Reputation Disinflation

Economists have to learn to live with volatility, but our reputation has gone to extremes over the past twelve months. Last year, our team won a prestigious forecasting award; this year, we were a long way off. The distance between the penthouse and the doghouse for us was, unfortunately, quite short.

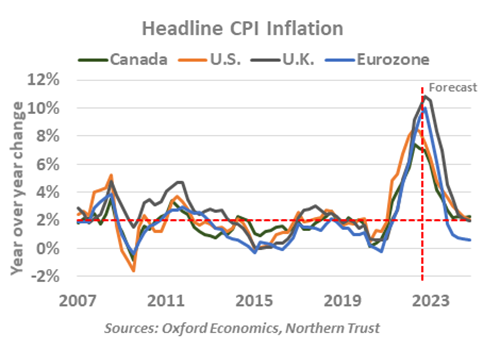

The bane of our existence has been inflation, which went from dormant to dominant. Supply chains proved more brittle than anticipated; the invasion of Ukraine, unforeseen at the beginning of the year, roiled energy and commodities markets. An unexpected and unwanted surge in home prices pushed shelter costs up. And labor shortages persisted, pressuring the prices of basic services.

Month after month, forecasters declared that inflation had peaked, only to witness further escalation. But the worst may finally be in the past. In major markets, inflation is either near or past its zenith, and we think that it will decline somewhat more sharply from here than others do. Energy costs are 50% below their midsummer peaks, house prices are falling and mended supply chains are producing an excess of inventory.

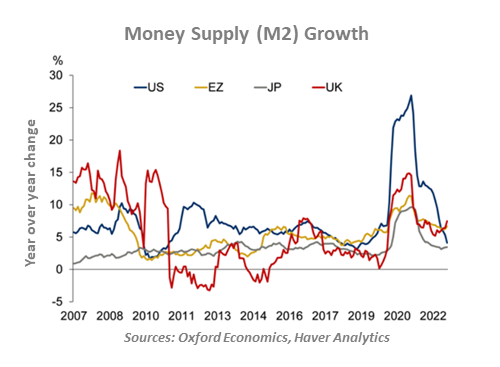

From a top down perspective, central bank tightening has restrained money supply growth (which is actually declining in the United States). Large and small firms are reporting less freedom to raise prices; after a post-pandemic splurge, consumer frugality may once again serve as a secular governor on inflation. Recession is coming to Europe and may visit the United States, taking an edge off demand.

If we are finally right, we will have avoided disrupting the rational inattention that workers have applied to inflation. Had they incorporated recent conditions more completely into their compensation demands, a wage-price spiral could easily have formed.

We had a lot of company in our miscalculations, but that carried little weight with my boss. He has sardonically referred to the persistent price level increases as the “Tannenbaum transitory inflation.” I fear that designation may stay with me long after our forecast accuracy improves.

Power Play

German Philosopher Friedrich Nietzsche once said, “what doesn’t kill me, makes me stronger.” The sentence portrays a picture of resilience amid adversity. The Europeans, faced with armed conflict and the most serious supply disruptions since World War II, can vouch for that maxim.

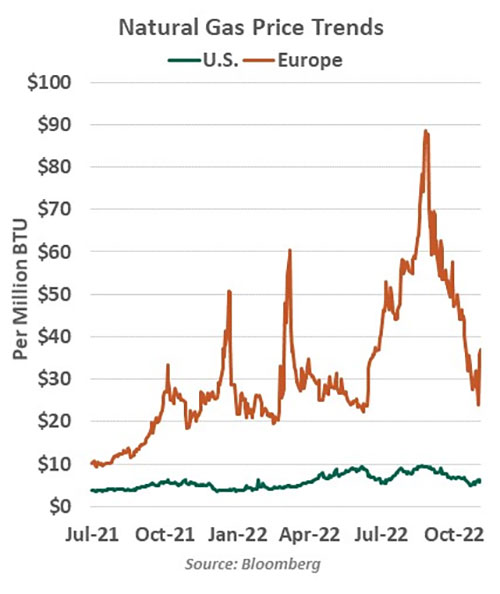

While kinetic activity has largely been confined to the Ukrainian borders, the economic implications have been felt across Europe. Food and energy markets have been the main channels of stress for the continent, as both Ukraine and Russia are major suppliers of essential commodities. The bloc has been dealing with an energy crisis ever since flow through the Nord Stream pipeline was curtailed. European gas prices reached record levels.

Natural gas is used extensively in Europe for heating, transportation and generating electricity. The rise in energy bills for both households and businesses has been weighing on economic activity. Industries have struggled to pay the cost of fuel, and some have been forced to curtail their activity. Climate change aggravated the pain this summer and is likely to lead to a faster depletion of reserves this winter. The bloc faces an imminent recession.

