Bond Investors Underperformed Despite A Bull Market. Now What?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBonds have been in a secular bull market for forty years, and bond investors have reaped the benefits. Or have they?

Bond investors benefitted from secularly falling interest rates, but their active management within the overall fixed-income market detracted significantly from their returns. Recently updated data from Dalbar show bond investors, like equity investors, tend to buy high and sell low. As a result the “typical” active individual fixed-income investor has secularly underperformed virtually any buy-and-hold fixed-income strategy.

We believe that we are at the start of a pro-inflation paradigm shift, which will challenge traditional buy-and-hold fixed-income investing. If active individual fixed-income investors performed so terribly during a secular bull market, it seems quite a challenge to expect them to perform well during a less advantageous secular period.

A history of poor active management

The annual DALBAR study that estimates investors’ performance was recently released for 2021. Investor returns are calculated by DALBAR using the change in total mutual fund assets after excluding sales, redemptions and exchanges. This method of calculation captures realized and unrealized capital gains, dividends, interest, trading costs, sales charges, fees, expenses and any other costs. RBA then analyzed DALBAR’s results to see how the “Average Fixed Income Investor” would have performed over the past 3, 5, 10 and 20 years. RBA compared the DALBAR fixed income fund investor returns with those of different fixed income asset classes and sub-classes for the 3, 5, 10 and 20-year periods ending December 31, 2021.

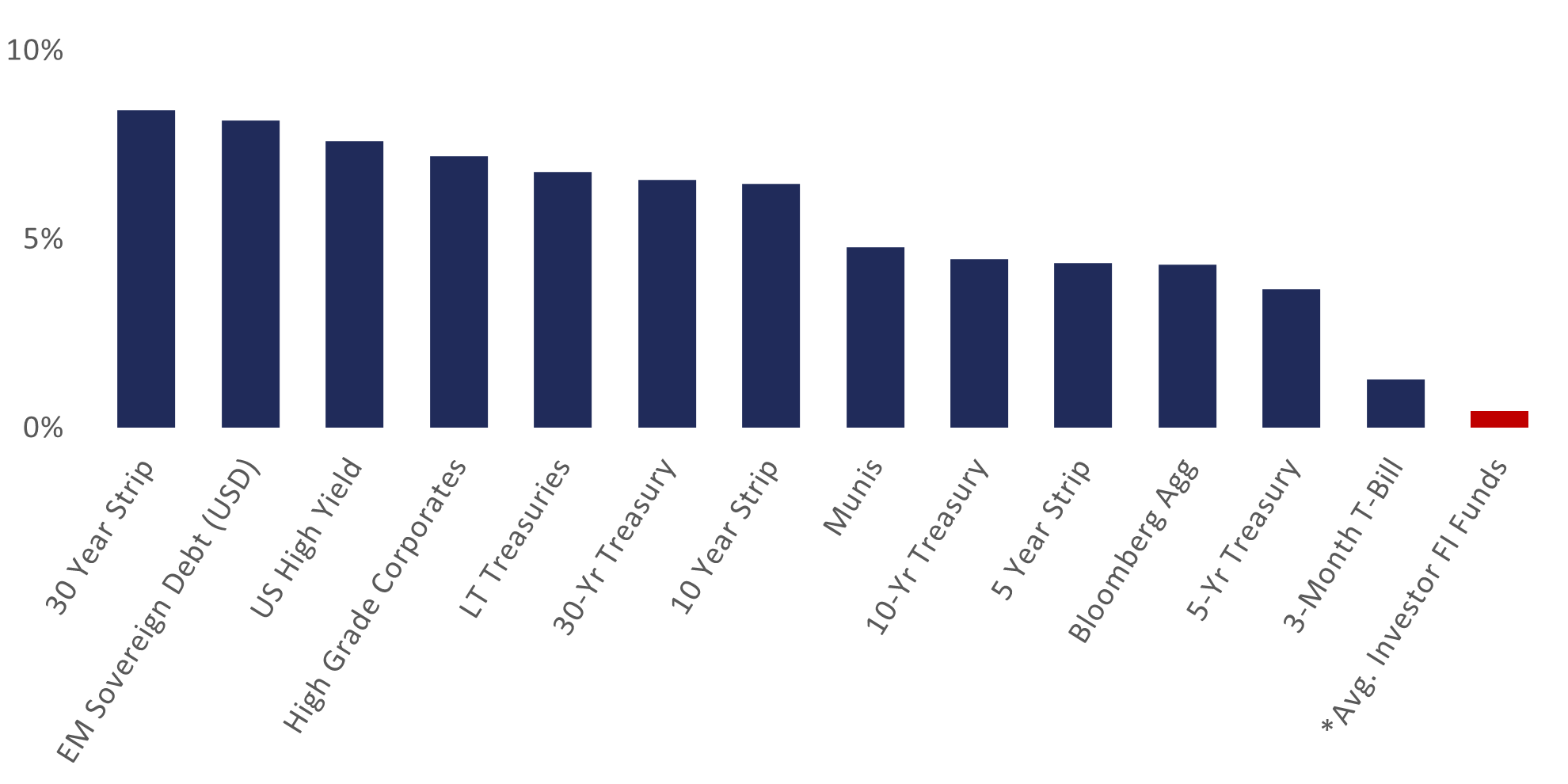

Chart 1 shows the annualized returns of various fixed-income asset and sub-asset classes over the past 20 years. The only requirement for outperformance during the period was a willingness among fixed-income investors to take risk because bets on both long-duration and credit significantly outperformed. The top three performing classifications were 30-year zero-coupons, EM sovereigns, and US high yield.

However, Dalbar’s “typical” investor actually underperformed cash. Their timing decisions were so poor that they underperformed any buy-and-hold strategy in any fixed-income classification. Essentially, investors simply needed to pick one fixed-income category and hold to perform better than they actually did.

Chart 1: Asset Class Returns

(20-Years Annualized 12/31/2001-12/31/2021)

Source: Richard Bernstein Advisors LLC., Bloomberg, ICE BofAML, DALBAR. Total Returns in USD. *Average Investor Fixed Income (FI) Fund returns are represented by DALBAR's fixed income fund investor returns which represent the change in total mutual fund assets after excluding sales, redemptions and exchanges. For descriptors, see "Index Descriptions" at end of document.

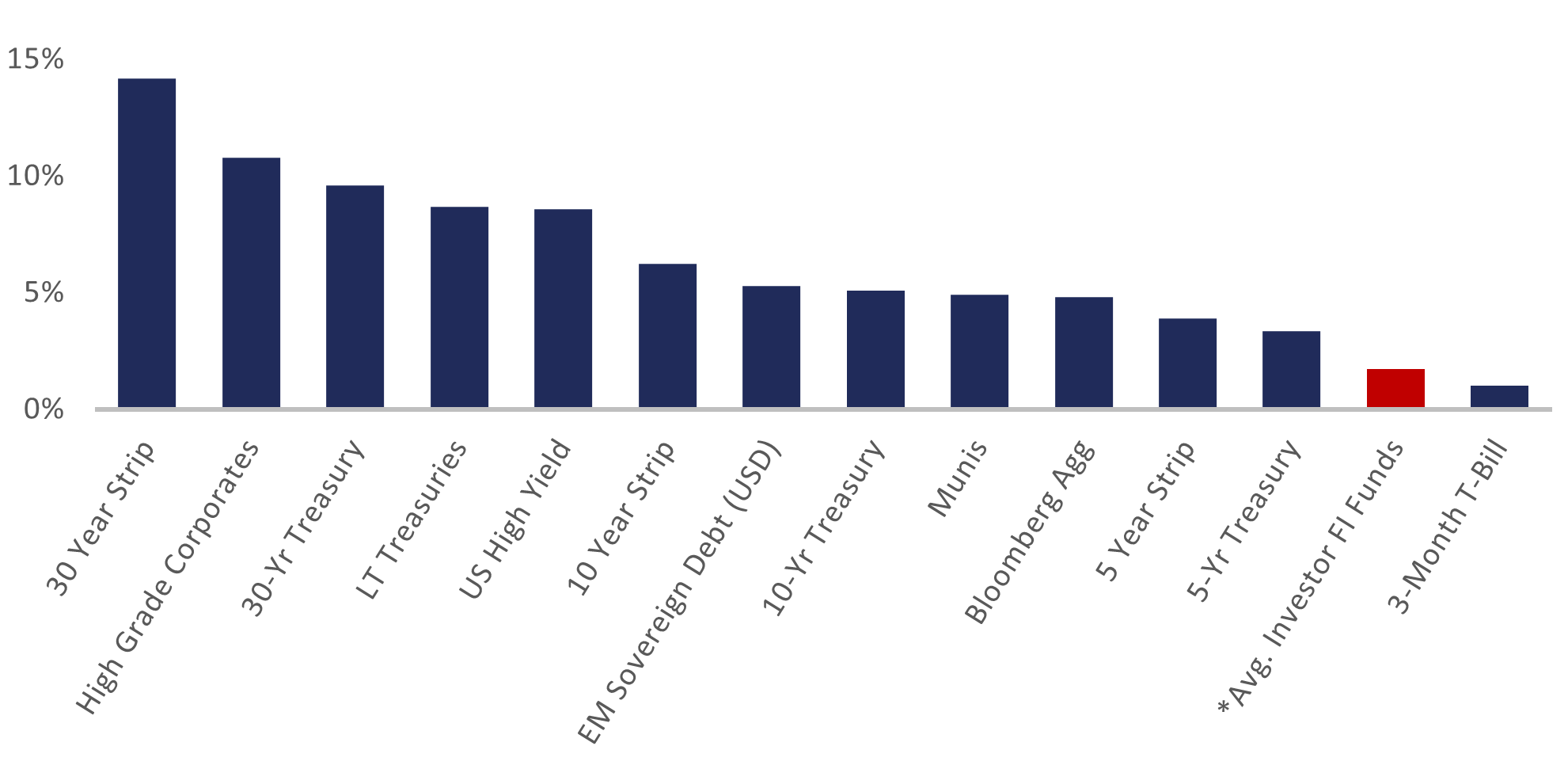

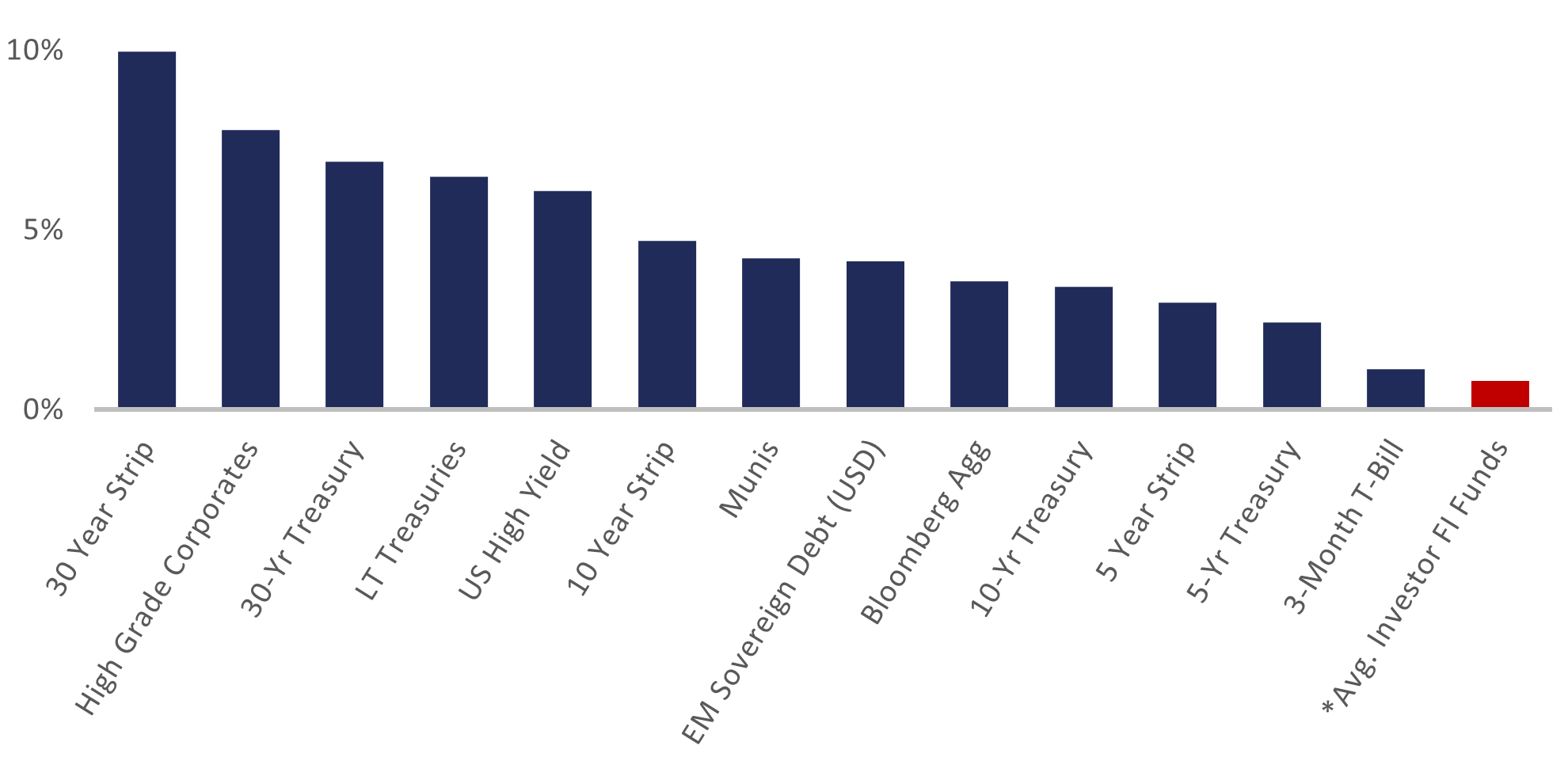

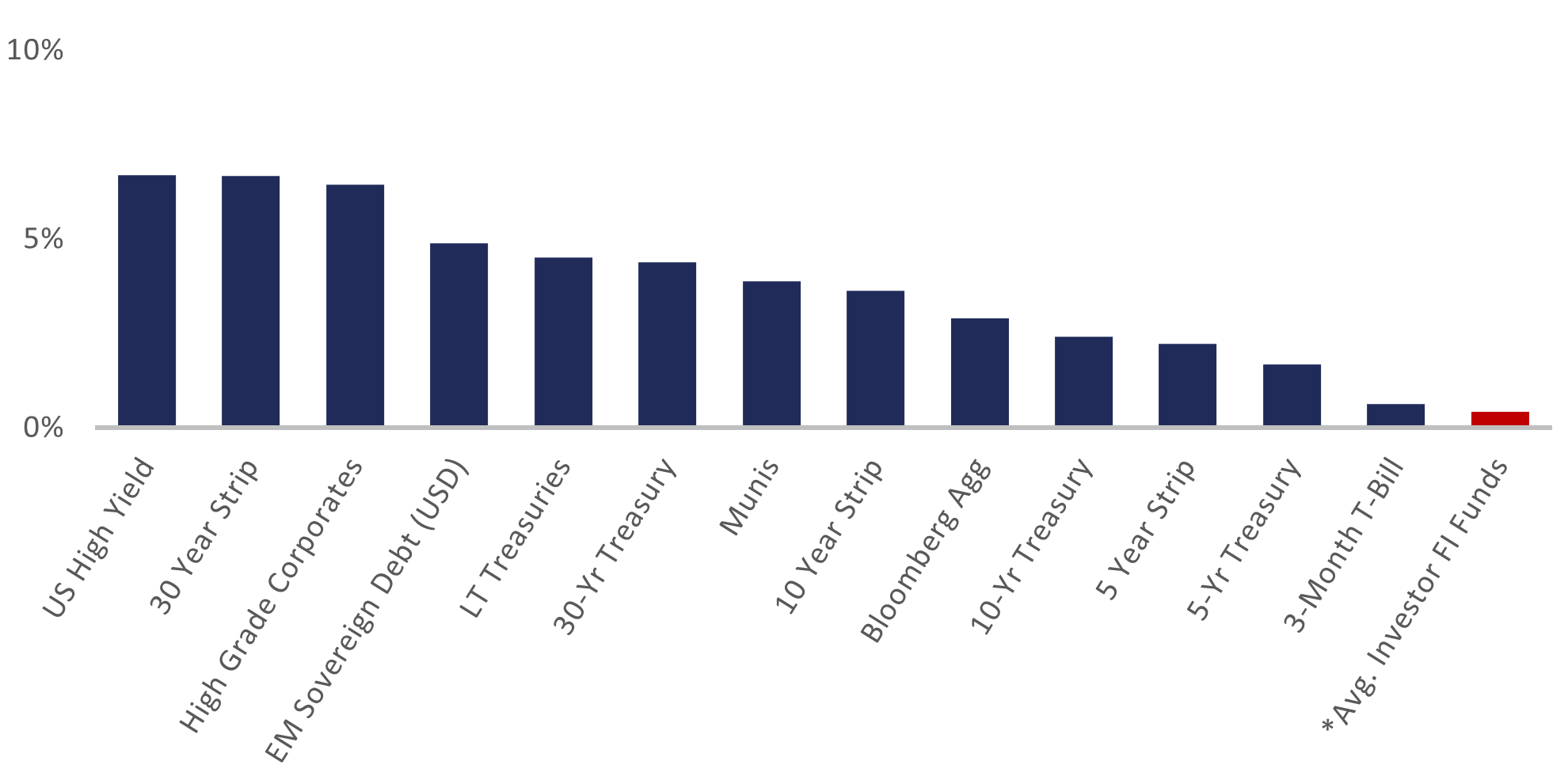

Charts 2, 3, and 4 show similar returns data for the last 3, 5, and 10 years, and the results are not different. Fixed-income investors’ active management proved unsuccessful in each of their periods, and the “typical” investor consistently underperformed virtually every major fixed-income category.

Chart 2: Asset Class Returns

(3-Years Annualized 12/31/2018-12/31/2021)

Source: Richard Bernstein Advisors LLC., Bloomberg, ICE BofAML, DALBAR. Total Returns in USD. *Average Investor Fixed Income (FI) Fund returns are represented by DALBAR's fixed income fund investor returns which represent the change in total mutual fund assets after excluding sales, redemptions and exchanges. For descriptors, see "Index Descriptions" at end of document.

Chart 3: Asset Class Returns

(5-Years Annualized 12/31/2016-12/31/2021)

Source: Richard Bernstein Advisors LLC., Bloomberg, ICE BofAML, DALBAR. Total Returns in USD. *Average Investor Fixed Income (FI) Fund returns are represented by DALBAR's fixed income fund investor returns which represent the change in total mutual fund assets after excluding sales, redemptions and exchanges. For descriptors, see "Index Descriptions" at end of document.

Chart 4: Asset Class Returns

(10-Years Annualized 12/31/2011-12/31/2021)

Source: Richard Bernstein Advisors LLC., Bloomberg, ICE BofAML, DALBAR. Total Returns in USD. *Average Investor Fixed Income (FI) Fund returns are represented by DALBAR's fixed income fund investor returns which represent the change in total mutual fund assets after excluding sales, redemptions and exchanges. For descriptors, see "Index Descriptions" at end of document.

It has been widely recognized that short-term interest rates have been historically low for a long time and how unattractive money market investing has been. Yet, and perhaps most startling, fixed-income investors underperformed short-term T-Bills in all but the past 3-year period.

What happens now?

If we are correct and fixed-income performance will become more difficult in the future as secular disinflation turns to secular inflation, then fixed-income investing will likely need to change. The earlier charts demonstrated that fixed-income investors weren’t successful during a significant secular bull market for bonds. It seems unlikely that they’d perform better during a secular bear market when there are no positive trends to disguise allocation mistakes.

We think active fixed-income investing will change such that investors may need to be more:

- 1) Creative – look for both unique asset classes and hedging strategies.

- 2) Tactical – be willing to significantly alter duration and credit depending on the cycle.

- 3) Active – buy-and-hold strategies are likely to perform poorly as the secular tailwinds of disinflation and falling rates reverse.

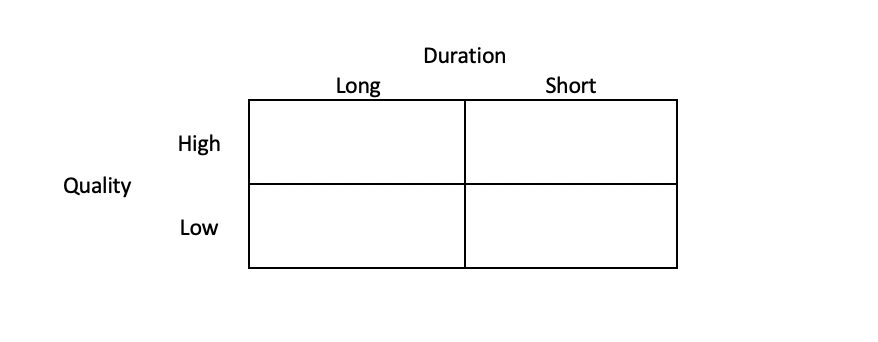

Active fixed-income is often summarized by the following 2x2 matrix. One side of the matrix differentiates high versus low quality, whereas the other side highlights long versus short duration. Fixed-income investors must decide which exposures they want within their portfolios or whether to neutralize their positions to their benchmark (i.e., being on a dividing line in the graphic).

The following two charts compare the performance of credit versus quality while keeping duration constant and the performance of long versus short duration while keeping credit constant. In other words, the charts examine the historical performance when deciding between columns only or rows only.

Chart 5 shows there were 5 strategic decisions investors had to make in the last 10 years regarding quality. Chart 6 indicates there were 11 decisions regarding duration. In most cases the duration decisions didn’t coincide with the credit decisions. Thus, an active fixed-income investor would have had to make roughly 16 important allocation decisions in the last 10 years.

Making such decisions was a significant challenge to investors during the bond bull market. They underperformed, but at least returns were positive. If they have similar difficulty during a secular bear market, it seems highly likely their returns would be negative.

Chart 5: Bloomberg US High Yield vs. Bloomberg US Corporates

May 3, 2012 – May 3, 2022

Source: Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.

Chart 6 Bloomberg 20+ Year Corporates vs. Bloomberg 3-5 Year Corporates

May 2, 2012 – May 3, 2022

Source: Bloomberg Finance L.P. For Index descriptors, see "Index Descriptions" at end of document.May 2, 2012 – May 3, 2022

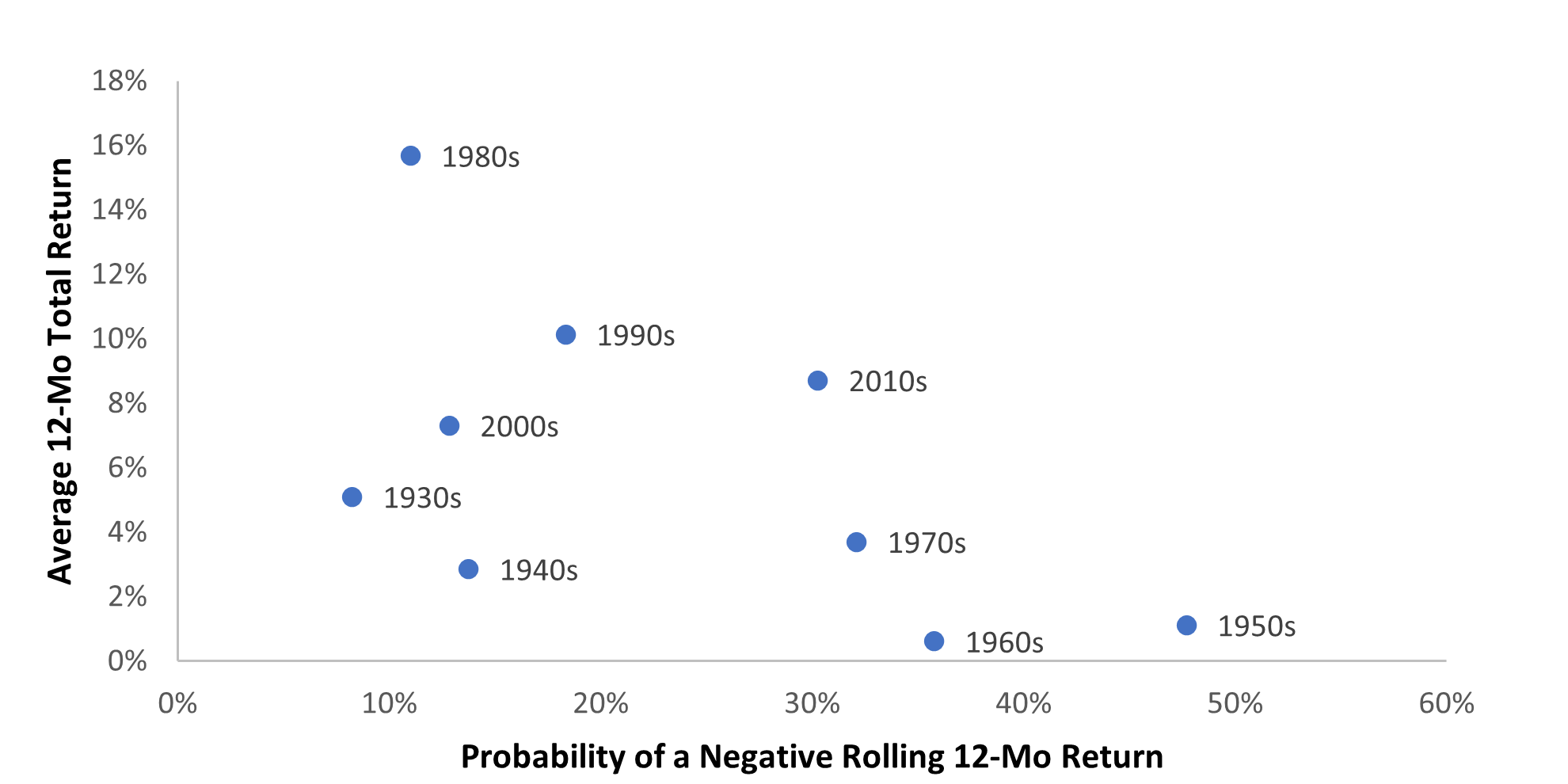

Reliving the 1960s and 1970s

If the period of secular disinflation that fueled the secular bond bull market is ending, then bond investors may be challenged as they were in the 1960s and 1970s. Chart 7 shows the risk return statistics of long-term Treasuries by decade.

The chart highlights how the overall bond market bailed out poor active management. Bonds gave high returns with relatively little probability of losing money over the past several decades . However, bonds had poor returns during the 1960s and 1970s and a higher probability of negative returns.

Chart 7: Risk/Return of Long Term Government Bonds by Decade (total returns)

Source: Richard Bernstein Advisors LLC, SBBI® YearbookChart 7: Risk/Return of Long Term Government Bonds by Decade (total returns)

A new paradigm of bond investing.

The changing global economy is signaling a potential end to secular disinflation and secularly falling interest rates. Accordingly, the global economy might be signaling a paradigm shift in fixed-income investing.

Buy-and-hold strategies worked well when the bond market was in a secular bull phase. Poor active management’s mistakes were easily masked by the downward trend in rates. However, a review of earlier decades shows that buy-and-hold strategies don’t work well during a secular bear market and mistakes are quickly exposed.

