I think one of the better ways to invest for the long-term is to latch onto trends in a region and, in Asia, one of the long-term trends that we see is innovation. We believe focusing on innovation is a better approach to finding growth companies in this region. I'd like to explain how we think about innovation. Most people associate innovation with breakthrough products, but we’ve broadened that concept to include companies that are implementing new ideas to build great businesses in Asia. So, that includes companies that are building products and services to create new markets or gain market share within existing industries, and it also includes companies that are using innovative strategies to build entry barriers and sustainable competitive advantages.

Innovation is more than Technology

I think it's important to emphasize that we look for innovative companies across all industries and sectors, not just in one or two specific sectors. We believe that innovation comes in different shapes and forms, it could be either disruptive or sometimes incremental. For example, companies like Alibaba or Didi are very disruptive, they’ve completely changed how we shop or use transportation. On the other hand, companies like Samsung and TSMC are more incremental; every year they make incremental changes to their existing products, but they're still successful and very profitable.1 We also believe that innovation happens across all levels of corporate structure, so we look at products and services, and we also look for innovations in strategy, marketing, how they manage their customer relationships and supply chains as well.

Asia: a Favorable Environment for Innovation

The next question is why Asia? Why do we believe that focusing on innovative companies is the right way to approach Asia? I believe that structural growth drivers are changing in Asia. Over the last 20 years, the main growth drivers have been simple: labor and capital inputs. During that time, opportunities were created in industries such as commodities, steels, and chemicals, and everyday consumer products like toothpaste, shampoo, instant noodles, among other very simple things. However, as regional income reached around $8,000 to $10,000 per capita2—which I see as an inflection point—we're beginning to see a shift in the economy and opportunities developing in more sophisticated industries such as automation, entertainment, healthcare, industries that are more services oriented. Opportunities emerging from these trends tend to last anywhere between three to five years, sometimes 20 years, providing great long-term investment opportunities.

Another reason to look at innovative companies in the region is the tremendous rise in worth over the past 20 years and the size of the market. With rising income, Asia has become the biggest market today, not just by volume, but in terms of spending power as well.

Chart 1:

Bubble Size = middle class population (millions); 2020 and 2030 data points are projections

*PPP=Purchasing Power Parity

Purchasing Power Parity is a rate that attempts to equalize the purchasing powers of differing currencies and pricing levels among countries.

There is no guarantee any estimates or projections will be realized.

Source: Homi Kharas, 2017, The Unprecedented Expansion of the Global Middle Class: An Update

If you look at Chart 1, by 2030, Asia is expected to be bigger than the US and Europe combined. Think about that, that's a huge market opportunity, and this is creating opportunities for companies with innovative products and services that Asian consumers want to buy. Consider Korean cosmetics companies, they've created innovative products that cater to Asian consumers, which are original inventions, not copycats. For example, they have products using ingredients that are well known to Asian consumers like ginseng, and they were the first ones to create products like BB cream or cushion products. Now global companies are copying these products to compete in Asia.

For a long time, these types of companies didn't create much value because the addressable market was quite small and limited, just Korea and Japan. But with the emergence of Chinese middle class, the addressable market becomes much larger—huge. The Chinese middle class, who couldn't afford to buy these products 10, 15 years ago, are now becoming their biggest customers.

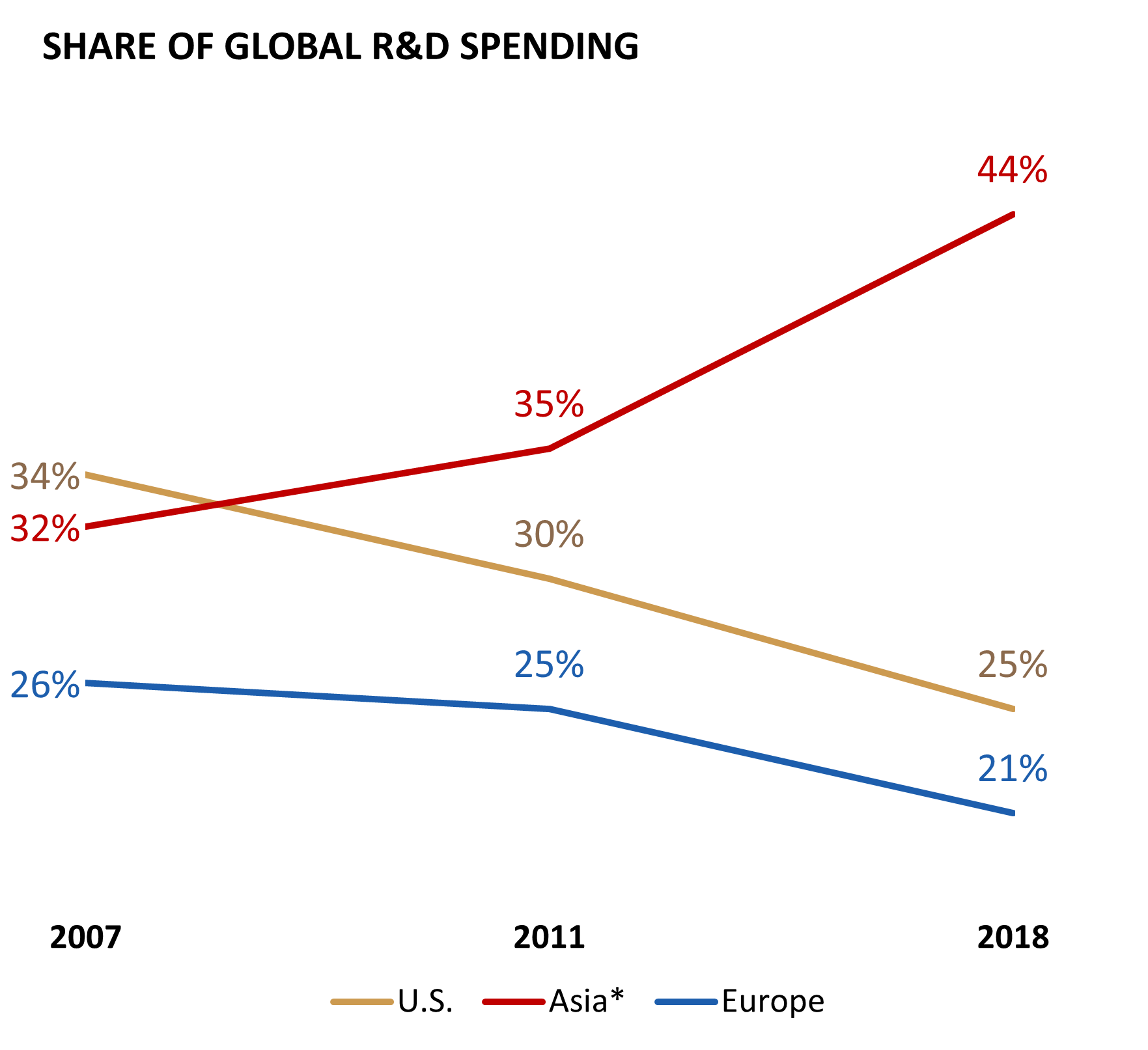

Chart 2:

|

|

|

Source: Global R&D Funding Forecast Dec 2018, Dec 2012; Businessswire 2009, Patent Application from World Intellectual Property Organization (WIPO) Database, December 2020.

*Asia includes East, Southeast and South Asia; 2018 data points are projections

There is no guarantee any estimates or projections will be realized.

|

Companies in Asia are also recognizing this trend, and they're increasingly spending more on research and development (R&D). Innovation today is creating change, which may provide opportunities to create value in Asia, and that's motivating many companies to invest more, which leads to bigger revenues and profits, followed by even bigger R&D budgets. This cycle is feeding itself and propelling Asia to be the biggest R&D spender, outspending both the US and Europe, as you can see in Chart 2. This focus on R&D and innovation is feeding tremendous appetite for entrepreneurship in Asia as well. For example, we have around 400-plus unicorns in the world as of November 20223, and there are as many unicorns in Asia as there are in the US. Five out of the top 10 biggest unicorns are based in Asia. That's an amazing achievement for entrepreneurs in Asia where the ‘startup’ concept was very foreign only 10, 15 years ago.

As of 12/14/2022, accounts managed by Matthews Asia portfolios held positions in Samsung and Taiwan Semiconductor Manufacturing Co., LTD. (TSMC).

1Samsung Electronics reported an operating profit of approximately 8.2 billion US dollars in Q3 2022. Statista.com

2Per Capita income reached $8,000 (USD) in China in 2015. Source: The World Bank

3CB Insights

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Investing in small- and mid-size companies is more risky and volatile than investing in large companies as they may be more volatile and less liquid than larger companies. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia

Read more commentaries by Matthews Asia