The U.S. economy has been underperforming this year, by both recent and historical standards. Real gross domestic product (GDP) has declined for two quarters in a row. This is a technical recession, not a broad one; nonetheless, concerns are rising as to when recession could come, how severe it will be, and how long it will last.

Looking at the larger picture, a downturn is not assured. Forward-looking indicators of industrial activity are still in positive territory, and labor markets still have plenty of momentum. Inflation has started to ease a bit, which will increase real output; continued hawkishness by the Federal Reserve will also help to cool price increases in the coming quarters.

The central question surrounding the outlook is whether it will require a recession to bring inflation under control. We don’t think so, but it’s going to be a very close call on the soft landing.

Key Economic Indicators

Influences on the Forecast

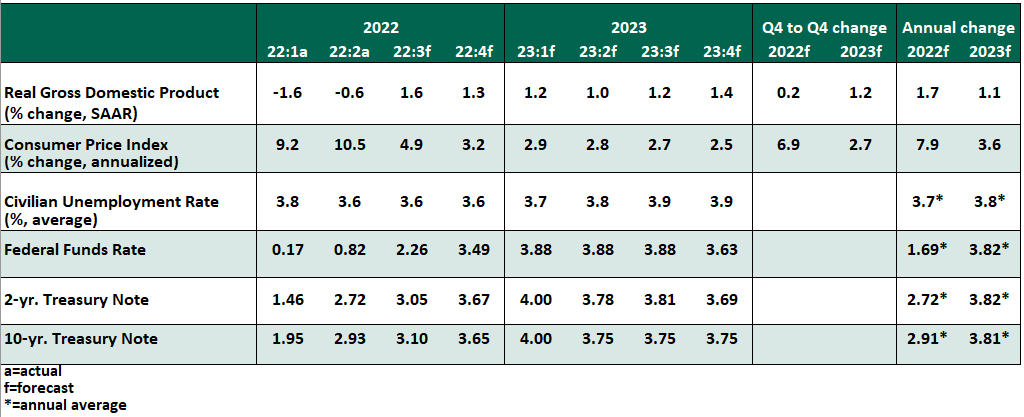

- The consumer price index for August came in a little higher than expected, decelerating only two-tenths to 8.3% year over year. The energy component provided a bigger benefit than last month amid moderating fuel prices, but food prices continued to rise. While the stronger dollar is producing lower import prices for materials that are used in the manufacturing of goods, there is no clear sign of pass-through to the consumer yet. The continued strength in core inflation, primarily rents, will likely keep the Fed on a sharp tightening path.

- Reports on payrolls, employment, and job openings suggest that the U.S. labor market is still very strong.

- The economy added 315,000 jobs in August compared to a blockbuster 526,000 payroll gain in July. The average payroll growth of 378,000 in the past three months is double the 190,000 monthly average gain recorded in the previous expansion. The unemployment rate increased two-tenths to 3.7%, largely driven by an encouraging 0.3 percentage point improvement in the participation rate. Wage inflation held steady at 5.2% year over year, well above the 3% rate observed before the pandemic.

- While the labor market will continue to defy recession fears, job creation is likely to moderate in the coming months as higher interest rates restrain economic activity.

- Fed Chair Jerome Powell offered a clear message in his Jackson Hole speech: Lowering inflation is paramount, even if a slowdown follows. The tight labor market, strong wage growth and high core inflation suggests that the war on inflation is still not won. We take Fed governors at their word: a restrictive policy stance will be maintained until inflation is under control. We expect large rate increases at each of the three meetings remaining in 2022, with the target rate reaching 3.75%-4.00% at year-end.

- Second quarter GDP was revised upwards from -0.9% to -0.6% as consumption proved more resilient. A significant upward revision to consumer spending and a larger inventory build offset a downward revision to residential investment. Corporate profits soared to a new record high, despite rising costs, an indication that businesses were able to pass on the burden to consumers. However, as warned by Chair Powell, policy tightening will inevitably “bring some pain to households and businesses,” contributing to weaker economic growth through 2023.

- Rising mortgage rates, which have climbed from below 3% in early 2021 to over 6% now, are hurting housing affordability and demand. Incoming data on the housing market depicts a sharp deceleration in activity. Housing starts have declined 20% from their peak, and existing home sales have fallen 30%. Residential investment is on course to post another sizeable contraction in the third quarter, a persistent drag on real GDP growth. The pandemic boost in demand for residential space has run its course. However, strong household balance sheets and a high proportion of fixed rate mortgages will continue to shield mortgagors and preventing spillovers to the broader economy.

© Northern Trust

Read more commentaries by Northern Trust