The Federal Open Market Committee (FOMC) will be gathering next week to take stock of monetary policy. The outcome is nearly a forgone conclusion: Fed Chairman Jerome Powell hinted strongly that half-point interest rate increases were “on the table” for the June and July meetings.

But how far will the Fed have to go to get the desired outcome? Can they steer to a soft landing, or will a recession be required to change the course of inflation? And how will they use their balance sheet to manage liquidity in the system?

Following are additional details on the factors the group will consider, with both sides of each issue presented. Elements that would lead to tighter policy are categorized in the “More Hawkish” column; factors that might suggest a more lenient path are detailed in the “Less Hawkish” column.

Economic Growth

|

More Hawkish

|

Less Hawkish

|

|

As of the second quarter of 2021, U.S. gross domestic product (GDP) returned to its pre-pandemic level, and continued growing from there. The pandemic damage has largely been undone, and an accommodative posture is no longer necessary. Sections of the economy, like housing and durable goods, are overheated, and higher rates may encourage a soft landing.

|

The Ukraine conflict brought about higher energy prices that are weighing on growth prospects. Equity and bond markets have had a difficult start to the year. First quarter GDP registered a contraction, suggesting the economy remains out of equilibrium. Concerns of an imminent recession are rising, and a more accommodative policy could help defuse tensions.

|

The past year brought growth and recovery from the pandemic that was better than expected. However, the recovery was uneven; some sectors (like transportation) were unable to keep up with demand, while others (like business travel) remain weakened. The Fed has an important role to play in setting a path toward sustainable growth.

The Fed has changed their posture very rapidly in just six months; thus far, their shift has not impaired growth. The economy has recovered well but is in a precarious state. FOMC members will have many important considerations as they cast their votes.

Inflation

The price level is the chief concern of the FOMC. Inflation rates have begun to plateau, but there is vigorous debate about how quickly rates will ease. Our analysis of the inflation picture can be found here.

|

More Hawkish

|

Less Hawkish

|

|

Many factors driving inflation are worse than they were six months ago. Filling up with gas has become a painful experience. Supply chains are still distressed, labor markets are tighter and food prices are surging. Housing costs are flowing into the CPI at a 7.6% annual clip. All of this threatens to become embedded more deeply in the economy by worker wage demands, which are being accommodated. A more aggressive path is recommended.

|

Futures markets in food and energy prices suggest relief in the months ahead. Level changes in the prices of many products are starting to settle. Strong labor market conditions are luring workers back into the employment markets. Savings levels among lower income households are down, which should presage heightened price consciousness. The strong dollar is providing a check on import prices.

|

One of the more interesting byproducts of the upcoming FOMC meeting will be the updated set of projections. In March, the median forecast anticipated inflation of 2.7% for 2023 and 2.4% for 2024. Will the group give credit to some of the initial signs of retreat?

Employment

The Fed has two mandates: maximum employment and stable prices. The rapid recovery in employment has allowed FOMC members to focus their attention on inflation. But at times, these two objectives can be in conflict with each other. The hot job market is offering great opportunities for workers to advance, but competition for scarce labor is driving up inflation. And the consequences of a mistake in either aspect are difficult to compare. High inflation is a sufferable burden on all consumers, while unemployment is a major disruption for a subset of workers.

|

More Hawkish

|

Less Hawkish

|

|

Wage gains have exceeded 5% year over year every month this year; in the prior cycle, earnings never grew by more than 3.5%. Fast wage growth risks a wage-price spiral, which will make inflation a long-running challenge. Meanwhile, with nearly twice as many job openings as unemployed workers, there is nothing left for the Fed to do to stimulate labor demand. Workers must overcome individual circumstances like childcare and long COVID.

|

In the later years of the growth cycle through 2019, Fed leaders were proud of the “broad based and inclusive” recovery. The racial gap in unemployment rates narrowed, and discouraged workers were able to find employment. The goal of an inclusive growth cycle remains. In this iteration, the lowest earners have seen the greatest wage gains and improvements to their household balance sheets.

|

The Fed’s tightening posture will be tested when labor demand slows. Lower job openings and slower turnover would suggest a soft landing is underway, while a rise in jobless claims and the unemployment rate could signal the start of a recession. Thus far, no distress signals are evident.

International Factors

The challenges facing the U.S. will sound familiar around the world, with most economies reckoning with higher prices and underperforming equity markets. The Federal Reserve is a national institution with a mandate that is domestically bound. However, tackling the highest inflation the United States has seen in decades raises the risk of repeating the so-called Volcker shock, as higher U.S. interest rates spread to all markets.

|

More Hawkish

|

Less Hawkish

|

|

The current account position of most emerging markets (EMs) looks more comfortable in this tightening cycle compared to history. Central banks have adequate currency reserves. Plus, higher commodity prices are only going to boost the position of exporters. EM central banks are further along in their tightening cycles than the Fed and other major central banks, implying already higher real interest rates.

|

COVID-19 has wreaked havoc on EM public finances. An aggressive tightening will further encourage capital flight, raise the rates on sovereign debt and destabilize currencies. Purchasing power will fall, and the cost of servicing dollar-denominated debt will increase. According to the International Monetary Fund, about 60% of low-income developing economies are either already experiencing debt distress or are close to it.

|

In 2013, the mere hint that rate increases were on the horizon sent several EMs into a tailspin. The Fed's aggressive rate hikes in the 1980s helped tame inflation in the U.S., but pushed global interest rates higher and drove numerous developing economies to default on their obligations. Big emerging economies have, thus far, avoided a repeat of the tantrums and turbulence of the past. This should allow the Fed to remain focused on fulfilling its domestic mandate.

Financial Conditions

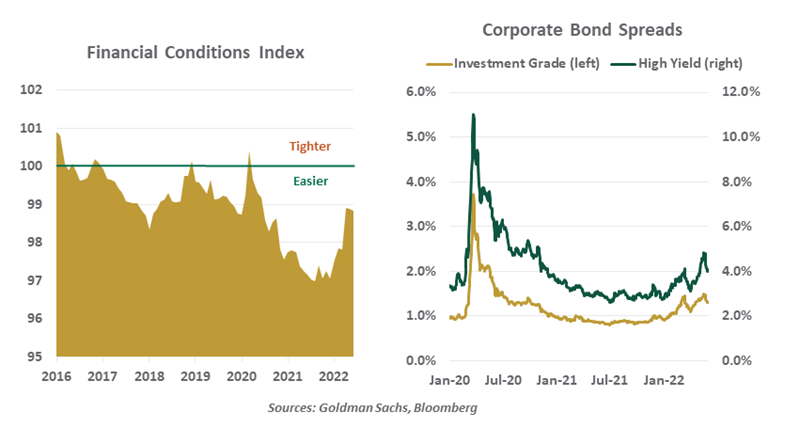

Financial conditions capture the ease with which capital can be accessed. Measures of financial conditions include bank lending activity, credit spreads, market levels and volatility.

The Federal Reserve’s actions work, in part, by influencing financial conditions. Their words and deeds lead to easing and tightening almost interactively. Policy normalization seeks to steer conditions to be more restrictive, but not overly so.

|

More Hawkish

|

Less Hawkish

|

|

Financial conditions are not as easy as they were at the beginning of the year, but they are still on the easy side of neutral. Credit spreads widened in May, but have retreated in June. Lending standards are still accommodative. Equity market declines should not be cause for changes to monetary policy.

|

Conditions have shifted substantially in the past month, and threaten to overcorrect. Measures of both stock and bond volatility have crested, suggesting that markets are concerned that the Fed may end up going too far. Policy will have to proceed with extreme caution as we move through the year.

|

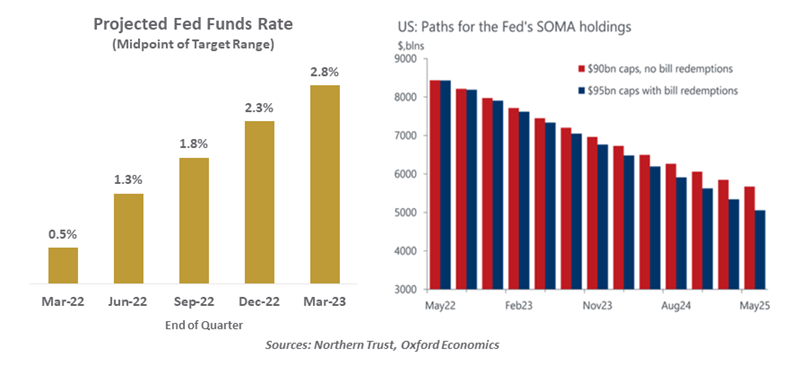

Shifting conditions led us to update our expectations for the Fed frequently during the first four months of the year. But we are quite comfortable with our current forecast. We expect overnight interest rates to peak at around 3% by the early part of next year; two more 50 basis point hikes will be followed by a series of quarter-point moves. As announced, the Federal Reserve’s balance sheet is on track to decline by almost $2 trillion over the next two years.

As noted earlier, we’ll get an updated set of projections from the FOMC on Wednesday afternoon. The dispersion of interest rate expectations in the “dot chart” has been exceptionally wide, suggesting that members have different views of how much restraint will be required to bring inflation to heel.

Chair Powell will have to continue his firm communication. His guidance has been quite good this year, but he’ll need to remain adroit in front of the microphone. Markets are clearly edgy as they adjust to policy that is less supportive. If Powell can engineer a soft landing after helping to manage through the pandemic, a spot on the Federal Reserve’s Mount Rushmore may be in order.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust