Major world economies have lost substantial momentum. Higher prices continue to squeeze living standards and depress consumer confidence. Economic policy has turned from supportive to restrictive. Idiosyncratic events like the war in Ukraine, property protests in China, and extreme heat across many countries have been troubling. Readings on output and expectations for the future have diminished.

However, there are some positive signs emerging. Commodity prices are cooling, and supply chain pressures are easing amid softening demand. We believe global growth will slow, but won’t come to a halt. The battle to contain inflation will be a central effort in most places.

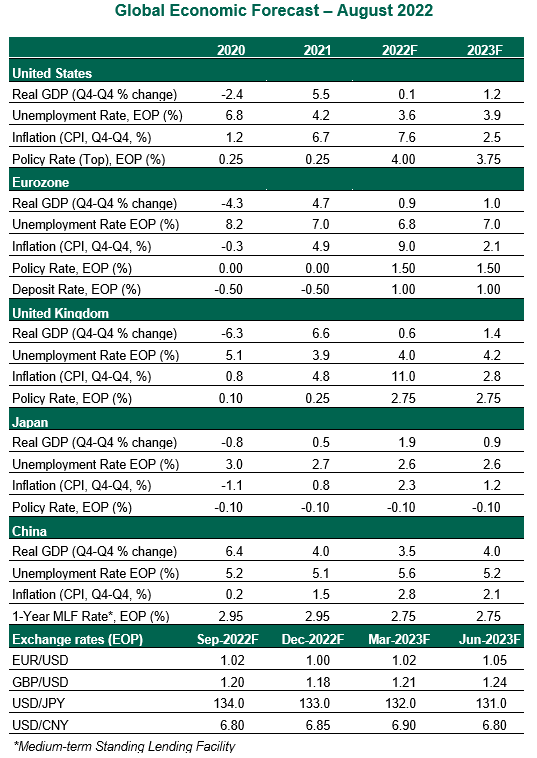

Here are perspectives on how major economies are poised to perform this year and next.

United States

- A decline in real U.S. gross domestic product (GDP) for the second quarter renewed speculation that the economy has entered a recession. While slower inventory accumulation was the primary downward force, consumption growth was also sluggish. However, the red-hot labor market offers support to the view that activity hasn’t collapsed.

- The July inflation report offered an encouraging signal. Headline inflation was flat month over month, bringing the year over year measure down to 8.5%. Lower energy prices led the decline. Costs fell in sectors that had been especially hot throughout the year, such as airfares and used vehicles. That said, one favorable reading will not drive the Fed off its path of rapid interest rate increases. We expect the target rate for overnight rates to reach 3.75%-4.00% at the end of the year.