When will the bear market end? That is the question to which everyone wants an answer. While there is no specific answer to that question, there are indicators and technical measures that provide some guidance. From the portfolio management perspective, those are the parameters we must operate from to minimize capital destruction and limit emotionally driven mistakes.

2022 has been a year unlike many investors have seen in their investing lifetimes. While there are some that went through the 2008 bear market, there are fewer still who lived through the “Dot.com” crash. Such is the nature of “real” bear markets that tend to destroy investors and drive them from investing in the financial markets permanently.

While there are many “buy and hold” practitioners suggesting investors just dollar-cost-average their way through a downturn, reality tends to be far different. When markets decline enough, there is a point where every investor changes from “Buy The F***ing Dip” to “Get Me F***ing Out.”

When it comes to investing, most armchair portfolio management systems work great as long as markets rise. However, when the eventual correction comes, the psychology of “loss aversion”disrupts the best-laid plans.

It is also important to understand that “bear markets” are just the natural completion of a “full market cycle.” During bull markets, excesses are built which are reflected in valuations as investors overpay for assets on expectations for infinite growth. Obviously, since the business cycle is not infinite, the ensuing bear market is the reversal of those excesses. While “bear markets” often surprise investors, they are the logical conclusion of the preceding advance.

So, with a potential bear market at hand as the Fed hikes rates, inflation remains high, and the economy continues to slow, let’s get to the question at hand:

“When will this bear market end?”

Evidence Of The Bear

There is considerable technical evidence that U.S. financial markets are in a “bear market.” The NYSE Composite (US stocks + ADRs + bond ETFs) has broken below its 100-week moving average. In the past 25-years, every recession and/or crisis has coincided with a break of that long-term moving mean.

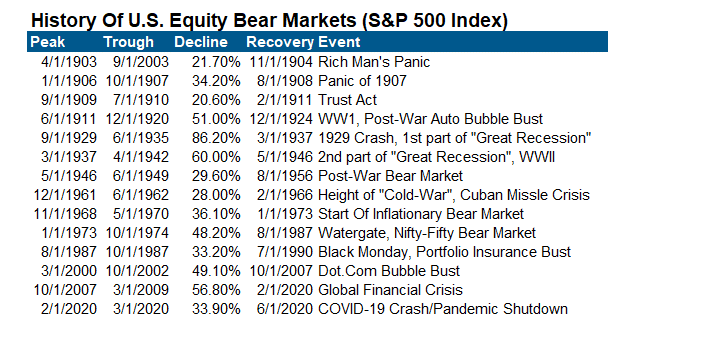

As noted above, bear markets are not uncommon and follow preceding bull market excesses. Over the last 120-years, there have been 14-bear markets that averaged roughly a 33% decline from peak to trough.

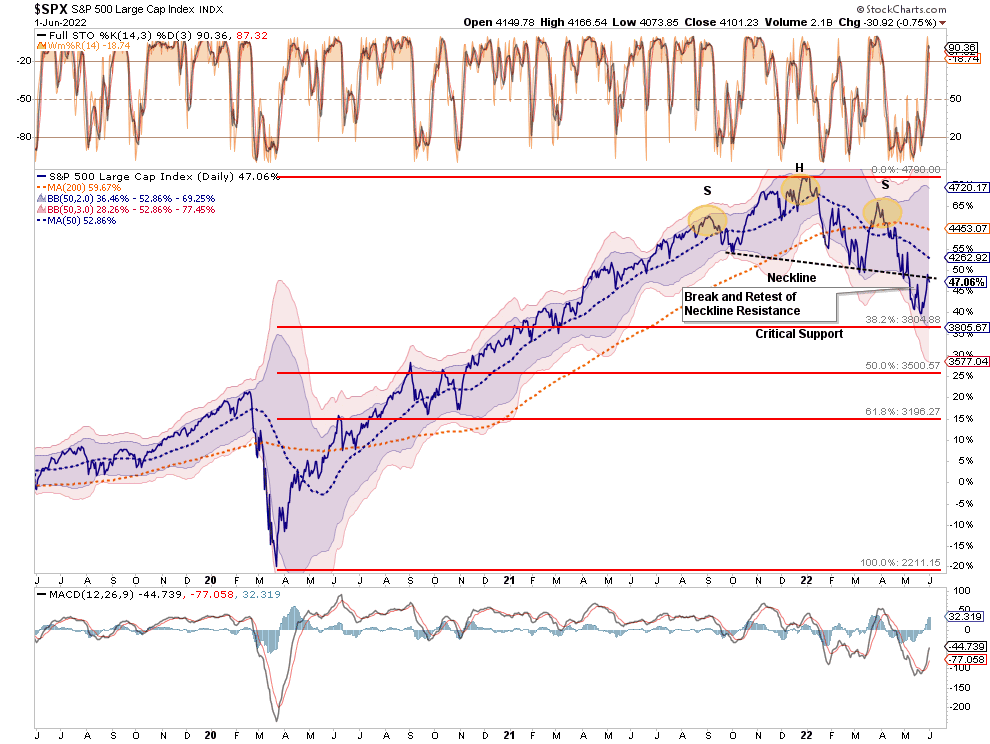

As I discussed recently,the price action of the market in 2022, has a lot of similarities to what we witnessed in 2008 prior to the collapse of Lehman Brothers.

“The head and shoulders topping pattern is quite evident. The break of the rising neckline was the first warning of a recessionary bear market. The subsequent rally to, and failure at, the neckline confirmed the topping process was complete.”

We see the same market action in 2022.

Again, we see the topping process, the clear break of the neckline, and a failed test of the neckline, turning it into resistance. While the market sits on critical support, any failure will confirm a recession, and a bear market is underway.

The technical data is only confirming what we are already seeing economically as well. The EOCI (economic composite output index) is contracting quickly as the Leading Economic Index (LEI) confirms the data trend. While the negative Q1-GDP may reverse slightly in Q2, such will not change the eventually recessionary outcome.

The Bear Market Will End…Eventually

There are certainly many technical and economic supporting negative market views, however, it is crucial to remember that bear markets end, eventually. Yes, while such seems to be tautological, investors tend to extrapolate current market trends indefinitely into the future.

The question is how will we know when the current bear market cycle is over? Given that financial markets lead economic cycles, the market can provide several clues as to when things may be turning more positive from an investment view.

The first is the most obvious; asset prices stop going down. Using our 2008 analogy, coming out of a bear market stock prices begin to establish a series of higher highs and lows. More importantly, begin to see momentum measures establish a more positive trend as well and moving averages slope upward.

Notably, the economy did not exit the recession until June of 2009, but financial markets began to rally in anticipation.

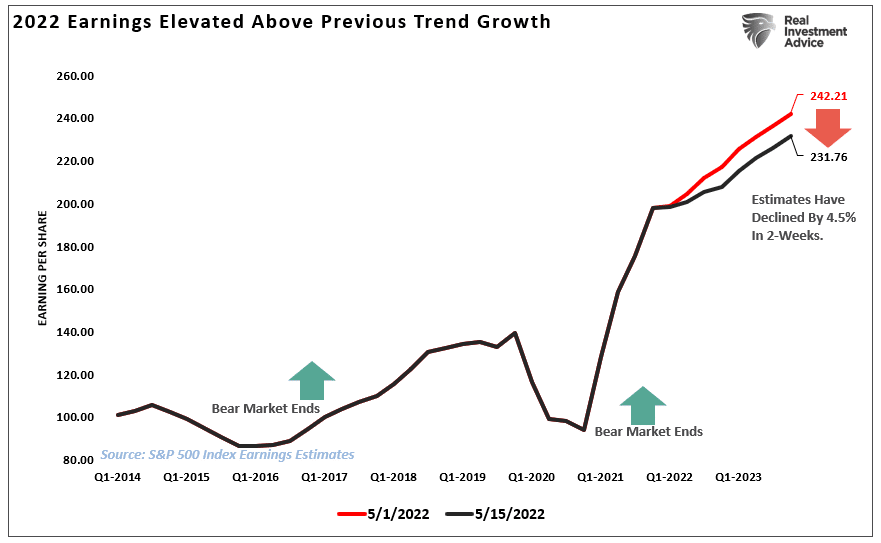

Furthermore, during the last four recessions, and subsequent bear markets, the typical revision to consensus EPS estimates prior to the onset of a recession ranged from -6% to -18% with a median of 10%. Coming out the recession, analysts start to increase estimates markedly. Currently, we are only just starting the negative revision phase, but the reversal of that trend will be key in identifying the bear market end.

While there are many other indicators worthy of watching to denote an end to the bear market phase, the most critical aspect of investment outcomes is remaining disciplined in your process.

Stick To Your Process

There is a sizable contingent of investors, and advisors, who have never been through a real bear market. After a decade-long bull-market cycle, fueled by Central Bank liquidity, it is understandable why mainstream analysis believed the markets could only go higher. What was always a concern to us was the rather cavalier attitude they took about the risk.

“Sure, a correction will eventually come, but that is just part of the deal.”

What gets lost during bull cycles, and is always found in the most brutal of fashions, is the devastation caused to financial wealth during the inevitable decline.

Therefore, it remains important to follow your investment discipline. If you don’t have one, here is the process that we follow during tough markets.

7-Rules To Follow

Move slowly. There is no rush in making dramatic changes. Doing anything in a moment of “panic” tends to be the wrong thing.

If you are overweight equities, DO NOT try and fully adjust your portfolio to your target allocation in one move. Again, after big declines, individuals feel like they “must” do something. Think logically above where you want to be and use the rally to adjust to that level.

Begin by selling laggards and losers. These positions were dragging on performance as the market rose and they led on the way down.

Add to sectors, or positions, that are performing with, or outperforming the broader market if you need risk exposure.

Move “stop-loss” levels up to recent lows for each position. Managing a portfolio without “stop-loss” levels is like driving with your eyes closed.

Be prepared to sell into the rally and reduce overall portfolio risk. There are a lot of positions you are going to sell at a loss simply because you overpaid for them to begin with. Selling at a loss DOES NOT make you a loser. It just means you made a mistake. Sell it, and move on with managing your portfolio. Not every trade will always be a winner. But keeping a loser will make you a loser of both capital and opportunity.

If none of this makes any sense to you – please consider hiring someone to manage your portfolio for you. It will be worth the additional expense over the long term.