Today’s chronic inflation has a wide variety of causes. Attention has been rightly focused on the pandemic, supply chains and stimulus programs. But the classic theory of money-driven inflation is worth a review, especially as the money supply reaches an inflection point.

The monetary theory always carried intuitive appeal: Holding all other factors equal, an increase in the money supply makes more money available for economic activity, leading to higher prices. In the past, we have noted that the monetary relationship is no longer reliable, especially in developed markets. Structural forces like globalization and technological advancements have helped to keep inflation in check. The notion that “inflation is always and everywhere a monetary phenomenon” seemed destined for the history books.

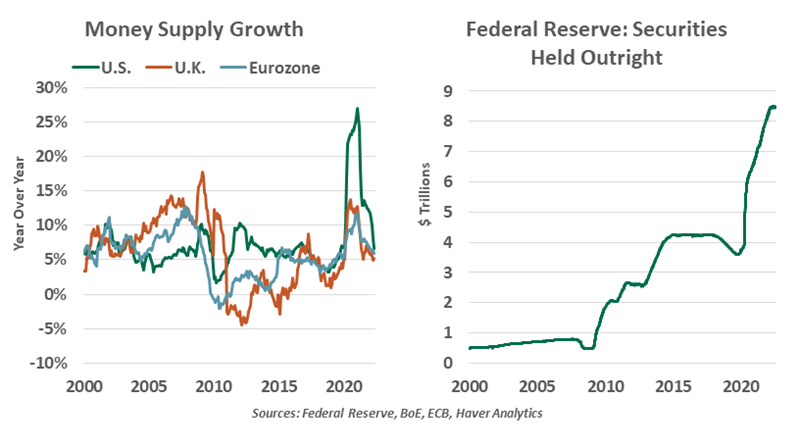

But then COVID-19 arrived. Governments launched massive stimulus programs to steer their populations safely through the pandemic. Central banks ramped up bond purchases to ensure liquidity. A financial crisis was averted as the world focused on the health risks and mitigation of COVID-19. But the surge of money in these efforts was massive. Since the COVID crisis, the money supply has grown by 40% in the U.S., 22% in the U.K. and 20% in the eurozone.

While monetarism does not fully explain inflation, a liquidity flood of that size was bound to have significant ripple effects, appearing with long and variable lags. At first, the additional funds prompted little activity. Monetary velocity (the ratio of gross domestic product to money supply) dropped across economies, as activity slowed while money grew. But as consumer spending and bank lending recovered, demand moved far above supply, elevating prices.

Now, the printing presses have slowed. The U.S. money supply (M2) peaked in March and has since held nearly flat. On a year over year basis, growth rates are returning to their pre-crisis norms across economies. This is an important omen as we hope to see an end to high inflation. As money growth retreats, less funding will be available to keep demand at the high level that spurred inflation, though it will be a gradual disinflationary force.

Slower money growth bodes well for slower inflation to follow.

A return to normal money growth would be fine, but monetarism is now poised for a new test in the U.S.: How will the economy react to a decline in the money supply? The U.S. has never seen a sustained decline in money in its modern history, but one may begin soon. The Federal Reserve began reducing its portfolio in June and expects to withdraw more than $1 trillion in liquidity from the financial system over the next year.

The Fed has engaged in quantitative tightening only once before, starting in 2017. The program ceased after two years and about $700 billion of runoff, from a starting point of $4.5 trillion. One of the signals to stop was stress in overnight repurchase markets, suggesting banks were running short of liquidity. The Fed has not set an end point for the current round of tightening, but overnight reverse repurchase markets suggest at least $2 trillion of excess liquidity can be cleaned up, which would be a significant curtailment.

Central bank assets are a component of the monetary base, the foundation for financial transactions. A more flush financial system has greater capacity to issue loans, generating new money. As central bank holdings decline, the ability for money to grow will be constrained. Should this become a source of stress, though, the Fed has proven itself responsive and can alter the course of tightening, or halt the plan altogether.

Inflation is an economic malady with a long history. The old-fashioned cure of slower money growth may be just what the doctor ordered.

© Northern Trust

Read more commentaries by Northern Trust