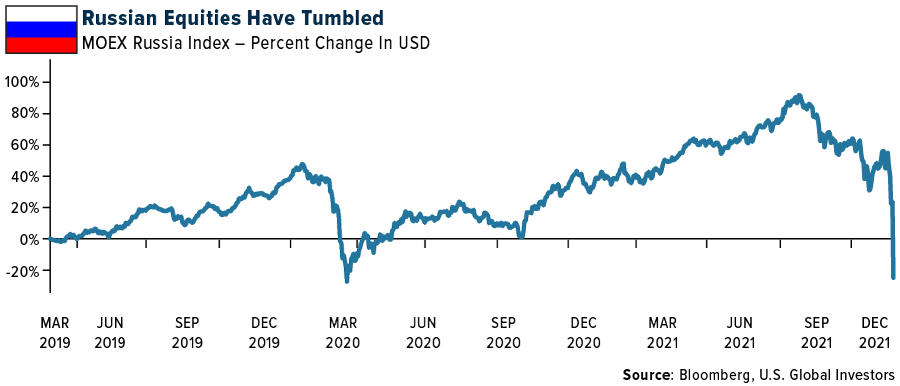

Our withdrawal was well timed, as Russian stocks had their worst one-day selloff on record. The dollar-denominated RTS Index fell around 40% on Thursday.

You may wonder when we’ll feel comfortable enough to dip our toes in the Russian market again. The simplest and most honest answer is that it’s too early to tell. The situation is highly volatile and changing by the hour.

Putin has never been a friend to the West, but this week he has obliterated any doubt that he’s a threat to the rule of law and his neighbors’ right to exist. Therefore, it may be decided that we can’t invest in Russia again until the Kremlin is under new management, one way or another. Which is a shame because we’ve always liked Russian stocks for their cheap valuation and attractive dividends.

Having said that, Putin signed a law last year that effectively resets his term limits to zero, allowing him to potentially remain in office until 2036. A lot can happen in 14 years.

Playing the Long Game… with Gold

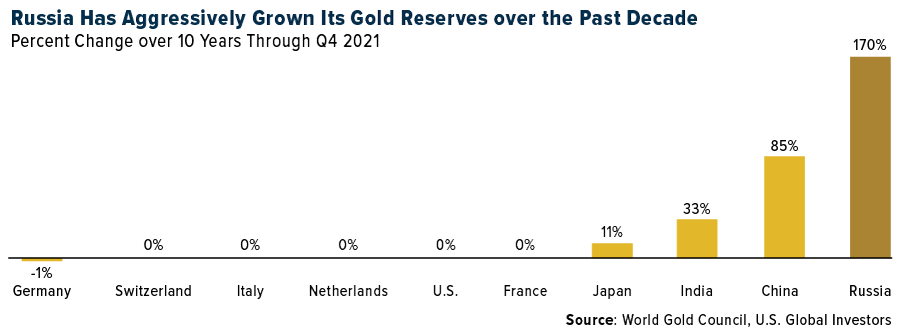

If we look at how Russia has been positioning its central bank reserves over the past decade, it becomes clear that Putin has been planning this invasion for some time.

In 2010, gold represented only 7.4% of Russia’s official reserves. By the end of the 2010s, this share had grown to 23.4%. Over the same period, the country significantly reduced its holdings of U.S. dollars and debt, and in January 2021, it announced that it held more gold than greenbacks for the first time ever.

As you can see below, no other major gold holding country has come close to expanding its reserves as aggressively as Russia has.

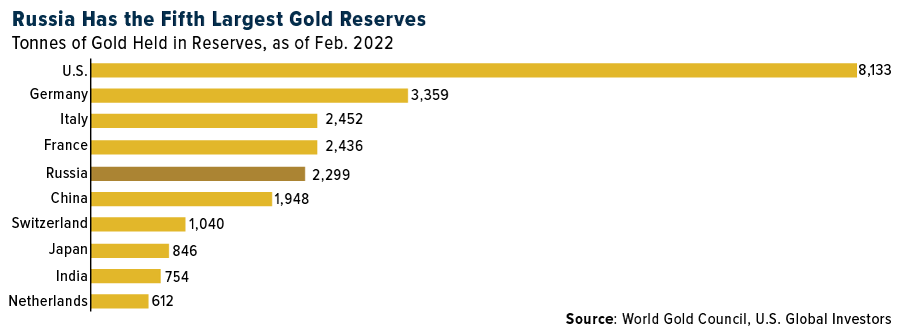

As a result, Russia now has the fifth largest official gold hoard of any central bank, with holdings currently standing at over 2,298 tonnes, according to the World Gold Council (WGC). At today’s prices, that comes out to about $145 billion, or around 10% of Russia’s gross domestic product (GDP).

This should help the country weather the raft of economic sanctions imposed by the U.S. and its allies.

Gold Is No One’s Liability

I’m reminded, in fact, of Germany’s use of gold in its preparations for what eventually became World War II. The country ransacked Europe’s central banks to acquire hundreds of millions of dollars of the yellow metal, which helped finance Hitler’s ambitions. (The U.K. famously managed to keep its gold out of the Nazis’ hands by transporting it to Canada in a daring mission known as Operation Fish.)

Some might think this reflects poorly on gold, but remember, the metal is completely apolitical. It’s no one’s liability. It belongs to everyone.

The same goes for Bitcoin. Half a million dollars in Bitcoin donations have been sent to Ukraine in support of its armed forces. At the same time, Russia is reportedly using cryptocurrencies, which could include Bitcoin, to bypass certain sanctions.

I believe these are compelling reasons to own gold, Bitcoin and other alternative assets.

For more on gold and Bitcoin, watch my interview with Kitco News by clicking here!

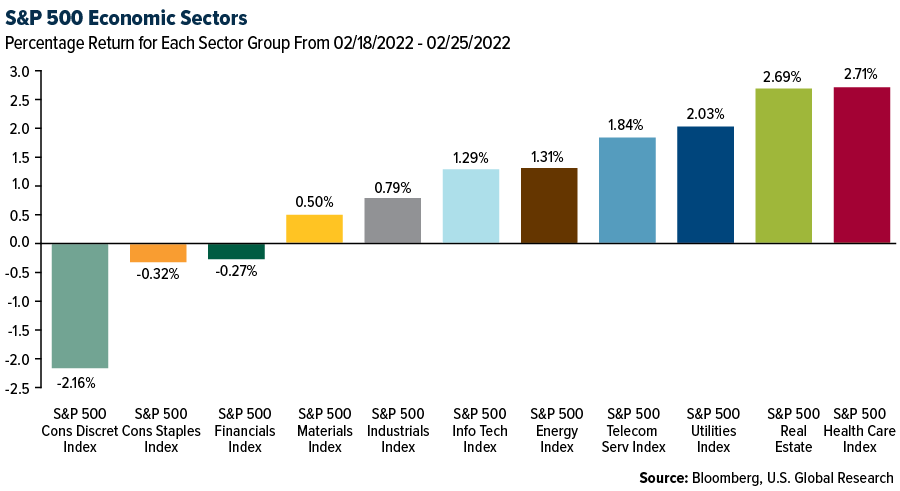

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.06%. The S&P 500 Stock Index gained 0.82%, while the Nasdaq Composite rose 1.08%. The Russell 2000 small capitalization index gained 1.57% this week.

- The Hang Seng Composite lost 6.09% this week; while Taiwan was down 3.11% and the KOSPI fell 10.10%.

- The 10-year Treasury bond yield rose 3 basis points to 1.963%.

Airline Sector

Strengths

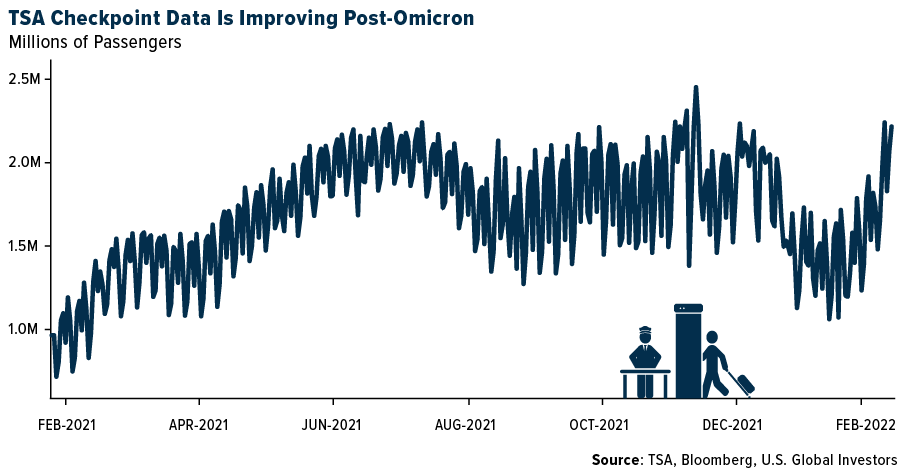

- The best performing airline stock for the week was AeroMexico, up 3%. System net sales improved for the sixth straight week to -38.5% versus 2019 (versus last week of down -44.6%). The improvement since early January is beginning to show up in TSA figures as seen in the chart below, with trailing seven-day figures at -17% versus 2019, compared to -20% last week and -25% in mid-January. Leisure bookings are back to pre-pandemic levels.

- Domestic leisure volumes (tickets sold through online channels) are now at -2.6% versus 2019 and -8.8% last week, while consolidated domestic tickets sold improved to -15.2% versus -19.0% last week. Before omicron, leisure bookings exceeded 2019 levels at peak travel periods, so this data is encouraging, as it shows the continued health of the leisure traveler.

- European airline bookings showed a strong improvement in the week, with growth in both international and intra-Europe net sales. Intra-Europe net sales were up by three points to -49% versus 2019 (versus -52% in the prior week) and increased by 13% this week. International net sales improved by eight points to -45% versus 2019 (and versus -53% in the prior week) and grew by 8% this week.

Weaknesses

- The worst performing airline stock for the week was SAS, down 18.0%. U.S. airline stocks fell on Thursday after Russia’s attack on Ukraine reset expectations on the timeline for a full global recovery in travel, reports Seeking Alpha. This was part of a broad market selloff after Russian military invaded Ukraine through the air, land, and sea.

- Air France KLM announced it will press ahead with equity or quasi-equity issuances of up to 4 billion euros. Air France needs to raise 1.9 billion euros of equity to meet its 2X 2023-estimated net debt to EBITDA target, but it also needs to resolve its 3.8-billion-euro negative equity.

- The German airline Lufthansa said Saturday it was suspending flights into and out of Kyiv from Feb. 21 to Feb. 28 “and will decide on further flights at a later date.” Austrian Airlines, part of the Lufthansa Group, will cancel flights to Kyiv and Odessa through the end of February. Air France suspended its flight rotation scheduled for Tuesday because of the geopolitical situation, according to a statement Monday from the airline.

Opportunities

- According to JPMorgan, Air Canada’s results echoed the firmer demand trends cited by North American peers, but without the ex-fuel cost drama and omicron impact that dominated the U.S. narrative during earnings season. While management prefers to withhold meaningful guidance until its Investor Day next month, the overall tone of its call and fourth quarter top-line resilience suggests a path toward a narrower 2022 loss.

- Bank of America’s “year ahead” themes remain intact, which include: 1) demand hit a trough in early January with sequential improvement each week led by leisure; 2) corporate bookings have been tracking return to office, which the bank believes will continue to accelerate; 3) first half 2022 unit cost guidance was higher than expected given omicron; 4) consensus estimates have been moving lower and 5) the industry has worked with higher rates, outperforming the S&P 500.

- Chase card spending on air travel is accelerating. The week-on-week airline spending growth has averaged 13% since early February. On an indexed basis (back to January 2019), weekly spend has now rebounded to a level not witnessed since early June, a time which pre-dated both global variant waves.

Threats

- Low-cost airline Wizz Air is most impacted by higher oil prices: 1) due to no hedging; and 2) operational impact is hard to gauge, but a closure of Ukrainian and Russian airspace would involve the re-routing of flights especially from Europe to Asia. Wizz could sell off more than other airlines (given its Eastern European exposure).

- Fuel remains a wild card for the airline industry. Fourth quarter earnings season spot prices were $2.53 per gallon, while spot today is $2.59, (but in the interim has averaged $2.66). Airline equities tend to trade more on yield and RASM trends than short-term swings in fuel, even though the latter can materially impact earnings.

- American Airlines further trimmed its international flights as the 787 Dreamliner delays continue. Late last week, the WSJ reported that American is further trimming its summer flying schedule due to the continued delay of Boeing’s 787 Dreamliner aircraft. According to an 8K published last week, the company is planning to temporarily suspend routes between Seattle and London, Los Angeles and Sydney, and Dallas and Santiago, Chile, as well as delay the launch of service between Dallas and Tel Aviv.

Emerging Markets

Strengths

- The best relative performing country in emerging Europe for the week was Romania, losing 2.2%. The best performing country in Asia this week was Indonesia, losing 0.30%.

- The Romanian lieu was the best relative performing currency in emerging Europe this week, losing 0.65%. The Philippine peso was the best performing currency in Asia this week, gaining 0.15%.

- February’s Preliminary Service PMI remains strong in Europe. The index jumped to 55.8 from 51.1 one month ago, while a reading of 52.1 was expected. February Preliminary Manufacturing PMI was reported at 58.4, versus January’s 58.7, and in line with the expected reading of 58.7.

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 27.2%. The worst performing country in Asia this week was Hong Kong, losing 6.9%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 6.5%. The Thailand baht was the worst performing currency in Asia this week, losing 1.1%.

- Russian equites, as measured by the MOEX Russia Index, have lost more than 30% in dollar terms this week. Investors were net sellers after Russia unexpectedly declared the two breakaway territories of Donetsk and Luhansk in the east of Ukraine as independent states and later in the week invaded Ukraine from the South, the North and the East.

Opportunities

- Following Russia’s attack on Ukraine, the MSCI may decide to remove some Russian equites from its indices. In such a scenario, the weight of other members would automatically increase. PKO BP Securities commented that in the case of full exclusion of Russia, they would see around $63 million from ETFs on Polish stocks, $20 million of demand on Hungary, and $12 million on the Czech Republic. The MSCI Emerging Markets Index currently allocated 16% to Poland, and in the case of Russia being excluded from the benchmark, the Polish portfolio will increase up to 46%.

- A recent poll by Reuters shows that China’s property market is expected to stay soft in the first half of the year before rebounding later in 2022. The poll of 17 analysts and economists showed that average prices are expected to fall 1% year-over-year in the first half with full-year prices increasing 2.0%.

- The European Union’s final February Manufacturing PMI will likely show the economy to be resilient. Data will be reported next week on March 3.

Threats

- The worst-case scenario in the Russia-Ukraine conflict unfolded this week. Russia launched a full-scale invasion in Ukraine. Russian equites have sold off sharply in the past five days. More downward pressure may follow depending on new sanctions and restrictions imposed on Russia that will be announced in the coming weeks and/or months.

- Eastern European central banks continue to hike rates to bring inflation lower. Hungary increased its one-week repo rate by 0.50%, from 2.90% to 3.40%. Additional rate hikes may follow.

- Bloomberg economists expect China’s Manufacturing PMI to remain below the 50 level that separates growth from contraction. Manufacturing PMI is expected to decline to 49.8 in February from 50.1 in January. The Caixin Manufacturing PMI is expected to be released at 49.2 versus 49.1 in January. Data will be announced on February 28.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was proxied by the Sprott Physical Uranium Trust, up 13.23%, on the Russian invasion. Energy prices surged after Russian President Vladimir Putin signed an order to send what he called “peace keeping forces” to the two breakaway areas of Ukraine that he officially recognized on Monday. Brent crude oil was closing in on $100 a barrel, and power and coal prices rose as well. Russia’s move is a dramatic escalation in its standoff with the West over Ukraine. Russia exports 7% of the world’s oil supply, half of that going into Europe.

- The European natural gas market is the most at risk from a supply disruption. In January 2022, the U.S. supplied more than half of the LNG into Europe. But from a total natural gas-need perspective, Europe will likely need to rely on diverted cargos, coal, and other sources of fuel to power and heat the region. The U.S. is exporting record amounts of LNG already, but the near-term capacity isn’t there right now to replace Russian supply.

- European lawmakers could take steps to the region’s dependence on Russian natural gas by investing more in renewables, nuclear power, and hydrogen. Economist Holger Schmieding of Berenberg wrote that faster diversification away from Russian gas to renewables will be a long-term impact from the current crises. Shares in solar and wind power stocks tallied double-digit gains on the report after the sector has been in the doldrums for the past year.

Weaknesses

- The worst performing commodity for the week was the Bloomberg Powder River Basin 8800Btu Coal Spot Price Fob/Gillette Wyoming, down 9.41%, likely indicating supply lines may be easing in the mid-west which was hard hit with Covid. Wyoming coal jumped 113% on November 15 but has since shed about 50% of that gain.

- Although no sanctions have been imposed on Russian oil or gas sales to keep markets flowing freely, complications have arisen. Singapore banks would not issue a letter of credit for an oil tanker to take on Russian oil for international shipping. Bloomberg reports that Chinese buyers of Russian crude also say they will sit on the sidelines for now until there is more clarity on cargo financing. International buyers report that Russian crude currently loaded on ships are finding those cargos being offered to buyers at a discount to international prices. Perhaps that is the punishing mechanism whereby Russian oil is only bid for purchase at spot, less a sanction penalty of perhaps 25%.

- The western response to Russia’s latest escalation over Ukraine became clearer as Germany halted the certification process for the Nord Stream 2 pipeline following President Vladimir Putin’s decision to send troops to two self-proclaimed separatist republics. German Chancellor Olaf Scholz, said that “no certification of the pipeline can happen right now.” Without it, he told reporters in Berlin, the gas pipeline from Russia to Germany “cannot go into operation.”

Opportunities

- This week Rio Tinto Group joined the ranks of the big global winners in the commodity markets by delivering its highest-ever profits and announcing another massive dividend for shareholders. Rio Tinto benefited from record iron ore prices. Glencore Plc reported record profits last week setting the global mining industry up for investors to take notice as there is rotation in the market for investments that offer more inflation protection for investors than popular growth stocks.

- With Russia being the world’s largest exporter of nitrogen in 2021, fertilizer markets are worried over any disruption to world supplies that are already tight with production curtailments in Europe, due to high natural gas prices. Investors are bidding up the shares of major nitrogen producers like CF Industries, Mosaic, and Nutrien that are benefiting from the tight markets that may persist.

- Nickel’s three-month price hit $24,925 per ton, while aluminum reached $3,380 per ton, equaling its record high of 2008. “The threat of more sanctions on Russia raises the risk that commodity trade flows will be disrupted between Russia and its trading partners,” Fastmarkets head of base metals and battery research William Adams said on Tuesday.

Threats

- Qatar said it wants to meet European Union requests for additional supplies of liquefied natural gas, but that most of its exports are already tied to long-term contracts. “Qatar is very clear about the sanctity of contracts,” Energy Minister Saad al Kaabi said to reporters at a gas conference in Doha.

- Belarusian Potash Company (BPC), the commercial arm of the Belarusian potash producer Belaruskali, sent a statement to Brazilian customers stating that it will not be able to meet contracts due to sanctions imposed on the nation by Europe and the U.S., according to a Bloomberg article which cited the Brazilian newspaper Valor Economico. BPC has not found alternative routes to railing product to the Lithuanian port of Klaipeda.

- Bloomberg reported this morning that China’s National Development and Reform Commission is setting up a single state backed platform for purchasing iron ore, according to people familiar with the matter. This follows recent interventions by policymakers looking to cool markets following a large spike in prices after recent announcements of stimulus. The iron ore market used to trade on annual contracts until 2010 when spot pricing took over and the negotiations were dropped.

Domestic Economy & Equities

Strengths

- Initial jobless claims declined by 17,000 week-over-week to 231,000, beating estimates for 235,000. Continuing claims also declined to 1,476,000, beating estimates for 1,583,000, which was a fresh pandemic low.

- The second print of fourth-quarter gross domestic product (GDP) was revised up by 0.1%. GDP grew by 7.0% in the fourth quarter on a year-over-year basis versus previously reported growth of 6.9%.

- Etsy Inc., an e-commerce platform, was the best performing S&P 500 stock for the week, increasing 17.00%. Shares soared after the company announced strong quarterly results.

Weaknesses

- January pending home sales were reported down 10.9% from December. Increasing mortgage rates, higher prices, and less inventory are the main reasons behind the slowdown.