European governments have worked feverishly to keep a lid on costs, rebuild their stocks and wean themselves off Russian energy. Those efforts are not only serving the purpose of avoiding severe rationing, but are also allowing the continent to prevent Moscow from making a fortune from the war. But all of this has cost billions of euros and added to the mounting fiscal burden among European countries.

Gas prices have retreated sharply from the highs reached during the summer, and stocks should get Europe through this winter. But volatility in energy markets will continue to dictate the European economic outlook, posing risks to both growth and inflation in 2023. Europe will have to invest heavily in energy transition and infrastructure to prevent another winter of discontent.

Lingering Labor Limitations

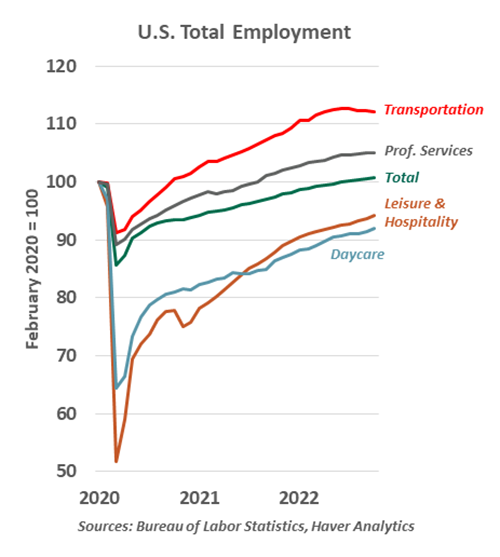

The sluggish recovery of labor markets was one of the biggest concerns of 2021. After shutdowns and stimulus programs had run their course, positions sat vacant for want of workers. The past year witnessed better progress: Total payrolls exceeded their pre-pandemic peak in June 2022 and kept growing every month thereafter.

But the new normal is still a long way from the old normal. Job openings remain abundant, whether informally gauged by "help wanted" signs or through the swollen count of job openings in official data. The top-line recovery of employment obscures a lot of stories that make the labor market feel misaligned. These are the trends we are tracking on this front:

Early retirements. Older workers were the first to step out of the workforce as COVID-19 struck, and many have not returned. Labor force participation is holding lower across demographics, but the decline has been especially pronounced and persistent for workers over age 55. Past intervals of low unemployment have helped to bring older workers back onto payrolls, so we have hope for more “unretirements.” But they may not come quickly.

Childcare. Daycare centers require close contact and were shut down for long intervals at the height of the pandemic. The workers in those centers moved on to other roles. While most sectors have recovered, daycare employment remains lower than its pre-pandemic level by 8%, or 84,000 workers.

Permanent shifts. Daycare employees were not the only workers who found other jobs. Turnover has been elevated ever since the initial COVID reopening. Workers found opportunities that suited them better and often found generous raises to boot. Their former employers are struggling to attract them back to their old roles.

Long COVID and other disabilities. Not everyone who contracts COVID makes a quick recovery; some suffer prolonged symptoms that prevent a rapid return to work. This summer, the Census Bureau estimated up to four million workers were sidelined due to lingering limitations brought on by the virus. On the upside, greater availability of remote work is helping people with physical disabilities to find accommodative roles.

Recruiters have their work cut out for them. Higher wage offers can entice some workers at the margins, but can't correct a shortage. More entry of younger workers and a normalization of immigration flows will help us restore equilibrium, but it may be a while before help is on the way.

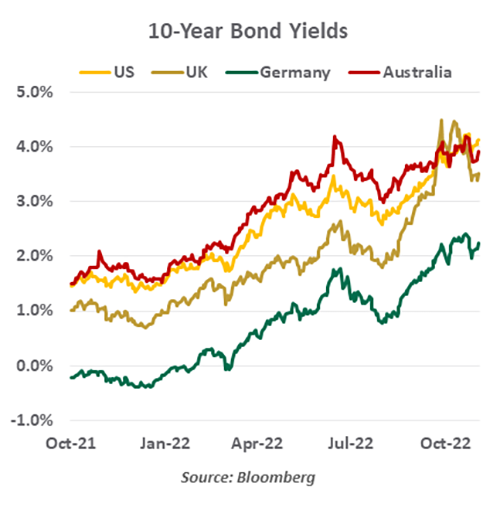

Catching Up To The Curve

Prior to the arrival of COVID-19, central banks were frustrated with inflation…because it was too low. So when the first signs of price pressure appeared in the spring of last year, they were not entirely unwelcome. Unfortunately, the inflation rate waved as it flew by targeted levels and continued to forty-year highs.

Belatedly, central banks began tightening policy. Interest rates were increased in large chunks: the speed and scale of these adjustments have not been seen in twenty years, and the ultimate impact on markets and business activity has yet to be felt. One early casualty has been the global housing industry and households in markets where mortgage rates reset frequently.

Further, balance sheet reductions (known as quantitative tightening, or QT) commenced during the summer, restraining growth in the money supply. The reduction in central bank demand for government securities is one reason for reduced liquidity in sovereign bond markets, which could become an issue for financial stability. A similar situation in 2018 forced the Fed to end its QT program months earlier than they had intended.

The current crowd of central bankers does not want to be remembered for squandering the control of the price level achieved by their ancestors. They all view low and stable inflation to be essential for long-term employment, business formation and market progress. While they would not welcome a recession, it is a price that they are willing to pay if that is what’s required to get inflation back under control. If recession does come, our view is that balance sheets across economies will prevent it from being a severe one.

The longer that central banks keep at it, the less comfortable it will be. Industries are already complaining about the restraint, and governments are complaining about the rising cost of servicing national debts. Dissonance between fiscal and monetary policy was at the heart of the October crisis in the U.K.

2022 was a very difficult year for central banks. 2023 could be even harder.

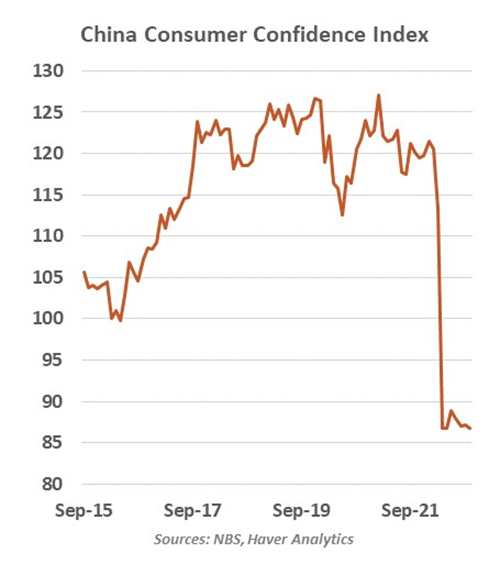

Zero Out

Keeping the spread of the virus in check was critical during the initial waves of the pandemic, when COVID-19 was poorly understood. But three years later, the cost of quarantine exceeds the benefits. Economies around the world have put the worst of the pandemic behind them, with one major exception: China.

There is no doubt that the zero-COVID approach has limited the consequences of the virus for public health. But prevention has come at substantial economic cost. Arduous restrictions on mobility have dented consumer confidence and consumption. Households have remained cautious amid lingering uncertainty over the virus, with income prospects damaged by the rolling lockdowns. Domestic and international tourism by Chinese travelers is still well below pre-pandemic levels.

Stringent controls have also been a source of frequent interruptions in the industrial and transportation sectors, leading global companies to consider moving production elsewhere. All of this has added pressure to an economy that was already struggling with a real-estate downturn, a regulatory reset and moderating external demand.

Chinese authorities have started recalibrating their approach. While Beijing is hoping for a gradual shift away from zero-COVID, it could prove to be wishful thinking. The experience of other parts of the world shows that the virus runs wild when allowed to spread, so any step back from preventing outbreaks will almost certainly be followed by a surge in cases.

China has a rapidly aging population, less effective domestic vaccines and very little natural immunity through exposure to the virus. This could put healthcare systems under severe strain and translate into a more disorderly 2023. Maintaining zero-COVID has been expensive, but policymakers will have to ensure that abandoning it doesn’t prove to be more costly.

Austerity Returns

Before the pandemic, a movement was building around modern monetary theory (MMT): the notion that government debt can be issued without a quantifiable limit. Fiscal conservatives derided MMT as the “magical money tree.” But since a government cannot default, the theory goes, it could stimulate its own economy until it reaches its full potential. Low unemployment and rising inflation would be the signals to pull back.

Circumstances pushed most economies into a real-life test of MMT. Responses to the pandemic varied worldwide, but nearly all governments spent rapidly and substantially to get through the worst of the COVID-19 crisis. Programs ranged from conventional support for public health to novel programs designed to support small businesses and expand eligibility for unemployment insurance. By many measures, they were a success: nations pulled through recurring COVID waves with minimal economic scarring, such as bankrupt businesses or foreclosed homes.

Now, nations are dealing with high inflation and an insatiable demand for labor. The time for fiscal discipline has returned. After two years of generous spending, 2022 was the year that governments tightened their belts. The U.S. deficit was cut in half from $2.8 trillion in fiscal 2021 to $1.4 trillion in 2022, a pattern matched (to varying extents) around the world.

Spending reductions are well-timed, as the rising interest rate environment has made the cost of debt noticeably more expensive. To mitigate debt servicing burdens, nations will need to find a new balance, likely to be a major struggle for many emerging economies.

This is not a theoretical concern. The short-lived Truss government in the U.K. was foiled by a spending package that could have made deficits unsustainable. Not long ago, an ambitious government agenda would likely have encountered little opposition; in 2022, bond markets reacted violently, ending careers and forcing a newfound discipline.

Calls for fiscal constraint are nothing new. But this year, they became more salient. The belt-tightening is not over, and the magical money tree may never bloom again.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

More Sustainable Investing Topics >