There’s an old joke about a patient who wakes up in the hospital after an operation. The doctor walks in and tells him he is going to live. In the next moment, though, the surgeon shares the bill for his services. The patient asks, “Is there any good news?”

The global economy has faced two heart-stopping events since 2020: first, the pandemic; then, the Russian invasion of Ukraine. Both have taken a significant humanitarian and financial toll. To aid in recovering from these situations, governments around the world have spent immense sums of money; more may be necessary to ensure a full recovery. The bills for the operation are coming due, though, and the carrying costs of financing them are rising.

Nations have accumulated immense amounts of debt during the past half-century. Classically, fiscal expansion is used to counteract shocks to private demand, such as those associated with war, natural disasters, or recessions. But since the 1980s, it has become much more common for countries to run deficits even during times of peace and prosperity.

Progressives have always favored using government to achieve a range of societal goals, while conservatives adopted a supply-side, tax-cutting approach to economic policy in the early 1980s. The two sides rarely agreed on legislation, but they generally agreed that deficits weren’t a concern…and made little effort to contain them. Borrowing grew gradually, and then substantially after the challenges of 2008 and 2020.

Financing these endeavors has been facilitated by a seemingly boundless appetite among investors for sovereign debt. With rare exceptions, auctions of government paper are enthusiastically received; international investors are often heavy buyers. Carrying costs have generally been modest for most countries, enabling them to go further and further into debt.

The world’s central banks have been among the most ravenous consumers of government debt during the past 14 years. Following the Global Financial Crisis, quantitative easing (QE) became a prominent part of monetary strategy in developed countries. Under QE, central banks purchase government bonds, helping to finance stimulative fiscal policy. This strategy was used to a significant degree from 2008-2015, but the response of monetary policy to the pandemic set a new standard. Leading central banks now own significant fractions of their nations’ debt, leading some to wonder whether monetary and fiscal policy remain independent.

|

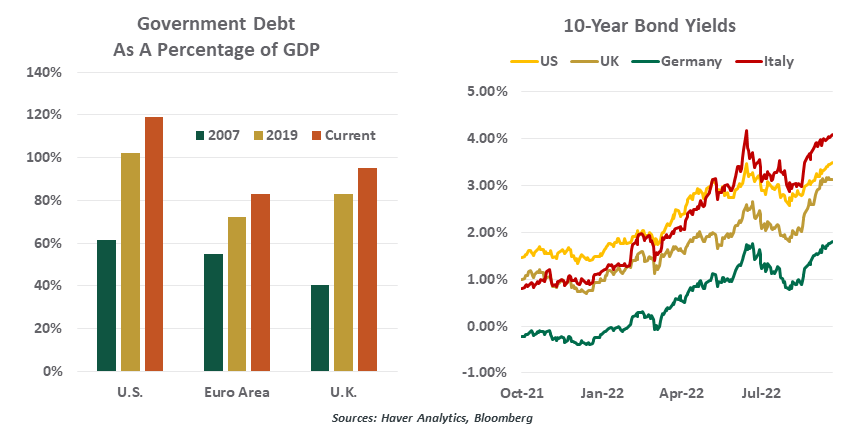

Tighter monetary policy is proving expensive for governments.

|

In retrospect, pandemic relief was excessive. Many countries recovered significant fractions of their lost output by the fall of 2020, but government programs were still stimulating demand. This demand was out of alignment with supply, creating the highest levels of inflation since the early 1980s. In an effort to bring the price level back under control, central banks are tightening policy aggressively; the Federal Reserve and the Bank of England (among others) announced large rate increases this week.

Further, a handful of central banks are seeking to reduce their investment portfolios, a process that has become known as quantitative tightening (QT). The Federal Reserve is in the forefront of this endeavor; its balance sheet is scheduled to fall by over $2 trillion over the next two years. Private investors will be asked to absorb the debt.

All of this has caused the first sustained bear market in bonds for more than a generation. Yields are up across countries and across the maturity spectrum. At one point in 2020, more than one-third of global government debt carried negative interest rates; now, almost none of it does. As a result, interest as a fraction of government spending is rising sharply, and will continue to do so for some time as old issues mature and new ones are offered.

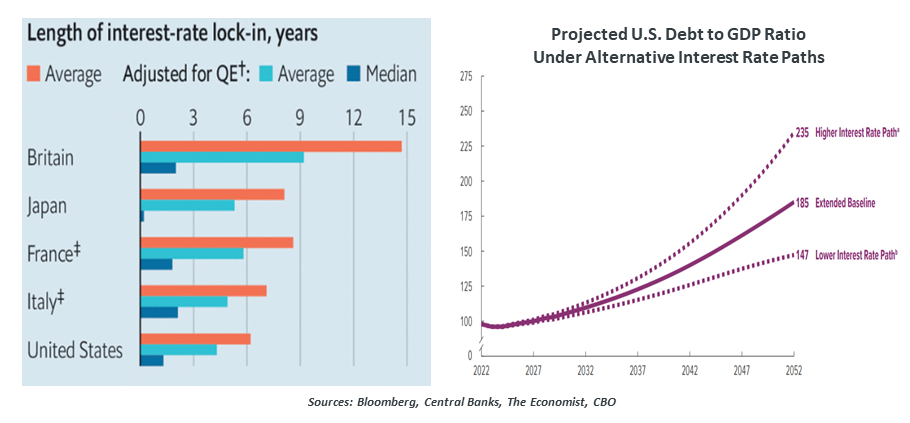

Countries had a golden opportunity in 2020 to reduce the sensitivity of their budgets to interest rates by locking in borrowing for longer terms. However, since the yield curve remained upward sloping, offering short-term bills saved interest. That funding strategy is now proving immensely costly.

Forecasts of debt and deficits for the world’s leading economies are reaching uncomfortable levels. Rising interest payments may limit efforts to use fiscal policy to combat the possibility of economic downturns during the next twelve months. Over the longer run, borrowing costs can spiral out of control and become unsustainable.

The likelihood of that fate befalling a major developed market remains low. But in a number of cases, investors are taking note. As an example, Italy’s borrowing costs are rising much more rapidly than Germany’s, a situation that is being called “fragmentation.” Italy’s debt recently exceeded 150% of its annual gross domestic product (GDP), more than double the level seen in Germany. That is creating an uncomfortable situation for the European Central Bank.

|

Stress between governments and central banks could rise in the years ahead.

|

For most of its history, the United States has not faced concerns about debt sustainability. While America’s fiscal position is far from pristine, the Treasury bond market has attracted huge inflows as other markets have faltered. But it is not clear how long the U.S. will remain favored; the latest debt projections from the Congressional Budget Office show a debt to GDP ratio of more than 180% by mid-century…more than Italy bears today.

Given the budgetary challenges caused by tighter monetary policy, stress between central banks and legislatures could increase in the years ahead. Partners in the effort to overcome the pandemic, the two may come into conflict as they go their separate ways.

For many years, many leaders have asserted that debt and deficits don’t matter. But the bill for all the borrowing may soon come due…and may leave the markets in shock.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust