It is said that life is a marathon and not a sprint. If so, Eliud Kipchoge has led a life well-lived. Last Sunday, the peerless Kipchoge set a world record in the marathon, cementing his reputation as the best of all time at that distance.

Economic and market performance is best measured over long intervals, as well. That hasn’t been the easiest perspective to maintain, as the pandemic (and the associated policy response) has produced a series of extremes in both directions. We’re presently dealing with a deceleration caused by rising interest rates, wondering if activity will slow to a halt or reverse course.

The outcome will vary by location. Our updated global economic forecast reflects our expectation that the United Kingdom and Europe will experience a recession in the coming quarters. But we have not yet concluded that the U.S. economy will enter a downturn. Questions about our call continue to come in, so we thought it would be useful to offer a current balance sheet for the American economy.

| Still no recession call for the U.S. |

Liabilities

- The housing industry is in recession. We’ve experienced a 20% drop in home sales over the past year, and home prices fell last month. Both trends are likely to continue, with mortgage rates more than double what they were last January. A slowing housing market will limit the purchase of furnishings and a range of services used by homeowners.

- The Federal Reserve is going to raise interest rates to much higher levels than previously thought. Financial conditions are still not overly tight, and real interest rates are still negative. Fed balance sheet reductions will add to the restraint that monetary policy will place on activity.

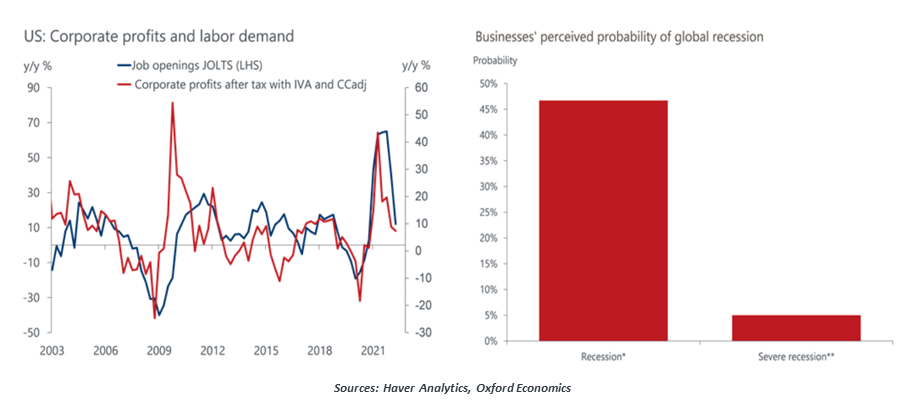

- International markets are slowing. This will increase the American trade deficit, which is a drag on gross domestic product (GDP).

- The equity market correction will likely lead companies to diminish their demand for labor. After working hard to hold on to staff in a tight labor market (and keeping postings out for more talent), firms will have to manage costs to sustain profitability. Unemployment is unlikely to rise substantially, but increased joblessness will diminish consumption.

Assets

- Even if the labor market loses a little of its luster, it is still one of the strongest in many years. Wage income has grown solidly, providing a durable source of spending. There are also still pockets of pent-up pandemic saving on household balance sheets.

- Inflation is falling. It is likely that real income growth will turn positive again within the next two quarters, restoring gains in purchasing power. The retreat of energy prices is already having a favorable impact on consumer confidence.

- American manufacturers are still doing quite well, with leading indicators like the purchasing managers index (PMI) still in expansionary territory. U.S. industry will likely benefit somewhat from the growing desire for re-shoring.

If a downturn comes, we expect it to be shallow and short. The softening of economic activity will likely lead the Fed to conclude its interest rate increases by early next year. We do not see the excesses of leverage that have turned mild problems into deeper ones in the past.

Even if recession is avoided, though, American economic growth over the coming year may not be overly robust. Fiscal policy has stretched itself to extremes over the last two years, and rising debt and interest costs will limit the ability of governments to promote a more robust expansion.

As we enter this phase, it bears repeating that recessions are not fatal for economies and markets. They arise because of imbalances, and serve to reduce them. In their wake, markets and economies typically perform well. Best to stay focused on the long run.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

More Global Markets Topics >