Brazil and Argentina recently announced their intention to create a new common currency, to be called the sur. The plan seeks to create a new value unit that facilitates trade between the two regional heavyweights, reducing dependence on the U.S. dollar. The idea has faced criticism from all quarters, and rightly so.

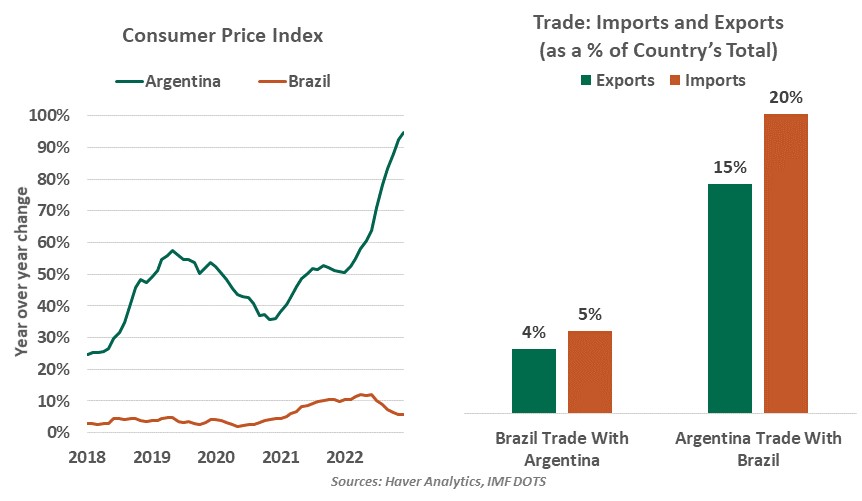

Brazilian and Argentinian economic cycles and policies diverge significantly. The former has a floating exchange rate and an independent central bank. On the other hand, the Argentinian peso is not a free-floating currency. The country has capital controls, and neither its government nor its corporations have access to international money markets. Argentina’s history of defaults and lack of a sound economic plan have spurred hyper-inflation. In Brazil, inflation has cooled to below 6%. As a result, policy rates in the two countries are a massive 61 percentage points apart.

The creation of the new currency would require a settlements bank to be capitalized in both hard and common currencies by the two economies. Brazil is a creditor to the world financial system with ample foreign exchange reserves (over $300 billion) for its share of the capitalization. By contrast, Argentina is facing a balance of payments and currency crisis: the country is struggling to repay its bondholders and fund its imports. It already owes more than $70 billion to the International Monetary Fund. Under circumstances like these, Brazil will likely be the one bailing out its struggling partner to prevent a collapse of the joint currency.

The benefits of a joint currency are obvious for Argentina, not so much for Brazil.