Capital represents the resources and labor used to produce goods and services.

“Ism” is a system.

Capitalism is an economic system based on the private ownership of the means of production and the incentives which drive their for-profit operation.

Capitalism differs from other economic systems as it allows for the private ownership of production and the resulting profits. Most other economic systems rely to varying degrees on the government to decide how resources and labor are used and how profits get distributed.

Almost everyone uses the word capitalism to define the United States economy. Unfortunately, the U.S. is straying from capitalism. The United States government and Federal Reserve increasingly pick winners and losers by dictating how capital is employed and how profits and losses get distributed.

This article focuses on one facet of government interference; the Federal Reserve’s distortion of the price of capital and the negative economic and social consequences its actions have.

Productivity is Paramount

Before harping on the Fed, it’s worth appreciating productivity, the most critical cog in any economic engine and a vital element of capitalism.

A country’s economic growth and the financial well-being of its citizens can be directly linked to how effectively an economy deploys capital. In a purely capitalistic economy, the incentive for profit is the leading factor promoting the most effective use of a nation’s available capital, labor, and resources.

Economists use the term productivity when discussing said effectiveness.

The greater the productivity, the more wealth generation occurs, with the fewest resources requiring the least amount of labor. The more productive society is, the wealthier its citizens are.

Conversely, if there is little to no productivity growth, economic growth is limited by the amount of labor and resources. In developed economies such as ours, labor and resources have finite growth. Over time as natural resources become scarcer and more expensive and demographic contributions to growth weaken, flat or negative productivity growth becomes likely.

Measuring Productivity

Like many economic measures, productivity is impossible to measure precisely, but there are ways to gauge it. For instance, many economists consider total factor productivity (TFP) a reliable measurement of productivity. It may not be exact, but it provides valuable insight into productivity trends over various time frames.

TFP boils down to the ratio of GDP to its inputs. The greater the proportion, the more the economy grows per its usage of resources.

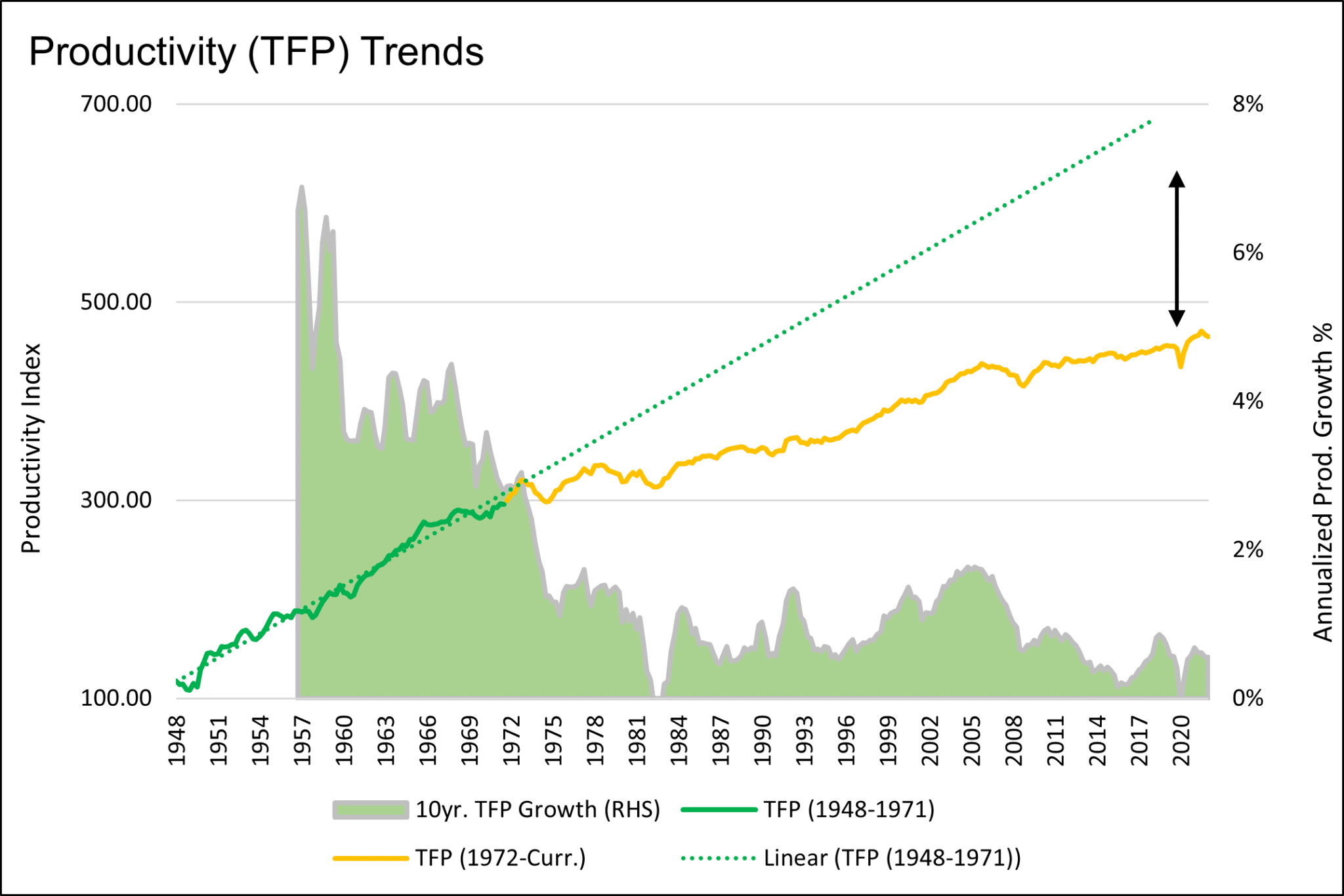

The San Francisco Federal Reserve provides historical TFP data.

Since 1980 TFP growth has stagnated from 0% to 2% annually. Such change is well below the 4% to 6% range in the thirty years following WWII. The graph below shows how the trend of the productivity index shifted to a lower growth rate in the early 1970s. The dotted lines highlight where it would be, assuming the productivity growth trend from 1948 to 1971. The green area graph highlights that the ten-year productivity growth rate is now below 1%.

Not surprisingly, GDP growth followed the declining path of productivity growth. As we share below, it’s possible GDP could run much higher if the pre-1970 productivity trends continued.

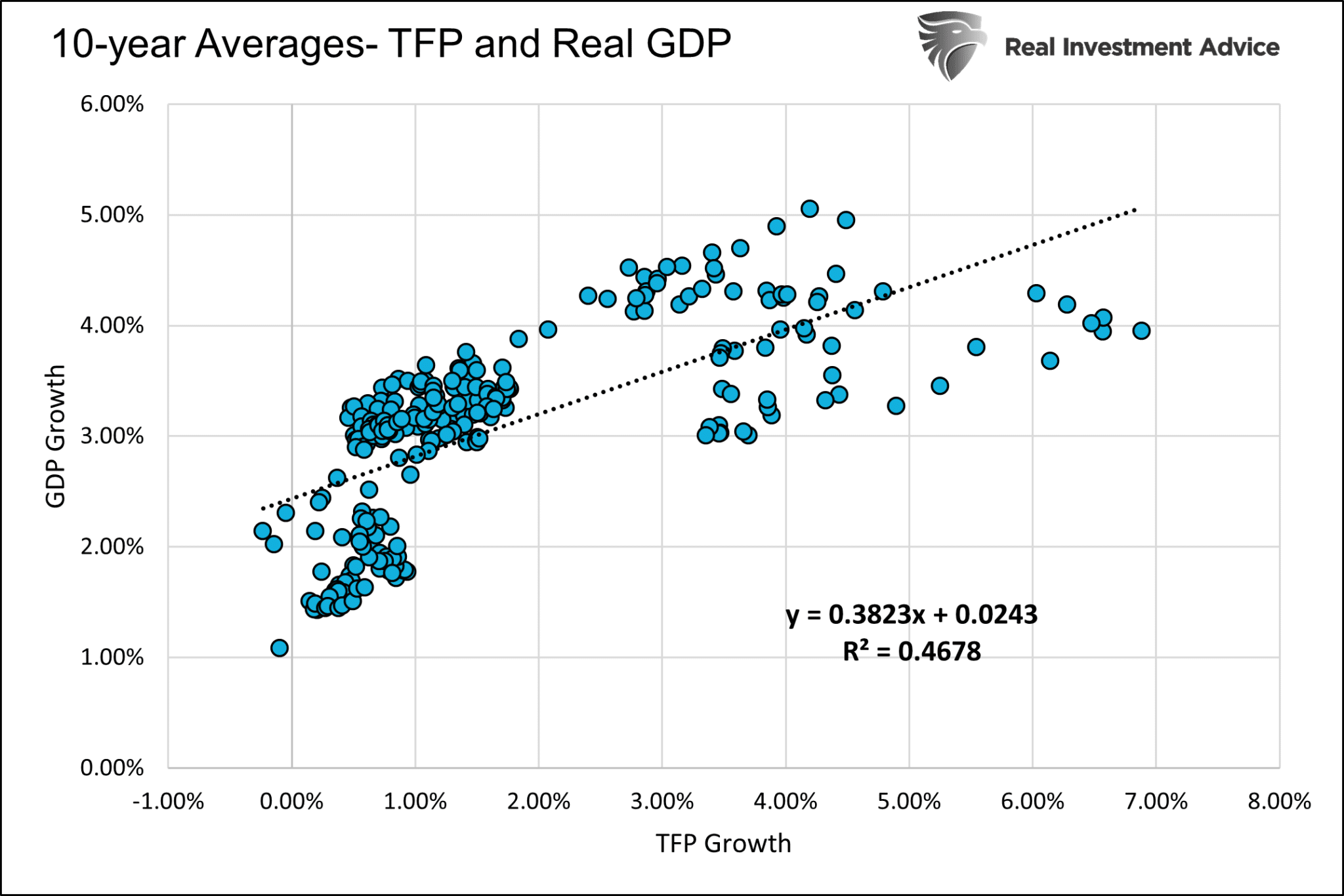

The following graph shows the strong correlation between productivity and economic growth. For every 1% decline in productivity growth, real GDP falls by .41%.

The Price of Money Drives Capitalism

Why is productivity growth and, therefore, economic growth slowing? There are many reasons, including government policies and regulations, societal behaviors, demographics, and geopolitics, to name a few. Our focus is on the gasoline of the capitalism engine, the price of money, or interest rates.

Those investing capital are incentivized to earn the most they can for their investment. Therefore, they should want to invest in the most productive ventures.

Money, via wages, incentivizes people to work hard and maximize their earnings potential.

Why, then, is money not providing the proper incentives?

In 2008, President George Bush went on CNN and provided a clue.

I’ve abandoned free-market principles to save the free-market system.

George Bush is one of many recent leaders from both sides of the aisle that ignore free-market principles for what they believe is for the greater good.

Letting the Fed manipulate the price of money versus letting the market determine the price of money was a systematic way to achieve the “greater good.” In some instances, the price of money was compromised to bail out those taking on too much leverage. In other cases, it was used to prop up economic growth to win elections. Sometimes it was for wars to flex our geo-political muscles.

Whether you agree with the politics of such actions or not, counteracting free market principles removes the profit incentives that drive labor and production. Worse, the consistent non-capitalistic reaction to “crisis” creates a circular problem. The further we stray from capitalism, the more government interference is needed to hide economic ills.

Interest Rates Drive Investment

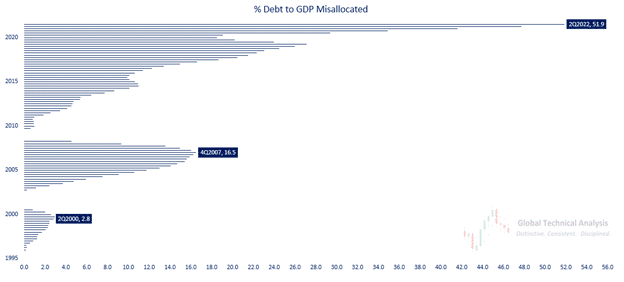

Lower than natural interest rates result in unproductive debt.

On the other hand, if market rates of interest are held abnormally below the natural rate, then capital allocation decisions are not made based on marginal efficiency but according to the average return on invested capital. This explains why, in those periods, more speculative assets such as stocks and real estate boom.”

The graph below from Brett Freeze highlights that the percentage of debt allocated to unproductive investments flourishes during periods when the Fed pushed interest rates below market levels.

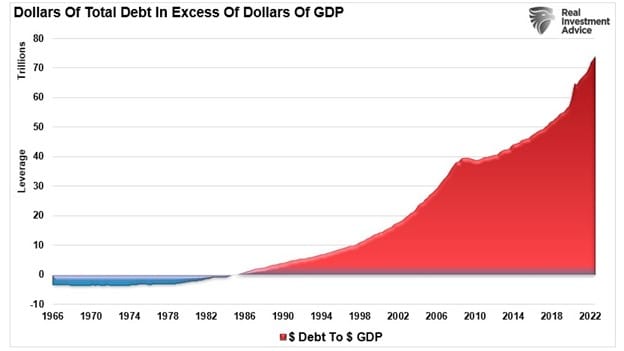

The following graph shows total debt outstanding has risen significantly greater than GDP. If the debt were used for productive purposes, GDP would have increased even more than the debt.

Rinse, Wash, Repeat

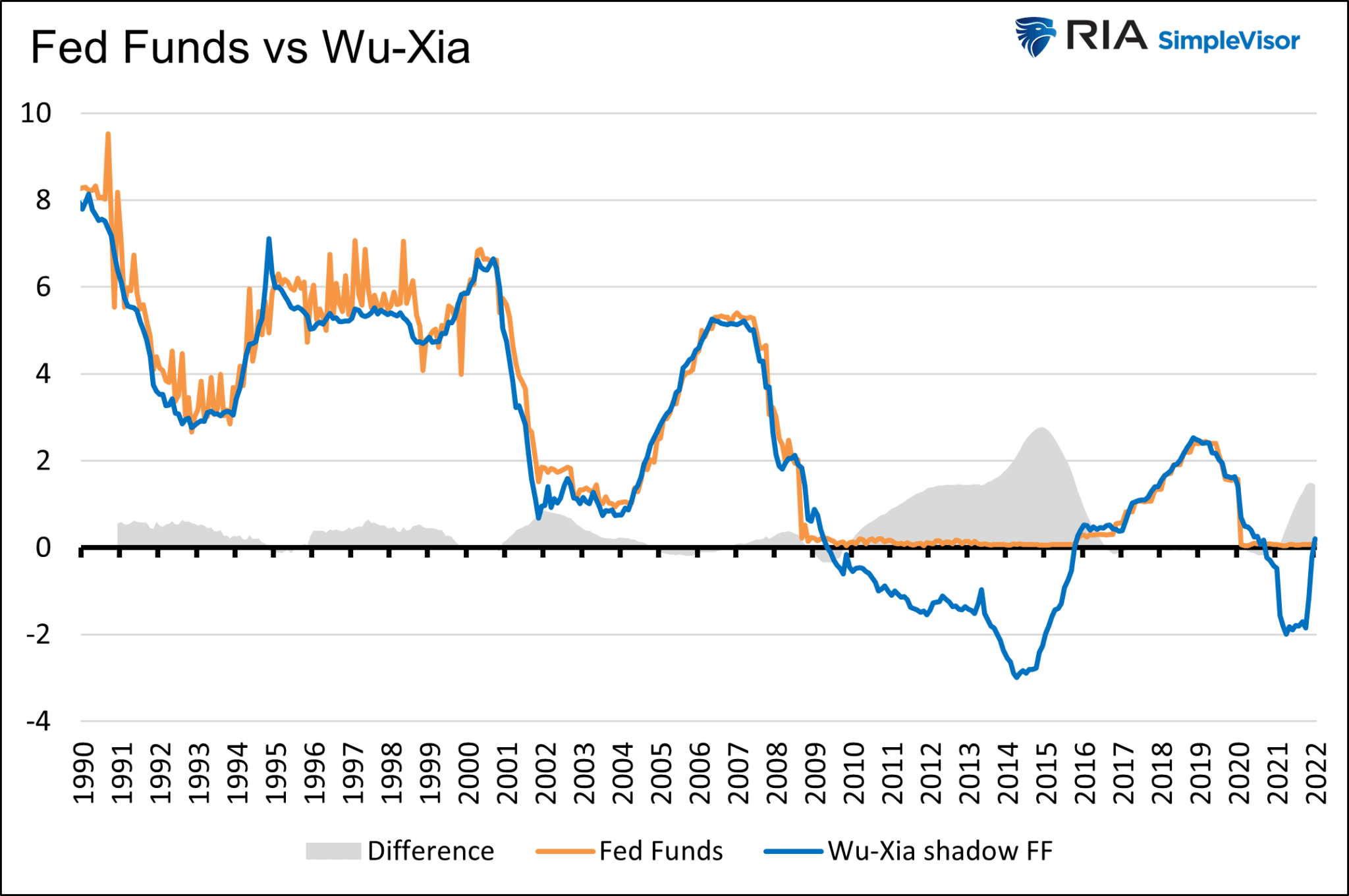

Let’s revisit the monetary policy in the aftermath of the financial crisis. The graph below charts the Fed Funds Rate versus a proxy rate developed by Fed researchers Jing Wu and Fan Xia. The proxy rate quantifies a truer Fed Funds rate incorporating Fed Funds and QE. As it shows, the Wu-Xia rate ranged from negative one to negative three percent from 2009 to 2015.

The Fed was effectively employing negative interest rates. While such a policy may have helped speed up the recovery, it led to greater leverage, additional unproductive debt, and more significant financial imbalances. For example:

Corporations use cheap funding to buy back stock. The rationale is to reduce the share count, which boosts the earnings per share. Unfortunately, the money they spend promoting share prices is not going toward productive ventures.

Government debt as a percentage of GDP is up two-fold since 2007. Almost all government spending is unproductive. Simply, it does not create income in which to pay it back. Therefore, the government must issue more debt to pay back interest and maturing debt. To fund deficits, the government relies on the economy’s investable dollars. Those ever-increasing investable dollars that must fund the Treasury cannot fund productive investments.

In the latter half of 2020 and most of 2021, when the Wu-Xia real Fed Funds rate was negative, rampant speculation was occurring in the riskiest asset classes. SPACs and cryptocurrency were all the rage. The bored ape yacht club #8817 (digital NFT) sold for $3.4 million. Indeed there is a more productive use of $3.4 million!

Summary

Nothing is free. Every time the Fed lowers rates to boost the economy or prop up stock prices, there is a future price to pay. Repeatedly manipulating the price of capital results in weaker productivity growth and ultimately reduced economic activity. Ultimately it is the citizens that pay the price.

Adapting free market principles does not guarantee a utopia. But over time, it provides the economy and its operators the best chance to be as productive as possible. Letting markets decide the price of money based on the economic environment will produce better outcomes than twelve bankers, with little real-world experience, determining the price of money.