- January new home sales were 800,000, just below consensus of 801,000. Meanwhile, the December figures were revised up 28,000 units to 839,000, the best month since March 2021.

- Epam Systems Inc., an information technology company, was the worst performing S&P 500 stock for the week, losing 13.72%. The company announced that it will be negatively impacted by Russia’s invasion of Ukraine. Epam said it has about 14,000 personnel in Russia, including roughly 13,000 delivery workers.

Opportunities

- The U.S. market recorded a bounce in equites on Friday on news that Russia will send a delegation to Minsk to hold high level talks with Ukraine. This week’s market correction may follow a technical move up next week. Nevertheless, investors will be carefully observing developments in eastern Europe.

- The labor market in the U.S. should continue to improve. February’s unemployment rate is expected to decline to 3.9% in February from 4.0% in January. The upcoming unemployment rate will be announced on March 4.

- Preliminary February Manufacturing and Service PMIs were both reported stronger than expected. Manufacturing PMI came in at 57.5 while Bloomberg economists were expecting a reading of 56.0. Service PMI came in at 56.7 versus expected 53.0. U.S. PMIs are pointing to continued resilience and strength of the U.S. economy.

Threats

- Headlines from eastern Europe occupied most news portals this week. Russia invaded Ukraine creating extra volatility in the financial markets. Western countries announced sanctions on Russia targeting companies and individuals. Russia’s military is moving toward the capital of Ukraine, Kiev, and is capable of capturing the whole country within days/week(s). We expect high volatility to remain in the financial markets for now.

- The Unites States has been confronting China and will now be confronting Russia as well. The relationship with Russia has gotten more complicated and will likely remain difficult for years to come.

- Money markets may be roiled by Russia’s $300 billion in foreign currency held offshore if it’s frozen by sanctions or moved suddenly to avoid them, Bloomberg reported. According to Credit Suisse’s Zoltan Pozsar, “If things escalate, it’s hard not to see a direct impact on FX swaps and U.S. dollar Libor fixings.” He estimates about $200 billion is held in FX swaps and another $100 billion in deposits at foreign banks.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was MetaDogecolony, rising 1,375%.

- A group of engineers and traders at crypto prime brokerage SFOX are working on a way to expand access to Bitcoin for banks and big investors through a bespoke derivative, writes Bloomberg. SFOX’s co-founder, George Melika, said his firm is in talks with large banks and market makers including Jane Street to open a market that facilitates the trading of derivatives, the article explains.

- Senator Ted Cruz has taken advantage of the Canadian Freedom Convoy protests to advocate for Bitcoin, writes InsideBitcoins.com. During the Conservative Political Action Conference (CPAC), Cruz said he is bullish on the digital currency due to its decentralized nature making it immune from government control.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was BFK Warzone, down 98.22%.

- Advertisements related to cryptocurrency and NFTs in India must state clearly that such products are unregulated in India and can be highly risky, writes Bloomberg. The words “currency”, “securities”, “custodia”, and “depositories” may not be used in advertisements of cryptocurrencies in India.

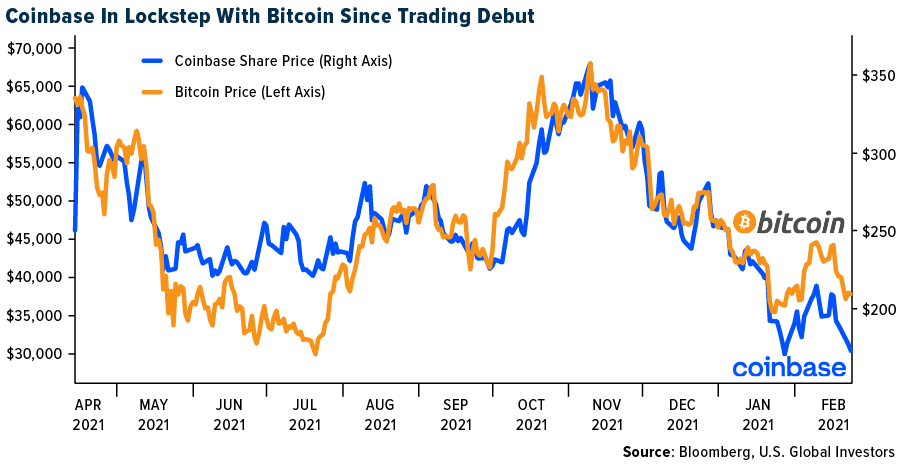

- Coinbase Global shareholders are bracing again for quarterly results that may show the lull in cryptocurrency markets, reports Bloomberg, which continues to dampen the enthusiasm of individual investors. In recent months Coinbase scored an impressive Super Bowl ad, drummed up interest in its upcoming NFT marketplace, and avoided a potential hack of its new trading function.

Opportunities

- FTX has hired Lauren Remington Platt as its head of global luxury partnerships as the company looks toward marketing efforts beyond the sport realm, Bloomberg reports. In her new role, Platt will target major luxury brands that have yet to integrate with cryptocurrencies as a way to focus more on marketing to other consumer segments.

- Yearn Finance, a DeFi protocol providing yield farming, lending aggregation and other services, launched on another blockchain network-Arbitrum. Arbitrum is the largest Ethereum layer 2 blockchain, with about $3 billion on total value locked and has much lower fees, according to CryptoPotato.

- Bitcoin increased 2.5%, back to $39,394, after fluctuating between $37,784 and $39,700 this week. Ethereum increased 3.4%, back to $2,727, after prices fluctuated between $2,546 and $2,747, writes Bloomberg.

Threats

- Cryptocurrencies extended declines as Russia’s attacks on targets across Ukraine sent risk assets reeling, with Bitcoin slumping to a one-month low. The largest token fell as much as 8.5% after Vladimir Putin’s push to demilitarize Ukraine started with a barrage of missile attacks on Thursday, writes Bloomberg.

- Bitcoin is falling while gold is rising as investors seek traditional refuges amid the turmoil in Ukraine, undercutting the often-touted argument from advocates that cryptocurrency is now a digital version of the long-time haven asset, writes Bloomberg.

- Trading volume has also slowed across many cryptocurrency trading platforms during the rout in global assets triggered by the Ukraine crisis, writes Bloomberg. Bitcoin’s aggregated daily spot trading volume on Coinbase, Bitstamp, FTX, Gemini, ItBits, Kraken and LMAX Digital was around $3 billion, according to data from researchers Skew.

Gold Market

This week May 22 gold futures closed at $1,893.20, down $6.00 per ounce, or 0.35%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.47%. The S&P/TSX Venture Index came in off 1.87%. The U.S. Trade-Weighted Dollar rose 0.53%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-22 | Conf. Board Consumer Confidnece | 110.0 | 110.5 | 111.1 |

| Feb-23 | Eurozone CPI YoY | 2.3% | 2.3% | 2.3% |

| Feb-24 | Hong Kong Exports YoY | 18.2% | 18.4% | 24.8% |

| Feb-24 | Initial Jobless Claims | 235k | 232k | 249k |

| Feb-24 | GDP Annualized QoQ | 7.0% | 7.0% | 6.9% |

| Feb-24 | New Home Sales | 803k | 801k | 839k |

| Feb-25 | Durable Goods Orders | 1.0% | 1.6% | 1.2% |

| Feb-28 | Caixin China PMI Mfg | 49.2 | — | 49.1 |

| Mar-1 | Germany CPI YoY | 5.0% | — | 4.9% |

| Mar-1 | ISM Manufacturing | 57.9 | — | 57.6 |

| Mar-2 | Eurozone CPI Core YoY | 2.5% | — | 2.3% |

| Mar-2 | ADP Employment Change | 325k | — | -301k |

| Mar-3 | Initial Jobless Claims | 230k | — | 232k |

| Mar-3 | Durable Goods Orders | — | — | 1.6% |

| Mar-4 | Change In Nonfarm Payrolls | 400k | — | 467k |

Strengths

- The best performing precious metal for the week was palladium June 22 future, up 1.21% which surged on the first day of the Russian invasion. Gold moved to its highest since 2020 after Russian forces attacked targets across Ukraine, triggering the worst security crisis in Europe since World War II and crushing risk sentiment. President Vladimir Putin vowed to “demilitarize” Ukraine and replace its leaders, while the West threatened additional sanctions in response. U.S. President Joe Biden announced he would impose “further consequences” on Russia after what he called an “unprovoked and unjustified attack.” The move sparked a flight to haven assets, with European stocks and U.S. futures dropping while Treasuries rallied. Gold jumped the most in almost two years, even as the dollar strengthened.

- Gold Royalty has entered into an agreement to acquire an existing 0.75% net smelter return royalty on a portion of the Cote Gold Project, located in Ontario, Canada, and owned by IAMGOLD Corp. and Sumitomo Metal Mining, according to a news release. “Together with our royalty on Canadian Malartic’s Odyssey Project, Gold Royalty will own royalties on what is expected to be two of Canada’s largest and longest-life gold mines,” said CEO David Garofalo.

- Lundin Mining reported a strong quarter. Revenue of $1.02 billion was up 9% versus consensus and EBITDA (earnings before interest, taxes, depreciation and amortization) of $623 million was up 14% versus consensus. Net earnings of $282 million was up 8% versus consensus.

Weaknesses

- The worst performing precious metal for the week was platinum April 22 future, down 1.65%, despite hedge funds raising their net long position to a 14-week high on fear of disruptions to Russian supplies. AngloGold Ashanti trimmed jobs and is reviewing its assets after full-year profits declined amid rising costs and the temporary halt of operations at a key African mine. The Johannesburg-based company cut 215 support roles across its global business as part of a cost-savings reorganization. It has also begun a full review of the potential of all its assets.

- Agnico Eagle Mines reported fourth quarter earnings per share (EPS) of $0.46, a miss versus the $0.57 consensus. Fourth quarter cash flow per share (pre-WC) was $1.37, also a miss versus the $1.45 consensus. Agnico Eagle announced that Ammar Al-Joundi has been appointed President and CEO, effective immediately, and that Tony Makuch will step down as CEO and director. Mr. Makuch’s departure is sudden, as he was announced as Agnico’s incoming CEO in September 2021 following the merger with Kirkland Lake.

- Dundee Precious Metals’ fourth quarter earnings were 10% below consensus, driven by higher operating costs, general and administration expense (G&A) and depreciation. The company continues to experience inflation pressures, which are expected to continue into 2022 cost guidance achieved with fiscal year 2021 AISC of $657 per ounce.

Opportunities

- Centerra Gold is acquiring the Goldfield District Project from Waterton. Centerra will pay $175 million in cash at closing plus a $31.5 million milestone payment upon the earlier of 18 months following closing or Centerra making a construction decision with respect to the project.

- “In the globe’s latest maelstrom—U.S./Russia/Ukraine—Bitcoin, the asset purported to be the answer to every question, has quietly weakened and is notably underperforming its arch-enemy, gold,” said John Roque of 22V Research in a note on Monday.

- Sandstorm Gold announced the restructuring of its 30% interest in Hod Maden into a traditional gold stream. This is a transformative event that repositions Sandstorm’s portfolio as a pure-play royalty/streaming company. Sandstorm will retain a $200 million gold stream on the Hod Maden project.

Threats

- Bloomberg reports that as part of streamlining new U.S. regulations to permit domestic mines to meet future critical mineral needs to support the energy transition, an overhaul of the 1872 General Mining Law is envisioned. This body of law has largely remained unchanged and could be counterproductive to the goal of increasing production. A new royalty payment system would be introduced alongside a more certain permitting timeline. There is already a publicly traded market for royalty and streaming companies, so this would be an additional tax of the resource being mined.

- Pan American Silver reported fourth quarter adjusted EPS of $0.19 versus consensus of $0.30. Cash flow from operations came in at $118 million versus consensus of $149 million. Revenues of $422 million were below consensus of $455 million, with the company noting that revenues were impacted by the timing of sales this quarter.

- According to JPMorgan, following CEO Alberto Calderon’s appointment in July 2021, AngloGold’s shares are up 14% but have lagged the Philadelphia Gold and Silver Index at 30% since the start of 2020 due to operational weakness and the strategic overhang triggered by his predecessor’s surprise departure. The bank expected a “reset” by Mr. Calderon for fourth quarter results, and 2022 production guidance was lowered, and costs raised. In the fourth quarter of 2022 the group expects a further cut to previous management’s ambitious longer-term guidance as new management completes their portfolio review.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits