Over the last two centuries, at least 23 ships are recorded as having been sunk by icebergs, while many more have sustained damage. Most of these accidents occurred before the era of sonar, a time in which a sailor in a ship’s crow’s nest (sometimes two sailors, as in the case of the Titanic) would have to peer through the dark and foggy sky to try and spot the tips of icebergs before it was too late. Misidentifying even a small iceberg tip could be fatal, since 90% of an iceberg’s mass lies unseen beneath the ocean’s surface. Yet, if spotted early enough, ships would quite likely be able to navigate around the iceberg and into safer waters.

Over the years, while ships have grown larger, so have icebergs. The largest iceberg in the world, at about 80 times the size of Manhattan, broke off the coast of Antarctica just last year. And investors in 2022, encouraged by ever-more-sensationalist headlines, may be forgiven for thinking that the financial equivalent of Iceberg A-76 may be lurking in the markets today, waiting to sink an unsuspecting portfolio. Indeed, market uncertainty has recently grown more intense, particularly through a series of three developments: 1) an extremely strong January employment report, suggesting that higher wages are attracting people back into the labor force, but at the same time keeping the door wide open for policy tightening. Also, 2) inflation that has hit levels that were inconceivable just a few months ago, and 3) the Russia-Ukraine situation, and accompanying geopolitical tensions. While policy has stayed accommodative thus far, 2022 returns are reflecting these developments, including the potential for policy to aggressively change course. Oil and gold are the only major assets in the green this year, echoing the return pattern of 2018, another year in which real economy inflation was accompanied by financial economy deflation.

Inflation as a Market Iceberg

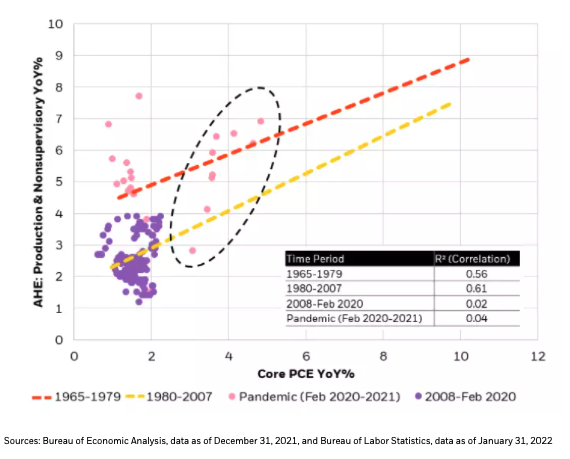

With the Federal Reserve (Fed) focused on inflation, and the market focused on the Fed, certain dangers do concern us. Energy prices continue to make new highs, propelled in part by geopolitics, while other commodities may also be well supported by a loosening of policy in China. This could prolong the raw material, cost-push inflation that has made its way into consumption baskets over the last year. At the same time, higher wages, which are usually a welcome development for an economy, look to be more correlated to broad prices than they have been in decades (see Figure 1), threatening a “wage-price spiral” that could keep inflation hotter for longer.

Figure 1: The correlation between wages and prices is picking up to pre-1980 levels

Yet, there are reasons to believe that calmer waters lie beyond these dangers, taking some pressure off the Fed (though they still need to normalize policy), and therefore, some panic out of the market. While wages and prices may be correlated, evidence suggests that causation in recent times is more driven by price than by wage, giving us some comfort that wages won’t cause prices to spiral out of control. At the same time, a common saying in the commodity markets seems to be ringing true again, namely that ‘the cure for high prices is high prices.’ Consumer confidence around durable goods purchases is at the lowest level in at least a decade, aggregate credit card spending on electronic and home goods is down from a year ago, and retail sales are cooling, allowing stretched inventories to be rebuilt, all in response to…high prices.

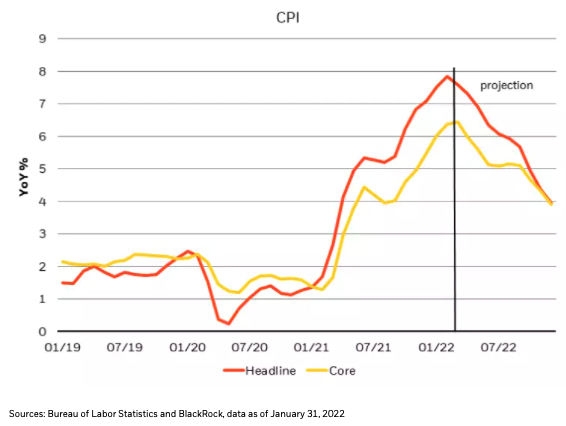

So, while the risk of high prices has not abated, there is also the risk that consumption decelerates too much if monetary policy takes an overly aggressive stance aimed at quelling near-term inflation. We remain optimistic though; that once we are past the shock of 7% to 8% inflation (see Figure 2), data-dependence and sustaining a strong labor market will guide the Fed’s forward path, with a gradual return toward long term equilibrium as our base case.

Figure 2: Calmer prices are likely to lie ahead in the coming months

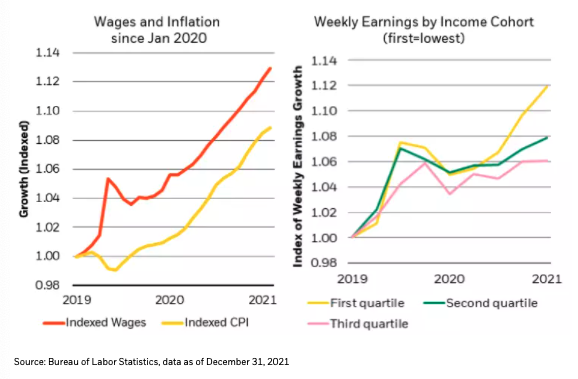

Inflation is certainly an unwelcome tax, but some narratives that seize on today’s extreme inflation readings as proof of “negative real wage growth” may be victims of recency bias. Wages have outpaced inflation quite nicely over the last four years (two of which are Covid-years), to the tune of nearly 2% each year (see Figure 3, left). While January’s data could be cherry-picked to show a 7.5% inflation print outpacing 6.9% wage growth, a longer (and perhaps more statistically significant) lookback reveals that wage growth has outpaced inflation in 41 of the last 50 months, or 82% of the time. We expect that by the middle of the year, the overarching trend of positive real wage growth will retake control – led by none other than the lowest wage jobs, which have been exhibiting the fastest growth of any income bracket (by far) since the onset of the pandemic (see Figure 3, right). In our view, policymakers would do well to embark on a path that preserves and cultivates that trend.

Figure 3: Policy should look to preserve positive real wage growth in the lowest bracket

What is the right set of financial conditions for policy to target?

Long term equilibrium growth tends to be a function of aggregate income, itself broken down into a wage component and the number of people earning that wage. Over the last 50 years, wage growth has averaged 3.5%, just enough to exceed core PCE inflation over that time and create a positive real growth rate for most workers. Over the next 50 years, working age population growth is expected to grow at just less than 0.5%, meaning aggregate income could arguably grow at about 4%. Further, over the last 50 years, the risky corporate borrowing spread has averaged about 2.1%, based on a blend of 80% of the Investment Grade index spread and 20% of the High Yield index spread, a blend that is reflective of the composition of the S&P 500. A 4% equilibrium growth rate and a 2.1% risky spread would imply a 1.9% risk free (Fed Funds) rate, acting as a natural hurdle rate to keep financial conditions (marginal borrowing) in line with the economy.

In the U.S., market pricing is now reflecting a forward path that approaches these levels, after having priced Fed Funds too low for too long. Yet, both the market and policymakers need to recognize that the economy’s most likely path is to decelerate from great to merely good, apart from the notable exceptions of the strong labor market and private sector cash balances, which are still flush from pandemic-induced liquidity injections. Investors need to tactically consider that policymakers may make decisions that are more heavily weighted by near-term (and possibly even coincident) conditions rather than expected long-term outcomes. More risk premium could quickly be injected into markets if a clear plan for a return to neutral is not laid out.

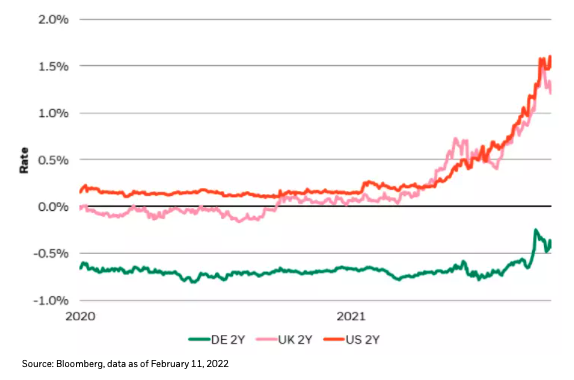

At the same time, investors need to recognize that there is a difference between “getting to neutral” and “tightening beyond neutral.” In Europe, for example, we have long since argued that Negative Interest Rate Policy (NIRP) had overstayed its welcome and risked more harm than good by destroying demand for capital and the banking system. A year ago, ECB policy rates were negative out to 2030, but now the market is expecting an end to this era (thankfully) by the end of 2022. It is more the speed of this repricing that has shocked market participants than the level of yields – indeed, it is not out of line with economic reality for European rates to be somewhat closer to zero, or slightly above; and with the ECB still so far from neutral, it is hard to see them making a hawkish mistake (see Figure 4).

Figure 4: The ECB Is a lot further from neutral than the Fed

The market has already done a lot of heavy lifting to tighten financial conditions ahead of any policy actions. Nonetheless, financial conditions are still on the easier side of the last decade’s range. There is still room for 10-Year U.S. Treasuries to back up between 25 to 50 basis points (bps), especially if there is some easing of geopolitical tensions. That would go a long way toward normalizing financial conditions, such that the Fed would not need to, as some prognosticators argue, “push stocks considerably lower” from here to achieve the same effect.

How should investors allocate their portfolios to navigate such uncertain waters?

When assessing what the “right” risk premium should be for risk assets amidst so much uncertainty around economic growth, inflation, policy and geopolitics, it doesn’t help that market liquidity is the poorest it’s ever been. It doesn’t take many sellers in today’s markets to push prices one way or the other in dramatic fashion – often beyond what fundamental changes might have suggested, based on historical precedent in more liquid times. Nonetheless, flows into global equities remain elevated and corporate buybacks are quite generous in this strong-growth, high-cash flow environment, such that some confidence can be maintained in the long-term demand for equities.

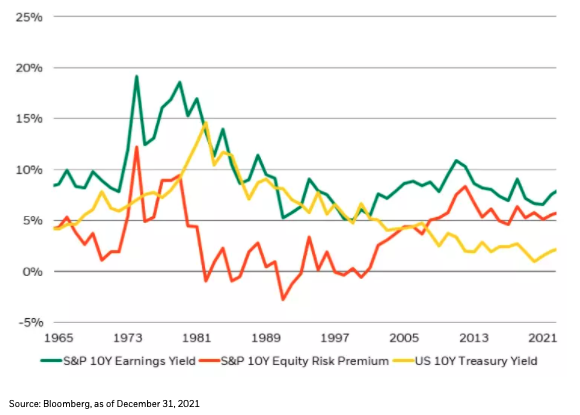

Fundamentally, earnings grew by more than 30% last year, explaining the 29% total return in the S&P 500 in 2021. While we expect moderation on this front, sticky inflation shouldn’t be a fear for equity earnings and valuations, given companies’ ability to exploit pricing power and operating leverage. In past inflationary regimes (which were far more dramatic than today’s) the 10-year equity risk premium was essentially zero – today it is a comfortable 5% (see Figure 5).

Figure 5: In the past, the 10-year equity risk premium has traded below the 10-Year UST

Strong nominal growth creates a favorable environment for continued earnings growth. Indeed, companies reported record earnings in the recent earnings season. These cash flows are being plowed back into investment, especially in the areas of research and development (R&D) in cloud computing and software, which ends up benefiting tech companies that sell such services. While higher rates can eat into valuation multiples in a vacuum, we are not in a vacuum today – the earnings growth of the largest tech companies helps place a floor under valuations, when book value is accreting at a 15% to 20% annual clip. This compounding of earnings growth is often underestimated by the market. A stock that declines 10%, but delivers 15% earnings growth for just two consecutive years, will inevitably end up with a price/earnings valuation ratio that has collapsed by a third. That puts a powerful valuation floor under companies that can exhibit such strong, sustainable, growth. On the flipside, there are many companies that do not have such prospects and can bear the full brunt of a valuation repricing on the back of higher-than-expected discount rates (it goes without saying that such investments should be avoided).

