After months of troubling news on inflation, the tide seems to have turned. Increases in the broad price indexes are easing, and the outlook for important components is more constructive. Energy costs have dropped, and supply chains have healed. Monetary and fiscal policy are working together to bring supply and demand into closer alignment.

One area where inflation continues to concern central bankers is services. Output in developed economies is dominated by services; in the United States, for example, they account for well over 70% of gross domestic product (GDP). The key ingredient in the provision of services is labor, which has been in short supply. In these areas, rising wages could continue to pressure prices.

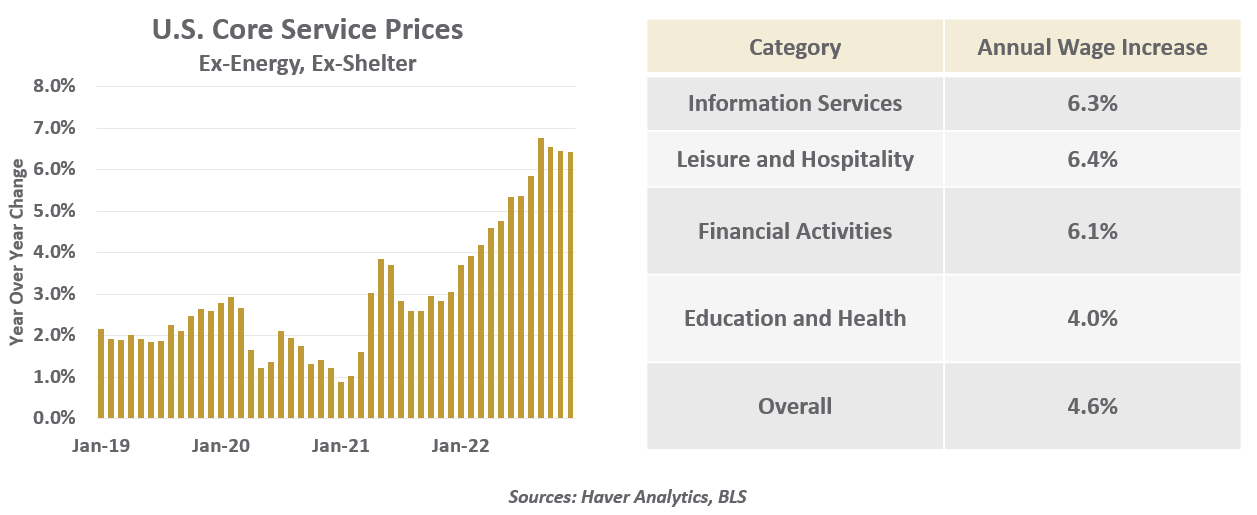

The Federal Reserve has placed particular focus on what it calls “core services,” which exclude housing and energy-related categories. Prices for this collection have escalated by more than 6% over the past twelve months, and have barely tapered from their peaks. Associated with that, wages in some key service sectors are rising by more than they are for the labor force as a whole.

The prices of services will likely moderate in the months ahead.

There is, however, reason for optimism. Travel costs like airfares, hotel rates and car rentals are all moderating or retreating. Demand has eased; families sought to enjoy their first post-pandemic vacations and holidays, but are expected to be a bit more conservative going forward. For that reason, pricing power has diminished, breaking the link with wages. Further, immigration to the United States has returned to its pre-pandemic pace. Newcomers often take jobs in basic services like home health care and hospitality; pay increases in these industries have moderated.