Truly active “active” management might be the new requirement for successful fixed-income investing.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

Bloomberg US Aggregate Bond Index: The Bloomberg US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency).

3-Mo T-Bills: ICE BofAML 3-Month US Treasury Bill Index. The ICE BofAML 3-Month US Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. The Index is rebalanced monthly and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date.

5-Year Treasury: The ICE BofAML 5-Year US Treasury Index. The ICE BofAML 5-Year US Treasury Index is a one-security index comprised of the most recently issued 5-year US Treasury note. The index is rebalanced monthly. In order to qualify for inclusion, a 5-year note must be auctioned on or before the third business day before the last business day of the month.

5-Year Strip: The ICE BofAML US 5-Year Constant Maturity STRIP Index. The ICE BofAML US 10 Year Constant Maturity STRIP Index tracks the performance of a single synthetic US Treasury STRIP purchased at the beginning of the month, held for one month, and then sold at the end of the month with the proceeds rolled into a new instrument. Therefore, on the purchase date, the bond has a maturity exactly equal to the stated maturity of the index, and at the point it is sold it is one month short of the index stated maturity. The synthetic STRIP has a zero coupon, a purchase yield equal to the yield of the corresponding point on the coupon STRIP curve, and a purchase price which is derived from the purchase yield.

10-Year Treasury: The ICE BofAML 10-Year US Treasury Index. The ICE BofAML 10-Year US Treasury Index is a one-security index comprised of the most recently issued 10-year US Treasury note. The index is rebalanced monthly. In order to qualify for inclusion, a 10-year note must be auctioned on or before the third business day before the last business day of the month.

10-Year Strip: The ICE BofAML US 30-Year Constant Maturity STRIP Index

The ICE BofAML US 10 Year Constant Maturity STRIP Index tracks the performance of a single synthetic US Treasury STRIP purchased at the beginning of the month, held for one month, and then sold at the end of the month with the proceeds rolled into a new instrument. Therefore, on the purchase date, the bond has a maturity exactly equal to the stated maturity of the index, and at the point it is sold it is one month short of the index stated maturity. The synthetic STRIP has a zero coupon, a purchase yield equal to the yield of the corresponding point on the coupon STRIP curve, and a purchase price which is derived from the purchase yield.

30-Year Treasury: The ICE BofAML Current 30-Year US Treasury Index

The ICE BofAML Current 30-Year US Treasury Index is a one-security index comprised of the most recently issued 30-year US Treasury bond. The index is rebalanced monthly. In order to qualify for inclusion, a 30-year bond must be auctioned on or before the third business day before the last business day of the month.

30-Year Strip: The ICE BofAML US 30 Year Constant Maturity STRIP Index

The ICE BofAML US 30 Year Constant Maturity STRIP Index tracks the performance of a single synthetic US Treasury STRIP purchased at the beginning of the month, held for one month, and then sold at the end of the month with the proceeds rolled into a new instrument. Therefore, on the purchase date, the bond has a maturity exactly equal to the stated maturity of the index, and at the point it is sold it is one month short of the index stated maturity. The synthetic STRIP has a zero coupon, a purchase yield equal to the yield of the corresponding point on the coupon STRIP curve, and a purchase price which is derived from the purchase yield.

INDEX DESCRIPTIONS cont’d

Long-term Treasury Index: ICE BofAML 15+ Year US Treasury Index. The ICE BofAML 15+ Year US Treasury Index is an unmanaged index comprised of US Treasury securities, other than inflation-protected securities and STRIPS, with at least $1 billion in outstanding face value and a remaining term to final maturity of at least 15 years.

Municipals: ICE BofAML US Municipal Securities Index. The ICE BofAML US Municipal Securities Index tracks the performance of USD-denominated, investment-grade rated, tax-exempt debt publicly issued by US states and territories (and their political subdivisions) in the US domestic market. Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule, and an investment-grade rating (based on an average of Moody’s, S&P and Fitch). Minimum size requirements vary based on the initial term to final maturity at the time of issuance.

High Grade Corporates: ICE BofAML 15+ Year AAA-AA US Corporate Index. The ICE BofAML 15+ Year AAA-AA US Corporate Index is a subset of the ICE BofAML US Corporate Index (an unmanaged index comprised of USD-denominated, investment-grade, fixed-rate corporate debt securities publicly issued in the US domestic market with at least one year remaining term to final maturity and at least $250 million outstanding) including all securities with a remaining term to final maturity of at least15 years and rated AAA through AA3, inclusive.

U.S. High Yield: ICE BofAML US Cash Pay High Yield Index. The ICE BofAML US Cash Pay High Yield Index tracks the performance of USD-denominated, below-investment-grade-rated corporate debt, currently in a coupon-paying period, that is publicly issued in the US domestic market. Qualifying securities must have a below-investment-grade rating (based on an average of Moody’s, S&P and Fitch) and an investment-grade-rated country of risk (based on an average of Moody’s, S&P and Fitch foreign currency long-term sovereign debt ratings), at least one year remaining term to final maturity, a fixed coupon schedule, and a minimum amount outstanding of $100 million.

EM Sovereign: ICE BofAML BBB & Lower Sovereign USD External Debt Index. The ICE BofAML BBB & Lower Sovereign USD External Debt Index tracks the performance of US dollar denominated emerging market and cross-over sovereign debt publicly issued in the Eurobond or US domestic market. Qualifying countries must have a BBB1 or lower foreign currency long-term sovereign debt rating (based on an average of Moody’s, S&P and Fitch). Countries that are not rated, or that are rated “D” or “SD” by one or several rating agencies qualify for inclusion in the index but individual non-performing securities are removed. Qualifying securities must have at least one year remaining term to final maturity, a fixed or floating coupon and a minimum amount outstanding of $250 million. Local currency debt is excluded from the Index.

Avg. Investor Fixed Income Funds: Returns are for the 3,5,10 and 20-year periods ending December 31, 2021. The DALBAR Inc. Average Investor Fixed Income Fund performance results are calculated using data supplied by the Investment Company Institute. Investor returns are represented by the change in total mutual fund assets after excluding sales, redemptions and exchanges. This method of calculation captures realized and unrealized capital gains, dividends, interest, trading costs, sales charges, fees, expenses and any other costs. After calculating investor returns in dollar terms, two percentages are calculated for the period examined: Total investor return rate and annualized investor return rate. Total return rate is determined by calculating the investor return dollars as a percentage of the net of the sales, redemptions and exchanges for each period.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All