While we think equities work over the intermediate term, for all the reasons mentioned, we aren’t in calm waters yet. We believe in holding a good deal of cash for now, which at a return of 0% and a volatility of 0%, has outperformed most major assets this year (to read more about how we think about cash as a portfolio tool, read The Queen’s Gambit Declined). Still, as the market reprices to account for tighter policy, investment opportunities should open up. In the fixed income universe, and particularly in higher quality short-term assets, there are now areas that look a whole lot more attractive these days as a portfolio complement.

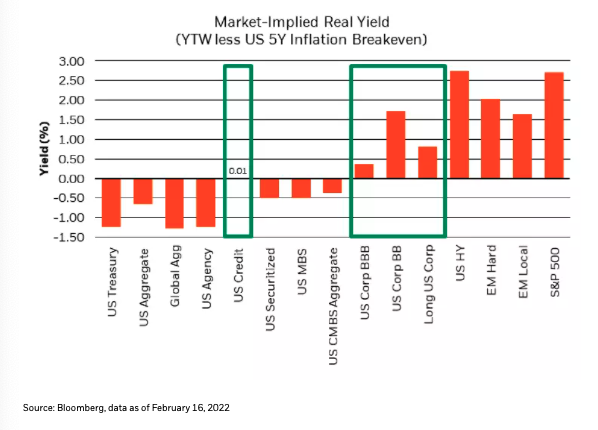

For many months we have observed the lack of positive real-yielding assets. But now pockets of fixed income are opening up to investors who want to lock in positive real yields – especially in crossover credit. For instance, 1-to-5-year Investment Grade (IG) bonds have captured about 70% of the back up in lower quality High Yield (HY), making this part of the IG curve interesting again (see Figure 6). Additionally, after an incredible re-pricing, front-end sovereign and higher-quality credit assets are also offering very unique carry profiles, especially relative to their volatility, with some tangible portfolio benefits given these high-quality assets’ record of performing well during adverse market shocks. Last, but not least, European credit spreads for most issuers are trading at the widest discount to U.S. spreads in at least a decade, so even European fixed income is investable again!

Figure 6: Pockets of fixed income are popping into positive real yield territory

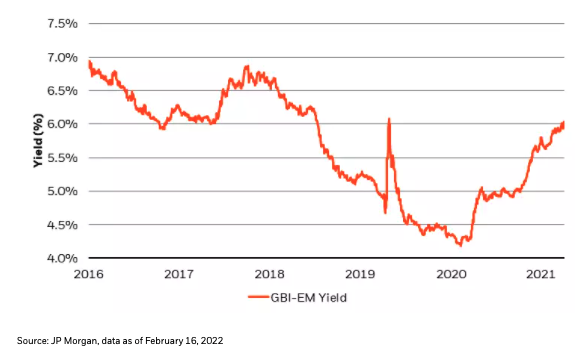

If yields in developed markets continue to rise, yields in emerging markets (EM) may rise even more. Indeed, local yields have already risen almost 2% from their post-pandemic tights but have not yet quite reached the wider levels of 2018. It may be worth being patient in EM, and being discerning when it comes to country selection, since an index yield of 6% may look attractive, but it masks some large differences between countries (see Figure 7).

Figure 7: EM yields have cheapened up a lot, but are not yet at historically wide levels

During periods of high dispersion and high volatility, amidst an environment fraught with uncertainty, we like to consider the variability of possible returns across major asset classes when constructing portfolios. Risk-free rates have a wider and more symmetric potential return distribution than markets are used to, with an uncertain correlation to risky assets. This makes risky assets, themselves, from credit to equities, likely to be more volatile with almost as much downside as upside, but we still think there is a bias toward modest positive returns, given the damage that has already been inflicted on financial assets thus far this year. As assets cheapen up, usually in dramatic fashion, given the dearth of market liquidity, we are ready to deliberately deploy some of the cash that we’ve stored over the last year, but we are not in a rush to do so. We think the next two months will provide a lot more clarity on the economy and on policy, which will help us navigate through whatever market icebergs the surrounding waters may contain, and hopefully toward safer waters beyond.

Investing involves risks, including possible loss of principal. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of February 28, 2022 and may change as subsequent conditions vary. The information and opinions contained in this commentary are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents. This commentary may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Prepared by BlackRock Investments, LLC, member FINRA.

©2022 BlackRock, Inc. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

USRRMH0322U/S-2052039-1/9

© BlackRock

Read more commentaries by BlackRock