We enter the summer seeking relief from a challenging spring. The past several months have witnessed a bear market, rapid central bank tightening, continued supply chain pressures and an ongoing war in Ukraine.

The key issue in the outlook remains inflation and the Federal Reserve’s reaction to it. Increases in the price level continue to exceed expectations, and the outlook for monetary policy continues to be more hawkish. Prospects for a soft landing are diminishing.

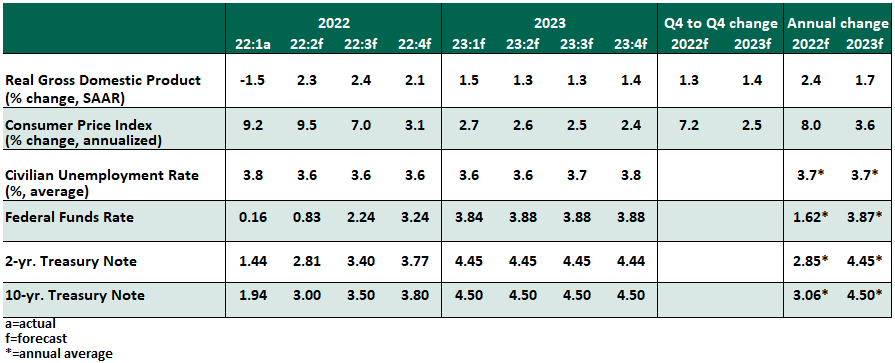

Fear of recession is on the rise in both formal surveys and anecdotal observations. Spending power has diminished somewhat, as wage gains have not kept pace with prices. A review of the data shows that the economy continues to function well, but we have reduced our estimates of growth through the end of 2023. Our outlook does not feature a recession, but the risks of that outcome are rising.

Key Economic Indicators

Influences on the Forecast

- Inflation for May was still exceedingly high, with the consumer price index registering a gain of 8.6% from a year before. Nearly all sectors showed price gains from April; supply chain dislocations and labor shortages are apparent across a range of categories. Travel costs (for airfare and gasoline) are jumping as Americans are enjoying their first COVID-light summer in three years.

There are certainly reasons to think that inflation will cool. Demand destruction from higher prices is inevitable, markets expect energy and food prices to level off and higher interest rates will take a toll on activity. But the persistence of inflation has caught most forecasters by surprise.

- The May employment report continued a long-running favorable streak, with 390,000 jobs created. Payrolls are now less than one million jobs shy of their February 2020 peak; at this time two years ago, the gap was over 19 million. The unemployment rate held at 3.6% as more people returned to the workforce.

- As of April, the number of job openings was estimated to be 11.4 million, a slight decline from March but still almost double the estimate of six million unemployed workers. Quit rates remain elevated while layoffs are rare, showing workers still have confidence and leverage. The vision for a soft landing will feature the economy slowing down enough to reduce this excess demand for labor, but not so much as to cause significant layoffs.

- The Federal Reserve raised its overnight rates by 75 basis points at its June meeting, and the median outlook among the participants calls for interest rates to close the year at around 3.5%. While there are many ways to get there, we expect the Fed to raise rates by 75 basis points next month and by 50 basis points each in September and November. As long as inflation is elevated and unemployment is low, the strategy of front-loading rate hikes is appropriate. Combined with balance sheet reduction, financial conditions are set to tighten in the coming months.

- Interest rates on new 30-year fixed rate mortgages have settled at around 5.5% over the past month, a rapid rise after starting the year closer to 3%. Higher interest costs are reducing affordability, contributing to a slowdown in housing markets; mortgage applications for purchases have reached a post-pandemic low. However, constrained inventories are keeping prices firm, with the Federal Housing Finance Agency reporting an increase of 19% nationwide through March. A cooler housing sector will be a welcome return to normal.

- The automotive market remains slow as vehicle supplies remain disrupted. Domestic auto inventories are down over 90% from their 2017 levels and have not yet shown growth this year. Limited availability pushed vehicle sales in May down to an annualized rate of 12.8 million, far shy of the pre-pandemic norm of over 17 million. Pent-up demand for new vehicles as production gets back on track will support growth in the year ahead.

- The effects of stimulus paid through 2021 are dwindling. Talks have resumed of one more spending package before the Democratic party is likely to lose control of at least one chamber of Congress in November’s midterm elections. The scope of any bill will be limited, with little direct support to consumers and high suspicion of any potential inflationary pressure.

© Northern Trust

Read more commentaries by Northern Trust