For years, I have been known as the reverse indicator. The more certain that I am that something is going to happen, the more likely the opposite will occur. This does nothing for my self-esteem, but I am consistent…and clients who pick up on the signaling have made a lot of money during my career.

A variant of my curse extends to travel. Statistically speaking, my flights are more likely to be delayed and my seats are more likely to be situated next to a screaming child. Once on the ground, the dollar is almost guaranteed to be weak against the home currency of any foreign country I am visiting.

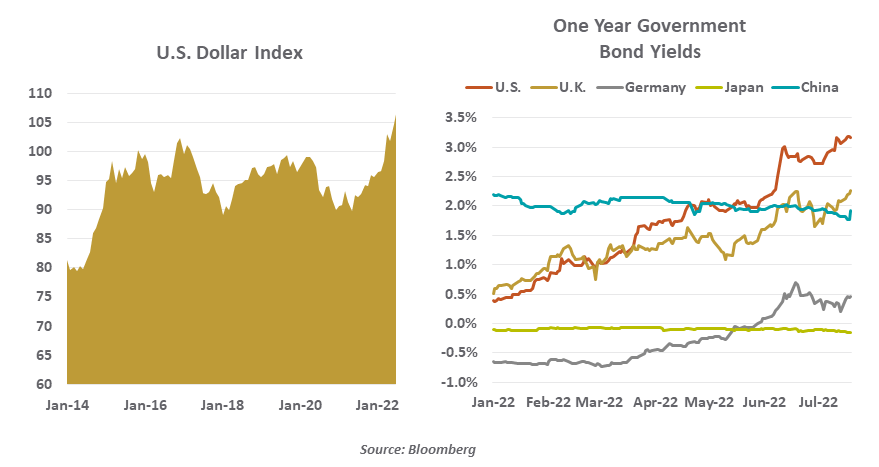

On that latter front, my losing streak has come to an end…in a big way. The American dollar has been soaring in value over the past few months, briefly passing parity against the euro earlier this month. But while this trend has been good for me personally, it has introduced considerable discomfort elsewhere.

The United States is a country with 9% inflation, rising risk of recession, a massive trade deficit, substantial political strife, flagging stock markets, and national debt that is equal to 100% of gross domestic product (GDP). That would normally be the formula for currency depreciation, not near-record strength.

The conundrum is resolved with the following observation: currencies are graded on a curve. They have value relative to one another, not on an absolute scale. While America is hardly in an ideal economic place, other countries are faring even more poorly. Inflation and recession risk are higher in Europe; activity in China has been limited by their zero-COVID policy; and the war in Ukraine has prompted a rush to safety among global investors. U.S.-dollar based assets remain the world’s leading safe haven.

On that latter front, the U.S. has become even more attractive. For many years, international investors paid a price for parking their funds here: short-term American interest rates have been anchored near zero for most of the past fifteen years. But U.S. yields have broken away from the lower bound in a substantial way. Overnight interest rates will likely be 2.5% by the end of July, and are heading even higher from there. Yields on American government bonds are now well in excess of those available in other developed markets.

|

Rising interest rate differentials explain the dollar’s popularity.

|

In general, a country which runs a very deep merchandise trade deficit will have a weak currency. Imports must be paid for in the currency of your counterparty; the higher those imports are, the higher the demand for foreign currencies relative to one’s own.

In the U.S., capital flows and not trade flows are the dominant influence on the currency. Foreign investors seeking the yield and stability of American investments trade their currencies for the dollar. This is the main reason why the U.S. dollar is so strong at the moment, in spite of fundamentals which might suggest otherwise.

Beyond the micro effect of helping American travelers afford morning coffee overseas, the strong dollar will have a series of more important macro impacts. Among them:

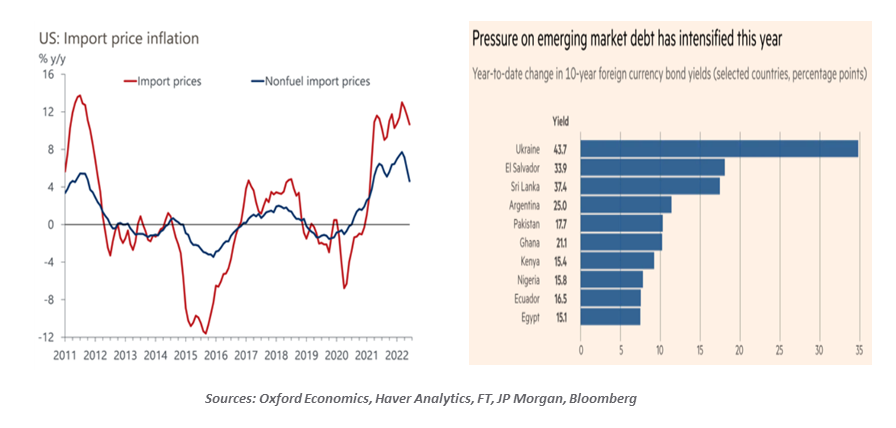

- The cost of U.S. imports is moderating. The purchasing power of the dollar has improved on global markets, bringing down inflation on products sourced from overseas. The flip side of this, however, is that American exports are becoming more expensive, creating additional inflation in other countries.

The combination of these factors has served to deepen the U.S. trade deficit, which is now approaching 5% of GDP. This serves as a drag on American economic growth, and is one reason why the U.S. experienced a contraction in the first quarter of the year.

- U. S. yields have surpassed levels seen in some of the large emerging markets, China among them. This has prompted some capital flows out of those markets to the U.S., producing declines in a range of world currencies. Central banks in smaller markets seeking to preserve inbound foreign investment have been forced to raise their interest rates, even as their economies are struggling. This has increased the risks of financial and civic upheaval in several nations.

The dollar is the currency of choice for transactions in oil markets. The appreciation of the dollar has therefore added to the high cost of crude and made petroleum imports much more expensive. To pay for the energy they need, small countries are forced to deplete their reserves of dollars. This was one of the ingredients in the recent trouble in Sri Lanka, where the government fell and the nation defaulted on its debt. There may be similar situations in other emerging markets which could come to the surface in the months ahead.

- American companies earning profits in non-U.S. markets will see the value of those earnings diminished upon consolidation. Almost 40 percent of the market-weighted sales of the S&P 500 are international. While many large firms maintain sophisticated currency hedging programs, the speed with which the dollar has advanced may have revealed residual risk. And smaller companies without such programs will see their incomes diminished by trends in exchange rates.

|

The strong dollar is a significant problem for many emerging markets.

|

Exchange rates are often changeable, so the dollar’s recent strength may turn out to be transitory. The euro, in particular, regained ground this week as the European Central Bank announced a 50 basis point increase in interest rates. Other moves may certainly follow elsewhere.

And if the United States experiences a recession, the Federal Reserve may be forced to back off a bit, bringing U.S. interest rates into closer alignment with foreign alternatives. This would diminish the volume of capital flows which have been washing up on American shores.

I have several international trips coming up, so I am hoping the dollar holds its value for a little while longer. But this may not be sufficient compensation for the airport dysfunction that the world has been dealing with in recent months. If my usual (bad) luck returns and my luggage goes missing during my next voyage, at least I’ll be able to afford fresh clothes and a new suitcase.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust