As we rounded out 2021, we offered a detailed review of the labor market recovery. In past recessions, jobs were destroyed and regained slowly, with sidelined workers standing ready to take them. In the COVID recovery, after an immediate and severe disruption, jobs were created faster than workers were able to fill them. This has led to economic stress and contributed to excessive inflation.

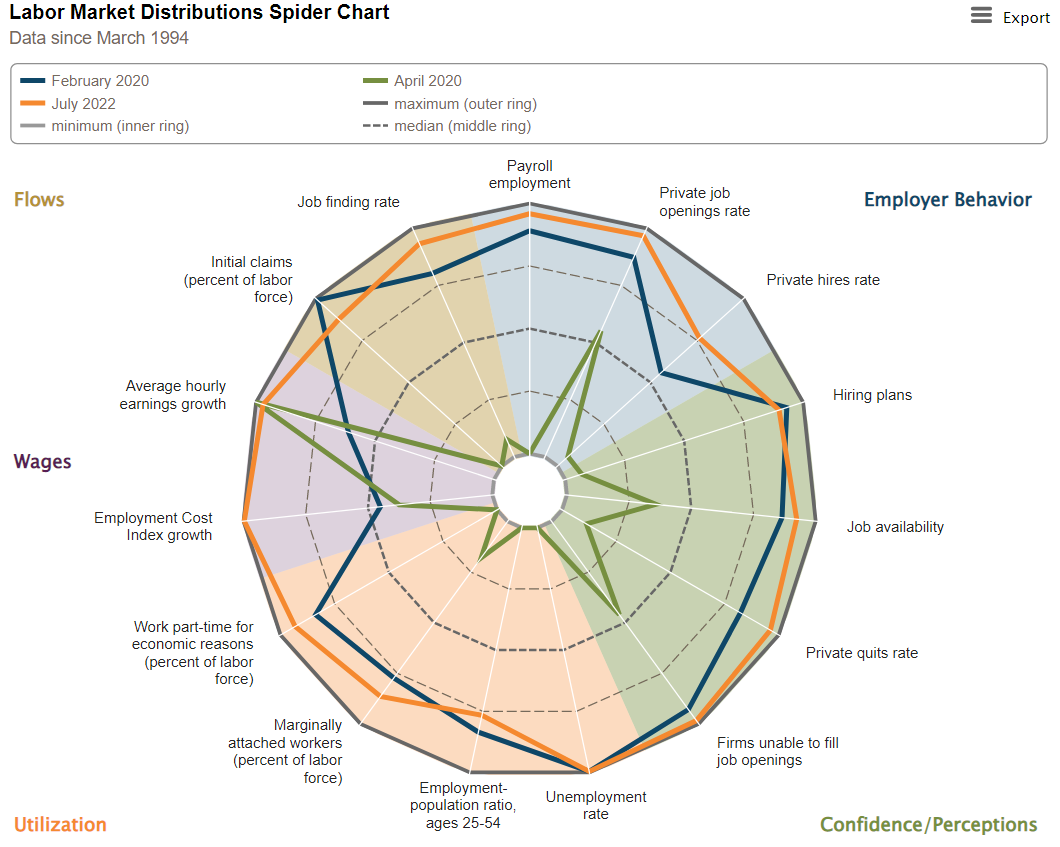

The Federal Reserve has made cooling the U.S. labor market a specific objective, and there are early signs that tighter monetary policy is having the desired effect. But we are still a long way from balance between demand and supply. As before, we will use the Atlanta Fed’s “spider chart” to frame progress.

The most encouraging news from the July employment report was that total employment has caught up to its pre-pandemic level. From a deficit of nearly 22 million jobs in April 2020, that is no small feat.

But there is still not enough labor to go around. Job openings weighed in at 10.7 million in June, a decline from a record high 11.9 million in March, but still holding much higher than the pre-pandemic norm of about seven million. The number of openings is still almost double the estimated number of unemployed workers. Surveys routinely show that employers are still feeling an overheated labor market.

|

Labor force participation is the greatest shortfall of the labor recovery. |

Conventional wisdom states that firms add headcount when they are confident in their outlook for growth. In today’s market, some of this hiring may be labor hoarding, trying to capture good candidates now, instead of assuming that workers will be available to fill roles at the moment vacancies open. Workers also show their confidence through elevated quit rates (or voluntary separations). People leave jobs when they have found a better role or are confident they will find one quickly; in a weaker labor market, workers guard their current roles jealously.

A review of labor force flows includes the metrics that are still in recovery: employment-population ratios and labor force participation rates are below their pre-pandemic norms. Prime-aged (25-54) workers are closer to a full recovery, but older workers have not bounced back. Through the prior growth cycle, participation by workers over 55 grew, and this can happen again in the years ahead; retirement does not need to be a permanent state, especially for knowledge workers.

We are closely tracking weekly unemployment claims. They have risen from record lows earlier this year, and are now at a level consistent with the strong labor market before the pandemic. However, a continued increase will be cause for concern.

Wages are running hot. In the entire cycle before the pandemic, year-over-year wage gains never exceeded 3.6%, comfortably in excess of the rate of inflation, leading to real wage gains. At the time, we contemplated whether this could spur inflation out of its dormancy. In every month of 2022, wage gains have exceeded 5%. In the second quarter, the employment cost index, which includes all compensation costs including benefits, notched a record annual increase of 5%.

Wage gains are a double-edged sword. They are a higher cost to businesses, and they will be passed through to final prices, fueling inflation. However, few workers would turn down a raise. Higher wage offers may motivate potential workers back into the workforce. But how many people remain on the fence? Anyone who needs an income has likely taken a job (and gotten a raise); there are only so many retirees and stay-at-home parents to coax back into the labor force.

All of these metrics help to explain the state of the labor market, but they still do not paint a complete picture of the populace. The pandemic has done permanent damage: while the majority of COVID-19 fatalities were among the elderly, people under age 65 still accounted for over 250,000 deaths. This grim figure is one reason for the continued scarcity of workers. Complications of long COVID and drug abuse make it harder to get people back to work.

Childcare remains dislocated, as well. While total employment has recovered, payrolls in day care centers remain 88,000 (or 8%) below their pre-pandemic level. Many daycare centers closed in pandemic lockdowns, and their workers found other roles. Even if this sector stalls, this challenge will work itself out in due course for many families, as children reach school age. Flexible work schedules may allow working parents to find an adaptable role to return to.

|

Tight labor markets lead to higher wages, which add to inflation. |

And it is not all bad news, as new business formation has been running at an elevated level since 2020. It’s likely that some workers who appear to be missing are now working for themselves or in small startups.

A reduction in foreign workers is compounding the lack of available labor. The flows of both permanent immigrants and temporary workers stopped entirely in 2020 as nations closed borders, then resumed slowly. We are seeing progress this year, which is encouraging. Higher wages alone will not create more workers, and a restoration of immigration will help to fill gaps in labor supply.

Labor markets are a vital gauge of economic health. Their strength makes the current recession speculation implausible. Every recession has included significant job losses, but 2022 has thus far shown only strong gains. Fed governors will pay close attention to these measures in their effort to orchestrate a soft landing, bringing inflation under control without impairing growth or destroying jobs. We will keep a close eye on them, too.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.