The worst impasse over the U.S. federal debt ceiling occurred twelve years ago. Worries escalated in markets and Capitol corridors until an accord was reached at the 11th hour, narrowly avoiding a default by the U.S. Treasury. Disappointed by Congressional dysfunction, Standard and Poor’s downgraded U.S. federal debt on August 5, 2011.

That episode has proven very costly for the American public, in a number of ways. So it is an understatement to say that the prospect of going through another debt ceiling debacle is not an exciting one. Nonetheless, discussions I had in Washington this week suggest that we are headed back to the brink.

At the outset, it is important to acknowledge that America’s finances are not in the best condition. As we discussed here, pandemic programs (however necessary) added substantially to the national debt, which was on an unsustainable trajectory in the first place. We warned that pending increases in interest rates would make the situation even less comfortable, as debt service payments are absorbing a growing share of Federal revenues.

We’ve written about the debt ceiling on a number of occasions, most recently here. The United States is the only country that has this feature; others view the issuance of debt as a mathematical byproduct of the spending and tax measures passed by legislatures. Supporters of the ceiling say it creates opportunities for important discussion of government expenditures. Detractors note that little has been produced by debt ceiling debates, other than impressions that the United States cannot get its fiscal house in order.

As we anticipated when we analyzed the 2022 election results, the debt ceiling looked to be one of the few levers that the House of Representatives could pull to affect federal spending. The balloting that ultimately elected Kevin McCarthy as the Speaker of the House hinged on a small group of budget hawks, who extracted a stiff price for their support: a pledge to include steep cuts in outlays as part of any agreement to raise the debt limit.

The American government reached its borrowing limit this week. That initiated a series of maneuvers that are known as “extraordinary measures.” The major components are suspensions of reinvestment in certain government funds, which would be restored when new debt can finally be issued. Fortunately for the Treasury, we are also heading into the interval where monthly tax receipts exceed expenditures, which reduces the need to borrow.

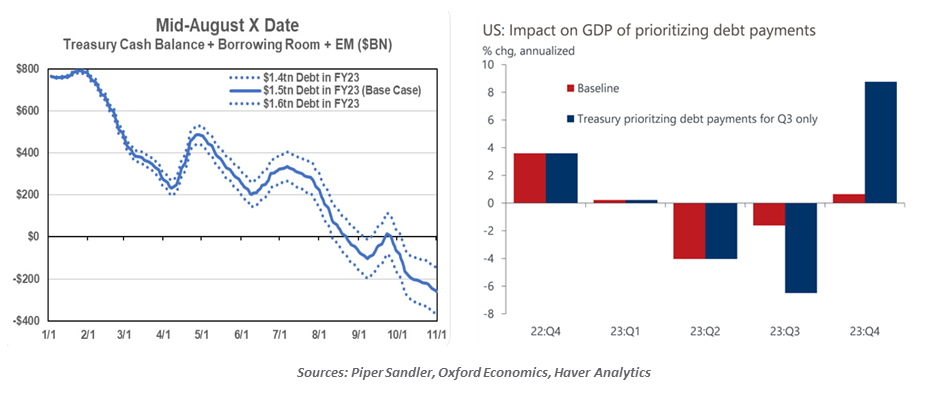

The reservoir of extraordinary measures is estimated to be about $400 billion. Based on projections of federal cash flows, this should tide the Treasury through to the middle of the summer. After passing the “X date,” however, prioritization of government payments will be necessary if the debt ceiling has not been changed. The tradeoff between paying civilians and paying bondholders will be very difficult to reconcile.

Any delay in federal transfers and/or a government shutdown would have an immediate and substantial impact on U.S. economic growth. If we have managed to avoid a recession through the middle of the year, the consequences of Congressional inaction would be enough to tip the economy over. Concerns over deferred interest payments on Treasury securities (which would create a “technical default”) are already creating dislocations in the bond market. These will become more acute as the debt ceiling drop-dead date approaches.

A risky debt ceiling impasse later this year is almost a certainty.

Uncertainty over the solvency of the U.S. government increases the cost of borrowing in both the short and long term. And it is entirely possible that ratings agencies observing the dynamic will review the Treasury’s debt rating. A downgrade would further add to borrowing costs.

Some in Washington that I met this week noted that those costs might be worth it, if the showdown results in stronger spending discipline. If realized, cost cuts could trim the deficit and limit interest expenses. But few think that this outcome is possible. Compromise seems unlikely, as both sides feel as if they are scoring political points by holding out.

After the debt ceiling was raised in August of 2011, I decamped from the nation’s capital (where I was working for the Federal Reserve) to enjoy a week away with my family. The reverie was short-lived; the debt downgrade followed me into the wilderness. It is looking increasingly likely that my summer plans will be spoiled again this year.

© Northern Trust

Read more commentaries by Northern Trust