The credit hype machine is going to break

According to Bloomberg, January was a record month for investment grade (IG) corporate bond ETF flows as the credit hype machine went into overdrive. As a result, the amount investors are being compensated for the additional risk relative to US Treasury bonds (known as credit spreads) has declined rapidly. From a credit manager’s perspective, we understand the appeal. At 5% yield, IG bond yields are now the highest since the Global Financial Crisis, making them unlikely to result in negative returns outside of a substantial recessionary scenario. With many IG companies having extended debt maturities at low fixed interest rates, overall leverage and interest coverage metrics for the market are arguably among the best they’ve been at this point in a cycle. Most IG managers are limited to investing in corporate debt, and the significant cash flows generated by these bonds create a substantial reinvestment back into the market.

But therein lies the rub: the rest of us are not limited to looking at this narrow market segment on a standalone basis. We can choose to underweight IG because better alternatives exist elsewhere or because we feel the risk/return is not compelling. That choice is what separates a style box manager from a tactical multi-asset manager.

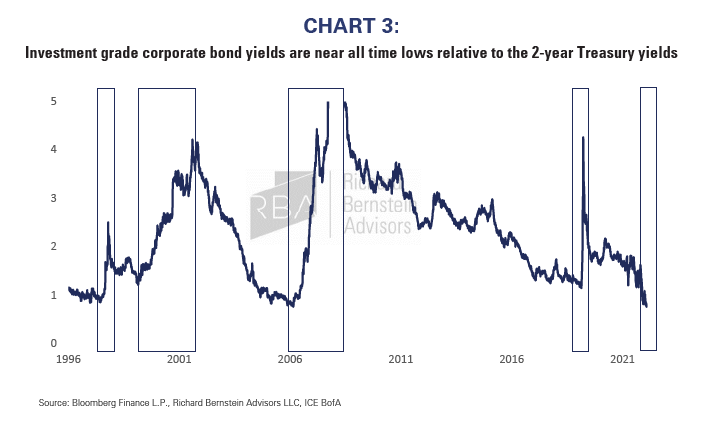

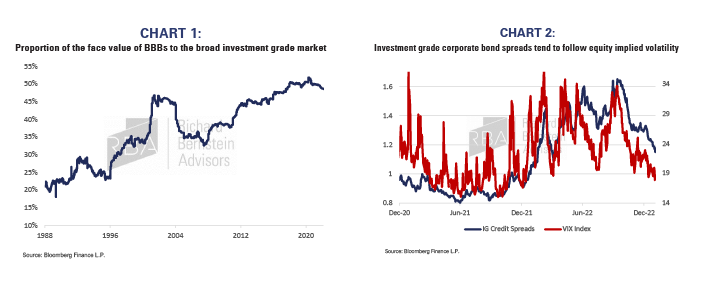

Low quality credit simply does not perform well during earnings recessions and the investment grade market’s weight in BBB-rated bonds (the lowest quality IG rating) is near a record high at 50%. Investors appear to be focused solely on the above-mentioned health of the market and seem to have forgotten about downgrade risk (due to an earnings recession), liquidity risk, and most importantly, volatility. Corporate bond investors hate volatility; they want the certainty of earning their coupon and the ultimate payment of principle. A good gauge of this risk is equity option volatility as proxied by the VIX Index*. Should equity volatility spike, credit spreads will likely widen.

*Cboe Global Markets revolutionized investing with the creation of the Cboe Volatility Index® (VIX® Index), the first benchmark index to measure the market’s expectation of future volatility. The VIX Index is based on options of the S&P 500® Index, considered the leading indicator of the broad U.S. stock market. The VIX Index is recognized as the world’s premier gauge of U.S. equity market volatility.