It’s tempting to take the underperformance of emerging markets in relation to developed markets over the past decade and use it as a yardstick to judge future growth. In our view, that would not only overlook the strong potential of emerging markets for growth and portfolio diversification but fail to grasp the long-term drivers that worked to shape these markets in the past and that will likely work to shape them again.

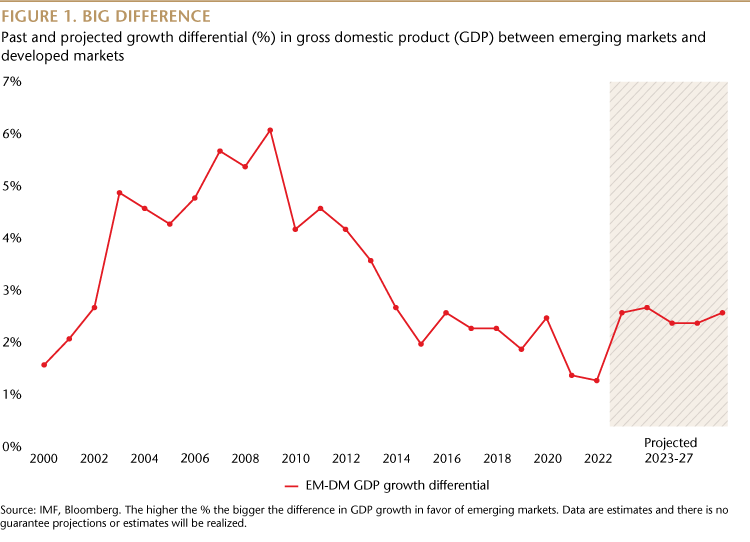

It's no secret that emerging markets underperformed U.S. equities over the last 10 years or so. But in the prior decade the opposite was true. So what were some of the underlying forces that made these two things happen? Well, one of them was a change in the so-called growth differential in gross domestic product (GDP) between emerging markets and developed markets. At the turn of the century, the differential began to expand in favor of emerging markets. Equities in emerging markets then went on to outperform developed market equities, including U.S. stocks, significantly in the 2000s. By the 2010s that trend started to reverse. As the economic growth differential narrowed so western stocks started to outperform emerging markets stocks. This year, the growth differential sits at the lowest point since 1999, in the immediate aftermath of the Asian Financial Crisis.

There are of course many drivers of equity market performance besides GDP growth, including money supply, valuations, market composition, geo-political and regulatory developments and governance standards. But economic expansion and earnings growth are a key buoyancy aid for markets. While strong GDP performance doesn’t always result in strong equity performance, especially in the short-term, it does generally lead to faster corporate topline growth. Under the right conditions, such as when capacity utilization rates increase, topline growth can lead to attractive earnings growth and this in turn over the long-term can provide upside pressure for stock prices. Higher earnings growth can then lead to higher returns on equity and ultimately higher price-to-book ratios.

“It’s reasonable to consider the possibility that emerging markets’ earnings growth may pick up and valuation discounts will narrow, potentially leading to improved relative performance.”

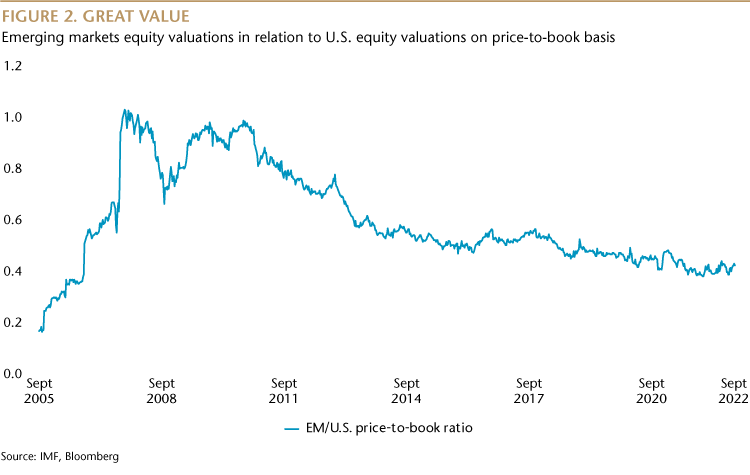

As well as this structural correlation between equity performance and GDP growth there is a cyclical correlation between relative valuation and GDP growth. During the 2000s, emerging markets equities narrowed the valuation discount on a price-to-book basis in relation to U.S. stocks as the GDP growth differential widened, earnings growth picked up and return metrics improved. Valuations achieved parity with U.S. markets and at the end of the decade emerging markets equities had outperformed U.S. equities by 286%. In the 2010s, as the GDP growth differential narrowed, the valuation discount expanded and U.S. equities have outperformed emerging markets by 262% over the past 12 years.

Return to growth

In light of these past long-term correlations we may wonder how the GDP growth differential between emerging markets and developed markets will behave in the future. Will it narrow or will it widen? In the medium term, there is some visibility. The International Monetary Fund (IMF) projects that between 2023 and 2027, the growth differential will widen again and return to the levels seen in mid 2010s. It’s perhaps reasonable therefore to consider the possibility that emerging markets’ earnings growth may pick up and valuation discounts will narrow, potentially leading to improved relative performance compared with the U.S. equities.