Editor’s note: we are publishing a short issue early, in advance of the upcoming holidays. For those of you celebrating this month, have a wonderful holiday season!

As we head into the winter break, hopes of calmly winding down for the year have been dashed by the last major central bank decision of the year.

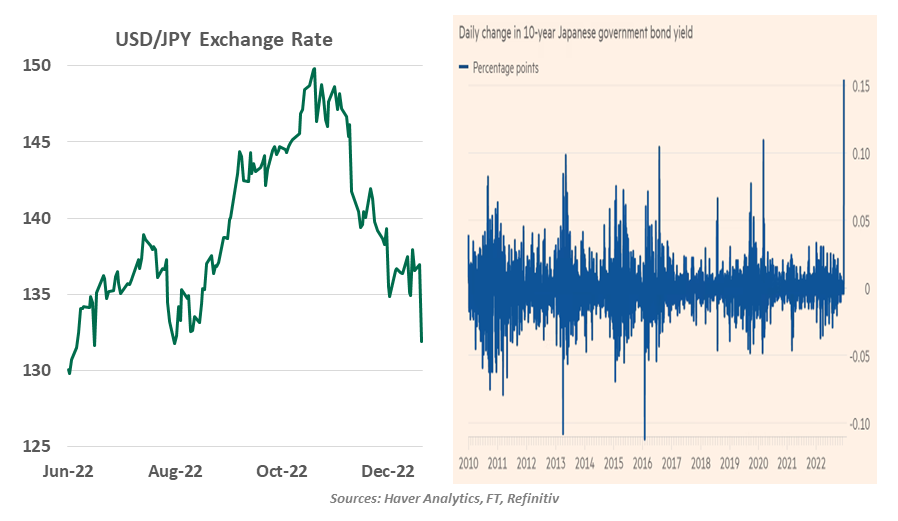

This week’s Bank of Japan (BoJ) monetary policy meeting was widely expected to be a dull event, like most of its sessions in recent times. The BoJ had bucked this year’s global trend of hiking rates and cutting asset purchases, and wasn’t expected to change course this month. However, the BoJ stunned markets by expanding the tolerance band used for yield curve control (YCC). The 10-year Japanese government bond (JGB) yield will now be allowed to trade in a range of +/-0.50%, up from +/-0.25%.

In the past, BoJ Governor Haruhiko Kuroda has indicated that any adjustments to the YCC policy would effectively amount to an interest rate increase. As a result, the move was seen by markets as a long-awaited pivot by the central bank. This triggered wild swings in bond, equity and currency markets. The yen soared 4% against the dollar, yields on 10-year JGBs increased 16 basis points and the Nikkei 225 stock index was down 2% on Tuesday. The ripple effects were felt far beyond Tokyo. U.S. Treasury yields climbed, and equities slumped.

|

Inflation dynamics in Japan will keep explicit rate hikes off the table in 2023. |

As emphasized by Governor Kuroda at this month’s meeting, the move is aimed at enhancing the sustainability and effectiveness of YCC, in addition to easing pressure on the yen. It also takes the pressure off Mr. Kuroda’s successor to change the policy stance after his term ends in April 2023. In our view, though, this should not be viewed as the beginning of tighter of monetary policy. Japanese inflation has increased in recent months, but is expected to fall below the 2% target by the end of 2023, led by a host of factors such as energy subsidies, lack of sustained wage pressures and weak demand.