Global Economic Outlook: Run-of-the-Mill

2023 will be a tough year for growth, everywhere in the world. The U.S. economy is poised to continue its expansion, albeit at a snail’s pace. Europe will do well to fend off a deep recession. With the engines of growth struggling to match recent horsepower, suppliers in Asia aren’t going to fare well either.

Prices will moderate as commodity prices ease and supply chains heal, but inflation will take time to reenter central bankers’ comfort zones. The fight to bring inflation closer to target levels will require raising rates through this spring and keeping them elevated during the remainder of the year. Modest increases in unemployment are expected across most developed markets.

Unresolved issues like the U.S. debt ceiling and the Ukraine war, coupled with reopening disruptions in China, have the potential to add volatility to the world economy.

Here are perspectives on how major economies are poised to perform in 2023.

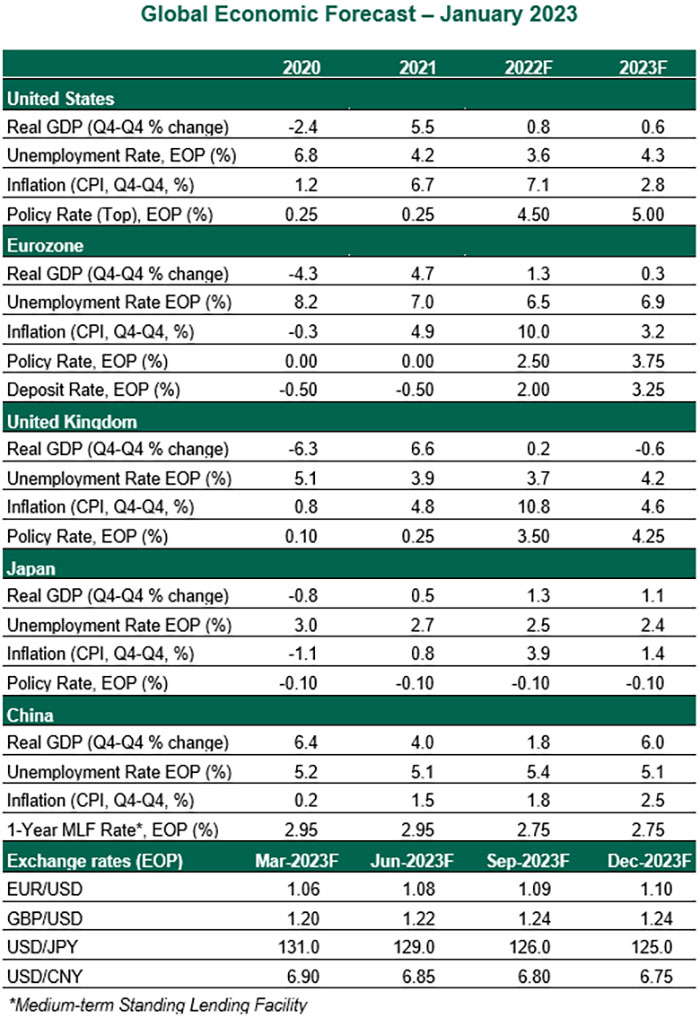

United States

- The December consumer price index report delivered further evidence of inflation cooling from its 2022 highs. Excluding the volatile food and energy sectors, price growth measured 5.7% year over year in December—an improvement, but still too high for comfort. From a policy perspective, the Fed needs to see the core measure move steadily lower. Recent softer readings have supported the case for smaller rate hikes of 25 basis points each at the February and March meetings.

- Lower inflation will also be crucial in heading off a recession. Nominal growth is poised to slow this year after a period of post-pandemic rebound. Decelerating inflation will reduce the drag on both household incomes and real gross domestic product, helping avoid a downturn.

Eurozone

- The eurozone economy has shown remarkable resiliency amid hardships. With the risk of gas rationing almost ruled out for this winter, thanks to warmer temperatures, survey and sentiment indicators are improving. This implies that the downturn may not be as bad as feared a few months ago; however, several challenges remain. Households’ purchasing power has been squeezed by high inflation. External demand is looking weak. The bloc still faces the task of refilling its gas storage before next winter, with flows from Russia unlikely to resume.

- There are signs that inflation may have finally peaked in the eurozone, as the pace of price increases fell from 10.1% in November to 9.2% year over year in December. The drop has been largely driven by weaker energy prices, rather than moderation in core inflation. This will lead the European Central Bank to tighten policy aggressively through midyear; a short and shallow contraction will not alter their course.

United Kingdom

- A fiscal policy pivot by the new leadership has stabilized financial markets, but the British economy is a long way from stability. The U.K. is facing a shallow recession triggered by falling real household incomes and tight policy. The recent drop in energy prices coupled with large negative base effects will come into play, contributing to lower headline readings. However, still-tight labor markets and upward pressure on wages will keep core inflation elevated through the year.

- The British housing market entered a downturn late last year which is set to deepen further. Mortgage rates are far higher than they were at the start of 2022. More than 750,000 British households are at risk of mortgage default in the next two years. A spillover from housing to the broader economy cannot be ruled out entirely. The Bank of England is expected to raise its interest rates by a total of 75 basis points at its next two meetings, before pausing to assess the outlook.

Japan

- Pent up demand coupled with easing supply chain frictions will continue to underpin activity in Japan during the first half of the year. However, the unfavorable external economic backdrop will drag the performance of the export sector down. Inflation has returned to Japan, but likely temporarily, given the lack of sustained wage gains.

- The Bank of Japan (BoJ) made no policy changes at this month’s meeting. Nonetheless, the December tweak to the Yield Curve Control framework has heightened speculation over policy normalization. With inflation likely to fall below 2%, the BoJ will maintain current policy rates even after Governor Kuroda's term ends in April 2023. Persistent pressure on the yield curve, however, could force the central bank to widen the tolerance corridor further.

China

- The growth rate of China’s economy slowed to less than 3% in the fourth quarter, supporting the case for relaxing the costly zero-COVID policy. However, a normalization in economic activity will take some time. While domestic demand may recover quickly once the current outbreak recedes, exports face headwinds from weaker backdrop.

- The struggle for the Chinese economy lies beyond COVID. The path of its highly leveraged property sector recovery is uncertain. A profound demographic shift is underway, with the population declining for the first time in six decades. This will weigh on labor force growth and productivity.