The Fed Is NGMI

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBen Hunt: NGMI

Non-Linear Properties

Financialization

SIC and Mar-a-Lago

We found out this week that the first quarter was recessionary: GDP down 1.4% when the expectation was that the quarter would be up 1%. Rather large miss! Even so, the quarter-over-quarter comparisons were difficult so I believe the Fed will look past it and a 50-basis-point hike in May is still on.

Even if the US has a positive second quarter, the rest of the year is up to consumers. Europe will likely enter recession, which won’t help.

But what will help you is all the information that you will glean from the 18th annual Strategic Investment Conference starting Monday, May 2, at 10:00 am Eastern.

I hope you’ll join us in time to watch the livestream for the full SIC experience. Click here to get your Virtual Pass now.

This year’s faculty is even bigger and better than in the previous years, and that is saying something. I am rather proud of the group we have assembled. We’ve had the good fortune to book Dr. Henry Kissinger... David Rubenstein... Howard Marks... Joe Lonsdale... and other top names in policy, business, and finance.

We also have all our audience favorites back: Louis Gave and his father, Charles Gave... geopolitical wiz George Friedman... Felix Zulauf, one of the most visionary macro minds I’ve met... David Rosenberg, who as usual will kick off the SIC... Mark Yusko... Lacy Hunt... and Bill White.

On top of that, we have crypto and blockchain expert Dan Tapiero, founder and managing partner of 10T Holdings... Liz Ann Sonders, managing director and chief investment strategist at Charles Schwab... Dan Pickering, founder and CIO of Pickering Energy Partners, our go-to man for all things energy... and so many more, I can’t list them all.

(For a full list of speakers, click here.)

And as you know, we’ll have important things to talk about. If there was ever a year where we desperately needed input from the world’s top minds, this would be it.

Do yourself a favor and don’t miss it. You can watch and listen on all your devices—while commuting or working out if you wish. Or you can read the transcripts.

Click here to get your Virtual Pass now.

I have been neck-deep in planning for this conference, and honestly just haven’t had the time to do the research for a solid Thoughts from the Frontline. But my good friend Ben Hunt of Epsilon Theory, who will have his own session at the conference, has written what I think is one of his most powerful letters ever. He’s basically saying the Fed just isn’t going to make it. I wish I had written it. He is such a wordsmith. With that, let’s turn it over to Ben.

Ben Hunt: NGMI

For the over-40 or crypto-uninitiated or non-bodybuilding-4chan-reading crowd, NGMI stands for “not gonna make it.”

It’s typically used in a tsk-tsk fashion to describe someone who is not going to succeed because they chickened out or fundamentally misunderstood the big picture, as in “Joey sold all his Bitcoin at $40K. NGMI.” or “I sent Jimmy the links to my due diligence on GameStop and MOASS, but he still didn’t buy. NGMI.” It’s meant as an accusation of a lack of knowledge, but in truth it’s almost always an accusation of a lack of faith.

Jay Powell and the Fed, hiking rates to Whip Inflation Now? NGMI.

I mean that as both an accusation of lack of knowledge and lack of faith.

Source: Ben Hunt

This is Loretta Mester, from a screen shot of her appearance this Sunday on Face the Nation. Mester is the head of the Cleveland Fed and a 2022 voting member of the FOMC, the Fed committee that decides on interest rate hikes. Loretta Mester is a 63-year-old academic economist. She joined the Philly Fed in 1985, a freshly minted Princeton PhD, and has never worked outside of the Federal Reserve system. Never.

It’s going to seem like I’m picking on Mester, but everything I say about her and every quote I have from her could just as easily be said about or quoted from any other Fed governor. They are ALL part of the same inbred, arrogant, frequently wrong but never in doubt, Soviet nomenklatura-esque priesthood of central economic planning and control.

- John Williams, head of the NY Fed, has never held a job outside of the Federal Reserve system.

- Jim Bullard, head of the St. Louis Fed, has never held a job outside of the Federal Reserve system.

- Esther George, head of the Kansas City Fed, has never held a job outside of the Federal Reserve system.

- Mary Daly, head of the San Francisco Fed, has never held a job outside of the Federal Reserve system.

- Charles Evans, head of the Chicago Fed, has never held a job outside of the Federal Reserve system and academia.

- Raphael Bostic, head of the Atlanta Fed, has never held a job outside of the Federal Reserve system and academia.

- Kenneth Montgomery, interim head of the Boston Fed since Eric Rosengren resigned in disgrace, has never held a job outside of the Federal Reserve system.

- Meredith Black, interim head of the Dallas Fed since Rob Kaplan resigned in disgrace, has never held a job outside of the Federal Reserve system.

- Patrick Harker, head of the Philadelphia Fed, is not a Fed lifer. No, he’s an academia and government lifer.

- Thomas Barkin, head of the Richmond Fed, is also not a Fed lifer. No, he’s a former senior partner and CFO at McKinsey. LOL. Oh and fun fact… while she’s no longer a regional Fed president (but is on the Fed board of governors), Lael Brainard had a stint at McKinsey as her only job outside of government and academia. So weird.

- And then there’s Neel Kashkari, head of the Minneapolis Fed. Neel is just a stalking horse.

Anyhoo… here’s part of the transcript of Mester’s interview:

Q: The White House argues the true read of the economy is the strong jobs market. Do you believe employment is so strong, too strong to actually generate a recession?

MESTER: I think we can reduce that excess demand relative to supply without pushing the economy into a recession. So, I’m pretty optimistic we can do this. It’ll be challenging, but I think we can do it. And certainly my modal forecast of what’s going to happen this year is that the expansion will continue.

“My modal forecast”

Not “model” but “modal,” as in mean, median, and mode, as in run some econometric simulations and see whatever the most frequently observed outcome looks like. It is—and I mean this in all literal seriousness—the modern equivalent of cutting open a dozen rams and examining their entrails to see what the most typical pattern looks like.

Here’s what Loretta Mester saw in the entrails’ modal forecasts last year.

“I expect some higher inflation measures in the next couple of months but that is different from underlying inflation levels reaching 2%.” —Feb. 28, 2021

“I am unconcerned with inflation running away from us.” —April 5, 2021

“I’m not worried about inflation getting out of control.” —May 5, 2021

“The Fed needs inflation expectations and real inflation to rise.” —May 6, 2021

“I’d like to see inflation rise to 2% or higher.” —May 14, 2021

“By the end of the year, I expect inflation to be between 3.5% and 4%, with a drop in 2022.” —Aug. 27, 2021

“Inflation will be little more than 2% in the next years.” —Sept. 24, 2021

But wait, there’s more. It’s not just that Mester and the entirety of the Federal Reserve economic research team—more than FOUR HUNDRED PhD economists with a budget of literally hundreds of millions of dollars—got the 2021 transition to an embedded inflationary environment completely and utterly wrong, it’s also that Mester et al. got the prior embedded deflationary environment completely and utterly wrong.

Non-Linear Properties

Since early 2009, the Fed has provided the most accommodative monetary policy in human history with the express purpose of stimulating inflationary expectations and behaviors to something close to their 2% target. This effort was based on an essentially linear model of the macroeconomic relationship between the price of money and the velocity of money.

Does lowering the price of money from 8% to 7.5% create more risk-taking? Does it increase the velocity of money through the real economy as corporate and household risk-takers are willing to borrow and spend and invest more at 7.5% than they were at 8%? Yes.

How about lowering the price of money from 7.5% to 7%? Yes.

7% to 6.5%? to 6%? to 5.5%? to 4%? Yes, yes, yes, and yes.

It’s a nicely linear relationship (technically the word is “monotonic,” not linear per se, but close enough). Lower interest rates have a specific and direct relationship with risk-taking economic behavior and expectations. The lower the interest rate, the greater the spur to “inflation,” by which central bankers mean risk-taking economic behavior.

But a funny thing happens to risk-taking economic behavior and expectations when the price of money gets close to zero. Not only do you not get the same inflationary bang for your lower interest rate buck, but the relationship starts to go the other way. You start to get LESS risk-taking and inflationary behaviors in the real economy as you get really low interest rates.

Why?

Because the relationship between the price of money and real-world behavior is non-linear.

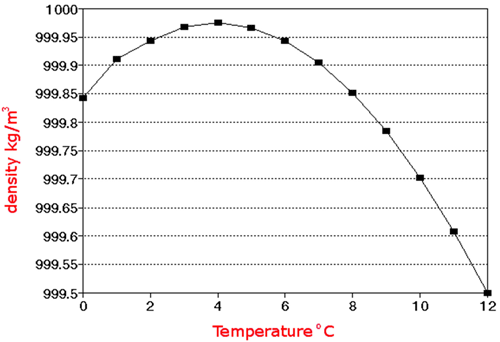

Just like water.

See, we all know that when gases or liquids get colder, they get denser. They get heavier. The molecules in the gas and the liquid are less energetic as they cool off. They bounce around less. They sink. This is why pool water and lake water and ocean water gets colder the deeper you go. It’s a perfectly linear relationship… the colder the water, the heavier the water… the colder the water, the more it sinks.

But when water gets to 4 degrees centigrade, this nicely linear relationship between temperature and density stops happening. In fact, it REVERSES. It’s not only non-linear, it’s non-monotonic (a ten-dollar word that means reversal). As water gets colder than 4 degrees centigrade, it no longer gets heavier. It no longer gets denser. It no longer sinks.

Source: Ben Hunt

Without this non-linear, non-monotonic property of water, life as we know it would hardly exist.

Every Ice Age would be every bit as much an extinction event as a giant meteor of death. Every lake or pond above or below a certain latitude would be as lifeless as the moon.

It’s a miracle of life that liquid water—the foundation of life on our planet—gets lighter instead of heavier right before it changes state into solid ice.

There’s no reason why this non-linear property of water should exist.

And yet it does.

If you were predicting the behavior of water from a theory of thermodynamics, there is no way you would predict 3-degrees cold water would be lighter than 4-degrees cold water.

And yet it is.

Financialization

What’s the point here? Just this:

So long as the academic Fed continues to use a set of essentially linear, monotonic models to understand the relationship between the price of money and real-world economic behaviors, their predictions will be just as wrong in the hiking stage of ZIRP monetary policy as they were in the cutting stage.

The Fed will overestimate the impact of rate hikes on curtailing inflation in exactly the same way they overestimated the impact of rate cuts on stimulating inflation.

Will hiking rates off the near-zero line make a difference in economic behaviors? Oh yes! Just not the behaviors that the Fed (and the White House) expect.

Cutting rates from 4% to 0% did not spur real-world inflationary behaviors, it spurred market-world financialization behaviors.

What is financialization?

Financialization is profit margin growth without labor productivity growth.

That sounds like a small thing, but I tell you it is EVERYTHING.

Financialization is the smiley-face perversion of Smith’s invisible hand and Schumpeter’s creative destruction, where profit margin growth is both pulled forward from future real growth and pulled away from current economic risk-taking.

Financialization is tax and balance sheet arbitrage to leverage laws passed by bought-and-paid-for politicians.

Financialization is stock buybacks to sterilize stock-based comp awarded to entrenched management.

Financialization is the acquisition and burying of smaller competitors to create an insurmountable, anti-competitive moat of scale in every economic sector.

Financialization is the zombiefication of an economy and the oligarchification of a society.

What has the last decade-plus of Fed interest rate cuts and balance sheet expansion given us? Not stable prices with healthy 2% inflation expectations. LOL.

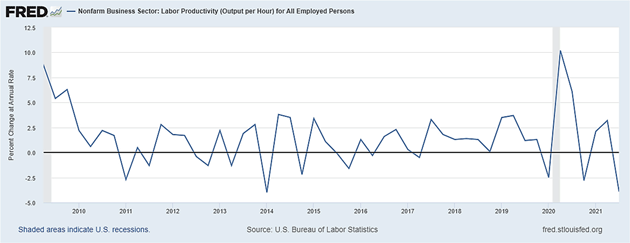

No, the last decade-plus of Fed monetary policy has given us this, the worst stretch of labor productivity growth in the history of the United States of America, not coincidentally occurring alongside the greatest stretch of financial asset appreciation in the history of the United States of America.

US Labor Productivity, Q2 2009 – Q2 2021

Source: Ben Hunt

What will Fed rate hikes reverse? Not inflation. Financialization.

What will Fed rate hikes spur? Not number go up. Productivity.

Like this: Starbucks’ Schultz announces halt to stock buybacks, shares fall

“Starbucks Corp. will pause billions of dollars of stock buybacks to invest more in employees and stores, longtime former chief executive Howard Schultz said on Monday on his return to lead the global coffee chain for a third time.”

I think what Howard Schultz did is very smart. I think Howard Schultz gets it. I think that taking the risk of investing more in employees and stores is exactly how Starbucks in particular and this economy in general will grow its way out of embedded inflationary expectations. I think what Howard Schultz announced is great for his company and great for the country!

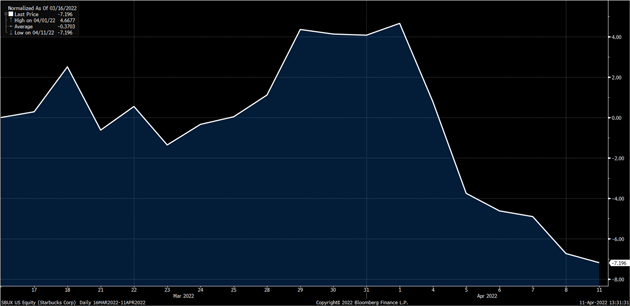

If you’re a Starbucks investor, though, you probably don’t agree with me. Here’s a price chart for SBUX starting on March 16, when the company announced that Schultz would be returning (again) as CEO. That sharp decline starting on April 4, an 11% free fall in the stock price? Yeah, that was the day that Schultz announced he was going to use their cash to take a shot at boosting productivity instead of the sure thing of stock buybacks.

Starbucks (SBUX) % price change, March 16–April 11, 2022

Source: Ben Hunt

I figure it will take 2+ years for Schultz’s capital allocation shift to translate in a serious way to improved, more robust profit margins through improved, more robust labor productivity. It may not happen at all if all the reinvestment is sucked dry by unionization. It’s a risk. A risk worth taking, I suspect, but definitely a risk. Which is why risk-takers get paid the big bucks. Or used to, anyway, until the non-risk-takers figured out they could get paid even bigger bucks by awarding themselves enormous levels of stock-based comp, converting it into cash comp through sterilizing stock buybacks, and then giving themselves even larger stock awards under the narrative of “aligning interests with shareholders.”

So 2+ years for this risk to pay off, if it pays off at all. Meanwhile, Starbucks’ stock price is down 30% from last summer.

And this is why the Fed NGMI.

Will the Fed rate hikes work to spur real growth and real productivity improvement in the real economy, breaking the vicious cycle of embedded inflationary expectations? Yes! Yes, they will! It’s already happening, in fact, with the most recent (partial Q4 2021) labor productivity rates jumping to 6.6%, the highest non-recession rate in 15 years!

But the rate hikes won’t curb inflation in the way that the Fed thinks they will. Their linear, monotonic models will get this all wrong until rates get back up to some normal-ish risk-free rate… I dunno, say 3.5% or thereabouts.

And while the reversal of our obscenely financialized world will lead to more and more companies taking real risks in the real economy, just like Starbucks is doing, which is fantastic for the long-term growth prospects of the United States, this process will take years. It took a decade-plus to get into this mess, and it will take a decade-plus to get out of this mess. We don’t have that kind of time.

Because capital markets have become political utilities.

Our political system cannot withstand a decade-plus of mediocre to poor returns from capital markets, even though that’s exactly what is required to wring out the decade-plus of financialization that Fed ZIRP policies and monetary accommodation have created. Hell, I don’t think our political system can withstand more than a quarter or two of this, where every company is a Starbucks down 30%+ and every bond portfolio is having the worst year in 40 years.

The Fed’s not gonna make it because:

a) their lack of knowledge, using linear models to predict a non-linear system, and

b) their lack of faith, choosing a path of political expediency over stewardship of American productivity.

What comes after all this? What happens when it becomes common knowledge that the Fed can’t “control” inflation the way they predicted?

I think we get a war.

I think we get a man with a plan.

And that’s when our troubles truly begin.

SIC and Mar-a-Lago

John here again. Thank you to Ben Hunt for permission to share his piece. Over My Shoulder members can read an annotated version here.

I am pumped and primed for the SIC. We are still last-minute negotiating some famous names. More info here.

Turns out Saturday night I was in Palm Beach and having dinner with friends, including Barry Habib (mortgage guru who will also be speaking at SIC). Since I was riding with him, he shanghaied me and took me to Mar-a-Lago. It was late and I was not enthusiastic, but I did get to meet some, shall we say, interesting and controversial people. Made the evening and late night worth it. And George Hamilton at 82 still has the best tan on the planet.

You should follow me on Twitter. It is about to get interesting. Have a great week!

Your ready to learn at SIC along with you analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All