My fifth grade teacher was as old school as you can get. She made us write out so many multiplication tables that our hands would cramp. We were expected to recite them from memory, and if we failed, we were shamed by having to write six of them on the chalkboard in front of the class.

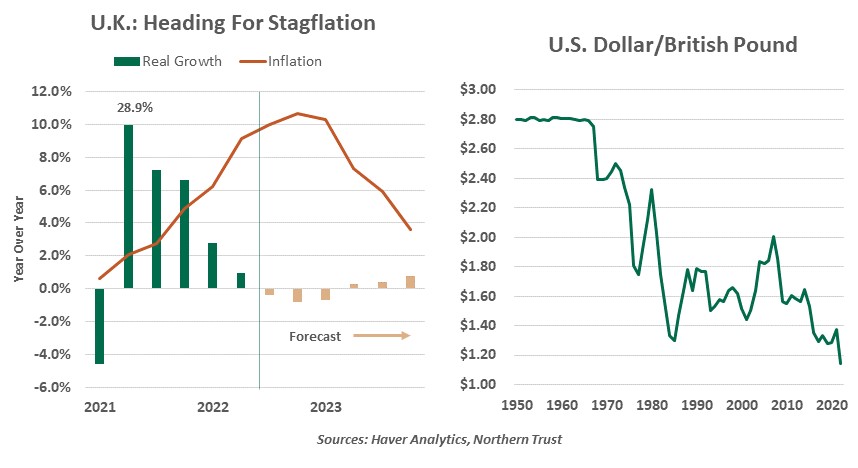

To mix things up a bit, she once had us prepare tables converting the U.S. dollar to foreign currency equivalents. To show you how the translations got burned into my brain, I still remember that the British pound was worth $2.40 at the time.

So, it was especially significant for me when the pound dropped to less than half that rate this summer. The fall of sterling has resulted from a series of missteps by the British government, some fleeting and others that are more lasting. As we watch developments, we should keep in mind that what’s troubling the United Kingdom could easily become problematic elsewhere.

My colleague, Vaibhav Tandon, covered the basic details of what happened in his excellent piece, “The U.K. Takes A Pounding.” In the four weeks since that article was posted, markets have remained volatile. And last week, Prime Minister Liz Truss was forced to resign after a tenure of only 45 days.

There are many lessons that can be derived from this episode, which should be appreciated across world capitals.

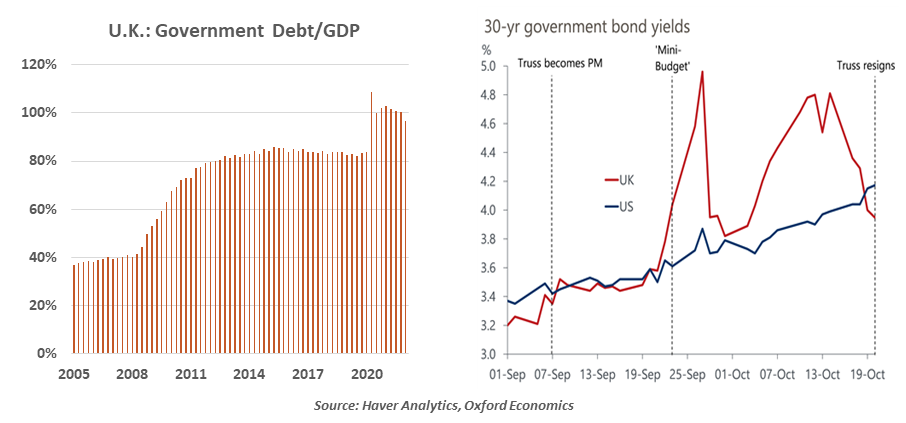

The bond vigilantes are back. In the early 1990s, the American political advisor, James Carville, said that he wanted to be reincarnated as the bond market, allowing him “to intimidate everybody.” During that era, budget policy that threatened the drive for price stability was met with reproach by investors, who became known as “vigilantes.”

For the past twenty years, however, fixed income investors have been relatively calm. Even though government borrowing has skyrocketed in most countries, interest rates have remained low. Secular governors were containing inflation, and central banks stood ready to react if it broke that containment.

But when the Truss government proposed a massive supply-side fiscal expansion, investors pushed back. Truss claimed that the package of £45 billion in tax cuts would pay for itself over time, but few believed her. Bonds sold off sharply, and brinksmanship commenced.

The episode was probably avoidable. Some inquiries with market participants could have revealed the sensitivity. It appears that investor tolerance for interminable deficits may have reached a limit, which should serve as fair warning for governments the world over.

It is very difficult to design policy to deal with stagflation. The U.K. is heading for at least a mild recession, and its inflation rate just crossed into double digits. Fiscal authorities would like to stimulate activity, but measures that boost growth also tend to exacerbate inflation. This provokes an offsetting response from the central bank. Unfortunately, the best thing a country can do in such situations is remain patient and hope that a return to low inflation will provide the backdrop for renewed growth.

However, political pressure increases the desire of legislators to act, creating battle lines with the central bank. The contretemps between the British government and the Bank of England (BoE) was acute. The BoE intervened in markets to restore some order after the meltdown, but placed a time limit on their efforts. This served to keep pressure on Parliament.

This may not be the last instance of stress between governments and their central banks. Rising interest rates are taking a toll on national budgets, and politicians have begun to complain that monetary policy is too tight. After collaborating very closely to deliver pandemic relief, the two agents of economic policy are now heading in opposite directions. The separation will not be without strain.

Systemic risk is a concern. The backup in the British bond markets revealed subtle exposures that stressed markets. Pension systems typically attempt to match their investments to the payments they expect to make to their beneficiaries. The most direct way to do this is with a ladder of bonds, but low bond yields have led pension managers to seek better returns. Some plans used “liability-driven investment (LDI)” products that purported to match off future payments and still allow investment up-side.

LDI strategies involved derivatives and leverage that came under pressure when British interest rates jumped. Plans and providers were forced to post margins and collateral that pressured their cash flow and caused short-term dislocation across a number of markets.

As of this writing, it does not appear that the U.K. pension sector will be a source of global systemic risk. But it is an example of opaque portfolios that use sophisticated instruments which can come under pressure in extreme market environments. The U.K. experience has heightened surveillance around the world to identify similar, and potentially more pernicious, analogs.

| What happened in the U.K. should serve as a warning to other countries. |

Government turnover is embarrassing in the short-term, but very damaging to an economy in the long term. With electoral margins thin, politicians are thinking short term to keep their seats, which prevents them from tackling enduring challenges like energy security, trade, and climate change. In the case of the U.K., the incomplete nature of Brexit is still a significant problem for the British economy; the Irish border situation is not settled, and the U.K. labor market is straining in the wake of mass worker departures over the last two years.

Further, leadership turmoil can erode the credibility of a government in the eyes of markets. This can diminish inbound capital flows and add basis points to borrowing costs, and it leads to weakness of the national currency.

New U.K. Prime Minister Rishi Sunak will be charged with righting the ship. But if he fails in that endeavor, the pound may fall to parity against the U.S. dollar. That would make the currency multiplication tables very easy to prepare.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust