I played dominoes often when I was a kid. The preferred variant in our home was muggins, or straight dominoes, in which players attempt to position their tiles so that the exposed ends total a multiple of five. My father taught me the game, believing it would help me to do math in my head.

My less nerdy friends played with dominoes, too. They’d set them up in long columns, and then set off a chain reaction by pushing over the first tile. Back then, a sophisticated layout included 100 pieces and would occasionally attempt a slight turn; today, domino architects are creating systems of more than 50,000 tiles, which take days to assemble and almost ten minutes to topple.

Dominoes have been front of mind lately for economists, as we try to anticipate the fallout from a potential recession and recent market corrections. Financial systems have become much more intricate over the last generation, and a topple in one sector has periodically jeopardized the entire network. The Asian Financial Crisis of 1997-98 spread to Russia and then New York; the U.S. mortgage crisis spread from Main Street U.S.A. to…almost everywhere.

This time around, balance sheets across the economy are serving as barriers against contagion. Lessons learned from the 2008-09 crisis have led firms, financial institutions, and regulators to safeguard themselves, reducing the risk that stress will spread.

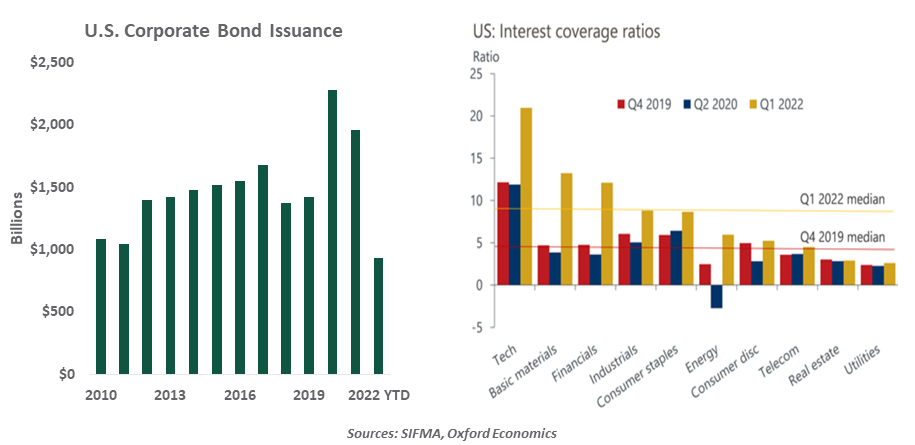

Corporate balance sheets are arguably in better shape than they have been in many years. Backstops provided by governments and central banks facilitated immense fundraising in 2020 and 2021, even among low-rated obligors. Borrowing was extended for longer terms, at very low interest rates. Cash levels at S&P 500 firms stood at $1.5 trillion at the end of 2019, and peaked at $2 trillion at the end of last year.

The technology sector led the equity market upwards in the decade prior to the pandemic, and that sector has corrected by the most since then. Fortunately, tech companies have very strong ratios of cash to interest payments, providing a substantial buffer against potential default.

Household finances were bolstered during the pandemic by direct payments to households, extended unemployment benefits, and expanded child credits. For a time, the pandemic restricted options for consumption, and personal savings accumulated. Low interest rates allowed homeowners to refinance their mortgages, locking in modest borrowing costs long into the future.

|

Balance sheets across the economy are in strong condition.

|

Despite the 2020 recession and the ongoing challenges posed by COVID-19, default rates on consumer debt have been very low during the past two years. Savings have dissipated, though, especially among households with more modest incomes. The use of consumer credit is rising modestly, but the ratio of interest payments to household income remains lower than it was prior to the pandemic.

The strength of labor markets has been very beneficial to household finances, even as budgets have been challenged by rising inflation. And underwriting standards for household debt remain much more cautious than they were prior to the 2008 crisis. 90-day delinquencies on consumer loans are still less than half the rate that we saw in 2019. There will certainly be stress for some households as the economy slows, but it seems unlikely to accumulate into something systemic.

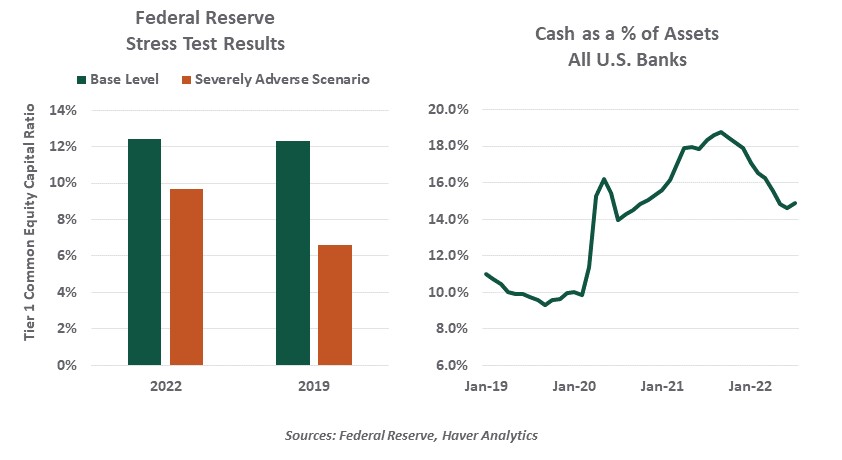

Bank balance sheets in most parts of the world are very strong. The injection of liquidity by central banks, combined with rigorous stress testing, have sustained a high level of capital in financial institutions. The results for the Federal Reserve’s most recent Comprehensive Capital Analysis and Review (CCAR) show that U.S.-based firms are much better able to withstand adversity than they were prior to the pandemic.

The strength of these barriers to contagion may, however, be tested in the year ahead. The most worrisome potential flash points are:

-

Emerging Markets. The pandemic hit some countries much harder than others. Those whose finances were not in good order prior to COVID are facing difficult choices as they attempt to stimulate their economies, protect the value of their currencies and sustain debt payments. Some large emerging markets are well positioned, but a handful of them may not be able to keep everything in balance. China, the world’s largest emerging market, is dealing with a chain of challenges that may affect others in the region (and around the world).

-

The “Crypto Correction.” Digital currencies and digital assets enjoyed tremendous popularity and performance through the fall of last year; since then, the Bloomberg cryptocurrency index is down by two-thirds. More attractive rates on more conservative investments have been one contributor, and the potential for new regulation is another.

Some observers are dismissive of the potential for crypto assets to cause contagion, but an estimated 20% of American investors have some holdings in this space. And funds specializing in the sector could be vulnerable to the challenges that have stressed other investment vehicles during times of decline: insufficient liquidity and improper use of leverage.

|

The next crisis rarely looks like the last one, so vigilance is recommended.

|

While financial crises have common ingredients, they rarely repeat themselves. In looking for vulnerabilities, we often focus excessively on past patterns. Peripheral vision and healthy imaginations will be critical in the year ahead, if we are to prevent one toppled domino from bringing down the whole string.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust