Americans Still Plan To Travel This Summer, “No Matter What”

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs of last month, the U.S. jobs market fully recouped the number of jobs that were lost due to the pandemic, in less than half the time it took following the previous downturn. A stunning 528,000 jobs were added in July, pushing the total number of payrolls above the February 2020 level.

Good news may be bad news in this case, however, as the blockbuster jobs report may prompt the Federal Reserve to tighten more aggressively than planned to cool growth. This could decisively trigger the recession many market-watchers believe we’ve already entered, with real gross domestic product (GDP) having shrunk for two consecutive quarters, inflation standing at near-historic highs and a service sector in contraction.

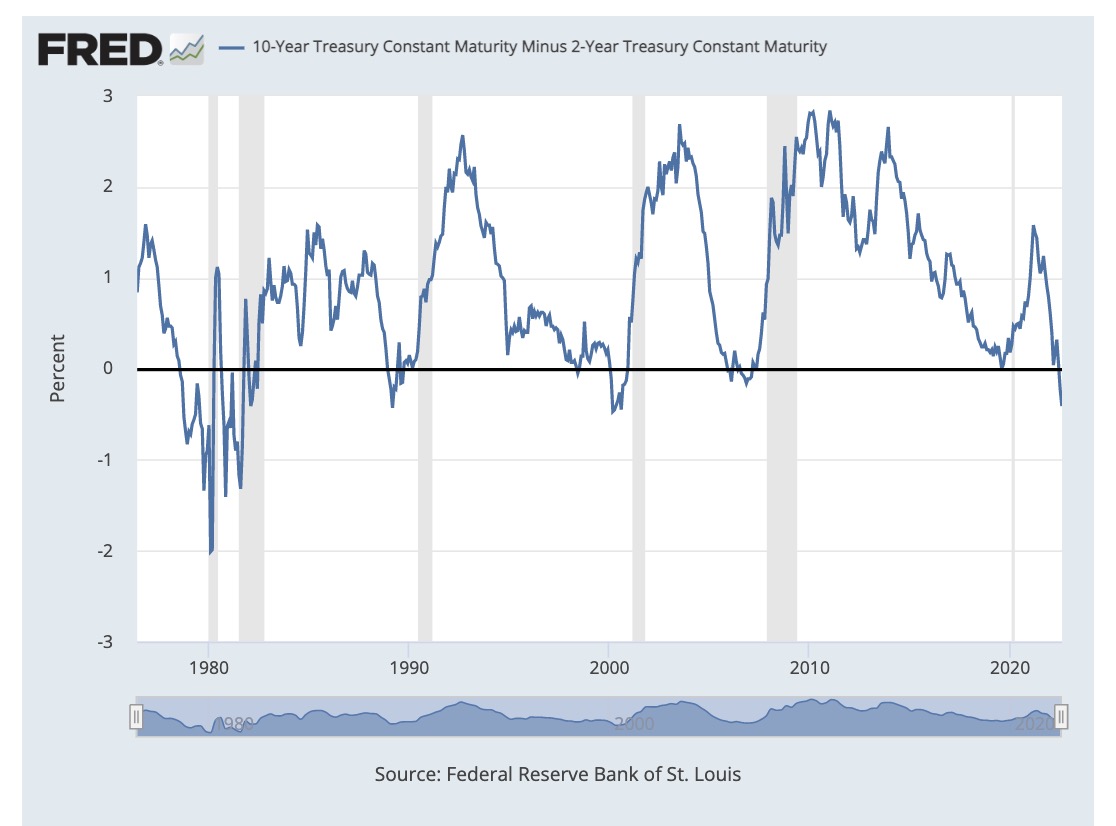

In addition, U.S. yields have inverted at the deepest level since 2000. On Thursday, the yield on the two-year government note closed at 3.03%, the 10-year at 2.68%, a difference of 35 basis points. Every recession in the past several decades has been preceded by a yield curve inversion, so we may be in the very late stages of the business cycle.

It will be interesting to see what Jay Powell & Co. decide to do at the next Federal Open Market Committee (FOMC) meeting, scheduled for September 20-21.

Americans Are Cutting Back On Driving, But Lower Fuel Costs Could Be A Game-Changer

Another sign that parts of the economy may be slowing? Lower fuel demand coupled with falling gas prices. Energy Information Administration (EIA) data shows that this summer, Americans are consuming less gasoline per day than they did in the summer of 2020, when nearly everyone was stuck in their homes bingeing Tiger King on Netflix.

Gas prices above $5 per gallon, it seems, are a greater deterrent to venturing outside your house than Covid fears and government-mandated lockdowns were.

The decrease in driving activity is in line with the results of a recent survey conducted by the American Automobile Association (AAA). The nonprofit found that a whopping 88% of Americans were driving less due to higher gas prices. Three quarters of respondents said they were combining errands, while 56% said they were reducing shopping and dining out.

Interestingly, only 13% of people who took the survey said they were driving a more fuel-efficient vehicle in response to soaring gas prices; virtually no one, or 2% of respondents, said they were switching to an electric vehicle (EV).

The EIA will report this week’s fuel consumption numbers next Wednesday, and I expect to see that demand has jumped back above 2020 levels now that gas prices have fallen for more than 50 straight days after peaking at an all-time national average high of $5.02 on June 14.

For Many Americans, Vacations Will Happen “No Matter What”

Another recent survey, this one conducted by McKinsey & Co., shows that many Americans are still planning a vacation this summer “no matter what,” even as inflation remains a top concern. Nearly 70% of respondents said they were taking a trip regardless of rising prices, Covid, a potential economic slowdown or other worries.

This positive sentiment was echoed by Booking Holdings CEO Glenn Fogel, who told CNBC this week that Americans are “going to keep on traveling and they are going to travel more and more over the long run.”

Fogel joined the network to discuss Booking’s incredible second-quarter financial report. The online travel agency, which owns well-known brands such as Priceline, Kayak and OpenTable, recorded more room night bookings in the three months ended June 20 than in any quarter in 2019, before the pandemic. Total revenues were $4.3 billion, nearly double what they were in the previous quarter, while net income was $857 million, compared to a net loss in the same quarter last year.

Looking ahead, Fogel expects record revenue in the third quarter, and bookings for the final quarter of the year are currently about 15% ahead of the same period in 2019.

We’re bullish on not just Booking but also rivals Tripadvisor and Expedia, shares of which have recovered their loses, and then some, as gas prices have retreated from all-time highs on June 14.

Shipping Giant Maersk Posts Record Results

Besides consumers, lower gas costs are beneficial to industries that consume great amounts of petroleum liquid fuels. Those include airlines and shipping container companies, the latter of which is still seeing worsening congestion at ports in North America, Europe and China, according to shipping giant A.P. Moller-Maersk.

The world’s second-largest shipping company is often seen as a barometer of the global shipping industry, and if that’s the case, Maersk’s second-quarter results should put investors’ minds at ease. The Copenhagen-based company reported record revenue of $21.7 billion in the June quarter and a net profit of $8.6 billion, also a new quarterly record.

Based on these impressive results, Maersk is raising its guidance for the full year, from $30 billion EBITDA (earnings before interest, taxes, depreciation and amortization) to $37 billion. It’s also raised its free cash flow (FCF) estimate from $19 billion to “above” $24 billion. Maersk’s Board of Directors is also increasing the company’s share buyback program to $3 billion for the years 2022-2025, up from $2.5 billion earlier.

Some financial news outlets have drawn attention to the fact that Maersk moved 7.4% fewer containers in the second quarter compared to the same quarter last year, but as the company itself points out, this is due to the increasing port congestion, not a meaningfully slowdown in demand. According to the Census Bureau, new orders for manufactured durable goods rose to $272.6 billion in June, a 2% increase from May. Shipments of manufactured goods have also been up 13 of the last 14 months as of June.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.13%. The S&P 500 Stock Index rose 0.36%, while the Nasdaq Composite climbed 2.15%. The Russell 2000 small capitalization index gained 1.94% this week.

- The Hang Seng Composite gained 0.02% this week; while Taiwan was up 0.24% and the KOSPI rose 1.60%.

- The 10-year Treasury bond yield rose 17 basis points to 2.825%.

Airline Sector

Strengths

- The best performing airline stock for the week was Bombardier, up 32.0%. SkyWest’s second quarter earnings per share (EPS) of $1.07 impressively beat consensus of $0.44. Earnings came in on better production (due to significantly improved operational performance, optimized schedules by aircraft, and some improvement in pilot attrition rates) along with strong demand/yields in the Prorate segment.

- Singapore Airlines released its 2022 first quarter figures this week, with a quarterly profit of $556 million, now one of the best operating profits in the history of the company’s operations. The first quarter’s profit has already met the full-year consensus profit estimate, despite high fuel costs during the quarter. Singapore Airlines’ solid beat showcases pricing power and market share gains helped by its above-peer network expansion.

- International Airlines Group (IAG) reported passenger unit revenues 6% higher than the second quarter of 2019, driven by long-haul premium leisure with the yield environment making up for load factors still lagging slightly behind 2019. Given the demand outlook for peak summer, that is a 6% increase in the third quarter versus the second quarter. The outlook is especially encouraging given a slowdown in short-haul bookings in the last few weeks as British Airways deals with the recent capacity cuts put in place by Heathrow.

Weaknesses

- The worst performing airline stock for the week was Allegiant, down 4.4%. Airbus cut 2022 deliveries to 700 jets from 720 and pushed its production target of 65 A320s per month to early 2024 instead of summer 2023. Similarly, Boeing, citing supply chain disruptions, slowness of taking airplanes out of storage, and timing of deliveries to Chinese customers, lowered 737 deliveries to the low 400s for 2022 versus 500 at the beginning of the year.

- Southwest Airlines announced that future travel credits will no longer have expiration dates. During the pandemic, the company issued nearly $1.1 billion of travel credits due to canceled flights that were set to expire this September. As such, the company had been recording higher-than-normal levels of breakage revenues up until this point, resulting in higher top-line results than would be seen under more normal conditions. With the move to no expiration date, these higher breakage levels will likely come down, and the airline now bases its future revenue trajectory off of this lower base.

- JetBlue recorded second quarter revenue up 16.1% and at the high end of the guidance range. However, this was not enough to overcome much higher operating expenses. The carrier’s realized fuel price in the second quarter was $4.24 per gallon, while spending on salaries and wages came in slightly below $700 million. The carrier will be constraining capacity for the remainder of 2022 like its competitors. Third quarter capacity is expected to be flat to down 3% 2022/2019 with full year 2022 capacity flat to up 3% 2022/2019.

Opportunities

- JetBlue unveiled a new cost savings program with run-rate savings of $150-$200 million and $75 million of cost reduction in 2024. This consists of spending on things like network efficiency, crew planning, and maximizing asset productivity. While this supports a flattish CASM-ex trajectory, the cost plan does not include potential labor deals and comes with execution risk as management also focuses on the Spirit transaction.

- According to Morgan Stanley, Boeing received preliminary U.S. regulatory clearance to restart deliveries of its 787 Dreamliner aircraft as the Federal Aviation Administration approved Boeing’s plans to inspect and repair tiny manufacturing flaws in the Dreamliner’s carbon-composite frame. This is a major milestone for the business and unlocks another level for free cash flow generation as 787 inventory stands at 120 aircraft, which may provide $17 billion of revenue.

- According to Raymond James, American Airlines’ gambit to stabilize pilot attrition at its regional subsidiaries may pay off in the near term. This would happen by helping to grab share in lucrative feeder markets where American noted it is seeing yields that are 25% greater than the rest of the system in the second quarter. While the group remains concerned about the long-term implications, network decisions among competitors that reduce service in these markets could help offset cost headwinds.

Threats

- According to JPMorgan, Spirit Airlines’ results merely being added to those of JetBlue’s should exceed those of stand-alone JetBlue. But then, year two sets in. This is the year in which labor costs inflate. Spirit pilots alone are set to receive an approximate 12% wage increase, and that’s before factoring in a secondary bump for the pro forma pilot group given the merger’s negative impact on seniority. Then come flight attendants and mechanics. Year two is also the year where cabin configuration begins, basically the de-densification of Spirit aircraft, which applies meaningful upward CASM pressure. On balance, Spirit’s configuration is 20% denser.

- Airbus and Boeing are likely to keep a cap on 2023 capacity. Notably, Boeing echoed commentary by GE last week that it may take supply chains 18 months to catch up with OEM production. Separately, production rates at Airbus are unchanged, while Boeing’s 787 deliveries should resume as early as the week of August 8 given reports indicating the FAA signed off on Boeing’s plan.

- Pilots at German flagship carrier Lufthansa voted on Sunday by a margin of 97.6% in favor of industrial action, threatening further disruption during the busy summer travel season. Strikes and staff shortages have already forced airlines including Lufthansa to cancel thousands of flights and have caused hours-long queues at major airports, frustrating holidaymakers keen to travel after Covid-19 lockdowns. The vote does not necessarily mean a strike will be held, but it was a signal to the employer that constructive steps needed to be taken.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 6.5%. The best performing country in Asia this week was Thailand, gaining 4.5%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 2.4%. The Pakistani rupee was the best performing currency in Asia this week, gaining 6.4%.

- China’s Caixin Service PMI surprised to the upside. July Service PMI was reported at 55.5 versus 53.9 expected by Bloomberg economists.

Weaknesses

- The worst performing country in Asia this week was China, losing 1.0%.

- The Indonesia rupiah was the worst performing currency in Asia this week, losing 0.70%.

- Inflation in Turkey increased by 79.6% year-over-year in July, above June’s 78.62% but below the expected 80.24%. Core inflation spiked 61.69% on a year-over-year basis. Turkey’s inflation runs much higher than global inflation.

Opportunities

- Stock market models from Wood & Company (a broker focusing on central emerging Europe) signal that we are close to the bottom for equity markets. Foreign direct investment is showing healthy net inflows across central emerging Europe, and inflows are also improving in the Eurozone. Greece is posting stellar performance, with net inflows of 3.3% of GDP, while Italy and France are also showing net inflows for the first time in a long time, Jarek Tomczysnki said this week.

- Russian President Vladimir Putin is meeting his Turkish counterpart Recep Tayyip Erdogan on Friday in the Russian resort town of Sochi. The two leaders are set to discuss military invasions. Putin and Erdogan last met less than three weeks ago in the Iranian capital, Tehran. Despite their differences over the war in Ukraine (Turkey is a major arms supplier to Kyiv), their countries have made diplomatic agreements. Small steps with the help of Turkey may bring Russia and Ukraine closer to peace agreement discussions.

- Hong Kong may announce a reduction in the amount of time international travelers need to spend in mandatory hotel quarantine as soon as Monday. Officials had anticipated making an announcement on Friday, but it has been pushed back to Monday. In addition, China reopened its border with Macau this week and resumed quarantine-free travel after a drop in Covid cases.

Threats

- It seems nobody is brave enough to tell Russian president Putin the truth that he is losing the battle in Ukraine. Ukrainian forces are trying to push back the Russian army on the south, retaking as much land as possible from the occupant. Russia is preparing to annex the east part of Ukraine within months, but the battle for the economically important land in the south could either end very soon or last much longer.

- U.S. House Speaker Nancy Pelosi traveled to Taiwan this week while visiting other countries in Asia. She is the most senior U.S. lawmaker to visit the island since Speaker Newt Gingrich went in 1997. Her visit aggravated China, which immediately started to perform military drills around the island to show its dissatisfaction. As a form of punishment, China stopped exports of sand that Taiwan uses for construction and blocked imports of some fruits and vegetables from the island.

- This week Bloomberg reported that within emerging markets of Europe, the Czech Republic is the most vulnerable to a gas crunch in the region. On a relative basis, the country has been importing more of its gas needs from Russia and has not been able to diversify gas imports like other countries in central emerging Europe.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was zinc, up 4.81%, as Glencore warns that Europe’s energy crisis poses a substantial threat to supply. Glencore has already put one of its zinc smelters on care and maintenance as they are unprofitable to run. According to Baker Hughes, the U.S. rig count continues to grow and is now at 767, driven by expansion in the unconventional oil rig count to 551 (up seven this week). Increases were reported in the Eagle Ford to 63 and the Permian to 330.

- The U.S. became the world’s largest LNG exporter in the first half of 2022, according to the EIA. Exports averaged 11.2 Bcf/d, up 12% to the second half of 2021, with utilization of peak capacity at the seven U.S. LNG export facilities averaging 87% in the first half of 2022 (primarily before the Freeport outage), consistent with the prior year.

- Fertiglobe Plc, the largest fertilizer maker in the Middle East, says the global market will remain tight with more European rivals likely to cut production due to

surging costs for natural gas, a key feedstock. “We could see more coming offline in Europe,” Fertiglobe CEO Ahmed El-Hoshy told Bloomberg Television. “Even at today’s elevated prices for ammonia and urea, much of Europe is operating well below cash costs. Some companies will have a difficult time with these unprecedented hydrocarbon prices.”

Weaknesses

- The worst performing commodity for the week was crude oil, down 10.39%. Crude oil has reached the lowest level since before Russia’s invasion of Ukraine in February and as the market continues to worry over global economic growth slowing faster than the Fed anticipates. In practice, OPEC+’s production is lagging far behind, with the members pumping about 2.7 million barrels a day less than planned in May, the most recent month for which full production figures are available. Nearly half of the shortfall is attributable to Russia, whose crude and refined products have been shunned by some European buyers after its troops invaded Ukraine in February. Diverting exports to India has helped Russia to avoid the full impact of buying bans, but it has not been able to completely offset the loss of much of its European market.

- According to UBS, the Chile copper bill is entering the final stages of negotiations. UBS believes an outcome is unlikely to be imminent but thinks the bill could be finalized by the end 2022. The latest proposal includes two ad-Valorem sliding scale royalty/tax components that would replace the current 6-8% royalty charged on profit before tax (PBT). At $3.50 per pound, UBS estimates that the effective tax rate could increase from 35-40% currently to 44-50%, but at $4.50 per pound they estimate that the effective tax rate could increase to 55- 60%.

- Oil held its decline after closing at the lowest level in more than five months. Traders counted down to an OPEC+ meeting on supply amid signs that physical markets have eased in recent weeks. West Texas Intermediate slipped 0.2%, having lost almost 5% at the start of the week on concerns a global economic slowdown will erode energy demand.

Opportunities

- With Russian gas imports already down sharply (-35%) across the first half of the year, Norway is comfortably Europe’s No.1 gas supplier. Broad cross-party government support provides the industry a clear “license to operate.” European peers have inversely enacted windfall taxes. The European Union has indeed agreed to step up cooperation in order to ensure additional short-term and long-term gas supplies from Norway.

- JPMorgan Commodities Research has provided thoughts on the Inflation Reduction Act. Analysts flag that of the $739 billion total package, $369 billion will be spent on “energy security and climate change” programs. This includes tax credits for purchasing electric vehicles (EVs) and incentivizing domestic production of battery metals. The bank views this as incrementally positive for producers of battery metals (cobalt, lithium, and nickel) including Glencore, Anglo American, Rio Tinto, BHP, First Quantum, Antofagasta, and Lundin. However, a faster-than-expected move toward EV adoption could be negative for the outlook for platinum group metal demand.

- Global investment in renewables rose to a first half record of $226 billion as nations lift spending on cleaner fuel sources to boost energy security.

Investment was 11% higher than the same period in 2021 even as the sector handles challenges like the rising costs of solar panels and wind turbines, driven by gains in raw materials including polysilicon and steel, reports Bloomberg.

Threats

- According to JPMorgan, weaker demand is driving larger forecasted copper surpluses and risks are skewed toward even greater oversupply. With demand to decelerate sharper than the bank expects or supply to over-deliver, the group now sees copper prices eventually falling to an average of $6,500/mt in the fourth quarter of 2022 and first quarter of 2023.

- According to JPMorgan, with aluminum, a much quicker-than-expected ramp-up of Chinese supply and downgrades to its demand forecasts have significantly changed the forecasted 2022 deficit and sent 2023 into a nearly 570 kmt global surplus. While cutting into cost curves now, they think aluminum prices will likely push lower until further supply cuts potentially occur, reaching an average low of $2,250/mt over the fourth quarter of 2022 and first quarter of 2023.

- Despite the positive move in nickel price recently, JPMorgan’s underweight stance on nickel remains firm, and the bank urges investors to sell into strength. The group’s core thesis is: 1) nickel to edge lower next year due to higher-than-anticipated supply from Indonesia and weaker demand; and 2) the cost structure for nickel to possibly be structurally higher due to higher energy costs and potential levies coming from Indonesia, lowering profitability despite higher nickel prices.

Luxury Goods

Strengths

- Service PMIs in the Eurozone and China surprised to the upside this week. The Final July Service PMI for the Eurozone was reported at 51.2 versus an expected reading of 50.6. The Caixin Service PMI was reported at 55.5 versus an expected reading of 53.9. The final July S&P Global U.S. Service PMI remains below the 50 level, the mark that separates growth from contraction, but it too surprised to the upside. The U.S. Service PMI was reported at 47.3 versus 47.0 expected.

- Hermes reported strong results and sales acceleration in the second quarter versus the first quarter in all regions except Asia (ex-Japan). Deutsche Bank analyst Matt Garland commented that the most impressive was the positive sales performance in China in the first half of the year despite two months of lockdowns in the region. On the back of strong results, Deutsche Bank increased its sales forecast for full year 2022.

- The RealReal Inc., an online retailer for luxury consignment, was the best performing S&P Global Luxury stock this week, gaining 26.82%. After losing 75% year-to-date, this week the price of the stock crossed above its 50-day moving average, suggesting further upside could follow.

Weaknesses

- In the current reporting season, Gucci seems to be the weakest link among big luxury names. Sales at French luxury group Kering’s top brand Gucci rose by just 4% in the second quarter, reports Reuters. A large amount of revenue comes from its key Chinese market, which was negatively impacted by a new wave of lockdowns.

- Retail sales weakened in the Eurozone. This week Bloomberg reported June sales dropping by 1.2% month-over-month and 3.7% on a year-over-year basis.

- SJM Holdings, a Hong Kong casino and gaming stock, was the worst performing S&P Global Luxury stock this week, losing 14.06%. Shares corrected sharply on Thursday after the company announced rights issuance.

Opportunities

- Later this month, vintage luxury cars will go on sale in Monterey, California. A 1955 Ferrari is expected to sell for as much as $30 million, a 1973 Porsche Carrera RS is valued at up to $2.25 million. Every August the major auction houses auction off millions of dollars’ worth of the world’s most expensive vehicles. Bloomberg reported that this year major auction houses increased the number of cars for sale. Inflation and a bear market will not stop vintage car lovers from buying.

- On Wednesday, China reopened its border with Macau allowing tourists to travel once again. Lifting of the six-week border closure was announced after Macau was able to control its Covid outbreaks. As of Tuesday, Macau has reported no new community Covid cases for 11 consecutive days.

- Pandora is outperforming in the U.S. jewelry market, which shows no signs of slowing. Positive momentum in the brand is driven by new designs and strategy as well as backing by a former Tiffany & Co. general manager appointed this year. Pandora is also rebounding in Europe, with revived tourism as an added benefit, Bloomberg reported this week. Light exposure to China helps in the short term, although plans to rebuild the brand are due next year.

Threats

- This week CLSA published a report discussing Chinese consumers’ sentiment. The broker observed a generally weaker sentiment among middle-class consumers in June 2022 compared with last November. However, those who still have plans to purchase luxury goods are more willing to raise their spending budget than they were last November, and the trend was observed in all age groups and all income groups. According to the survey, 63% of panelists did not buy luxury goods in the past 12 months and have no plans to buy moving forward.

- New data from the World Travel and Tourism Council, collected in partnership with ForwardKeys, shows that airline bookings to the U.S. spiked by 93% since the June 12 policy change, but the incoming tourists are not spending. In 2019, international tourism directly and indirectly brought $191 billion to the American economy—a number that tumbled by 80% in 2020 and only recovered by about 1% in 2021, according to Julia Simpson, World Travel and Tourism Council president and chief executive officer. At that rate, says Simpson, tourist spending is not expected to make a full recovery until 2025.

- With most luxury companies reporting first half results, JPMorgan says it was overall a good reporting season. The bank, however, sees less visibility in the second half of 2022. JPMorgan is predicting that the Western consumer might start slowing purchases post summer and into the fourth quarter. Visibility on the Chinese recovery remains especially low in the group’s view. Buying in the United States might slow while Europe most likely will remain a strong market for luxury goods.

Blockchain And Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Flow, rising 47.93%.

- Cryptocurrency companies have committed more than $2.4 billion to sports marketing in the past 18 months, according to data compiled by Bloomberg. Binance Holdings has signed contracts with soccer icon Cristiano Ronaldo and the Africa Cup of Nations (AFCON) tournament, while Coinbase Global has struck agreements with the NBA and top star Kevin Durant. FTX in the Bahamas has arrangements with Major League Baseball and franchises ranging from the NBA’s Miami Heat to e-sports, writes Bloomberg.

- Bitcoin rose as global stocks neared a two-month high and in advance of the U.S. payrolls report. Bitcoin climbed as much as 4% to $23,422 on Friday, staying within the range of around $19,000 to $25,000 that it has held since mid-June.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Qtum, down 15.93%.

- Skeptics who are betting against MicroStrategy’s Bitcoin strategy are piling onto positions that the company’s latest rebound will flame out. A record 51% of MicroStrategy’s available shares are currently sold short, carrying a notional value of $1.35 billion, according to an article published by Bloomberg. In related news, CEO Michael Saylor announced this week that he is stepping down as CEO of MicroStrategy to focus solely on the position of Executive Chairman. The company’s president, Phong Le, will take the role from Saylor.

- Hedge fund billionaire Steve Cohen exited his investment in cryptocurrency trading startup Radkl. The quantitative crypto trading firm, which was formed last year, has already lost at least two managing directors in 2022, writes Bloomberg.

Opportunities

- Luxury fashion brand Gucci is now accepting ApeCoin payments through Bitpay at select stores in the U.S. ApeCoin is the cryptocurrency affiliated with the Bored Ape Yacht Club, an NFT created by Yuga Labs. Gucci will become the first merchant to accept ApeCoin through Bitpay, a payment service provider that has been in operation since 2011, writes Bloomberg.

- Bets in the options market suggest speculators see $25,000 as a ceiling for Bitcoin and $20,000 as a floor. This is due to a high number of outstanding call and put contracts at those strike prices, according to data compiled by CoinGlass.

- Crypto platform Voyager Digital LLC, which filed for bankruptcy protection last month, said it expects to resume user access to the app for cash withdrawals next week. The withdrawal is anticipated to start August 11 for dollar holdings only, according to an article published by Bloomberg.

Threats

- The SEC this week charged 11 individuals for their roles in creating and promoting Forsage, a fraudulent crypto pyramid and Ponzi scheme. The scheme raised more than $300 million from retail investors worldwide, including in the United States, according to the announcement on the SEC website.

- Nomad, a bridge protocol for transferring crypto tokens across different blockchains, lost close to $200 million in a security exploit on Monday. The software system was drained of funds over hours and in small batches by various accounts, blockchain data shows. The attack makes Nomad the latest bridge to suffer an exploit this year, writes Bloomberg.

- Hackers targeted the Solana ecosystem early Wednesday, with thousands of wallets affected, in the latest hit to the cryptocurrency market. A reported $5.2 million in crypto assets have been stolen so far, from more than 7,900 Solana wallets, according to blockchain forensics firm Elliptic, writes Bloomberg.

Gold Market

This week gold futures closed at $1,790.30, up $8.50 per ounce, or 0.48%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by just 0.07%. The S&P/TSX Venture Index came in up 2.81%. The U.S. Trade-Weighted Dollar rose 0.65%.

| DATE | EVENT | SURVEY | ACTUAL | PRIOR |

|---|---|---|---|---|

| Jul-31 | Caixin China PMI Mfg | 51.5 | 50.4 | 51.7 |

| Aug-1 | ISM Manufacturing | 52.0 | 52.8 | 53.0 |

| Aug-3 | Durable Goods Orders | 1.9% | 2.0% | 1.9% |

| Aug-4 | Initial Jobless Claims | 260k | 260k | 254k |

| Aug-5 | Change in Nonfarm Payrolls | 250k | 528k | 398k |

| Aug-10 | Germany CPI YoY | 7.5% | — | 7.5% |

| Aug-10 | CPI YoY | 8.7% | — | 9.1% |

| Aug-11 | Initial Jobless Claims | 265k | — | 260k |

| Aug-11 | PPI Final Demand YoY | 10.4% | — | 11.3% |

Strengths

- The best performing precious metal for the week was platinum, up 4.47% as Impala Platinum reported weaker production for the quarter. Rough diamond prices have continued their ascent, unphased by the deteriorating consumer sentiment, with Anglo American reporting realized rough prices of US$213 per carat for the first half of 2022. Although eroding disposable incomes usually catch up with diamond markets, supply disruptions from Russia have kept rough diamond customers on-edge. Anglo American has been successfully favoring “value over volume” and diamond profits have exceeded consensus estimates for the first half of the year.

- Torex Gold reported strong second quarter 2022 results this week. The company announced adjusted earnings of $0.66 per share, materially beating the consensus estimate of $0.50 per share. Pre-reported production of 123,000 ounces of silver was up approximately 10% over first-quarter output. “Our strong production, combined with ongoing discipline in cost containment, resulted in robust revenue, operating cash flow and free cash flow generation this quarter,” Torex President and CEO Jody Kuzenko said.

- Gold extended gains later in the week, reports Bloomberg, as geopolitical tensions between the U.S. and China persisted, boosting haven demand. Bullion is hovering near a four-week high as the fallout from U.S. House Speaker Nancy Pelosi’s visit to Taiwan keeps markets on edge, the article explains. The Bloomberg Dollar Spot Index was little changed after slipping earlier on Thursday.

Weaknesses

- The worst performing precious metal for the week was silver, down 1.79% and ending a two-week run with the strong jobs report on Friday. Dundee Precious Metals reported second quarter results after pre-reporting consolidated gold production of 72,900 ounces and copper production of 8.8 million pounds. Adjusted earnings per share (EPS) of $0.17 missed consensus of $0.21.

- Eldorado Gold also reported second quarter operating and financial results after pre-reporting production of 113,500 ounces. Overall, the quarter came with higher costs, resulting in a miss to consensus expectations. Production guidance of 460-490,000 ounces was maintained, with the company now expecting production in the lower half of the guidance range. Gold production, however, did see an increase of 22% from the first quarter of 2021, driven by strong production and mine development in Lamaque.

- South Africa’s Royal Bafokeng Platinum reported weaker-than-expected first half of the year results, as highlighted in the company’s recent trading statement. The company reported a 58.1% fall in half-year profit, hurt by lower metal prices and higher mining costs, writes Kitco News. Its headline earnings per share, the main profit measure in South Africa, fell to 7.67 rand in the six months to June 30, from 18.32 rand.

Opportunities

- AngloGold Ashanti was one of the stronger gold stocks on Friday after announcing they were considering selling some of their smaller assets to shift their focus to larger lower-cost operations. Attaining scale is a challenge in the gold industry. Some companies chose to grow faster through acquisitions of known assets as exploration results can be unpredictable. AngloGold had previously de-risked by selling off their South African assets but leadership at the senior level has had a reboot over the past year and we now appear to be seeing some of their strategy beginning to unfold. Management noted that those projects capable of producing 300,000 ounce per year were more their target and those projects that could maybe achieve 120,000 ounces per year were best left in the hand of a smaller company to exploit.

- Mineros SA, a long-time dividend paying gold stock, currently sporting an indicated yield of 9.92%, reported its most recent quarterly gold production of 74,062 ounces, a 10% increase from the same quarter in 2021. The company also announced that it remains on track for annual guidance. Mineros listed on the Toronto Stock Exchange in late 2021. With the latest financials filed, Mineros traded at a price-to-earnings (P/E) ratio of 4.93 and its current return on invested capital is 10.90%.

- According to the Royal Bank of Canada (RBC), Centerra Gold announced the closing of the agreement with the Kyrgyz government regarding the transfer of Kumtor. They continue to see this agreement as removing a significant overhang for Centerra shares and increasing management’s flexibility in terms of funding growth post-2024 (along with potential additional cash return, either via a buyback or higher dividends).

Threats

- JPMorgan retains an elevated concern about recessionary impacts on downstream automobile customers and light vehicle production, and therefore potential downside risks to palladium prices in the second half of 2022 and into 2023. However, upbeat commentary from global original equipment manufacturers (OEMs) so far during the second quarter mitigates some of the bank’s near-term concerns pointing to improving second half volumes underpinned by robust pent-up demand and exceptionally low vehicle inventory globally. JPMorgan thinks it is premature to turn bullish on the outlook for palladium, given risks to autos in a recession scenario.

- Royal Gold’s most recent stream,Cortez, is amongst the highest caliber assets across the entire gold sector by both scale and duration (1.1 million ounces of production at bottom quartile costs). It is in one of the best jurisdictions globally and maintains high value in a royalty market where precious metals investable opportunities are scarce. Nonetheless, the transaction is also the largest value paid for a royalty and there is material dilution to Royal Gold.

- SSR Mining had a significant EPS beat that was driven by tax accounting. EBITDA (earnings before interest, taxes, depreciation and amortization) was toward the bottom end of the consensus range despite higher sales volumes and revenue, versus consensus, as costs were also higher. Consolidated production guidance is unchanged, but management has made material upward revisions to its cost guidance for the year.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/22):

Torex Gold

Dundee Precious Metals

Eldorado Gold

Royal Bafokeng Platinum

Argonaut Gold

Royal Gold

SSR Mining

SkyWest Inc.

Singapore Airlines

Airbus

Southwest Airlines

Boeing co/The

JetBlue

American Airlines

Spirit Airlines

Anglo American Platinum

First Quantum

Lundin Gold

Booking Holdings Inc.

TripAdvisor Inc.

Expedia Group Inc.

AP Moller-Maersk A/S

Hermes International

KeringSA

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg Dollar Spot Index tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar.

The Caixin China Manufacturing PMI (Purchasing Managers’ Index) is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 private manufacturing sector companies.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All