"Data is the new oil" has been a modern-day catchphrase, implying that oil was losing its status as the world’s most valuable resource. It seemed an apt metaphor, until Russia’s invasion of Ukraine showed the world’s sensitivity to oil shocks. But as we wrote here, oil isn’t the only commodity that is proving its worth.

The conflict has not only plunged the European continent into its worst crisis since World War II, but the economic implications are cascading across the globe. After a turbulent start to the year due to the Omicron wave, emerging markets (EMs) are now finding themselves in the midst of another storm.

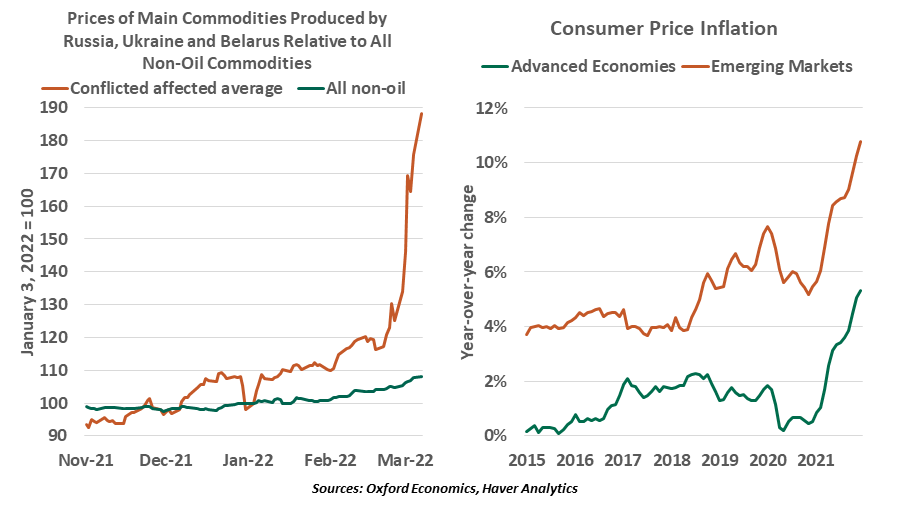

The war and retaliatory sanctions are delivering a major shock to commodity markets. The average price of nine commodities produced by Russia, Ukraine, and Belarus have almost doubled since the start of the year. These developments will have direct and knock-on effects on the emerging world.

Eastern European states, particularly the Baltics, have sizeable trade linkages with the combatants and are highly dependent on Russian gas. Should Russia decide to hold gas exports back, these countries would have limited options apart from power rationing. Energy-intensive sectors like chemicals, metals and refining will bear the brunt of such policies. Apart from energy, Moscow and Kyiv are also important sources of agricultural, iron ore and palladium supplies for the region.

In Eastern Europe, Poland appears to be most vulnerable as energy-intensive sectors account for almost one-third of manufacturing gross value added. Elsewhere in Europe, Turkey has significant dependency on Russia as an export destination for construction services, agricultural goods and revenues from tourism. All of these avenues have been narrowed or closed.

Since the debt crises of the 1990s that had swept from Asia to Latin America, some emerging countries created financial cushions to buffer external shocks. But the pandemic drained those resources, leaving many vulnerable.

High inflation has been a worry for advanced economies, but is a bigger concern for emerging markets. Energy and food items account for a higher share of consumer baskets in EMs than in developed economies. Higher international prices will significantly increase imported inflation.

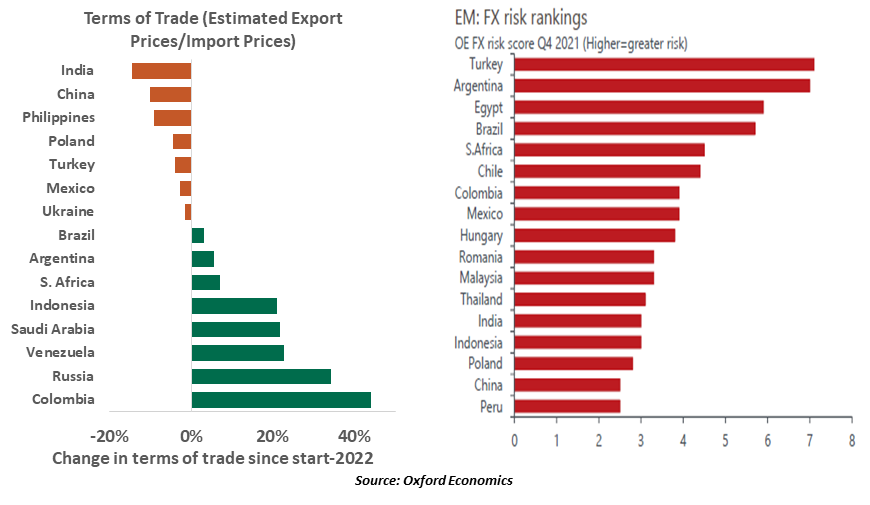

Countries like India, China and the Philippines have witnessed the biggest decline to their terms of trade since the start of the year, owing to their heavy reliance on imports of crude oil and gas. Beijing is already struggling to contain industrial inflation. Another bout of price spikes is only going to add to China’s manufacturing woes, even as it continues to work towards healing supply chains.

India imports nearly 80% of its fuel needs. Hence, despite adequate foreign exchange reserves and improved external balances, the Indian rupee has been among the worst performing major EM currencies in recent days. Even Latin American countries like Brazil and Mexico, which are major exporters, will struggle from shortages of fertilizers and metals imported from Russia.

Emerging economies, generally, lack policy credibility. Price increases coupled with weaker currencies are likely to prompt more aggressive action from EM central banks, which have already prioritized the inflation threat over risks to growth in the past year. This particularly holds true for Latin America, where inflation has emerged as a potent threat and is pushing key regional economies like Brazil into stagflation.

|

Price shocks produced by the conflict have hindered some countries and helped others.

|

High inflation has often been a trigger for protests in many EMs. Nations spend over $300 billion a year on subsidies to stave off unrest and keep essentials affordable. The near-doubling of oil prices in just a few months and rising food costs will further weaken fiscal positions in economies where subsidies are widespread.

The second-order effects of the struggle for Ukraine on emerging markets include risk aversion on the part of investors. The conflict is sparking a sell-off across several emerging markets. Credit spreads have widened in economies that are exposed to higher oil prices, have weak external balances and are geopolitically at risk. Aggressive interest rate hikes could derail growth and lead to further ratings downgrades and capital flight. This would raise the cost of external financing.

And with the forthcoming Fed tightening and a stronger dollar, riskier EMs could face challenges of debt sustainability. Turkey is particularly vulnerable on this front, owing to its weak external position. The country’s external financing requirements are far bigger than its central bank’s foreign reserves, meaning the Turkish lira could continue to slide, aggravating inflation problems.

|

Turkey will suffer a range of consequences in the wake of the crisis.

|

There will be humanitarian implications. COVID-19 has already pushed millions into extreme poverty around the world. Higher costs of living, including surging food prices, are going to push millions closer to starvation. In addition, many European countries will be welcoming refugees from Ukraine, and the cost of getting them re-settled will be significant. Members of the euro area are already discussing a second common bond issue to fund relief efforts.

That said, it’s not entirely gloomy for all EMs. Commodity exporters stand to benefit from higher international prices, which should help partly offset the imported price shocks. In fact, the majority of emerging economies have witnessed an improvement in terms of trade this year.

The long-term impact of the ongoing conflict on EMs is as uncertain as the war. But the damage that will be done to some countries may be difficult to recover from. Oil and other commodities remain the most expensive resource for the developing world, but the data needed to assess and react to the current situation will become a very hot commodity. We’ll be following it closely.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust