Fed Aggression and Upcoming Midterm Elections Add to September Jitters

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSeptember has historically been one of the worst months for stocks, with returns averaging -0.34% for the 30-year period, -0.26% for the 15-year period and -0.92% for the five-year period, according to Bloomberg data. As you can see below, September is the only month when the market was down on average in every time period.

This, coupled with the fact that 2022 has already been a highly volatile year due to scorching inflation, rising interest rates, recessionary fears and a persistent war in Ukraine, means that investors may consider seeking a haven for their wealth. At the moment, cash appears to be king, with the U.S. dollar’s value at a 20-year high.

Loyal readers know I also prefer gold and high-quality gold mining stocks, which I believe should make up no more than 10% of a conservative investor’s portfolio. Investors with a longer time horizon may consider between a 2% and 5% weighting in Bitcoin, which looks attractive now at around $20,000.

Two Additional Risks: The Fed and Midterm Elections

There are two additional macro risks that will make this September particularly interesting. The first is the Federal Reserve’s more aggressive stance against inflation. At last week’s Jackson Hole Economic Symposium, Fed Chair Jerome Powell admitted that rates will likely stay higher for longer to slow growth, which “will also bring some pain to households and businesses.”

Some market watchers and analysts translate Powell’s words to mean that he is no longer interested in a soft landing. Instead, he may be seeking what economists call a “growth recession,” defined loosely as a period during which the economy is growing at such a slow pace that more jobs are being lost than added.

We’re not there yet, though August’s jobs report, released today, could arguably be indicating a slowdown. An estimated 315,000 payrolls were added during the month, slightly exceeding some economists’ expectations but down significantly from July’s 526,000 jobs added.

Another indicator that the economy may be slowing? Lower oil prices. The price of West Texas Intermediate (WTI) crude fell for the third straight month in August, its longest losing streak since the beginning months of the pandemic in 2020. Just as it did then, oil could be telling us that global demand is slipping.

The second risk is the upcoming midterm elections. Market volatility has tended to be higher in advance of the November midterms, which are largely seen as a referendum on the incumbent president’s policies.

Historically, the political party in charge of the White House has lost seats in Congress during the first round of midterm elections. Notably, Democrats lost a whopping 63 seats in 2010, prompting then-President Barack Obama to call the defeat a “shellacking.” The most recent exception to the rule came in 2002 when Republicans picked up eight additional seats, suggesting Americans approved of President George W. Bush’s job as chief executive and commander-in-chief, particularly following the 9/11 attacks.

I decline to make any predictions on this year’s midterm elections, other than to say that the most favorable outcome may be a divided Congress. History shows that stocks have generally performed better when a Democrat was in the Oval Office but the U.S. House and Senate were split (though, admittedly, this arrangement has occurred far less frequently than others over the past 90 years).

In short, investors seem to prefer legislative gridlock. The day after the midterm elections in 2018, which saw the Democrats take control of the House and Republicans remain in control of the Senate, the S&P 500 jumped more than 2%.

Focus on the Policies, Not the Parties

As a reminder, we at U.S. Global Investors have no preference when it comes to political parties. It’s the policies that matter, and we believe there’s money to be made if you ignore the noise and follow the trendlines, not the headlines.

Below is the S&P 500’s performance from the start of each new presidency going back 30 years to the November midterm elections. Except for the second half of President Joe Biden’s term so far, and all of Bush’s first term—which had a series of unique challenges, including the remnants of the dotcom bubble, the Enron scandal and 9/11—stocks have generally headed higher no matter which party held the White House.

Fortune Favors the Patient?

Here’s another way to look at it: The market has been up three out of every four years going all the way back to 1926. If your portfolio is down for the year right now, as it is for most investors, it may make sense statistically to put it out of mind for the time being instead of selling at a loss.

This strategy has worked well over a longer timeframe. For the past 84 years, selling S&P 500 stocks after holding them for 10 years has led to a realized loss in only three main instances: the late 1930s (due to the Great Depression and World War II), the mid- to late-1970s and early 1980s (due to oil shocks and high inflation) and the 2008-2009 financial crisis. In all other cases, holding stocks for 10 years or longer has been a profitable action; on average, investors doubled their investment. Today, the market is down about 12% over the past 12 months, but over the past 10 years, it’s up 240%.

Not everyone has 10 years to make back their money, of course, which is part of the reason why I like to recommend gold. Gold was one of the few bright spots in the first half of 2022, helping investors mitigate losses in equities and bonds during an exceptionally volatile year.

U.S Global Investors (NASDAQ: GROW) reported operating income of $11.1 million, a 36% increase year-over-year, and an operating margin of 45% for the fiscal year ended June 30. Get all the details by reading the press release, found here.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.99%. The S&P 500 Stock Index fell 3.29%, while the Nasdaq Composite fell 4.21%. The Russell 2000 small capitalization index lost 4.74% this week.

- The Hang Seng Composite lost 3.28% this week; while Taiwan was down 3.96% and the KOSPI fell 2.89%.

- The 10-year Treasury bond yield rose 14 basis points to 3.189%.

Airlines and Shipping

Strengths

- The best performing airline stock for the week was Jet2, up 5.4%. Qantas’ fiscal year 2022 results show improved capacity and revenue per kilometer in the second half of the year, highlighting its pricing power. The earnings results, combined with strong bookings, saw net debt improve to A$3.94 billion, below pre-Covid and targeted levels. As a result, the company announced a A$400 million buyback, its first since fiscal year 2019.

- Traveler throughput had cooled modestly from the highs earlier in the summer, but as the Labor Day holiday weekend approaches, it looks like there may be a second wind. August 28 was the highest 2022/2019 percent change this year, up 22.5% and outpacing the previous summer high on June 30, up 17%. This also marks the ninth time this year that volume has exceeded 2019 levels.

- The Japanese government announced that from September 7, visitors or returning nationals entering Japan, will no longer be required to take a Covid test overseas. Specifically, proof of a negative test taken 72 hours prior to departure, and triple immunization with a vaccine designated by Japan, will no longer be required when entering Japan, including for foreign nationals.

Weaknesses

- The worst performing airline stock for the week was SAS, down 17.7%. FedEx is facing rising pressure from self-employed parcel delivery contractors to increase pay rates in response to soaring inflation and rapidly increasing operating costs (which have reportedly left many of them in severe financial difficulties). One of FedEx Ground’s biggest contractors, Spencer Patton, has led a well-publicized campaign for better pay rates and has formed a trade association for contractors.

- Airline system net sales took a sizable step back this week to -23.6% versus 2019 for the week (compared to last week’s -9.3%). System volumes and pricing decelerated -23.5% versus 2019 and -0.1% versus 2019 (versus up 2.5% last week), respectively.

- International airline volumes declined to -24.0% versus 2019 (versus -9.8% last week) and are now slightly behind domestic volumes for the first time since mid-May, which were -23.3% versus 2019 (versus -12.4% last week). Both channels saw pricing step back with domestic and international pricing now -3.5% versus 2019 and up 3.8% versus 2019, respectively.

Opportunities

- According to Cowen, given that airlines continue to limit capacity, the group does not expect to see a significant move down in air fares in the fall unless there is a resurgence in Covid cases. Conference season resumes in September, and Cowen anticipates business travel to increase, as most of these events are in person again. Demand will also get a boost from the workers returning to office.

- Morgan Stanley sees favorable risk-reward and industry outlook for airlines given: 1) the normalization of global supply chains and spot freight rates is likely to take much longer than market expectations, given the confluence of factors at play; 2) upcoming environmental regulations should take away 10-20% capacity over 2023-24, as estimated by OOIL, to offset new vessel delivery during the period; 3) major global liners have different priorities, compared to a prior focus on volume growth and market-share gains during the industry’s last downcycle.

- Major U.S. airlines have updated their customer service agreements, reports CNN, following pressure from the Biden administration to step up consumer rights. The policies have been rewritten in clearer language with tweaks in some cases to when passengers can receive meal and hotel vouchers if a flight is canceled or delayed, the article explains.

Threats

- Pilots at Lufthansa have rejected a wage offer by Germany’s flagship carrier and could go on strike anytime, union VC said on Thursday, as a dispute over pay continues. They had voted in favor of industrial action last month, threatening further disruption during the busy summer travel season. VC said Lufthansa’s most recent offer had been a step in the right direction but remained short of the union’s demands, which include a 5.5% pay rise this year for its pilots and automatic inflation compensation thereafter.

- The regional airlines are raising pilot pay to mainline levels, which may render the business model obsolete. Mesa Airlines raised starting pilot pay to $100 per hour for first year, first officers, and to $150 per hour for first year captains on the CRJ900 and the ERJ175. Other regional airlines previously raised first officer starting pay to the $90 per hour range. The more important point, however, is that these levels exceeded the levels United Airlines and its pilots negotiated earlier this year.

- Shippers are so worried that west-coast ports will be impacted by strikes during the ongoing collective contract negotiations that they are instead using ports on the country’s east coast, which is now suffering severe congestion. According to analyst firm Xeneta, the transfer of container traffic from west to east is so great that the difference in spot rates between the coasts is at a record high on freight between the Far East and the U.S.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Russia, gaining 8.5% (foreign investors have been banned from trading on the Moscow Stock Exchange since Russian troops invaded Ukraine at the end of February). The best performing country in Asia this week was Indonesia, gaining 0.6%.

- The Hungarian forint was the best relative performing currency in emerging Europe this week, gaining 3.5%. The Pakistani rupee was the best performing currency in Asia this week, gaining 1.2%.

- Hungary reported strong Manufacturing PMI while most emerging markets saw weakening manufacturing activity. The PMI in Hungary was reported at 57.8, unchanged from the prior month’s reading. In addition, this week Hungary reported strong second quarter GDP of 6.5% on a year-over-year basis.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 3.9%. The worst performing country in Asia this week was Taiwan, losing 3.9%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 0.4%. The Thailand baht was the worst performing currency in Asia this week, losing 1.4%.

- The Caixin Manufacturing PMI fell below the 50 level that separates growth from contraction. China’s Manufacturing PMI, the Caixin PMI and the Eurozone Manufacturing PMI all fell into contractionary territory.

Opportunities

- Germany’s natural gas storage has reached 80% and the nation is on track to meet its October storage targets early, according to a German official. But still, the EU needs to boost supply reserves to at least 90% to have a safe winter, the IEA has warned. At the same time, reports emerged that Russia is burning an estimated $10 million worth of natural gas a day near its border with Finland; gas that could have been exported to Europe to secure Europe’s gas resources for the winter.

- The Security Exchange Commission announced that the United States and China have agreed to allow U.S. regulators to review accounting firms in China and Hong Kong. Alibaba and JD.com will be amongst the first Chinese companies to be inspected by U.S. regulators in September.

- China continues to impose new restrictions, even as nationwide Covid cases are declining, due the country’s Zero-Covid policy that is strongly supported by President Xi Jinping (as the leader prepares for his next term re-election in October). With Xi securing his third term in power, he may be more open to the idea of moving away from the Zero-Covid policy and international travel restrictions.

Threats

- The chairman of Lukoil, Russia’s second-largest oil company and a critic of Putin’s war with Ukraine, died this week after falling out of his hospital window in Moscow. Tass, the Russian state-run news agency, called Mr. Maganov’s death a suicide. It cited an unnamed source in law enforcement who said that Mr. Maganov, 67, had been hospitalized after a heart attack and that he was taking antidepressant pills. Russian investigators were on the scene, Tass said.

- This week Europe paid respects to all who died during WWII, which erupted on September 1, 1939, when Russia invaded Poland from the East and Germany from the West. Poland has estimated its World War II losses caused by Germany at 6.2 trillion zloty ($1.32 trillion) and announced its plans to officially demand reparations from Berlin. An estimated 40,000,000 to 50,000,000 people died during the war. An estimated 5,800,000 Poles died, which was 20% of Poland’s population at the time. Warsaw, the capital of Poland, was 80-90% destroyed during the 1944 Warsaw Uprising.

- The Eurozone may soon join other global central banks in their rate hiking spree as inflation in the euro-area crossed the 9% mark. Analysts predict few hikes in the upcoming months in the amount of 50 or 70 basis points each.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was uranium, up 3.76%, as proxied by the Sprott Physical Uranium Trust, potentially following news that California legislators have extended the operation of the state’s last nuclear power plant by another five years. The state is finding that retiring gas plants cannot be replaced fast enough with solar and wind, thus needing this safety line to prevent blackouts during the transition period.

- Record U.S. fuel exports will be difficult to sustain as draining stockpiles and rising domestic demand are set to limit the country’s ability to satiate global consumption. Around 2 million barrels per day of gasoline and diesel have loaded out of the Gulf Coast so far this month, on track to make August the biggest export month since January 2016, when oil analytics firm Vortexa began tracking the data.

- U.S. crude oil and refined products exports reached 11.08 million barrels per day last week, the highest level in EIA data going back to February 1991. Crude oil exports of 4.18 million barrels per day exceeded the 4 million barrel per day threshold for the second straight week, the first time that has happened since the oil export ban was rescinded in late 2015. The U.S. has increasingly become the supplier of incremental barrels globally, particularly given limited OPEC+ spare capacity and EU efforts to phase out seaborne Russian imports.

Weaknesses

- The worst performing commodity for the week was tin, down 15.05%, along with most other metals on news that China is still pursuing lockdowns, with the recent closure of mega-city Chengdu. Lockdowns, along with economic activity being restricted in Europe due to high energy prices, are curtailing metal demand. French electricity for next year rose over 1,000 euros ($1,000) on Friday, the latest on record in a rally that’s seen the power price gain more than 10 times in the last year.

- The EIA reported a 61 billion cubic feet (Bcf) storage injection, which compares to the five-year average injection of 48 Bcf and last year’s 46 Bcf injection. Gas storage is now at 2.6 trillion cubic feet (Tcf), which is 11% below the five-year average and 9% below prior year levels.

- Oil sank to a two-week low on worries that global growth will slow as central bankers around the world embark on pushing interest rates higher to bring down inflation. This, coupled with a recent 10% production growth forecast by Permian Resources, is emblematic of the hundreds of Texas shale field drillers planning on boosting production, according to Bloomberg. U.S. oil output is still 8% below its peak in March 2020 but getting new production back online coming out of Covid, along with supply chain issues, have restrained growth, but are likely abating at this point in time.

Opportunities

- Of 700-800 steel industry operators, 54% expect steel prices to recover from $770 per ton to $800-$1,000 per ton next year, 26% expect flat prices at $700-$799 per ton and 20% expect prices to fall to $600 per ton or below, according to this year’s poll. The bulls cite that prices could rise $100-$200 per ton in the coming months on account of falling imports and falling domestic production supporting mills’ pricing power.

- Uranium stocks have been up between 15% to 20% recently. Japan is bringing back nuclear reactors and adding next generation reactors while India is also adding nuclear to the power mix. Japan’s move back to nuclear power is due to a significant policy shift as fuel prices soar and Modi’s nuclear push gains traction.

- In the U.S., Freeport LNG plans to restart its operations in November instead of October and targets to be fully operational by March. The Texas facility has been down since June. Freeport is the second-largest U.S. exporter of LNG. Notably, the U.S. is now the largest LNG exporter. U.S. LNG exports increased 12% year-over-year during the first half of 2022, averaging 11.2 Bcf/d and reflecting higher export capacity, higher prices, and higher demand in Europe.

Threats

- Goldman believes that gas prices have overshot fundamentals helped by poor market liquidity, and that European gas markets can balance with TTF well below current levels. Specifically, while the bank’s upward revision to forward gas generation demand reduces the inventory buffer driven by high LNG imports, it still expects NW European storage to end summer at 90% full even if third quarter TTF prices return to their expected 170-190 EUR/MWh range. In addition, even if the upcoming NS1 outage becomes permanent, requiring higher demand destruction, Goldman estimates the region can manage storage levels with third quarter TTF at 215-230 EUR/MWh, well below current price levels.

- Asian LNG prices have fallen 30% since the beginning of the week as the EU announced that it was considering emergency intervention in the market to cool off runaway power costs. Asia and the Eurozone have been desperate to secure winter fuel supplies with Russian gas off the market. Traders are meanwhile leery to purchase, should some type of government mandate on pricing come into effect.

- European fertilizer production is threatened by rising natural gas prices, with more than a quarter of the region’s nitrogen fertilizer capacity thought to already be lost, according to Bloomberg. A derivative impact of the growing energy supply situation in Europe is a deepening reduction in fertilizer output owing to rising natural gas prices (an important feedstock for most nitrogen fertilizer, including ammonia) given scarcity of supply and resulting impact on industrial users.

Luxury Goods

Strengths

- Consumer confidence in the United States rose again in August, after three months of decline. The index measuring this climbed to 103.2 points, according to the Conference Board index released on Tuesday, against 95.3 in July, according to data revised down slightly. Analysts were expecting just 97.4 points.

- The jobs market in the U.S. had stronger results this week. Job openings were reported higher and initial jobless claims declined. However, continuing claims increased slightly, but in-line with Bloomberg Economist expectations.

- Carmaker Aston Martin Lagonda Global Holdings was the best performing equity in the S&P Global Luxury Index this week, gaining 12.02%. Shares surged almost 7% on Friday. On the prior day, September 1, the company strengthened its senior leadership in Asia with the appointment of luxury automotive leader Greg Adams as the company’s new regional president of Japan and South Korea.

Weaknesses

- The China Caixin Manufacturing PMI, which measures manufacturing activity among smaller, private companies, fell below the 50-mark, following the China Manufacturing PMI, which measures manufacturing activity in larger, state-owned enterprises. The Caixin PMI was reported at 49.5 and the China PMI at 49.4.

- Consumer confidence in the eurozone weakened in August and prices keep rising. The economic confidence index dropped to 97.6 from 99.00 in July. Year-over-year inflation increased to 9.1% in August from 8.9% in July, above an expected 9.0%.

- Faraday Future Intelligence, an application software, was the worst-performing stocks in the S&P Global Luxury Index this week, losing 30.67%. Shares sold off as the company delayed production of its electric car (FF 91) again due to a lack of capital.

Opportunities

- India luxury car sales have been strong. Bloomberg reported that the Mercedes EQS, a luxury electric car, was sold out just a day after its launch in India. Similarly, the Lamborghini Urus was sold out in 2022. These companies are now taking orders for delivery only in 2023. The average age of buyers of super luxury cars in India is 24-36 years, and over 50% of these buyers also demand customization.

- Despite market headwinds, Porsche has lined up investor interest for its initial public offering at a valuation of as much as $85 billion, signaling one of Europe’s biggest-ever listings. Porsche plans to announce its intention to list in Frankfurt in the first week of September.

- With the stock market correcting, luxury goods, especially designer handbags, are gaining interest as safe heaven investments. A July study from the Business of Fashion says that 40% of U.S. consumers bought or were planning to buy a luxury bag, helping to grow the global market from $72 billion this year to an estimated $100 billion in 2026. Bags and jewelry watches will be in high demand, potentially offering protection against rising inflation.

Threats

- According to data shared by Saxo Bank, consumer discretionary stocks are down 13% since their peak in November 2021, and the energy crisis is yet to be priced in. The European luxury industry is probably going to be the hardest hit, according to Peter Garnry of Saxo Bank. European car brands will most likely also feel the pinch, he further commented. Discretionary spending in the U.K. is expected to take a big hit, due to falling wages in real terms. Some brokers expect inflation in the U.K. to spike to 20% next year if energy prices do not stabilize.

- An airline industry report predicts that business travel spending will return to pre-pandemic levels in 2026 rather than 2024, as previously forecasted. The Global Business Travel Association’s (GBTA) annual report states that the 2021 figure was still less than half of the over $1.4 trillion that was generated by business travel in 2019.

- The S&P Supercomposite Homebuilding Index has fallen behind the broader stock market this month and is on pace for a 7.9% decline compared to the S&P 500’s drop of 3.5%, Bloomberg reports. LGI Homes and KB Homes are among the worst performing stocks, dropping more than 10% each this month.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Celsius, rising 29.97%.

- U.S. accounting rule makers took a significant step on Wednesday toward crafting long-awaited rules for how companies report holdings of cryptocurrencies like Bitcoin, a move that would bring clarity to big crypto investors like Tesla and MicroStrategy. Their first move is defining the exact narrow population of digital assets that potential new rules would cover, writes Bloomberg.

- Celsius Network, the bankrupt cryptocurrency lender, is seeking to give back to a sliver of users who are locked out of their accounts. The company asked for a U.S. bankruptcy judge’s permission to release about $50 million worth of cryptocurrency stuck on the platform in so-called custody accounts, reports Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Hellium, down 26.39%.

- Texas was once a promised land for Bitcoin miners, a business-friendly state with stable regulations and seemingly endless energy supply. But that tide has turned, reports Coindesk. The state’s grid operator, the Electric Reliability Council of Texas, has slowed issuance of new permits for miners to connect to the grid.

- After a cruel summer, crypto fans might be in for an unforgiving September, too. The ninth month of the year has historically been one of the worst for the largest cryptocurrency, explains Bloomberg, falling every September since 2017. Bitcoin has averaged an 8.5% drop for the month over the past five years, according to Bespoke Investment group.

Opportunities

- Singapore state investor Temasek Holdings Pte is joining a $100 million funding for Animoca Brands, betting on one of crypto’s most prolific investment houses, even after a $2 trillion market meltdown. Temasek has said it doesn’t directly invest in cryptocurrencies and prefers to back service providers in the space instead, writes Bloomberg.

- Japan’s financial regulator proposed easing corporate tax rules for crypto assets as well as lighter levies for individual stock investors in support of Prime Minister Fumio Kishida’s efforts to reinvigorate the economy. Companies should be exempt from paying taxes for paper gains on crypto coins that they hold after issuing them, the regulator proposed in its annual tax-code change request announced Wednesday, Bloomberg reports.

- Swiss digital assets bank Sygnum will open a branch in the Metaverse to reach more clients seeking blockchain-based financial services. Sygnum was one of two banks that were awarded in 2019 for connecting traditional finance with cryptocurrencies and the blockchain, according to a swissinfo.com article.

Threats

- Bitcoin dipped below $20,000 once again, as hawkish comments from the Federal Reserve about inflation and the economic slowdown continue to weigh on riskier assets. Bitcoin dropped as much as 2.3% on Tuesday to trade around $19,723. Riskier assets have been having a rough few days as traders digested comments from Fed Chair Jerome Powell, who reiterated that the central bank is willing to continue monetary tightening even at the risk of an economic downturn, writes Bloomberg.

- Washington DC is suing MicroStrategy co-founder and Chairman Michael Saylor for tax fraud, claiming that he skipped out on paying more than $25 million in income taxes despite living in the district for more than a decade, reports Bloomberg. According to the lawsuit, Saylor knowingly avoided paying taxes he owed since 2005 by fraudulently claiming to be a resident of other, lower-taxed jurisdictions including Virginia and Florida.

- As reported by Bloomberg, Thailand tightened rules on advertising by crypto companies, joining countries like Singapore in seeking to protect retail investors in the wake of a $2 trillion selloff in digital asset markets. Ads for virtual tokens must include clean and visible warnings about the risks of investing in cryptocurrencies, the nation’s Securities and Exchange Commission said in a statement Thursday.

Gold Market

This week gold futures closed at $1,721.20, down $28.60 per ounce, or 1.63%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.50%. The S&P/TSX Venture Index came in off 2.15%. The U.S. Trade-Weighted Dollar rose 0.75%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-30 | Germany CPI YoY | 7.8% | 7.9% | 7.5% |

| Aug-30 | Conf. Board Consumer Confidence | 98.0 | 103 .2 | 95.3 |

| Aug-31 | Eurozone CPI Core YoY | 4.1% | 4.3% | 4.0% |

| Aug-31 | ADP Employment Change | 300k | 132k | 268k |

| Aug-31 | Caixin China PMI Mfg | 50.0 | 49.5 | 50.4 |

| Sep-1 | Initial Jobless Claims | 248k | 232k | 237k |

| Sep1 | ISM Manufacturing | 52.9 | 52.8 | 52.8 |

| Sep-2 | Change in Nonfarm Payrolls | 298k | 315k | 526k |

| Sep-2 | Durable Goods Orders | 0.0% | -0.1% | 0.500% |

| Sep-8 | ECB Main Refinancing Rate | 1.250% | — | 0.500% |

| Sep-8 | Initial Jobless Claims | 240k | — | 232k |

Strengths

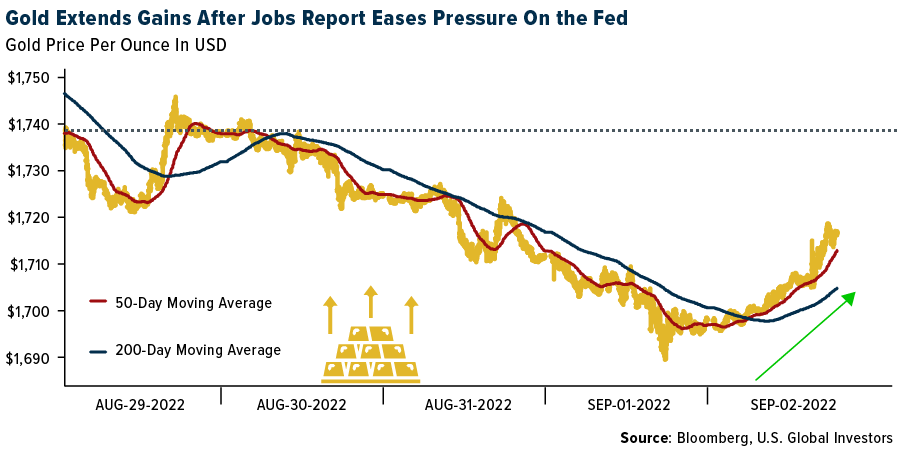

- The best performing precious metal for the week was gold, still down slightly 1.63%. Gold showed some strength as we closed out the week on a jobs report showing that more Americans are coming back to the labor market. The report reduces the risk that the Federal Reserve will hike faster-than-expected, according to Edward Gardner of Capital Economics.

- Revival Gold’s share price moved up 20% this week as the company announced it will extend the earn-in agreement to acquire 100% of the Beartrack property from Meridian Gold, a wholly owned subsidiary of Yamana Gold, for an additional two years. Revival Gold also made the final option payment of $250,000 to acquire 100% of the Barnett claims, which expands the flexibility of the Beartrack property and adds exciting exploration potential, noted Hugh Agro, President and CEO of Revival.

- Steppe Gold provided an update on progress of its Phase 2 Sulphide Expansion for the ATO Gold Mine located in Mongolia. Progress has been made on two key milestones, the grid power connection, and the new fixed crusher construction. Approval has been granted by the Mongolian government agencies to provide power to the ATO Phase 2 Expansion. This will materially decrease operating costs (by more than $100 per ounce) through significantly decreased power costs.

Weaknesses

- The worst performing precious metal for the week was palladium, down 5.28%, on little specific news other than a potentially weakening industrial pace ahead. Investor interest in gold continues to wane due to a hawkish Federal Reserve, with Chair Jerome Powell signaling higher-for-longer rates in his speech at Jackson Hole. Global holdings in bullion-backed ETFs have shrunk for 11 straight weeks, the longest stretch since September 2018. Moreover, the latest outflows have been dominated by those who established positions only within the past two years, suggesting that recent buyers have been less committed compared to traditional ETF investors, said Suki Cooper, a precious metals analyst at Standard Chartered Plc.

- Endeavour Mining reported that unidentified gunmen killed six people and wounded two others in an attack on a convoy from the Boungou gold mine in eastern Burkina Faso. Boungou accounts for 9% of the company’s asset value.

- Harmony Gold reported a swing to a net loss for fiscal year 2022, citing higher production costs and impairment charges. Gold production of 1.49 million ounces was achieved, coming in lower than the 1.54 million ounces in the prior year. Harmony’s share price slid more than 20% over the week.

Opportunities

- Maverix Metals said it has acquired a portfolio of 22 royalties from Barrick Gold Corp for an upfront cash consideration of $50 million, reports Proactive Investors, and up to $10 million in contingent consideration depending on certain events occurring. The portfolio includes royalties on development, advanced exploration and exploration stage projects located predominantly in Canada, the United States, and Australia.

- Goldman reiterated its “buy” rating on Sibanye Stillwater. The bank sees appealing valuation coupled with strategic focus on acquiring green metal assets in developed markets and unique exposure to gold within its coverage.

- “Sad” is how Dirk Treasure, CEO of Chrysos Corp., described the share price of his company after its IPO three months ago. With the price down more than 50%, largely on the overall negative tone since gold peaked earlier in the year, Chrysos has a revolutionary, game changing technology for rapidly analyzing drilled rock core for its metals content. The company uses high-powered X-rays to travel through the rock core, activate the atoms of gold and other metals, and then measure their concentration levels. This process should ultimately disrupt the historic process of splitting the core and sending it off to a lab for fire assays and then waiting weeks to months to find out where in the exploration program you’re at. Chrysos just reported maiden results with revenue up 215% to $14.2 million, ahead of the forecast $13.6, and has $92 million on hand to help fund its manufacturing pipeline.

Threats

- Northam expects cost inflation just under 10% on a unit cost basis but sees the current environment as one of “elevated business risk.” Diesel, which has doubled in price, remains a key uncertainty and is the primary energy input at Booysendal. Northam expects the diesel price to moderate alongside oil.

- UBS cut its medium-term earnings and cash generation forecasts for Northam following a disappointing fiscal year 2022 operational performance and deteriorating medium-term management outlook. UBS subsequently reduced its PT by 7% to R140 per share and reiterates its “sell” rating as the group is increasingly concerned by Northam’s unit cost and capex inflation, and questions when/if this trend will reverse through greater economies of scale and declining growth capex.

- De Beers reported sequentially “flat” rough diamond sales for its seventh sale of the year, indicating a continued strong uptake for its unprocessed diamonds amid uncertainty around the supply of rough stones out of Russia. Interestingly, this dynamic is different to polished diamond markets that had started to show signs of a souring consumer sentiment amid softening prices. It remains to be seen how long the price performance disparity persists between rough and polished markets.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits