I had to fill up my car last week. I had been reading about pain at the pump, but experiencing it first hand was excruciating. The terminal shared a tissue instead of a receipt at the end, the better to dry my tears.

As I drove away much the poorer, I wondered why this was happening. The United States is one of the largest producers of petroleum in the world; the ability to cover our own needs has been a buffer against price shocks. (In fact, America became a net exporter of oil products in late 2019.) World supply has been roiled by the move to cut off imports from Russia, but the U.S. has not been directly affected by the ban.

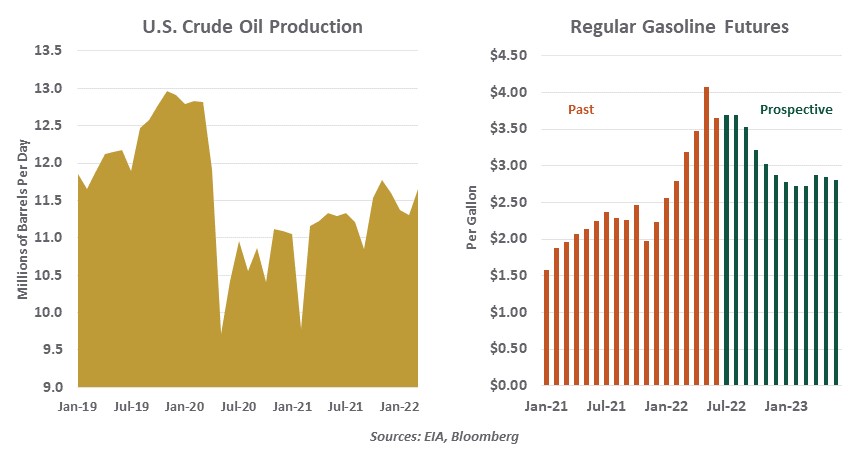

The answer to my question, as it is for so many current economic questions today, is the pandemic. Transportation was steeply curtailed during the early months of COVID-19, causing oil prices to plunge by two-thirds. This put substantial financial stress on producers; some were able to withstand the pressure, but some American firms in the sector were not. Refining has also been impaired during the past two years; capacity to turn oil into fuel is at its lowest level in eight years.

The consequent loss of U.S. refining capacity has limited output, which remains more than 10% below pre-pandemic levels. Even the lure of prices which are double what they were in late 2019 has not been enough to bring more capacity back online.

Producers in the Organization of Petroleum Exporting Countries (OPEC) have held output below potential for many months, refilling their coffers after they were depleted in 2020. It is important to note that oil prices were increasing long before the invasion of Ukraine, which confirms that the war alone does not bear much responsibility for high U.S. fuel prices. President Biden is scheduled to make a visit to the Middle East later this month in the hope of securing additional supplies.

A range of measures have been taken or contemplated to offer relief for motorists, but none will have much of an impact on gasoline prices. The Federal government is releasing about 1 million barrels of crude oil per day from its strategic petroleum reserve, which is now down to its lowest level in 35 years. Additional ethanol has been allowed in fuel formulation. A gasoline tax holiday has also been proposed. All three of these steps carry costs, and all would blunt the natural tendency of high prices to diminish demand…and thereby force prices lower.

Ironically, the threat of falling prices is one of the factors cited by American producers when asked why they haven’t ramped up production. Their significant financial losses are a vivid memory. A recent survey conducted by the Federal Reserve Bank of Dallas also cited supply chain problems, labor shortages and government regulation as primary reasons for sluggish output growth.

|

Markets are anticipating lower gasoline prices, which would reduce inflation and boost confidence.

|

On the last front, industry participants noted the Administration’s intention to address climate change through industry regulation as inhibiting their ability to bring additional crude to market. As we have written, efforts to contain carbon emissions are terribly important. But we’ll need fossil fuels throughout the transition to cleaner energy, and a modest level of investment and support will be needed for the oil industry during the interim. Striking the right balance on this front will continue to be a difficult exercise.

Despite all of these challenges, markets are expecting the price of gasoline to decline significantly in the next twelve months. Futures markets are calling for a barrel of crude oil to cost 30% less a year from now, and a gallon of regular gasoline is expected to be more than a dollar cheaper. If this comes about, it will provide significant relief from inflation. Further, inflation expectations are tied closely to energy prices, so cheaper gas would help prevent those expectations from becoming unmoored.

We’re taking a driving vacation later this summer, and I am certainly hoping that gasoline prices have eased by the time we begin. Otherwise, we’ll have to ditch admissions fees to attractions and make our own fun. A good game of hopscotch sounds nice…

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust