Diversification is a hedge against uncertainty

To start, let’s discuss what diversification is and what it is not. Diversification is a hedge against uncertainty. If one knew with 100% certainty what the best performing investment would be, any rational investor would simply put all their money into that one single investment because owning anything else would detract from performance. The less certainty you have, the more diversification you should seek.

Diversification is a function of concentration and correlations

Diversification is less about increasing portfolio returns, and more about creating a smoother ride. For example, let’s say you have two investments that will generate the same return but with very different performance trends. In this scenario, you will end up with the same returns whether you own one investment, the other investment or both. But the day-to-day volatility of those returns should be dampened when you own them together vs. owning them separately. Just how much the volatility is dampened will depend on (1) the concentration of the portfolio in each investment and (2) the correlation between the investments.

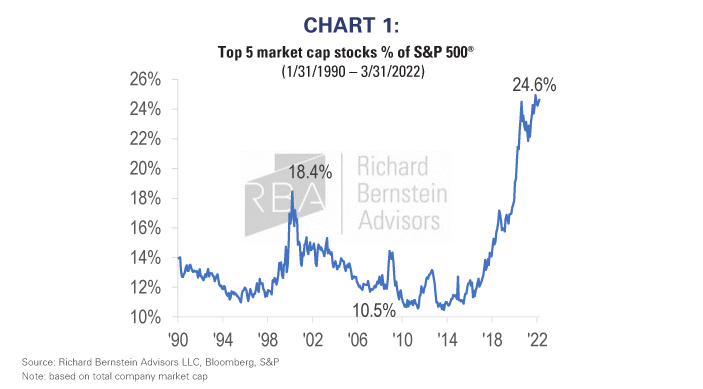

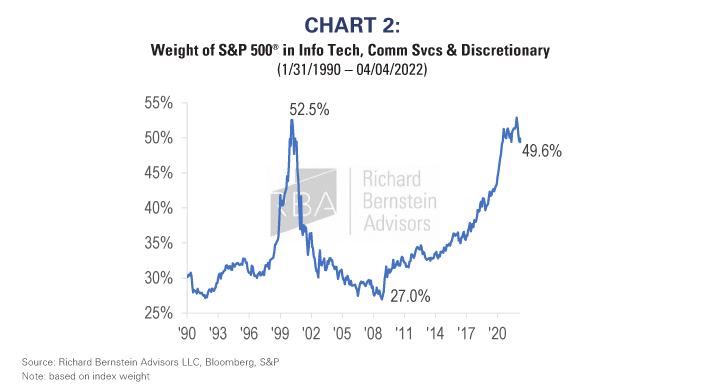

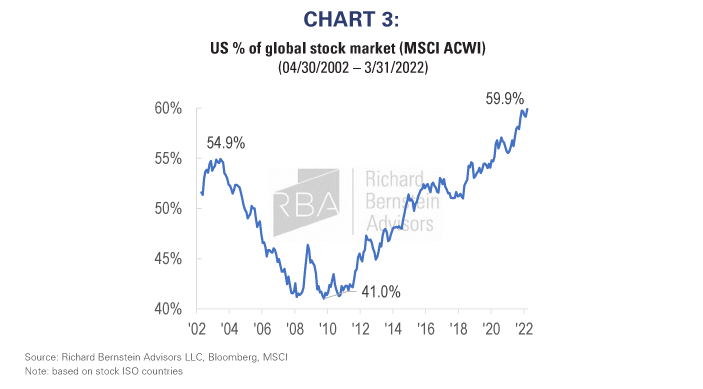

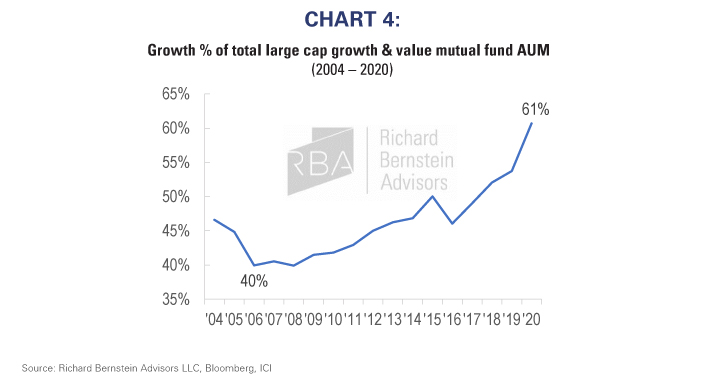

The problem in portfolios today is that concentration is high…

The narrow leadership of the past decade has led to high market concentration in those areas that have worked, namely US over international, large caps over small caps, and growth over value. Whether one focuses on single stocks, sectors, regions or styles, the level of concentration in the stock market is at or near record levels (Charts 1-4).

…AND so are correlations

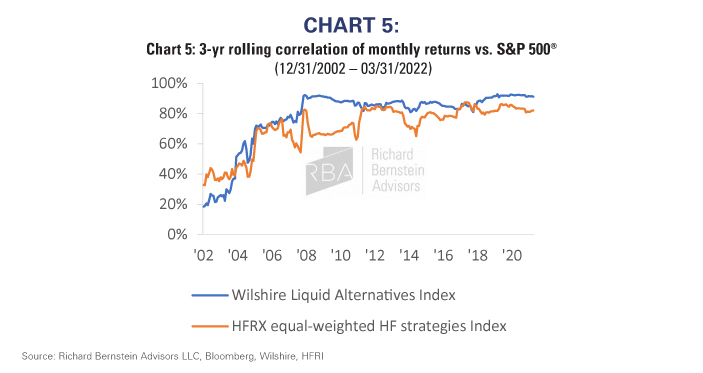

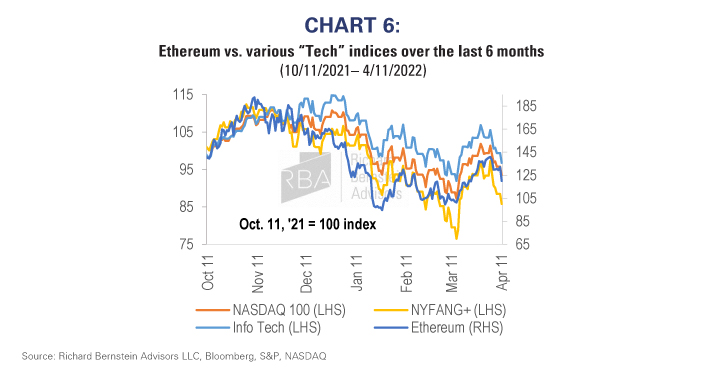

The very assets most sought after as sources of diversification, such as bonds and alternative investments, tend to have high or rapidly increasing correlations with stocks. Consider the Wilshire Liquid Alternatives Index, which is predominately made up of hedge funds. Both liquid alternatives and the broader hedge fund universe have become extremely correlated with stocks (Chart 5). In their limited history, cryptocurrencies have also become increasingly correlated with stocks, particularly with the areas of the market where concentration is the highest (Chart 6).

Bonds offer limited diversification in a rising rate paradigm

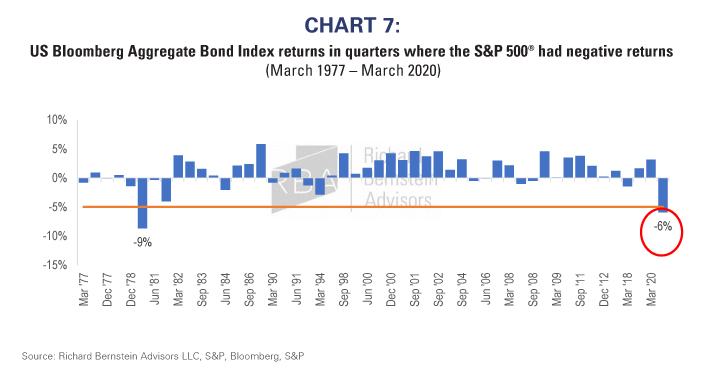

We believe we are in a new paradigm of rising interest rates, which suggests that bonds are not likely to provide anything like the type of negative correlations with stocks that investors have come to expect over the past 40 years. Case in point, the first quarter of this year was the first quarter since 1980 — the tail end of the last rising rate regime — where stock markets fell and bonds were down more than 5% (Chart 7).

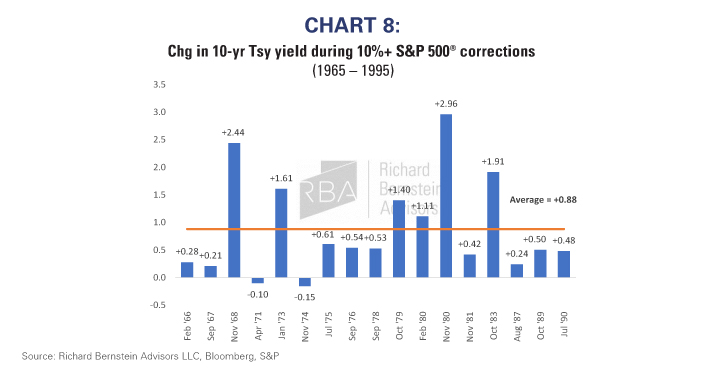

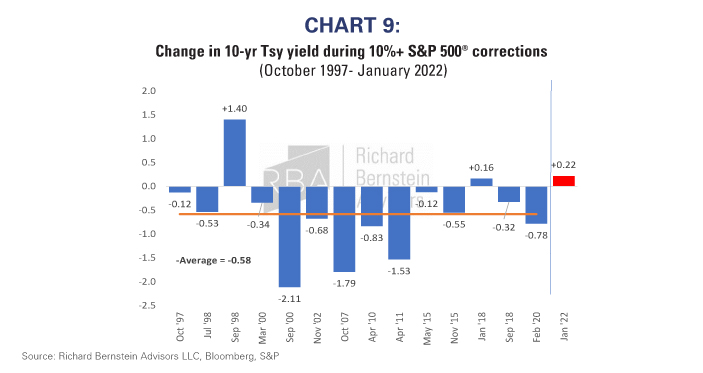

In fact, during the entire 30-year period from 1965 through 1995, there were only two instances where stocks fell by over 10% and the yield on 10-year Treasury bonds also declined — i.e. bond prices rose. All of the other 15 stock market corrections saw Treasury yields rise (bond prices fall) by an average of 88bp (Chart 8). It was only in the past two decades of low and declining interest rates where Treasury yields have tended to fall during stock market corrections, but that period may now be over (Chart 9).`

Higher interest rates hurt long-duration assets and those reliant on leverage

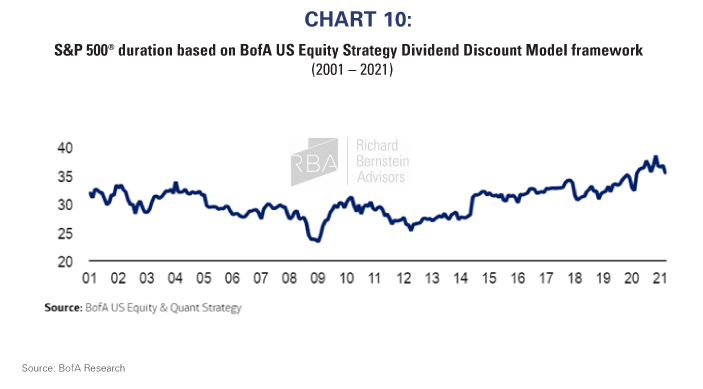

Other areas that investors often look to for diversification are private equity and real estate. However, if the new paradigm results in higher debt financing costs, the returns and valuations of these investments could come down dramatically due to their reliance on low-cost leverage. Additionally, long-duration investments, for which the bulk of the profits are projected to be far into the future, face significant valuation risk from higher interest rates. While this may pertain to some alternative investments such as venture capital or cryptocurrency, this also comes full circle back to the concentrated areas of the stock market. As highlighted in a report by BofA Research, the investment recovery period — also known as duration — for the US stock market remains near record levels, which makes it extremely vulnerable to higher interest rates (Chart 10).

Almost everything is dependent on low interest rates

To summarize, today’s stock markets are more concentrated than they have ever been. The increased concentration is in long-duration equities, which has increased the stock market’s sensitivity to interest rates. Investors have flocked to alternative investments hoping to add diversification, but most of these investments have high or increasing correlations with stocks and/or may struggle in a period of secularly rising interest rates.

Getting diversification today requires an active approach

The high degree of market concentration combined with elevated correlations across the investment landscape suggests that passive diversification is extremely low. This is not a desirable situation given the increased likelihood of a new paradigm of higher inflation and higher interest rates, and is particularly worrisome against the current fundamental backdrop of slowing corporate profit growth, tightening liquidity and elevated investor sentiment. We think the prudent response to such an environment would be to proactively force diversification into portfolios by reducing concentration and having exposure in areas with lower correlations. In our portfolios, we accomplish this by having less exposure to US stocks associated with innovation, technology and growth, while lessening our portfolios’ vulnerability to higher interest rates. Investors that attempt to follow suit should be prepared for tremendous resistance from their risk managers who will argue that the benchmark risk is too big. But that is exactly the point: prudent investors seeking diversification today should not look anything like their overly concentrated and highly correlated benchmark investments.

Dan Suzuki, CFA

Deputy Chief Investment Officer

Please feel free to contact your regional portfolio specialist with any questions:

Phone: 212 692 4088

Email: [email protected]

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

Wilshire Liquid Alternatives Index: The Wilshire Focused Liquid Alternative Index℠ measures the performance of a focused basket of mutual funds that provides risk adjusted exposure to equity hedge, global macro, relative value, and event driven alternative investment strategies.

Dan Suzuki is registered with Foreside Fund Services, LLC which is not affiliated with Richard Bernstein Advisors LLC or its affiliates.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially and should not be relied upon as such. The investment strategy and broad themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided "as is" without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of an

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors