Environmental, Social and Governance-based (ESG) investing has become a significant force in financial markets. The aim of the movement is to promote good works and good values while earning good returns.

The War in Ukraine has initiated an interesting set of discussions around ESG portfolio construction. Reconciling the goals of E, S and G has become more complicated in the wake of Russia’s aggression. As a consequence, investment design and global policy objectives are both working through healthy introspection.

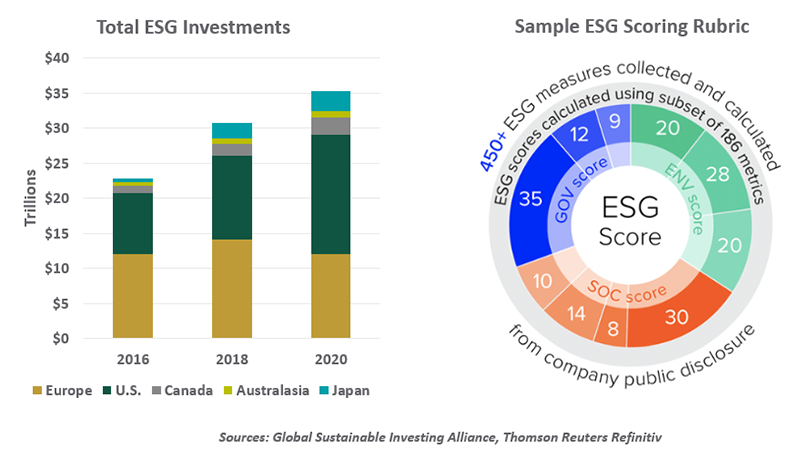

ESG-style investing has been around for more than 50 years. At inception, some asset owners sought to remove support for industries like tobacco or for regimes which practiced apartheid. Decisions were binary: specific holdings were either allowed or prohibited. Today, assets managed using ESG principles total more than $35 trillion, and ESG products come in a wide array of styles.

Environmental factors in the ESG rubric include the contribution a company or government makes to the quality of air, water and soil around the world. The consequences of climate change are included under this heading.

Social considerations include a firm’s or government’s approaches to human rights, labor laws, supply chain standards, societal equity and other public policy concerns.

Governance factors encompass the manner in which firms or governments balance the interests of stakeholders. Clear rules or principles defining rights, responsibilities and expectations that balance competing interests are essential on this front.

What sounds simple on the surface is intricate to administer. Determining which investments have the desired qualities in proper measure requires sophisticated scoring algorithms. Prompted by stakeholders and supervisors, firms are providing expanded sets of ESG information that can be used in these assessments. The data, and the conclusions drawn from it, are under increasing scrutiny: “greenwashing” has been in the headlines more frequently of late.

Environmental considerations for investors have been advancing significantly over the past decade, in concert with rising temperatures and sea levels. Global policymakers have struggled to plot a course to a greener future, but portfolio managers have pressed ahead with efforts to contain carbon.

Determining the most sustainable sources of energy is not straightforward. Taking power generation as an example, the use of coal and natural gas has direct consequences for the environment. The carbon footprint of solar panels is more subtle: mining raw materials requires energy, fabrication releases pollutants and the finished products often require lengthy trips on container ships (which use a lot of fuel). Over the long term, solar energy is cleaner, but it is not completely clean.

|

The war has made reconciling E, S, and G even harder.

|

When social and governance considerations are brought into the equation, it becomes more complicated. Some of the raw materials used to make solar panels come from parts of the world which do not have the best records of dealing with stakeholders. ESG investors are continually confronted with tradeoffs that require careful balancing.

The War in Ukraine has made the calculus considerably more complicated. Russia’s aggression has earned a failing grade on social and governance scales, prompting western authorities to enact punitive sanctions. Prompted by their stakeholders, a range of private companies have distanced themselves from Russia. As part of this effort, energy imports from Russia are being wound down.

Energy is a basic human need, and Russian supplies will need to be replaced. Some in Europe are proposing that ESG principles be used to promote an aggressive movement to alternative energy sources, but this would be an expensive transition that cannot be completed in just a few months. The search for alternative sources of fossil fuel has prompted conversations with producers whose social and governance scores are far from perfect. Europe is also considering continuing its use of nuclear power for a time, counter to the dictates of ESG.

Even in the absence of the war, a successful long-term transition to more sustainable energy sources involves reliance on fossil fuels for many years to come. Investments will be required to sustain those supplies and keep their prices reasonable.

On another front, companies that produce munitions are often screened out of ESG portfolios, but that posture is being questioned in places where security can no longer be taken for granted. NATO is about to get two new members, who will have to spend 2% of their annual gross domestic product on defense. Should investors discourage them from doing so? Without a basic sense of security, populations are less likely to strive for the higher-order ideals embodied in ESG principles.

Eighty years ago, the psychologist Abraham Maslow described a hierarchy of needs that human beings pursue. Basic things like food and shelter are at the bottom, while a sense of personal self-fulfillment is at the top. The system was shaped like a pyramid, implying that higher-level goals cannot be attained without first satisfying essential requirements.

|

ESG remains a powerful force, but it must adapt to evolving circumstances.

|

Populations struggling with security threats and immediate physiological needs are not able to focus on higher-level aspirations. In the wake of the war, the imperative of securing sufficient supplies of food and fuel at reasonable costs may defer progress on ESG fronts.

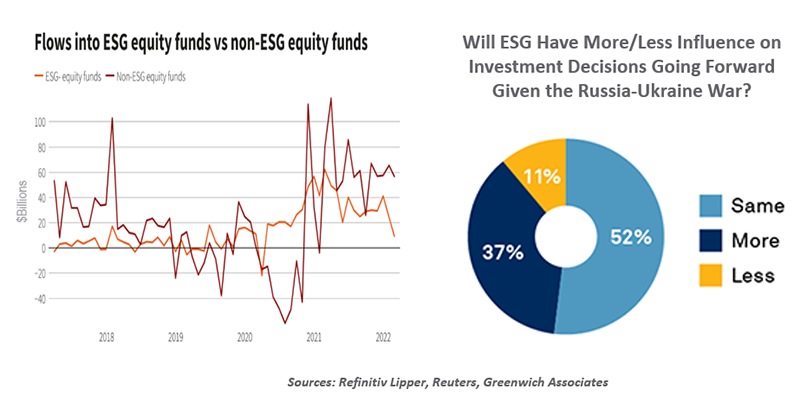

Questions surrounding sustainable investing recently led the Chief Investment Officer of the California Public Employees' Retirement System (CALPERS) to say “it’s time for RIP ESG.” This seems harsh. The recent underperformance of ESG funds will likely reverse as energy prices recede, and the potential for sustainable investments to create long-term value (financial and intrinsic) remains substantial. A recent Greenwich poll showed that ESG considerations will have more influence in the wake of the Ukraine war, not less.

In a literal sense, sustainability requires adjusting to changing circumstances, which the war in Ukraine has produced in great measure. To sustain its mission, sustainable investing must adapt to new realities without compromising its core principles. There is still a lot of good work to be done, and a lot of good returns to be earned.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust