Recently, the Biden Administration started taking victory laps on deficit reduction. Of course, the deficit remains the bully-pulpit of fiscal conservatives, so going into a mid-term election, it is not surprising to see it used for political advantage.

“The bottom line is the deficit went up every year under my predecessor, before the pandemic and during the pandemic. And it’s gone down both years since I’ve been here – period. That’s – they’re the facts.

And why is it important? Because bringing down the deficit is one way to ease inflationary pressures in an economy where a consequence of a war and gas prices and oil and food and – it all – it’s just a different world right this moment because of Ukraine and Russia. We reduce federal borrowing and we help combat inflation.

This process [progress] is a great deal – is good news, but it didn’t happen by itself. The previous administration increased the deficit every year it was in office, in part because of its reckless $2 trillion tax cut. I know you’re tired of hearing me saying that, but a $2 trillion tax cut that was not paid for. Was not paid for. And a tax cut that largely benefited the biggest corporations – 55 of which earned $40 billion in profits and paid not a single penny in income tax in 2020 – and wealthiest Americans, like the billionaires who on average pay just 8 percent in federal taxes.” – President Biden

While the President is trying to claim credit for falling deficits, a recent Congressional Budget Office report suggests something entirely different.

However, before we get to the CBO report, some background on the deficit.

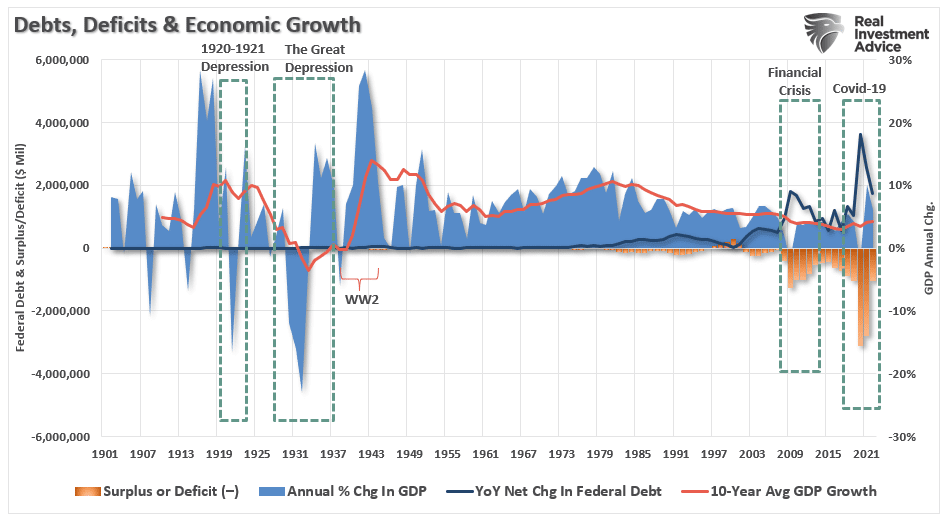

Deficit History

During most of the last 122 years, the U.S. economy ran with little or no deficit. However, President Reagan engaged in significant debt use to restart economic growth following two back-to-back recessions. Such was Keynesian economic theory in action as the Government engaged in spending to jumpstart economic growth.

It worked. However, politicians only heard the “spend money” part.

Following President Reagan, each Administration used debt to fund mostly unproductive investments, increasing the Federal deficit. Not surprisingly, the consequence of increasing debt and deficits was slower economic growth.

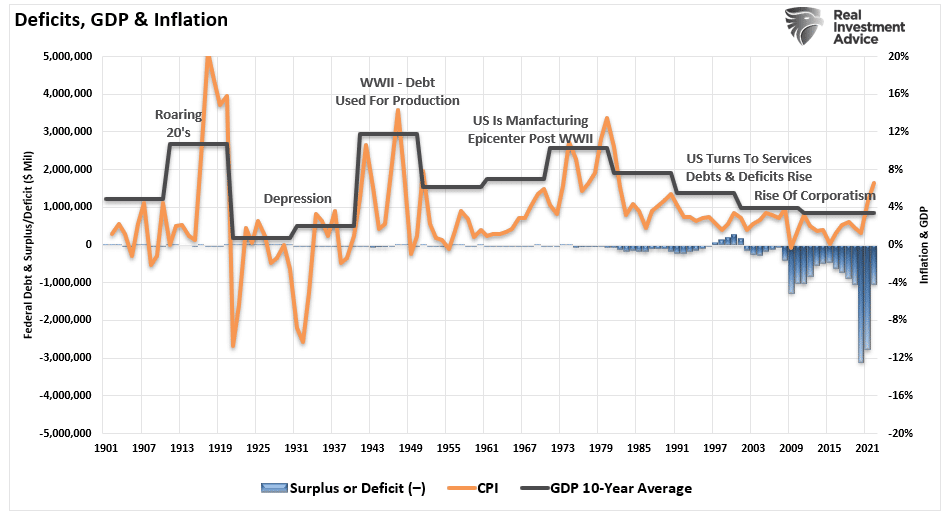

Notably, the decline in economic prosperity adds deflationary pressures on the economy. Such is the problem as the surge of inflation is not a function of more robust economic growth, as seen previously. Instead, the inflation directly resulted from the surge in deficit spending by the Government during the pandemic.

“Not surprisingly, the massive surge in money supply flooding the system during an ‘economic shut down’ created a demand glut against a constrained supply.

With consumers flush with ‘free capital’ to spend, there was no available production to provide the needed supply. With too much money chasing too few goods, inflation was the inevitable outcome.”

Of course, with that money now spent, the economic growth and inflation derived from those “stimulus checks” will likewise reverse.

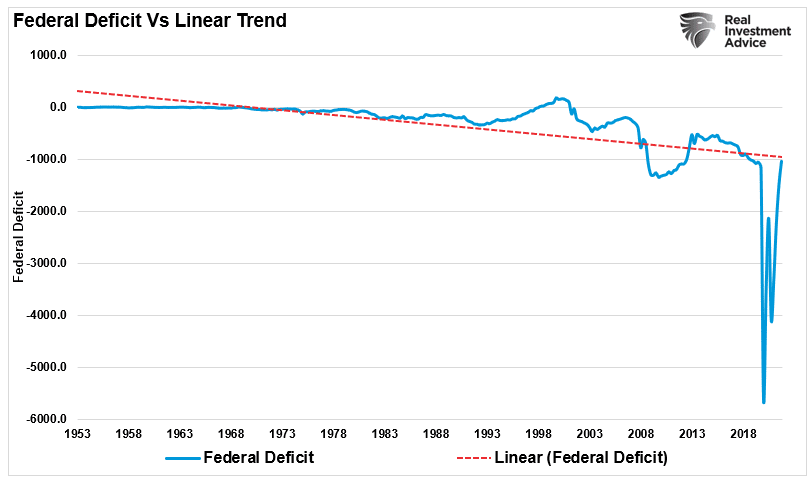

Deficit Reduction By Accident

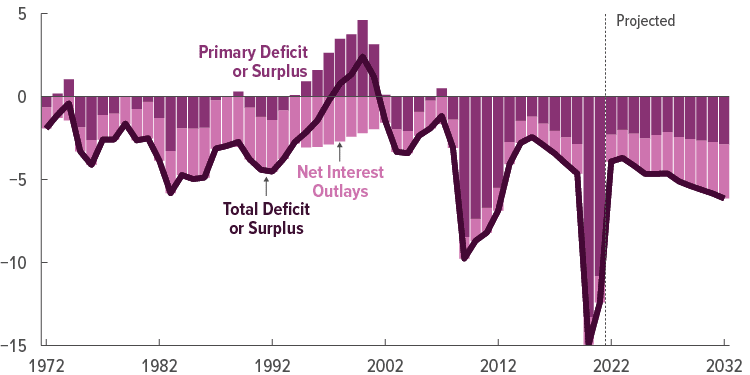

While President Biden takes credit for the deficit reduction, it is not due to any action to reduce spending. It was, by all measures, a function of reversion to the mean. As shown below, the deficit is reverting to its long-term linear trend. Given that trendline continues to decline, such suggests the current Administration is spending more than its predecessors.

As noted, such was a point made in the CBO report. To wit:

“By the time inflation comes under control, the federal budget deficit will balloon once again. It is on course to hit $2 trillion annually by the end of the decade.

The new economic and budgetary outlook released by the Congressional Budget Officeforecasts steady if unspectacular economic growth for the next 10 years, falling inflation rates, and climbing budget deficits. The report projects “the current economic expansion continues, and economic output grows rapidly over the next year.” But the government continues to spend more than it collects in tax revenue. Suchdrives annual budget deficits to $1.7 trillion by 2028 and $2.3 trillion by the end of the 10-year budget window in 2032.” – Reason

As the CBO projects, the deficit resumes growing over the next decade after the brief respite of money excess.

However, this assumes there is NO recession in the next 10 years.

Such is an unlikely probability, which means the deficit will be substantially worse over that period.

Debts & Deficits Do Matter

President Biden is taking credit for the evaporation of $5 Trillion in monetary liquidity. However, he overlooks $5 Trillion in additional debt to create those “stimulus checks,” which remain “on the books.”

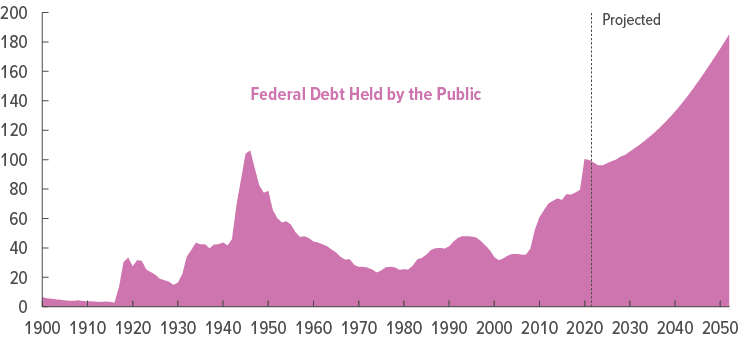

There is a long-standing addiction in Washington to debt. Every year, we continue to pile on more debt expecting economic growth to follow. As the CBO projects, Federal debt will top 180% of GDP by 2052, assuming no recessions in the next decade. The reality is that debt will likely reach those levels sooner than projected.

Such reckless abandon by politicians is simply due to a lack of “experience” with the consequences of debt.

“Excessive indebtedness acts as a tax on future growth.It is also consistent with Hyman Minsky’s concept of ‘Ponzi finance.‘ Such means the size and type of debt being added cannot generate a cash flow to repay principal and interest. While the debt has not resulted in the sustained instability in financial markets envisioned by Minsky, the slow reduction in economic growth and the standard of living is more insidious.“ – Lacy Hunt

As Lacy notes, debt-funded government spending increases and the “multiplier effect” becomes more negative over time.

So, while the President touts the deficit reduction, it will be only a momentary decline. The deficit will rise as additional increases in debt continue. The outcome will negatively impact Americans through slower economic growth and declining prosperity.

Such isn’t likely the outcome most Americans are voting for.